Вам также может понравиться

- Financial Accounting TestbankДокумент34 страницыFinancial Accounting Testbankemilio_ii71% (14)

- Study Material of Corporate Reporting Practice and ASДокумент57 страницStudy Material of Corporate Reporting Practice and ASnidhi goel0% (1)

- MBA604 - Financial Reporting and AnalysisДокумент319 страницMBA604 - Financial Reporting and AnalysisShivam singhОценок пока нет

- M2A Final Copy (V 3.9)Документ181 страницаM2A Final Copy (V 3.9)Cc HyОценок пока нет

- Introduction of IFRS-Issues and ChallengesДокумент12 страницIntroduction of IFRS-Issues and ChallengesAbhisshek GautamОценок пока нет

- IIFL Padmavathi Final Project 0814Документ75 страницIIFL Padmavathi Final Project 0814Matam Matam ChandraОценок пока нет

- IIFL Padmavathi Final Project 08Документ74 страницыIIFL Padmavathi Final Project 08Matam Matam ChandraОценок пока нет

- IIFL Padmavathi Final Project VenkateshДокумент75 страницIIFL Padmavathi Final Project VenkateshMatam Matam ChandraОценок пока нет

- IIFL Padmavathi Final Project VenkatДокумент75 страницIIFL Padmavathi Final Project VenkatMatam Matam ChandraОценок пока нет

- CHAPTER 1 Financial Reporting-ShareДокумент3 страницыCHAPTER 1 Financial Reporting-ShareCahyo PriyatnoОценок пока нет

- Impact of VUCA On Fair Value Accounting: CA Ajit Joshi & CA Rajul MurudkarДокумент8 страницImpact of VUCA On Fair Value Accounting: CA Ajit Joshi & CA Rajul MurudkarResky Andika YuswantoОценок пока нет

- Financial Reporting and Accounting Standards: Learning ObjectivesДокумент13 страницFinancial Reporting and Accounting Standards: Learning ObjectivesHanif MusyaffaОценок пока нет

- Cases Chapter 1Документ4 страницыCases Chapter 1Ahike HukatenОценок пока нет

- 4 6003688552603322754 PDFДокумент21 страница4 6003688552603322754 PDFHadeel Abdul SalamОценок пока нет

- 4357 8498 1 SMДокумент12 страниц4357 8498 1 SMAnu ReetОценок пока нет

- Lecture 1 - Regulatory Framework Financial Reporting - 2023Документ44 страницыLecture 1 - Regulatory Framework Financial Reporting - 2023Suwani HettiarachchiОценок пока нет

- Compiled By: Anwar A. (MSC)Документ14 страницCompiled By: Anwar A. (MSC)AN AdeОценок пока нет

- 1st Lecture - Ch. 1Документ15 страниц1st Lecture - Ch. 1otaku25488Оценок пока нет

- IFRS AdoptionДокумент16 страницIFRS AdoptionMuhammad AzamОценок пока нет

- WP-11 enДокумент44 страницыWP-11 enAlamgir ChowdhuryОценок пока нет

- IFRS 7 Financial Instruments: Disclosures: Technical SummaryДокумент1 страницаIFRS 7 Financial Instruments: Disclosures: Technical SummaryFoititika.netОценок пока нет

- CFAS MODULE and AssДокумент87 страницCFAS MODULE and AsshellokittysaranghaeОценок пока нет

- CFAS MODULE and AssДокумент87 страницCFAS MODULE and AsshellokittysaranghaeОценок пока нет

- Acfm Ch-Two 2022Документ46 страницAcfm Ch-Two 2022mihiretche0Оценок пока нет

- Lesson 1Документ11 страницLesson 1shadowlord468Оценок пока нет

- PG - M.B.a Corporate Secretaryship - English - 331 34 Securities Laws and Financial Markets - 5997Документ169 страницPG - M.B.a Corporate Secretaryship - English - 331 34 Securities Laws and Financial Markets - 5997SujayОценок пока нет

- Week 3Документ38 страницWeek 3Jason wibisonoОценок пока нет

- CH 1Документ97 страницCH 1Anteneh YitbarekОценок пока нет

- A Report ON: Defining Consumers Perception Towards Mutual FundДокумент39 страницA Report ON: Defining Consumers Perception Towards Mutual FundDevika GhorpadeОценок пока нет

- Ifrs D7105118419Документ7 страницIfrs D7105118419Asfawosen DingamaОценок пока нет

- Lesson 1Документ7 страницLesson 1Ira Charisse BurlaosОценок пока нет

- ACC702 Course Material & Study GuideДокумент78 страницACC702 Course Material & Study Guidelaukkeas100% (4)

- IFRS 7 Financial Instruments Disclosures - A CloseДокумент9 страницIFRS 7 Financial Instruments Disclosures - A Closeaditya pandianОценок пока нет

- Cfas Material 1Документ22 страницыCfas Material 1Maybeline BonifacioОценок пока нет

- Hanya AbstrakДокумент35 страницHanya AbstrakNisrinaОценок пока нет

- IFRS Conceptual FrameworkДокумент7 страницIFRS Conceptual FrameworkhemantbaidОценок пока нет

- Covering All EventualitiesДокумент4 страницыCovering All EventualitiesPiyush ShahОценок пока нет

- IFRS 7 Financial Instruments: Disclosures: Technical SummaryДокумент1 страницаIFRS 7 Financial Instruments: Disclosures: Technical SummaryMohammad Faisal SaleemОценок пока нет

- Does IFRS Adoption Improve Financial RepДокумент7 страницDoes IFRS Adoption Improve Financial RepGadaa TDhОценок пока нет

- Accounting QuizДокумент14 страницAccounting QuizMarthen YoparyОценок пока нет

- CFAS MODULE and Ass PDFДокумент86 страницCFAS MODULE and Ass PDFhellokittysaranghaeОценок пока нет

- Cfas Material 1 PDFДокумент6 страницCfas Material 1 PDFErmelyn GayoОценок пока нет

- Cfas Module and AssДокумент86 страницCfas Module and AsshellokittysaranghaeОценок пока нет

- Module 1 - Development of Financial Reporting Framework and Standard Setting Body PDFДокумент6 страницModule 1 - Development of Financial Reporting Framework and Standard Setting Body PDFAubrey CatalanОценок пока нет

- IPSAS1Документ13 страницIPSAS1Nelson BruceОценок пока нет

- Ch01 Financial Reporting - Accounting Standards Kieso Edit tARIEДокумент46 страницCh01 Financial Reporting - Accounting Standards Kieso Edit tARIEVivi RyousukeОценок пока нет

- Chapter-1 INTRODUCTION TO FINANCIAL ACCOUNTINGДокумент15 страницChapter-1 INTRODUCTION TO FINANCIAL ACCOUNTINGWoldeОценок пока нет

- The Objective of Financial ReportingДокумент3 страницыThe Objective of Financial ReportingRizwan HanifОценок пока нет

- ACC702 Course Material Study GuideДокумент78 страницACC702 Course Material Study Guidethùy TrầnОценок пока нет

- Financial StatemenДокумент26 страницFinancial StatemenSarthak SomaniОценок пока нет

- Student Name /ID Number Unit Number and Title Academic Year Unit Assessor Assignment Number and Title Issue Date Submission Date IV Name IV DateДокумент3 страницыStudent Name /ID Number Unit Number and Title Academic Year Unit Assessor Assignment Number and Title Issue Date Submission Date IV Name IV DateMai HươngОценок пока нет

- A Study On The Impact of International Financial Reporting Standards Convergence On Indian Corporate SectorДокумент8 страницA Study On The Impact of International Financial Reporting Standards Convergence On Indian Corporate SectorKiran KumarОценок пока нет

- Slide One Afs BbaДокумент12 страницSlide One Afs BbaMaqbool AhmedОценок пока нет

- Lecture 1Документ24 страницыLecture 1Brenden KapoОценок пока нет

- Ejaj Disser (1) (1) HYPOДокумент36 страницEjaj Disser (1) (1) HYPOEjajОценок пока нет

- Presentation of Financial Management and Services For Cie 2 ExamДокумент12 страницPresentation of Financial Management and Services For Cie 2 ExamAarti .k.ahir8210Оценок пока нет

- Finance (MBA) 322Документ98 страницFinance (MBA) 322Naveen Kumar I MОценок пока нет

- FR Expected Questions May 2022Документ27 страницFR Expected Questions May 2022Gourav JainОценок пока нет

- Ijsrp p102127Документ10 страницIjsrp p102127selman AregaОценок пока нет

- IFRS A Briefing For Boards of DirectorsДокумент60 страницIFRS A Briefing For Boards of DirectorsJose Martin Castillo PatiñoОценок пока нет

- Assignment On Brac BankДокумент9 страницAssignment On Brac BankFarukIslamОценок пока нет

- Comparative Study On Retirement Plan Between United States and BangladeshДокумент3 страницыComparative Study On Retirement Plan Between United States and BangladeshFarukIslamОценок пока нет

- Logo and Design of KFC (Kentucky Fried Chicken)Документ8 страницLogo and Design of KFC (Kentucky Fried Chicken)FarukIslamОценок пока нет

- Subject: Application For Trimester Drop Fall 2018Документ1 страницаSubject: Application For Trimester Drop Fall 2018FarukIslamОценок пока нет

- Job Responsibility As An InternДокумент8 страницJob Responsibility As An InternFarukIslamОценок пока нет

- Front Page & ContentДокумент2 страницыFront Page & ContentFarukIslamОценок пока нет

- Internship On Data PathДокумент10 страницInternship On Data PathFarukIslamОценок пока нет

- Religion of Host Country:: The Bangladeshi Constitution Establishes Islam As The StateДокумент6 страницReligion of Host Country:: The Bangladeshi Constitution Establishes Islam As The StateFarukIslamОценок пока нет

- Requirement 1 E-Business in Organization:: General Description of BusinessДокумент14 страницRequirement 1 E-Business in Organization:: General Description of BusinessFarukIslamОценок пока нет

- International Business Assignment-01: Sec-AДокумент3 страницыInternational Business Assignment-01: Sec-AFarukIslamОценок пока нет

- OPM Case StudyДокумент9 страницOPM Case StudyFarukIslamОценок пока нет

- Notices of Redelivery: Sumon's Exports Redelivery Process IsДокумент1 страницаNotices of Redelivery: Sumon's Exports Redelivery Process IsFarukIslamОценок пока нет

- PSY Memory Assignment NewДокумент9 страницPSY Memory Assignment NewFarukIslamОценок пока нет

- Electron Configurations & Periodicity: Electronic Structure of AtomsДокумент21 страницаElectron Configurations & Periodicity: Electronic Structure of AtomsFarukIslamОценок пока нет

- Activities of ": Uttara Finance and Investment LTD"Документ2 страницыActivities of ": Uttara Finance and Investment LTD"FarukIslamОценок пока нет

- Mughol Establishment of BAngladeshДокумент7 страницMughol Establishment of BAngladeshFarukIslamОценок пока нет

- Sec-D FSAДокумент12 страницSec-D FSAFarukIslamОценок пока нет

- Lab - 9 - NATДокумент5 страницLab - 9 - NATFarukIslamОценок пока нет

- Merchant Activity of Delta Brac Housing Finance Corporation LTDДокумент5 страницMerchant Activity of Delta Brac Housing Finance Corporation LTDFarukIslamОценок пока нет

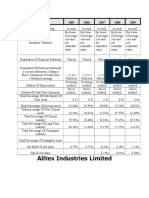

- Alltex Industries Limited: Particulars 2005 2006 2007 2008 2009Документ6 страницAlltex Industries Limited: Particulars 2005 2006 2007 2008 2009FarukIslamОценок пока нет

- Mushroom Chips ReportДокумент17 страницMushroom Chips ReportFarukIslamОценок пока нет

- Prepared For: S M Asif Ur Rahman Assistant Professor School of Business and Economics United International UniversityДокумент3 страницыPrepared For: S M Asif Ur Rahman Assistant Professor School of Business and Economics United International UniversityFarukIslamОценок пока нет

- DSP Lab 1Документ6 страницDSP Lab 1FarukIslamОценок пока нет

- Off All: For For If Else End EndДокумент3 страницыOff All: For For If Else End EndFarukIslamОценок пока нет

- FM 02 - Mfis NotesДокумент7 страницFM 02 - Mfis NotesCorey PageОценок пока нет

- QuestionsДокумент101 страницаQuestionsJhunmar PahimnayanОценок пока нет

- MCI CommunicationsДокумент3 страницыMCI CommunicationsRon BourbondyОценок пока нет

- 06 Cafmst14 - CH - 04Документ35 страниц06 Cafmst14 - CH - 04Mahabub AlamОценок пока нет

- QUIZ Debt InstrumentДокумент4 страницыQUIZ Debt InstrumentJaimell LimОценок пока нет

- Fin 221: Sample MCQ - Chapter 5Документ2 страницыFin 221: Sample MCQ - Chapter 5amalia izzatiОценок пока нет

- Pension Fund Crisis in UsaДокумент5 страницPension Fund Crisis in UsaHa PhamОценок пока нет

- Bus 262 Business Finance Student Final Part HW Corona 2020Документ4 страницыBus 262 Business Finance Student Final Part HW Corona 2020Olatowode OluwatosinОценок пока нет

- Letter To Treasury UCC Contract Trust Example 2Документ2 страницыLetter To Treasury UCC Contract Trust Example 2Lamario StillwellОценок пока нет

- 46 Cargill, Inc. v. Intra Strata Assurance Corp. (Case Digest)Документ2 страницы46 Cargill, Inc. v. Intra Strata Assurance Corp. (Case Digest)Patricia GumpalОценок пока нет

- Dearborn Trade (1) .The 8 Biggest Mistakes People Make With Their Finances Before and After Retirement. (2001.ISBN0793149061)Документ239 страницDearborn Trade (1) .The 8 Biggest Mistakes People Make With Their Finances Before and After Retirement. (2001.ISBN0793149061)Achmad FauzanОценок пока нет

- Pacific Wide CaseДокумент8 страницPacific Wide Casewiggie27Оценок пока нет

- Final Mba ProjectДокумент67 страницFinal Mba Projectlucky goudОценок пока нет

- Adhi - LK - 30 September 2023Документ241 страницаAdhi - LK - 30 September 2023Timothy GracianovОценок пока нет

- E IBD100908Документ24 страницыE IBD100908cphanhuyОценок пока нет

- Introduction To Financial ManagementДокумент13 страницIntroduction To Financial ManagementParveen Dahiya100% (1)

- Finals Answer KeyДокумент6 страницFinals Answer Keymarx marolinaОценок пока нет

- Gbus 7603 - Valuation in Financial Markets Fall 2017, SY Quarter 1Документ19 страницGbus 7603 - Valuation in Financial Markets Fall 2017, SY Quarter 1zZl3Ul2NNINGZzОценок пока нет

- Iifl Gold LoanДокумент79 страницIifl Gold LoanDavid Wright0% (1)

- Time Value of Money - ProblemsДокумент10 страницTime Value of Money - Problemsjav3d762Оценок пока нет

- Governance 1 9Документ381 страницаGovernance 1 9Jhaister Ashley LayugОценок пока нет

- NEPHILA - PSERS Presentation RevisedДокумент30 страницNEPHILA - PSERS Presentation RevisedPAindy100% (2)

- Repo Vs Reverse RepoДокумент9 страницRepo Vs Reverse RepoRajesh GuptaОценок пока нет

- Financial Management Principles and Applications 7th Edition Titman Test BankДокумент16 страницFinancial Management Principles and Applications 7th Edition Titman Test Banktrancuongvaxx8r100% (34)

- 2020 12 31 Southey Capital Illiquid and Distressed PricingДокумент2 страницы2020 12 31 Southey Capital Illiquid and Distressed PricingSouthey CapitalОценок пока нет

- Dfi 302 Lecture NotesДокумент73 страницыDfi 302 Lecture NotesHufzi KhanОценок пока нет

- CRD Trader Fixed IncomeДокумент8 страницCRD Trader Fixed IncomerockstarliveОценок пока нет

- Chapter 16 - Supplementary QuestionsДокумент3 страницыChapter 16 - Supplementary QuestionsRaj PatelОценок пока нет