Вам также может понравиться

- Branding Proposal SummaryДокумент3 страницыBranding Proposal SummaryAna Ckala33% (3)

- hw1 AnsДокумент7 страницhw1 AnsMingyanОценок пока нет

- YHUДокумент1 страницаYHUKartic GhoshОценок пока нет

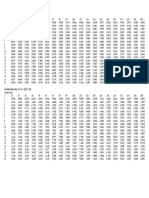

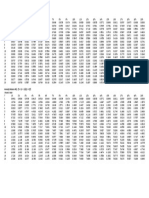

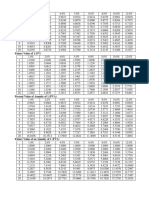

- Pvif & Pvaf Table ValuesДокумент1 страницаPvif & Pvaf Table ValuesDeepak Nandan100% (1)

- Tabel PvafДокумент1 страницаTabel PvafAnisa Siti Wahyuni100% (1)

- Tables PvifaДокумент2 страницыTables PvifaDdy Lee50% (4)

- CFA Chapter 10 PROBLEMSДокумент3 страницыCFA Chapter 10 PROBLEMSFagbola Oluwatobi OmolajaОценок пока нет

- FINS1613 File 03 - Decision Rules (With Solutions) Practice QuestionsДокумент9 страницFINS1613 File 03 - Decision Rules (With Solutions) Practice Questionsisy campbellОценок пока нет

- Present Value of Annuity TableДокумент1 страницаPresent Value of Annuity TableAntonette CastilloОценок пока нет

- K Pvif: Tabel PV Dari RP 1 Pada Akhir Periode Ke-N (Tabel Pvif)Документ4 страницыK Pvif: Tabel PV Dari RP 1 Pada Akhir Periode Ke-N (Tabel Pvif)Valentina AlenОценок пока нет

- Present Value of A $1Документ3 страницыPresent Value of A $1anonimussttОценок пока нет

- Present Value Annuity Due TablesДокумент1 страницаPresent Value Annuity Due TablesDecereen Pineda Rodrigueza100% (2)

- Present Value of A $1Документ3 страницыPresent Value of A $1Aah SonaahОценок пока нет

- Present Value Annuity Tables Formula: PV (1-1 / (1 + I) ) / IДокумент1 страницаPresent Value Annuity Tables Formula: PV (1-1 / (1 + I) ) / IАлинушка Вырлан АркушенкоОценок пока нет

- Present Value Annuity Tables Formula: PV (1-1 / (1 + I) ) / IДокумент1 страницаPresent Value Annuity Tables Formula: PV (1-1 / (1 + I) ) / IVarisha Nawaz100% (1)

- Tabel PV AnnuityДокумент1 страницаTabel PV AnnuityLittle RariesОценок пока нет

- Noi-Amort - Inter / R.F para Tat - Tat / Ean Shp. Amr VL - Nd/vite Ose Vl+inv/vite I Borxh I, (Brxh-Princ) IДокумент2 страницыNoi-Amort - Inter / R.F para Tat - Tat / Ean Shp. Amr VL - Nd/vite Ose Vl+inv/vite I Borxh I, (Brxh-Princ) IXhoiZekajОценок пока нет

- KEQ FV and PV TablesДокумент4 страницыKEQ FV and PV TablesRaj ShravanthiОценок пока нет

- KEQ FV and PV TablesДокумент4 страницыKEQ FV and PV TablesDennis AleaОценок пока нет

- FV and PV TablesДокумент4 страницыFV and PV TablesTanya SinghОценок пока нет

- PV Tables 2020Документ2 страницыPV Tables 2020Saurabh TripathiОценок пока нет

- Present Value of $1 To Be Received in Lumpsum at End of The PeriodДокумент2 страницыPresent Value of $1 To Be Received in Lumpsum at End of The PeriodSaurabh TripathiОценок пока нет

- PV TablesДокумент7 страницPV Tablesaditi shuklaОценок пока нет

- Present Value Factor PVF (R, T) 1 / (1 + R) TДокумент1 страницаPresent Value Factor PVF (R, T) 1 / (1 + R) TTrang NguyenОценок пока нет

- Present Value FactorДокумент1 страницаPresent Value FactorQuỳnh Linh NgôОценок пока нет

- Present value factor and annuity factor table for interest rates from 1% to 20Документ1 страницаPresent value factor and annuity factor table for interest rates from 1% to 20Quỳnh Linh NgôОценок пока нет

- Present Value FactorДокумент1 страницаPresent Value FactorNgan Dang KieuОценок пока нет

- Financial Management: Academy of AccountsДокумент10 страницFinancial Management: Academy of AccountsAshishОценок пока нет

- Practice Problems, CH 9 10 (MCQ)Документ5 страницPractice Problems, CH 9 10 (MCQ)scridОценок пока нет

- Future Value TablesДокумент1 страницаFuture Value TablesumisaaadahОценок пока нет

- Tabel Bunga (Pvif Pvifa)Документ1 страницаTabel Bunga (Pvif Pvifa)gbrlla tanОценок пока нет

- Present Value TablesДокумент2 страницыPresent Value TablesFreelansir100% (1)

- Tabel BungaДокумент2 страницыTabel BungaAnonymous 6bKfDkJmKeОценок пока нет

- Financial Tables PDFДокумент2 страницыFinancial Tables PDFomer1299Оценок пока нет

- PVIF FVIF TableДокумент2 страницыPVIF FVIF TableYaga Kangga0% (1)

- Present Value and Future Value TablesДокумент2 страницыPresent Value and Future Value TablesToniОценок пока нет

- Table PV Ordinary AnnuityДокумент1 страницаTable PV Ordinary AnnuityFisahatunОценок пока нет

- Present Value and Future Value of 1 and Annuities at Various Interest RatesДокумент1 страницаPresent Value and Future Value of 1 and Annuities at Various Interest RatesIrina StrizhkovaОценок пока нет

- F Distribution Tables for Statistics CalculationsДокумент5 страницF Distribution Tables for Statistics CalculationsPebo GreenОценок пока нет

- Present Value and Annuity Tables for Different Discounting RatesДокумент4 страницыPresent Value and Annuity Tables for Different Discounting RatesSupriya SinghОценок пока нет

- Present Value and Annuity Tables for Different Discounting RatesДокумент4 страницыPresent Value and Annuity Tables for Different Discounting RatesSupriya SinghОценок пока нет

- Tabel Present Value - RevisiДокумент3 страницыTabel Present Value - RevisiMagma Bumi RachmaniОценок пока нет

- FIN3120 Exam Paper May 2022Документ4 страницыFIN3120 Exam Paper May 2022Risvana RizzОценок пока нет

- PV Factors 1Документ12 страницPV Factors 1Marian Augelio PolancoОценок пока нет

- Compound Interest TableДокумент6 страницCompound Interest TablespmzОценок пока нет

- Present Value Tables: PRESENT VALUE OF $1.00: DO NOT Detach This Page From The Examination BookletДокумент2 страницыPresent Value Tables: PRESENT VALUE OF $1.00: DO NOT Detach This Page From The Examination BookletFreda DengОценок пока нет

- PV FactorsДокумент6 страницPV FactorsPatricia CaburogОценок пока нет

- Time Value of Money TablesДокумент12 страницTime Value of Money TablesHananAhmedОценок пока нет

- Z-table values for confidence levels from 0.1 to 0.001Документ59 страницZ-table values for confidence levels from 0.1 to 0.001AISYAH HANDINI 1Оценок пока нет

- Tabel Z, T, X, FДокумент59 страницTabel Z, T, X, FAISYAH HANDINI 1Оценок пока нет

- S O C R Socr: Tatistics Nline Omputational Esource F DistributionДокумент5 страницS O C R Socr: Tatistics Nline Omputational Esource F Distributionمهندس ابينОценок пока нет

- Time Value of Money: AppendixДокумент4 страницыTime Value of Money: AppendixnurlaeliyahrahayuОценок пока нет

- Present Value of Annuity CalculatorДокумент3 страницыPresent Value of Annuity CalculatorMotivational QuotesОценок пока нет

- Tabel Present ValueДокумент8 страницTabel Present ValuePricilla PutriОценок пока нет

- Test Bank Managerial Accounting 5th Edition John WildДокумент377 страницTest Bank Managerial Accounting 5th Edition John WildLhowellaAquinoОценок пока нет

- Table 1Документ4 страницыTable 1Baskaran PОценок пока нет

- Abdilah Adib Had Farhan - Tugas AKMДокумент4 страницыAbdilah Adib Had Farhan - Tugas AKMabdillahadib789Оценок пока нет

- Time Value of Money NEW FINALДокумент38 страницTime Value of Money NEW FINALAwais A.Оценок пока нет

- United States Census Figures Back to 1630От EverandUnited States Census Figures Back to 1630Оценок пока нет

- Nirmal Bang Securities Pvt. LTD Company ProfileДокумент7 страницNirmal Bang Securities Pvt. LTD Company ProfileTeja Choudhary Medarametla100% (2)

- Michael Mauboussin - Great Migration:: Public To Private EquityДокумент24 страницыMichael Mauboussin - Great Migration:: Public To Private EquityAbcd123411Оценок пока нет

- Cost Asg3Документ12 страницCost Asg3Shahzȝb KhanОценок пока нет

- SBP - Analyst Briefing NoteДокумент3 страницыSBP - Analyst Briefing Notemuddasir1980Оценок пока нет

- International School of Asia and The Pacific Management Advisory Services Institutional ReviewДокумент27 страницInternational School of Asia and The Pacific Management Advisory Services Institutional ReviewCharles BarcelaОценок пока нет

- Bulgari Hotel London - Creative BriefДокумент18 страницBulgari Hotel London - Creative Briefje100% (1)

- Super Rich StrategyДокумент18 страницSuper Rich StrategyARV PHOTOSОценок пока нет

- Intermediate Accounting II Chapter 15Документ3 страницыIntermediate Accounting II Chapter 15izza zahratunnisa100% (1)

- Edible Oil - Case StudyДокумент8 страницEdible Oil - Case StudyVansh Raj GautamОценок пока нет

- Business Mathematics Module 6.1 Margin and Mark UpДокумент15 страницBusiness Mathematics Module 6.1 Margin and Mark UpDavid DueОценок пока нет

- Threats. Normally The Strengths and Weaknesses Are Internal Factors. OpportunitiesДокумент2 страницыThreats. Normally The Strengths and Weaknesses Are Internal Factors. OpportunitiesHafizuddin Zaqi0% (1)

- Cadbury Dairy MilkДокумент20 страницCadbury Dairy MilkSRIRAMA CHANDRAОценок пока нет

- Bond Yields and Yield Calculations ExplainedДокумент17 страницBond Yields and Yield Calculations ExplainedJESSICA ONGОценок пока нет

- Social Media ManagementДокумент4 страницыSocial Media Managementmaybell panlaquiОценок пока нет

- PDF Book Read MeДокумент3 страницыPDF Book Read MenevatiamlmОценок пока нет

- M-127244 Nea 361Документ2 страницыM-127244 Nea 361Lonely NessОценок пока нет

- Irrometer Ghana PDFДокумент17 страницIrrometer Ghana PDFSarita JacksonОценок пока нет

- JPIM GanjilДокумент8 страницJPIM GanjilNanda Juragan Sandal JepitОценок пока нет

- Marketing Plan MR Bean SingaporeДокумент19 страницMarketing Plan MR Bean SingaporejennifersmithsahОценок пока нет

- Econ 202 Interview Consumption Paper 1Документ3 страницыEcon 202 Interview Consumption Paper 1api-479844980Оценок пока нет

- Chips & Chicken GuideДокумент28 страницChips & Chicken GuideMatata MuthokaОценок пока нет

- Chap 11Документ10 страницChap 11muneeb100% (1)

- Mishkin FMI9ge PPT C04Документ65 страницMishkin FMI9ge PPT C04kbica21Оценок пока нет

- BJT Tugas 2 ADBI4201 Bahasa Inggris Niaga PDFДокумент3 страницыBJT Tugas 2 ADBI4201 Bahasa Inggris Niaga PDFSakazukiОценок пока нет

- Revisiting Fred W. Riggs' Model in The Context of Prismatic' Societies TodayДокумент9 страницRevisiting Fred W. Riggs' Model in The Context of Prismatic' Societies TodayChudi OkoyeОценок пока нет

- Market-Driven Versus Driving MarketsДокумент10 страницMarket-Driven Versus Driving MarketsmkyenОценок пока нет