Вам также может понравиться

- Clif Bar Marketing Analysis ReportДокумент17 страницClif Bar Marketing Analysis Reportapi-360938204100% (6)

- Porters Five Forces Ayala Land IncorporatedДокумент12 страницPorters Five Forces Ayala Land IncorporatedPola Polz100% (3)

- Trade Life CycleДокумент98 страницTrade Life Cycleapi-19952066100% (16)

- Elements of Corporate FinanceДокумент9 страницElements of Corporate FinanceReiki Channel Anuj Bhargava100% (1)

- Financial ManagementДокумент65 страницFinancial Managementshekharnishu96% (27)

- Marketing Mix:: ProductДокумент2 страницыMarketing Mix:: Productbilal asifОценок пока нет

- Meaning of Financial ManagementДокумент4 страницыMeaning of Financial ManagementSheila Mae AramanОценок пока нет

- Financial Management - Meaning, Objectives and Functions Meaning of Financial ManagementДокумент9 страницFinancial Management - Meaning, Objectives and Functions Meaning of Financial ManagementGely MhayОценок пока нет

- Meaning of Financial Management: Scope/ElementsДокумент9 страницMeaning of Financial Management: Scope/ElementsLovida AspilaОценок пока нет

- The Scope and Environment of Financial ManagementДокумент3 страницыThe Scope and Environment of Financial Managementgian reyesОценок пока нет

- ACCN09B Strategic Cost Management 1: For Use As Instructional Materials OnlyДокумент3 страницыACCN09B Strategic Cost Management 1: For Use As Instructional Materials OnlyAdrienne Nicole MercadoОценок пока нет

- CH 1financial ManagementДокумент7 страницCH 1financial ManagementᎮᏒᏗᏉᏋᏋᏁ ᏦᏬᎷᏗᏒОценок пока нет

- Financial ManagementДокумент14 страницFinancial ManagementMru SurveОценок пока нет

- Entreprenurship & Management-Module 4 - WatermarkДокумент11 страницEntreprenurship & Management-Module 4 - Watermark81 SYBCOM A SHREYA SHINDEОценок пока нет

- Meaning of Financial ManagementassДокумент13 страницMeaning of Financial ManagementassMayankОценок пока нет

- Introduction To Financial ManagementДокумент13 страницIntroduction To Financial ManagementKayes Mohammad Bin HossainОценок пока нет

- Meaning, Scope & Objectives of Financial ManagementДокумент3 страницыMeaning, Scope & Objectives of Financial ManagementAmanDeep SinghОценок пока нет

- UntitledДокумент3 страницыUntitledZeyОценок пока нет

- Meaning of Financial ManagementДокумент8 страницMeaning of Financial ManagementDinesh GОценок пока нет

- Unit - 2 (Hotel Accounts)Документ5 страницUnit - 2 (Hotel Accounts)Joseph Kiran ReddyОценок пока нет

- Financial ManagementДокумент6 страницFinancial ManagementMik MikОценок пока нет

- Financial Management - Meaning, Objectives and FunctionsДокумент13 страницFinancial Management - Meaning, Objectives and FunctionsJose Conrad Nupia BagonОценок пока нет

- Functions of Financial ManagementДокумент5 страницFunctions of Financial ManagementAthar KhanОценок пока нет

- FM Module 1Документ9 страницFM Module 1ZekiОценок пока нет

- Financial Management - Meaning, Objectives and Functions Meaning of Financial ManagementДокумент6 страницFinancial Management - Meaning, Objectives and Functions Meaning of Financial ManagementsupriyaswainОценок пока нет

- Modules in Financial ManagementДокумент12 страницModules in Financial ManagementMichael Linard Samiley100% (1)

- Financial Management 2Документ7 страницFinancial Management 2Rashmi RanjanaОценок пока нет

- Financial Management - Meaning, Objectives and FunctionsДокумент29 страницFinancial Management - Meaning, Objectives and FunctionsNardsdel RiveraОценок пока нет

- The Role of FinanceДокумент3 страницыThe Role of FinanceDivyaDesaiОценок пока нет

- Topic 8Документ26 страницTopic 8Christine SantosОценок пока нет

- Financial Management NotesДокумент10 страницFinancial Management NotesMubarak Basha100% (1)

- Meaning of Financial ManagementДокумент6 страницMeaning of Financial ManagementYummyОценок пока нет

- Sample Compre Questions Financial ManagementДокумент6 страницSample Compre Questions Financial ManagementMark KevinОценок пока нет

- Finman ReviewerДокумент27 страницFinman Reviewerben yiОценок пока нет

- Financial Management NotesДокумент30 страницFinancial Management NotesChaitanya DongareОценок пока нет

- Financial Management - Meaning, Objectives and Functions Meaning of Financial ManagementДокумент3 страницыFinancial Management - Meaning, Objectives and Functions Meaning of Financial ManagementGirraj Prasad MinaОценок пока нет

- Financial MGTДокумент4 страницыFinancial MGTadidetheОценок пока нет

- Bba FM Notes Unit IДокумент15 страницBba FM Notes Unit Iyashasvigupta.thesironaОценок пока нет

- FM. Final ReportДокумент37 страницFM. Final ReportMuhammad AliОценок пока нет

- FM Theory Meaning of Financial ManagementДокумент10 страницFM Theory Meaning of Financial ManagementDarshan MoreОценок пока нет

- Financial ManagementДокумент48 страницFinancial ManagementAishu SathyaОценок пока нет

- Meaning of Financial ManagementДокумент5 страницMeaning of Financial ManagementJiya FaarОценок пока нет

- Financial Management and ControlДокумент31 страницаFinancial Management and Controljeof basalof100% (1)

- Financial ManagementДокумент2 страницыFinancial ManagementJanelle GalvezОценок пока нет

- Presentation 2Документ10 страницPresentation 2Gopal DasОценок пока нет

- Financial Management AssignmentДокумент5 страницFinancial Management AssignmentZeeshan UmerОценок пока нет

- Meaning of Financial ManagementДокумент3 страницыMeaning of Financial ManagementvanisagiОценок пока нет

- Introduction To Financial ManagementДокумент34 страницыIntroduction To Financial ManagementKevin OnaroОценок пока нет

- Financial ManagementДокумент33 страницыFinancial ManagementSandeep Ghatuary100% (1)

- Strategic Financial QTN MBAДокумент10 страницStrategic Financial QTN MBAMwesigwa DaniОценок пока нет

- Unit 1 Introduction To Financial ManagementДокумент12 страницUnit 1 Introduction To Financial ManagementPRIYA KUMARIОценок пока нет

- Meaning of Financial ManagementДокумент4 страницыMeaning of Financial ManagementNoemie BuñiОценок пока нет

- Introduction of FMДокумент11 страницIntroduction of FMsonika7Оценок пока нет

- Introduction To Financial ManagementДокумент24 страницыIntroduction To Financial ManagementKabile MwitaОценок пока нет

- First HomeworkДокумент6 страницFirst HomeworkDanaОценок пока нет

- Finance An OverviewДокумент25 страницFinance An OverviewJovelyn FerrolinoОценок пока нет

- Introduction To Advanced Financial ManagementДокумент33 страницыIntroduction To Advanced Financial ManagementShubashPoojariОценок пока нет

- Module I: Financial Management - An OverviewДокумент19 страницModule I: Financial Management - An Overviewanusmayavbs1Оценок пока нет

- Module - IV Finance Management 4.1 Introduction To Financial ManagementДокумент18 страницModule - IV Finance Management 4.1 Introduction To Financial ManagementthirumanaskrОценок пока нет

- Financial ManagementДокумент14 страницFinancial ManagementTaher KagalwalaОценок пока нет

- FM 1Документ7 страницFM 1Rohini rs nairОценок пока нет

- Financial Management: DefinitionsДокумент9 страницFinancial Management: DefinitionsAdliana ColinОценок пока нет

- Financial ManagementДокумент33 страницыFinancial ManagementAkash k.cОценок пока нет

- What Is International Entrepreneurship?Документ20 страницWhat Is International Entrepreneurship?Hamza AdilОценок пока нет

- DOSDOS, BIANCA MIKAELA F. Economic GlobalizationДокумент12 страницDOSDOS, BIANCA MIKAELA F. Economic GlobalizationBianx Flores DosdosОценок пока нет

- Interest Rate Hedging-Examples: Arshad HassanДокумент32 страницыInterest Rate Hedging-Examples: Arshad HassanirfanhaidersewagОценок пока нет

- Email Marketing and AutomationДокумент40 страницEmail Marketing and AutomationAMAN SОценок пока нет

- Blackrock PeriodicДокумент2 страницыBlackrock Periodicsameer1987kazi4405Оценок пока нет

- MKT305 ProjectДокумент16 страницMKT305 ProjectshaimaaelgamalОценок пока нет

- Bachelor of Business Administration (BBA) in Retailing III YearДокумент8 страницBachelor of Business Administration (BBA) in Retailing III YearMoksh WariyaОценок пока нет

- Chapter 12 AnswerДокумент13 страницChapter 12 AnswershaneОценок пока нет

- Ncda ResumeДокумент2 страницыNcda Resumeapi-446321851Оценок пока нет

- Class Problems Chapter 6 - Haryo IndraДокумент3 страницыClass Problems Chapter 6 - Haryo IndraHaryo HartoyoОценок пока нет

- Outsourced Chief Investment Officer (OCIO) - Details, Activities and BenefitsДокумент4 страницыOutsourced Chief Investment Officer (OCIO) - Details, Activities and BenefitsTanyamagistralОценок пока нет

- Designing and Implementing Brand Architecture StrategiesДокумент31 страницаDesigning and Implementing Brand Architecture StrategiesSrikant KapoorОценок пока нет

- Value InterviewsДокумент31 страницаValue InterviewsAmit Rana100% (1)

- Responsibility CenterДокумент14 страницResponsibility CenterKashif TradingОценок пока нет

- Esp 2 - Practice - Midterm 1Документ20 страницEsp 2 - Practice - Midterm 1TashaSDОценок пока нет

- JURNAL Manajemen PemasaranДокумент11 страницJURNAL Manajemen PemasaranZakiya AudinaОценок пока нет

- 1.1 Company Background: (CITATION Sho19 /L 1033)Документ14 страниц1.1 Company Background: (CITATION Sho19 /L 1033)Ena Popovska83% (6)

- Split ValuationДокумент13 страницSplit ValuationSandeep Reddy MuskulaОценок пока нет

- Corporate & Institutional Clients: FactsheetДокумент2 страницыCorporate & Institutional Clients: FactsheetNamita SardaОценок пока нет

- ACC 6313 University of Houston Downtown Apple Case StudyДокумент3 страницыACC 6313 University of Houston Downtown Apple Case StudyHomeworkhelpbylanceОценок пока нет

- LUXURY Retail - 6 P's of Luxury MarketingДокумент8 страницLUXURY Retail - 6 P's of Luxury MarketingRahulRahejaОценок пока нет

- Pricing-Good NightДокумент17 страницPricing-Good NightSanjeev ThadaniОценок пока нет

- The Calculations Are Based On "A Sustainable Spending Rate Without Simulation" by M. A. Milevsky & Ch. Robinson, FAJ Vol 61 No 6, 2005Документ6 страницThe Calculations Are Based On "A Sustainable Spending Rate Without Simulation" by M. A. Milevsky & Ch. Robinson, FAJ Vol 61 No 6, 2005morrisonkaniu8283Оценок пока нет

- Chapter Twelve QuestionsДокумент3 страницыChapter Twelve QuestionsabguyОценок пока нет

- ECO306 TutorialДокумент22 страницыECO306 TutorialRosa MoleaОценок пока нет

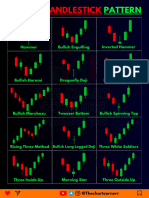

- Chart Pattern Cheat Sheet-1Документ18 страницChart Pattern Cheat Sheet-1YASHANK VISHWAKARMAОценок пока нет