Вам также может понравиться

- Preventive-Detective-Corrective Internal Control ModelДокумент1 страницаPreventive-Detective-Corrective Internal Control Modelsibudit100% (1)

- Audit of The Financing and Investing Cycle ReportДокумент20 страницAudit of The Financing and Investing Cycle ReportCyrell S. SaligОценок пока нет

- Chapter 10Документ6 страницChapter 10Melissa Kayla ManiulitОценок пока нет

- Keme Keme Kemeeee VMДокумент6 страницKeme Keme Kemeeee VMMelissa Kayla Maniulit100% (1)

- Acc 14 FinalДокумент7 страницAcc 14 FinalKiaОценок пока нет

- Chapter7Документ2 страницыChapter7Keanne ArmstrongОценок пока нет

- Input Error Correction (Accounting Information System)Документ14 страницInput Error Correction (Accounting Information System)Rachel Garcia0% (1)

- SM 07 New CHAPT 7Документ44 страницыSM 07 New CHAPT 7jelОценок пока нет

- Acctg 14 - MidtermДокумент5 страницAcctg 14 - MidtermRannah Raymundo100% (1)

- Activity 1.3 - Think Like An AuditorДокумент2 страницыActivity 1.3 - Think Like An AuditorIan Christian Alangilan BarrugaОценок пока нет

- Elleso, Kate Angel V. Acinsy DiscussionДокумент4 страницыElleso, Kate Angel V. Acinsy Discussionkateangel elleso0% (1)

- Keown Tif 20 FINALДокумент31 страницаKeown Tif 20 FINALhind alteneiji100% (1)

- Ict 2 Finals Exam Besa Bsa2aДокумент4 страницыIct 2 Finals Exam Besa Bsa2aJoyce Ann Cortez100% (1)

- Assignment 4 - Revenue CycleДокумент9 страницAssignment 4 - Revenue CycleGiselle Martinez100% (2)

- A&V Safety (A Case Study)Документ15 страницA&V Safety (A Case Study)Bryle Jay Lape100% (2)

- Chaper 1 & 2Документ22 страницыChaper 1 & 2Nisa IstafadОценок пока нет

- Assertion Based and Direct Reporting EngagementДокумент4 страницыAssertion Based and Direct Reporting EngagementFanny MainОценок пока нет

- Group 8Документ31 страницаGroup 8Jessa E. FabilaneОценок пока нет

- Bustamante, Jilian Kate A. (Activity 3)Документ4 страницыBustamante, Jilian Kate A. (Activity 3)Jilian Kate Alpapara BustamanteОценок пока нет

- The Revenue Cycle AISДокумент11 страницThe Revenue Cycle AISChrismae Monteverde SantosОценок пока нет

- Case 1.1 Enron CorporationДокумент6 страницCase 1.1 Enron CorporationZizhang Huang88% (8)

- Case 10 Relevant Facts of The CaseДокумент2 страницыCase 10 Relevant Facts of The CaseAFAD100% (2)

- Chapter 13Документ25 страницChapter 13Clarize R. Mabiog50% (2)

- Auditing Subsidiaries, Remote Operating Units and Joint VenturesДокумент56 страницAuditing Subsidiaries, Remote Operating Units and Joint VenturesRea De VeraОценок пока нет

- Matt Demko Is The Loading Dock Supervisor For A Dry Cement Packaging CompanyДокумент3 страницыMatt Demko Is The Loading Dock Supervisor For A Dry Cement Packaging CompanyShivam Arora100% (1)

- Enron Worldcom Reaction PaperДокумент2 страницыEnron Worldcom Reaction PaperKaren Yvonne R. BilonОценок пока нет

- Audit Prob InvestmentДокумент5 страницAudit Prob InvestmentANGIE BERNAL100% (1)

- Premier Sports MemorabiliaДокумент20 страницPremier Sports MemorabiliaMaia AshОценок пока нет

- Chapter 8.Документ6 страницChapter 8.Kate AlvarezОценок пока нет

- Activity 5Документ8 страницActivity 5Marielle UyОценок пока нет

- AuditingДокумент14 страницAuditingedrick LouiseОценок пока нет

- Advanced AccountingДокумент14 страницAdvanced AccountingBehbehlynn67% (3)

- LEC104-C: Debt Restructuring Problem 1: Asset Swap (IFRS Vs US GAAP)Документ1 страницаLEC104-C: Debt Restructuring Problem 1: Asset Swap (IFRS Vs US GAAP)Miles SantosОценок пока нет

- Survey Questionnaire For BSA GraduatesДокумент7 страницSurvey Questionnaire For BSA Graduateslady chase100% (1)

- Problem 8Документ5 страницProblem 8accounts 3 lifeОценок пока нет

- OpaudCh02-502E-Regunayan, M PДокумент4 страницыOpaudCh02-502E-Regunayan, M PMarco RegunayanОценок пока нет

- JelyneSRollon ACG4632-12 Week2Документ5 страницJelyneSRollon ACG4632-12 Week2Randy KuswantoОценок пока нет

- Chapter 4 SalosagcolДокумент3 страницыChapter 4 SalosagcolElvie Abulencia-BagsicОценок пока нет

- Chapter 10 SolMan Accounting For Special Transactions 1 Millan 2018Документ20 страницChapter 10 SolMan Accounting For Special Transactions 1 Millan 2018Alvin Jheii Sioco Alfonso0% (1)

- D6Документ11 страницD6lorenceabad07Оценок пока нет

- BSA35 Quiz 3Документ3 страницыBSA35 Quiz 3Raven ShadowsОценок пока нет

- Lessor Discussion U PDFДокумент4 страницыLessor Discussion U PDFadmiral spongebobОценок пока нет

- ACC 403 Final ExamДокумент5 страницACC 403 Final Examcaponegirl250% (2)

- ExpenditureДокумент10 страницExpenditurecerapyaОценок пока нет

- 3.name Three Sources of Business and Industry InformationДокумент2 страницы3.name Three Sources of Business and Industry InformationRiza Mae AlceОценок пока нет

- Biweekly 3.1 - QДокумент3 страницыBiweekly 3.1 - QVilma Tayum100% (1)

- c7 Review QuestionsДокумент5 страницc7 Review QuestionsPauline100% (1)

- Practice Problems AcctgДокумент10 страницPractice Problems AcctgRichard ColeОценок пока нет

- Hall 5e TB Ch12Документ12 страницHall 5e TB Ch12Patricia Ann GuetaОценок пока нет

- Case AnalysisOAДокумент2 страницыCase AnalysisOAJoelo De VeraОценок пока нет

- SMEs PDFДокумент56 страницSMEs PDFAlya100% (1)

- Hermosa, Rose Marie N. - Ex 5.3 - 5.4Документ5 страницHermosa, Rose Marie N. - Ex 5.3 - 5.4Rose MarieОценок пока нет

- Financial Management - Chapter 2-AKДокумент14 страницFinancial Management - Chapter 2-AKLily DaniaОценок пока нет

- Budgeting Multiple ChoiceДокумент2 страницыBudgeting Multiple ChoiceRachel Mae FajardoОценок пока нет

- Keme Chap 4Документ5 страницKeme Chap 4Melissa Kayla Maniulit100% (1)

- Chapter 13 - EXERCISEДокумент6 страницChapter 13 - EXERCISEFrancis CabasОценок пока нет

- Group 1Документ13 страницGroup 1sheardy limОценок пока нет

- Chapter 13 NavidadДокумент18 страницChapter 13 NavidadPdean DeanОценок пока нет

- HW CH 12 and 13 WK07Документ7 страницHW CH 12 and 13 WK07Sheree SandersОценок пока нет

- Reviewer On Ch. 6 7 8 AISДокумент18 страницReviewer On Ch. 6 7 8 AISYan FranciaОценок пока нет

- Personal Assignment 1 (Week 2 / Session 3) (120 Minutes) : A. Listening Skill 1 (8 Points)Документ7 страницPersonal Assignment 1 (Week 2 / Session 3) (120 Minutes) : A. Listening Skill 1 (8 Points)Mutia RamadhantyОценок пока нет

- BINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )Документ9 страницBINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )Mutia RamadhantyОценок пока нет

- Analysis TypeДокумент2 страницыAnalysis TypeMutia RamadhantyОценок пока нет

- Analysis TypeДокумент2 страницыAnalysis TypeMutia RamadhantyОценок пока нет

- Analysis TypeДокумент2 страницыAnalysis TypeMutia RamadhantyОценок пока нет

- AssuranceДокумент4 страницыAssuranceMutia RamadhantyОценок пока нет

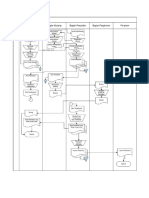

- Flowchart - Sales (Cash Receipt)Документ2 страницыFlowchart - Sales (Cash Receipt)Mutia RamadhantyОценок пока нет

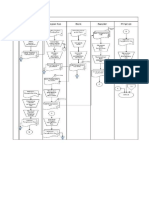

- Flowchart - WarehouseДокумент4 страницыFlowchart - WarehouseMutia RamadhantyОценок пока нет

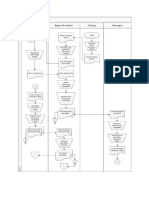

- Flowchart - Cash DishbursementДокумент1 страницаFlowchart - Cash DishbursementMutia RamadhantyОценок пока нет

- NUFLO Low Power Pre-Amplifier: SpecificationsДокумент2 страницыNUFLO Low Power Pre-Amplifier: SpecificationsJorge ParraОценок пока нет

- MSS SP 69pdfДокумент18 страницMSS SP 69pdfLaura CaballeroОценок пока нет

- 28 ESL Discussion Topics Adult StudentsДокумент14 страниц28 ESL Discussion Topics Adult StudentsniallОценок пока нет

- COSO DefinEDДокумент21 страницаCOSO DefinEDRefdy AnugrahОценок пока нет

- K To 12 Math 7 Curriculum Guide PDFДокумент15 страницK To 12 Math 7 Curriculum Guide PDFEdmar Tan Fabi100% (1)

- Volleyball Unit PlanДокумент4 страницыVolleyball Unit Planapi-214597204Оценок пока нет

- Lesson Plan Defining and Non Relative Clauses XII (I)Документ3 страницыLesson Plan Defining and Non Relative Clauses XII (I)mariaalexeli0% (1)

- Assignment Group OSHAДокумент10 страницAssignment Group OSHAariffikriismailОценок пока нет

- Accounting For A Service CompanyДокумент9 страницAccounting For A Service CompanyAnnie RapanutОценок пока нет

- UNIT 4 Digital Integrated CircuitsДокумент161 страницаUNIT 4 Digital Integrated CircuitssimhadriОценок пока нет

- 2 Beats Per Measure 3 Beats Per Measure 4 Beats Per MeasureДокумент24 страницы2 Beats Per Measure 3 Beats Per Measure 4 Beats Per MeasureArockiya StephenrajОценок пока нет

- 7273X 47 ITOW Mozart PDFДокумент3 страницы7273X 47 ITOW Mozart PDFAdrian KranjcevicОценок пока нет

- Classical Encryption TechniqueДокумент18 страницClassical Encryption TechniquetalebmuhsinОценок пока нет

- Grange Fencing Garden Products Brochure PDFДокумент44 страницыGrange Fencing Garden Products Brochure PDFDan Joleys100% (1)

- Tip Sheet March 2017Документ2 страницыTip Sheet March 2017hoangvubui4632Оценок пока нет

- Imcp - RocketbookДокумент11 страницImcp - Rocketbookapi-690398026Оценок пока нет

- Permutation, Combination & ProbabilityДокумент9 страницPermutation, Combination & ProbabilityVicky RatheeОценок пока нет

- ATA212001Документ3 страницыATA212001Tarek DeghedyОценок пока нет

- VRF Mv6R: Heat Recovery Outdoor UnitsДокумент10 страницVRF Mv6R: Heat Recovery Outdoor UnitsTony NguyenОценок пока нет

- Misc Ar2019Документ207 страницMisc Ar2019Sharon12 ArulsamyОценок пока нет

- Quizlet Table 7Документ1 страницаQuizlet Table 7JosielynОценок пока нет

- Rotc Reviewer FinalsДокумент11 страницRotc Reviewer FinalsAngel Atienza100% (1)

- Clepsydra - PesquisaДокумент2 страницыClepsydra - PesquisaJose Maria SantosОценок пока нет

- No Experience ResumeДокумент2 страницыNo Experience ResumeNatalia PantojaОценок пока нет

- Trend in Agricultural ProductivityДокумент1 страницаTrend in Agricultural ProductivityGiaОценок пока нет

- MetLife CaseДокумент4 страницыMetLife Casekatee3847Оценок пока нет

- Hotel Voucher: Itinerary ID Hotel Santika Taman Mini Indonesia IndahДокумент2 страницыHotel Voucher: Itinerary ID Hotel Santika Taman Mini Indonesia IndahSyukron PribadiОценок пока нет

- Amplificadores Automotivos PyramidДокумент13 страницAmplificadores Automotivos Pyramidedusf1000Оценок пока нет

- 064 DIR - Launching Whipping Creme & Skimmed Milk Di Channel Horeka (Subdist Masuya)Документ3 страницы064 DIR - Launching Whipping Creme & Skimmed Milk Di Channel Horeka (Subdist Masuya)indra sapta PrahardikaОценок пока нет