Вам также может понравиться

- Economic Highlights - A Slight Pick-Up in Industrial Production in August, But Economic Growth Still Trending Downward in The 3Q - 11/10/2010Документ3 страницыEconomic Highlights - A Slight Pick-Up in Industrial Production in August, But Economic Growth Still Trending Downward in The 3Q - 11/10/2010Rhb InvestОценок пока нет

- Economic Highlights: Industrial Production Slowed Down in June, GDP Growth Estimated To Have Softened To +8.1% in The 2Q-10/08/2010Документ4 страницыEconomic Highlights: Industrial Production Slowed Down in June, GDP Growth Estimated To Have Softened To +8.1% in The 2Q-10/08/2010Rhb InvestОценок пока нет

- Economic Highlights: Industrial Production Bounced Back in May, GDPGrowth To Remain Resilient in The 2Q - 08/07/2010Документ3 страницыEconomic Highlights: Industrial Production Bounced Back in May, GDPGrowth To Remain Resilient in The 2Q - 08/07/2010Rhb InvestОценок пока нет

- Economic Highlights - Manufacturing Sales Inched Up in August - 11/10/2010Документ2 страницыEconomic Highlights - Manufacturing Sales Inched Up in August - 11/10/2010Rhb InvestОценок пока нет

- Economic Highlights - Industrial Production Slowed Down in April - 10/6/2010Документ3 страницыEconomic Highlights - Industrial Production Slowed Down in April - 10/6/2010Rhb InvestОценок пока нет

- Economic Highlights: Manufacturing Sales Weakened in June - 10/08/2010Документ2 страницыEconomic Highlights: Manufacturing Sales Weakened in June - 10/08/2010Rhb InvestОценок пока нет

- Economic Highlights: Industrial Production Slowed Down in FebruaryDue To Shorter Working Days - 08/04/2010Документ3 страницыEconomic Highlights: Industrial Production Slowed Down in FebruaryDue To Shorter Working Days - 08/04/2010Rhb InvestОценок пока нет

- Economic Highlights - Economic Activities Improved in April - 30/04/2010Документ4 страницыEconomic Highlights - Economic Activities Improved in April - 30/04/2010Rhb InvestОценок пока нет

- Economic Highlights - Exports Weakened in August, in Tandem With A Slowdown in Global Demand - 11/10/2010Документ4 страницыEconomic Highlights - Exports Weakened in August, in Tandem With A Slowdown in Global Demand - 11/10/2010Rhb InvestОценок пока нет

- Economic Highlights - Vietnam: Real GDP Grew at A Stronger Pace in The 1H-01/07/2010Документ3 страницыEconomic Highlights - Vietnam: Real GDP Grew at A Stronger Pace in The 1H-01/07/2010Rhb InvestОценок пока нет

- Economic Highlights: Manufacturing Sales Held Stable in May - 08/07/2010Документ2 страницыEconomic Highlights: Manufacturing Sales Held Stable in May - 08/07/2010Rhb InvestОценок пока нет

- Vietnam - Economic Highlights - Stronger Economic Activities in May - 1/6/2010Документ4 страницыVietnam - Economic Highlights - Stronger Economic Activities in May - 1/6/2010Rhb InvestОценок пока нет

- Economic Highlights: Manufacturing Sales Grew at A Faster Pace in January - 11/03/2010Документ2 страницыEconomic Highlights: Manufacturing Sales Grew at A Faster Pace in January - 11/03/2010Rhb InvestОценок пока нет

- Economic Highlights - Exports Slowed Down Further in July, As Global Demand Weakens - 03/09/2010Документ4 страницыEconomic Highlights - Exports Slowed Down Further in July, As Global Demand Weakens - 03/09/2010Rhb InvestОценок пока нет

- Economic Highlights: Exports Slowed Down in February Due To Festive Celebration-05/04/2010Документ4 страницыEconomic Highlights: Exports Slowed Down in February Due To Festive Celebration-05/04/2010Rhb InvestОценок пока нет

- Economic Highlights - Vietnam: Economic Data Showing Signs of Weakness in July - 30/07/2010Документ4 страницыEconomic Highlights - Vietnam: Economic Data Showing Signs of Weakness in July - 30/07/2010Rhb InvestОценок пока нет

- Country Strategy 2011-2014 RussiaДокумент18 страницCountry Strategy 2011-2014 RussiaBeeHoofОценок пока нет

- Economic Highlights - Industrial Production Rebounded in March, Real GDP Grew Strongly in The 1Q - 12/5/2010Документ4 страницыEconomic Highlights - Industrial Production Rebounded in March, Real GDP Grew Strongly in The 1Q - 12/5/2010Rhb InvestОценок пока нет

- Economic Highlights: Vietnam: Real GDP Picked Up in The 1Q, Economic Outlook Remains Bright-01/04/2010Документ3 страницыEconomic Highlights: Vietnam: Real GDP Picked Up in The 1Q, Economic Outlook Remains Bright-01/04/2010Rhb InvestОценок пока нет

- Section 1Документ9 страницSection 1usman_maniОценок пока нет

- 1pstate of EconomyДокумент15 страниц1pstate of EconomysuvradipОценок пока нет

- Economic Highlights - Exports Slackened in June, As Global Demand Softened - 03/08/2010Документ4 страницыEconomic Highlights - Exports Slackened in June, As Global Demand Softened - 03/08/2010Rhb InvestОценок пока нет

- Tracking The World Economy... - 02/08/2010Документ3 страницыTracking The World Economy... - 02/08/2010Rhb InvestОценок пока нет

- Economic Highlights - Manufacturing Sales Slowed Down in July - 09/09/2010Документ2 страницыEconomic Highlights - Manufacturing Sales Slowed Down in July - 09/09/2010Rhb InvestОценок пока нет

- Economic Highlights: Manufacturing Sales Grew at A Slower Pace in February MARKET Due To Festive Season - 08/04/2010Документ2 страницыEconomic Highlights: Manufacturing Sales Grew at A Slower Pace in February MARKET Due To Festive Season - 08/04/2010Rhb InvestОценок пока нет

- Index of Industrial Production August 2010: Continued Volatility in Growth RatesДокумент6 страницIndex of Industrial Production August 2010: Continued Volatility in Growth RatesRishabh JainОценок пока нет

- Economic Highlights - Manufacturing Sales Slowed Down in April - 10/6/2010Документ2 страницыEconomic Highlights - Manufacturing Sales Slowed Down in April - 10/6/2010Rhb InvestОценок пока нет

- Economic Highlights - Vietnam: Real GDP Grew at A Faster Pace in January-September 2010 - 29/09/2010Документ3 страницыEconomic Highlights - Vietnam: Real GDP Grew at A Faster Pace in January-September 2010 - 29/09/2010Rhb InvestОценок пока нет

- Growth and Investment Recovery in Pakistan's EconomyДокумент31 страницаGrowth and Investment Recovery in Pakistan's Economymalikrahul_53Оценок пока нет

- Tracking The World Economy... - 18/08/2010Документ3 страницыTracking The World Economy... - 18/08/2010Rhb InvestОценок пока нет

- The World Economy... - 15/7/2010Документ3 страницыThe World Economy... - 15/7/2010Rhb InvestОценок пока нет

- Current State of Indian Economy August 2010 Current State of Indian EconomyДокумент16 страницCurrent State of Indian Economy August 2010 Current State of Indian EconomyNishant VyasОценок пока нет

- Special ReportДокумент11 страницSpecial ReportPriyan PradeepОценок пока нет

- Economic Highlights: Vietnam: Economic Activities Picked Up in March-01/04/2010Документ4 страницыEconomic Highlights: Vietnam: Economic Activities Picked Up in March-01/04/2010Rhb InvestОценок пока нет

- Indian EconomyДокумент13 страницIndian Economygadekar1986Оценок пока нет

- Current State of Indian Economy July 2010 Current State of Indian EconomyДокумент17 страницCurrent State of Indian Economy July 2010 Current State of Indian EconomyPritamkshettyОценок пока нет

- 3 Chapter 2Документ26 страниц3 Chapter 2Raphael MorenzОценок пока нет

- Sunpharma AnalysisДокумент52 страницыSunpharma Analysiskalpeshbadgujar83% (6)

- Economic Highlights: Real GDP Picked Up Strongly by 10.1% Yoy in The 1Q, But Growth Will Likely Slow Down in The 2H - 13/05/2010Документ4 страницыEconomic Highlights: Real GDP Picked Up Strongly by 10.1% Yoy in The 1Q, But Growth Will Likely Slow Down in The 2H - 13/05/2010Rhb InvestОценок пока нет

- NAB Forecast (12 July 2011) : World Slows From Tsunami Disruptions and Tighter Policy.Документ18 страницNAB Forecast (12 July 2011) : World Slows From Tsunami Disruptions and Tighter Policy.International Business Times AUОценок пока нет

- Singapore Economy Continues Robust Expansion in Q2 2010Документ14 страницSingapore Economy Continues Robust Expansion in Q2 2010Estelle PohОценок пока нет

- GDP GrowthДокумент3 страницыGDP GrowthmoulshreesharmaОценок пока нет

- Economic Highlights (Vietnam) : Economic Activities Were Mixed in February - 01/03/2010Документ4 страницыEconomic Highlights (Vietnam) : Economic Activities Were Mixed in February - 01/03/2010Rhb InvestОценок пока нет

- All ChapterДокумент294 страницыAll ChapterManoj KОценок пока нет

- 01 Growth and InvestmentДокумент24 страницы01 Growth and Investmentbugti1986Оценок пока нет

- Report On Index of Industrial Production of Manufacturing Sector From APRIL 2008 TO MARCH 2010Документ10 страницReport On Index of Industrial Production of Manufacturing Sector From APRIL 2008 TO MARCH 2010noorinderОценок пока нет

- GDP For 1st QuarterДокумент5 страницGDP For 1st QuarterUmesh MatkarОценок пока нет

- Tracking The World Economy - 24/08/2010Документ3 страницыTracking The World Economy - 24/08/2010Rhb InvestОценок пока нет

- Economic Highlights: Exports Slowed Down in May, Pointing To WeakerGlobal Demand - 05/07/2010Документ4 страницыEconomic Highlights: Exports Slowed Down in May, Pointing To WeakerGlobal Demand - 05/07/2010Rhb InvestОценок пока нет

- Interim Budget 2009-10Документ12 страницInterim Budget 2009-10allmutualfundОценок пока нет

- India Economic Update: September, 2011Документ17 страницIndia Economic Update: September, 2011Rahul KaushikОценок пока нет

- FRBM 1Документ6 страницFRBM 1girishyadav89Оценок пока нет

- Tracking The World Economy... - 30/07/2010Документ3 страницыTracking The World Economy... - 30/07/2010Rhb InvestОценок пока нет

- Tracking The World Economy... - 01/09/2010Документ4 страницыTracking The World Economy... - 01/09/2010Rhb InvestОценок пока нет

- State of The Economy and Prospects: Website: Http://indiabudget - Nic.inДокумент22 страницыState of The Economy and Prospects: Website: Http://indiabudget - Nic.inNDTVОценок пока нет

- India Econimic Survey 2010-11Документ296 страницIndia Econimic Survey 2010-11vishwanathОценок пока нет

- The Market Call (July 2012)Документ24 страницыThe Market Call (July 2012)Kat ChuaОценок пока нет

- Unloved Bull Markets: Getting Rich the Easy Way by Riding Bull MarketsОт EverandUnloved Bull Markets: Getting Rich the Easy Way by Riding Bull MarketsОценок пока нет

- EIB Investment Report 2023/2024 - Key Findings: Transforming for competitivenessОт EverandEIB Investment Report 2023/2024 - Key Findings: Transforming for competitivenessОценок пока нет

- Investment Report 2022/2023 - Key Findings: Resilience and renewal in EuropeОт EverandInvestment Report 2022/2023 - Key Findings: Resilience and renewal in EuropeОценок пока нет

- Hunza Properties Berhad: Headline Net Profit Skewed by EIs - 25/10/2010Документ3 страницыHunza Properties Berhad: Headline Net Profit Skewed by EIs - 25/10/2010Rhb InvestОценок пока нет

- LBS Bina Group Berhad: Removing The Recent High Will Spell More Rallies Ahead - 25/10/2010Документ2 страницыLBS Bina Group Berhad: Removing The Recent High Will Spell More Rallies Ahead - 25/10/2010Rhb InvestОценок пока нет

- Mandarin Version: Market Technical Reading - Short-Term Outlook Remains Positive... - 25/10/2010Документ6 страницMandarin Version: Market Technical Reading - Short-Term Outlook Remains Positive... - 25/10/2010Rhb InvestОценок пока нет

- Wah Seong Corp Berhad: Gladstone and Curtis LNG Projects Contract Get Environmental Green Light - 25/10/2010Документ2 страницыWah Seong Corp Berhad: Gladstone and Curtis LNG Projects Contract Get Environmental Green Light - 25/10/2010Rhb InvestОценок пока нет

- RHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Документ4 страницыRHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Rhb InvestОценок пока нет

- Corporate Highlights - 25/10/2010Документ2 страницыCorporate Highlights - 25/10/2010Rhb InvestОценок пока нет

- Economic Highlights - Inflation Unexpectedly Eased in September - 25/10/2010Документ3 страницыEconomic Highlights - Inflation Unexpectedly Eased in September - 25/10/2010Rhb InvestОценок пока нет

- QL Resources Berhad: Expansions To Start Contributing From FY12 Onwards - 25/10/2010Документ5 страницQL Resources Berhad: Expansions To Start Contributing From FY12 Onwards - 25/10/2010Rhb InvestОценок пока нет

- Economic Highlights - Foreign Exchange Reserves Rose To US$104.6bn As at 15 October - 25/10/2010Документ2 страницыEconomic Highlights - Foreign Exchange Reserves Rose To US$104.6bn As at 15 October - 25/10/2010Rhb InvestОценок пока нет

- Corporate Highlights - 22/10/2010Документ2 страницыCorporate Highlights - 22/10/2010Rhb InvestОценок пока нет

- Commodities & Currencies - Yet Another Sign of A Rebound On The Greenback - 25/10/2010Документ3 страницыCommodities & Currencies - Yet Another Sign of A Rebound On The Greenback - 25/10/2010Rhb InvestОценок пока нет

- RHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Документ4 страницыRHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Rhb InvestОценок пока нет

- Telecommunications Sector Update: Sizing Up The Pure Mobile Domestic Players - Maxis vs. DiGi - 22/10/2010Документ13 страницTelecommunications Sector Update: Sizing Up The Pure Mobile Domestic Players - Maxis vs. DiGi - 22/10/2010Rhb InvestОценок пока нет

- Market Technical Reading - Fresh Opportunity To Retest 1,500... - 22/10/2010Документ6 страницMarket Technical Reading - Fresh Opportunity To Retest 1,500... - 22/10/2010Rhb InvestОценок пока нет

- Malaysia Airports Holdings Berhad: Sabiha-Gokcen For Long-Term Prospects - 22/10/2010Документ7 страницMalaysia Airports Holdings Berhad: Sabiha-Gokcen For Long-Term Prospects - 22/10/2010Rhb InvestОценок пока нет

- RHB Equity 360° - 22 October 2010 (Telecom, MAHB, Fajarbaru Technical: B-Corp)Документ4 страницыRHB Equity 360° - 22 October 2010 (Telecom, MAHB, Fajarbaru Technical: B-Corp)Rhb InvestОценок пока нет

- Fajarbaru Builder Group Berhad: Lands RM36.5m Pasir Mas Halal Park Infrastructure Job - 22/10/2010Документ3 страницыFajarbaru Builder Group Berhad: Lands RM36.5m Pasir Mas Halal Park Infrastructure Job - 22/10/2010Rhb InvestОценок пока нет

- Axis REIT: Quattro West Started To Contribute - 21/10/2010Документ3 страницыAxis REIT: Quattro West Started To Contribute - 21/10/2010Rhb InvestОценок пока нет

- WCT Berhad: Secures RM1.36bn Building Job in Qatar and RM128m Hospital Project in Sabah - 21/10/2010Документ3 страницыWCT Berhad: Secures RM1.36bn Building Job in Qatar and RM128m Hospital Project in Sabah - 21/10/2010Rhb InvestОценок пока нет

- RHB Equity 360° - 21 October 2010 (Media, Rubber Gloves, Puncak Niaga, WCT, Axis REIT, BAT Technical: AFG)Документ4 страницыRHB Equity 360° - 21 October 2010 (Media, Rubber Gloves, Puncak Niaga, WCT, Axis REIT, BAT Technical: AFG)Rhb InvestОценок пока нет

- Rubber Glove Sector Update: Still Cautious On Near-Term Outlook - 21/10/2010Документ2 страницыRubber Glove Sector Update: Still Cautious On Near-Term Outlook - 21/10/2010Rhb InvestОценок пока нет

- Market Technical Reading - Recapturing The 10-Day SMA Will Renew Upbeat Sentiment... - 21/10/2010Документ6 страницMarket Technical Reading - Recapturing The 10-Day SMA Will Renew Upbeat Sentiment... - 21/10/2010Rhb InvestОценок пока нет

- Corporate Highlights - 21/10/2010Документ2 страницыCorporate Highlights - 21/10/2010Rhb InvestОценок пока нет

- Puncak Niaga Berhad: Eyeing Hogenakkal Water Project in India - 21/10/2010Документ2 страницыPuncak Niaga Berhad: Eyeing Hogenakkal Water Project in India - 21/10/2010Rhb InvestОценок пока нет

- British American Tobacco: Corporate HighlightsДокумент4 страницыBritish American Tobacco: Corporate HighlightsRhb InvestОценок пока нет

- Economic Highlights - Leading Index Bounced Back in August, Pointing To A Resilient Economic Activities Ahead - 20/10/2010Документ2 страницыEconomic Highlights - Leading Index Bounced Back in August, Pointing To A Resilient Economic Activities Ahead - 20/10/2010Rhb InvestОценок пока нет

- Media Sector Update - 9M10 Print and TV Adex Up by 18.2% - 21/10/2010Документ6 страницMedia Sector Update - 9M10 Print and TV Adex Up by 18.2% - 21/10/2010Rhb InvestОценок пока нет

- Economic Highlights - Decline in Manufacturing Investment Approvals Narrowed in The 2Q - 20/10/2010Документ3 страницыEconomic Highlights - Decline in Manufacturing Investment Approvals Narrowed in The 2Q - 20/10/2010Rhb InvestОценок пока нет

- Market Technical Reading - Tracking The Regional Volatile Sentiment... - 20/10/2010Документ6 страницMarket Technical Reading - Tracking The Regional Volatile Sentiment... - 20/10/2010Rhb InvestОценок пока нет

- Economic Highlights - Business Conditions Weakened But Consumer Sentiment Improved in The 3Q - 20/10/2010Документ2 страницыEconomic Highlights - Business Conditions Weakened But Consumer Sentiment Improved in The 3Q - 20/10/2010Rhb InvestОценок пока нет

- OSAP 10 Step Flow ChartДокумент2 страницыOSAP 10 Step Flow ChartPОценок пока нет

- Test 1Документ83 страницыTest 1Cam WolfeОценок пока нет

- IDBI Bank mulls merger of home loan unit to consolidate businessДокумент5 страницIDBI Bank mulls merger of home loan unit to consolidate businessprajuprathuОценок пока нет

- .Practice Set Ibps Cwe Po-IVДокумент18 страниц.Practice Set Ibps Cwe Po-IVsurendra3818Оценок пока нет

- GRC - Governance, Risk Management, and ComplianceДокумент16 страницGRC - Governance, Risk Management, and ComplianceBhavesh RathodОценок пока нет

- Full Length Paper - Role of Technology On Green BankinglДокумент15 страницFull Length Paper - Role of Technology On Green Bankinglapi-33150260Оценок пока нет

- Simple Loan AgreementДокумент3 страницыSimple Loan AgreementFrancis Dave Flores100% (4)

- The History of Banking Kerim CatovicДокумент10 страницThe History of Banking Kerim CatovicsolacevillarealОценок пока нет

- Introduction to ATM: Key Components, Functions, and TroubleshootingДокумент32 страницыIntroduction to ATM: Key Components, Functions, and TroubleshootingMalar100% (1)

- Mba III Advanced Financial Management NotesДокумент49 страницMba III Advanced Financial Management NotesThahir Shah100% (2)

- Indian Institute of Banking & FinanceДокумент8 страницIndian Institute of Banking & FinanceAnonymous QqGiVVKwDGОценок пока нет

- Customer Perceptions and Knowledge of Islamic Banking in Bangladesh (38Документ56 страницCustomer Perceptions and Knowledge of Islamic Banking in Bangladesh (38Md.Azizul Islam0% (1)

- Credit Risk Management at State Bank of HyderabadДокумент86 страницCredit Risk Management at State Bank of HyderabadSagar Paul'g100% (1)

- 28 CREDTRANS Saludo Vs SCBДокумент1 страница28 CREDTRANS Saludo Vs SCBJimenez LorenzОценок пока нет

- Standard Bank online banking payment confirmationДокумент1 страницаStandard Bank online banking payment confirmationEmmanuel EgbebuОценок пока нет

- Md. Mazharul IslamДокумент2 страницыMd. Mazharul IslamMazharul Islam AnikОценок пока нет

- Introduction To T24 - Treasury - R10.1Документ34 страницыIntroduction To T24 - Treasury - R10.1Gnana Sambandam50% (2)

- Hotel Float ChecklistДокумент18 страницHotel Float ChecklistAli Azeem RajwaniОценок пока нет

- 09304079.pdf New Foreign PDFДокумент44 страницы09304079.pdf New Foreign PDFJannatul FerdousОценок пока нет

- Financial Accounting AssignmentДокумент15 страницFinancial Accounting AssignmentEdward MtethiwaОценок пока нет

- DSK BANK Presentation 2007Документ13 страницDSK BANK Presentation 2007Stefania SimonaОценок пока нет

- Chapter 9 – Biological Assets Gain and ValuationДокумент3 страницыChapter 9 – Biological Assets Gain and Valuationma quenaОценок пока нет

- Ing Bank OverviewДокумент4 страницыIng Bank OverviewjohnshatijaОценок пока нет

- IBPS Clerk Main 2016 Capsule by AffairscloudДокумент91 страницаIBPS Clerk Main 2016 Capsule by AffairscloudMadhu SekharОценок пока нет

- Sally's Struthers Co. 2002-2003 financial activityДокумент1 страницаSally's Struthers Co. 2002-2003 financial activityLlyod Francis LaylayОценок пока нет

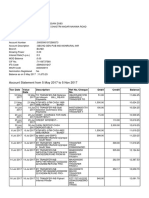

- Interim Statement 10-Mar-2023 12-25-49Документ2 страницыInterim Statement 10-Mar-2023 12-25-49zani arslanОценок пока нет

- HuiДокумент5 страницHuiShiv SinghОценок пока нет

- The development of the short story in Hispanic AmericaДокумент401 страницаThe development of the short story in Hispanic Americaramgomser100% (1)

- Banking Domain 10-Day TrainingДокумент9 страницBanking Domain 10-Day TrainingRedSunОценок пока нет

- Kapso BrochureДокумент13 страницKapso BrochuresathishОценок пока нет