Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Kidney Diet DelightsДокумент20 страницKidney Diet DelightsArturo Treviño MedinaОценок пока нет

- 4:30:21 PaystubДокумент1 страница4:30:21 PaystubRhoderlande JosephОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- ASTM C-1116 - 03 - Standard Specification For Fiber-Reinforced Concrete and ShotcreteДокумент8 страницASTM C-1116 - 03 - Standard Specification For Fiber-Reinforced Concrete and ShotcretemordeauxОценок пока нет

- 17-QA-QC ManualДокумент34 страницы17-QA-QC ManualAbdul Gaffar100% (3)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Draw-Through or Blow-Through: Components of Air Handling UnitДокумент23 страницыDraw-Through or Blow-Through: Components of Air Handling Unityousuff0% (1)

- Boost Listening 1 Teacher S Edition PDFДокумент96 страницBoost Listening 1 Teacher S Edition PDFHuy Lê QuangОценок пока нет

- Biological ClassificationДокумент21 страницаBiological ClassificationdeviОценок пока нет

- Excavation PermitДокумент2 страницыExcavation PermitRajesh Kumar SinghОценок пока нет

- Tips To Diagnose & Address Common Horse AilmentsДокумент6 страницTips To Diagnose & Address Common Horse AilmentsMark GebhardОценок пока нет

- Chapter 2 - Alkanes PDFДокумент54 страницыChapter 2 - Alkanes PDFSITI NUR ALISSA BINTI AHMAD RASMANОценок пока нет

- KBF (E5.2) : Service ManualДокумент140 страницKBF (E5.2) : Service ManualgeorgevarsasОценок пока нет

- PCC 2 What Is PCC 2 and Article of Leak Box On Stream RepairGregДокумент12 страницPCC 2 What Is PCC 2 and Article of Leak Box On Stream RepairGregArif Nur AzizОценок пока нет

- Info-Delict-Violencia Contra Las Mujeres - Dic22Документ181 страницаInfo-Delict-Violencia Contra Las Mujeres - Dic22LPF / SKOUL BASQUETBOLОценок пока нет

- 200 State Council Members 2010Документ21 страница200 State Council Members 2010madhu kanna100% (1)

- Solvents: Northwest EuropeДокумент7 страницSolvents: Northwest EuropegeorgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 14.02.15 PDFДокумент19 страницAthenian Shipbrokers - Monthy Report - 14.02.15 PDFgeorgevarsasОценок пока нет

- Solvents: Northwest EuropeДокумент9 страницSolvents: Northwest EuropegeorgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 14.01.15 PDFДокумент18 страницAthenian Shipbrokers - Monthy Report - 14.01.15 PDFgeorgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 13.11.15 PDFДокумент20 страницAthenian Shipbrokers - Monthy Report - 13.11.15 PDFgeorgevarsas0% (1)

- Athenian Shipbrokers - Monthy Report - 13.12.15 PDFДокумент18 страницAthenian Shipbrokers - Monthy Report - 13.12.15 PDFgeorgevarsasОценок пока нет

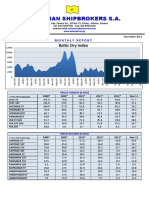

- Athenian Shipbrokers S.A.: Baltic Dry IndexДокумент17 страницAthenian Shipbrokers S.A.: Baltic Dry IndexgeorgevarsasОценок пока нет

- C H S&P W B: Larkson Ellas Eekly UlletinДокумент2 страницыC H S&P W B: Larkson Ellas Eekly UlletingeorgevarsasОценок пока нет

- C H S&P W B: Larkson Ellas Eekly UlletinДокумент2 страницыC H S&P W B: Larkson Ellas Eekly UlletingeorgevarsasОценок пока нет

- C H S&P W B: Larkson Ellas Eekly UlletinДокумент2 страницыC H S&P W B: Larkson Ellas Eekly UlletingeorgevarsasОценок пока нет

- C H S&P W B: Larkson Ellas Eekly UlletinДокумент3 страницыC H S&P W B: Larkson Ellas Eekly UlletingeorgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 14.08.15Документ17 страницAthenian Shipbrokers - Monthy Report - 14.08.15georgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 14.07.15 PDFДокумент18 страницAthenian Shipbrokers - Monthy Report - 14.07.15 PDFgeorgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 13.11.15 PDFДокумент20 страницAthenian Shipbrokers - Monthy Report - 13.11.15 PDFgeorgevarsas0% (1)

- Advanced - Week 12 - 16.03.18 PDFДокумент10 страницAdvanced - Week 12 - 16.03.18 PDFgeorgevarsasОценок пока нет

- Advanced - Week 52 - 16.12.26 PDFДокумент9 страницAdvanced - Week 52 - 16.12.26 PDFgeorgevarsasОценок пока нет

- Advanced - Week 24 - 16.06.10Документ11 страницAdvanced - Week 24 - 16.06.10georgevarsasОценок пока нет

- Advanced - Week 23 - 16.06.03 PDFДокумент11 страницAdvanced - Week 23 - 16.06.03 PDFgeorgevarsasОценок пока нет

- Incorporating Developmental Screening and Surveillance of Young Children in Office PracticeДокумент9 страницIncorporating Developmental Screening and Surveillance of Young Children in Office PracticeakshayajainaОценок пока нет

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruДокумент1 страницаIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDrsex DrsexОценок пока нет

- Fischer General-CatalogueДокумент108 страницFischer General-Cataloguebo cephusОценок пока нет

- Real Time EvaluationДокумент3 страницыReal Time Evaluationأيوب علاءОценок пока нет

- Evaluation and Comparison of Highly Soluble Sodium Stearyl Fumarate With Other Lubricants in VitroДокумент8 страницEvaluation and Comparison of Highly Soluble Sodium Stearyl Fumarate With Other Lubricants in VitroSvirskaitė LaurynaОценок пока нет

- Solar Grass Cutter MachДокумент21 страницаSolar Grass Cutter MachAnonymous I13s99Оценок пока нет

- Decide If Surrogacy Is The Right ChoiceДокумент13 страницDecide If Surrogacy Is The Right ChoiceSheen CatayongОценок пока нет

- FACSДокумент8 страницFACSKarthick ThiyagarajanОценок пока нет

- 9ha Power PlantsДокумент2 страницы9ha Power PlantsGaurav DuttaОценок пока нет

- 7-13-1996 Joel Nance MDДокумент3 страницы7-13-1996 Joel Nance MDAnother AnonymomsОценок пока нет

- Nama Anggota: Dede Wiyanto Endri Murni Hati Rukhi Hasibah Tugas: Bahasa Inggris (Narrative Text)Документ3 страницыNama Anggota: Dede Wiyanto Endri Murni Hati Rukhi Hasibah Tugas: Bahasa Inggris (Narrative Text)Wiyan Alwaysfans CheLseaОценок пока нет

- Decompensated Congestive Cardiac Failure Secondary To No1Документ4 страницыDecompensated Congestive Cardiac Failure Secondary To No1Qi YingОценок пока нет

- Eliasmith2012-Large-scale Model of The BrainДокумент5 страницEliasmith2012-Large-scale Model of The Brainiulia andreeaОценок пока нет

- Research Methods - Print - QuizizzДокумент5 страницResearch Methods - Print - QuizizzpecmbaОценок пока нет

- Publication Edition 2020Документ230 страницPublication Edition 2020Mech Dept GMITОценок пока нет

- CV TemplateДокумент5 страницCV TemplateLopezDistrict FarmersHospitalОценок пока нет

- Plumbing Design Calculation - North - Molino - PH1 - 5jun2017Документ5 страницPlumbing Design Calculation - North - Molino - PH1 - 5jun2017Jazent Anthony RamosОценок пока нет