Вам также может понравиться

- The VIX Trader's Handbook: The history, patterns, and strategies every volatility trader needs to knowОт EverandThe VIX Trader's Handbook: The history, patterns, and strategies every volatility trader needs to knowРейтинг: 4.5 из 5 звезд4.5/5 (3)

- Understanding ETF Options: Profitable Strategies for Diversified, Low-Risk InvestingОт EverandUnderstanding ETF Options: Profitable Strategies for Diversified, Low-Risk InvestingОценок пока нет

- Vix CollectionДокумент49 страницVix Collectionfordaveb100% (1)

- A Guide To VIX Futures and OptionsДокумент33 страницыA Guide To VIX Futures and OptionsSteve Zhang100% (2)

- Hedging With VIX FuturesДокумент8 страницHedging With VIX FuturesGennady NeymanОценок пока нет

- An Introduction To Volatility, VIX, and VXX: What Is Volatility? Volatility. Realized Volatility Refers To HowДокумент8 страницAn Introduction To Volatility, VIX, and VXX: What Is Volatility? Volatility. Realized Volatility Refers To Howchris mbaОценок пока нет

- William VIX FIX IndicatorДокумент7 страницWilliam VIX FIX IndicatorRajandran RajarathinamОценок пока нет

- Options Volatility Trading: Strategies for Profiting from Market SwingsОт EverandOptions Volatility Trading: Strategies for Profiting from Market SwingsРейтинг: 3 из 5 звезд3/5 (2)

- Trading VIX Derivatives: Trading and Hedging Strategies Using VIX Futures, Options, and Exchange-Traded NotesОт EverandTrading VIX Derivatives: Trading and Hedging Strategies Using VIX Futures, Options, and Exchange-Traded NotesРейтинг: 5 из 5 звезд5/5 (1)

- The Volatility Course Workbook: Step-by-Step Exercises to Help You Master The Volatility CourseОт EverandThe Volatility Course Workbook: Step-by-Step Exercises to Help You Master The Volatility CourseОценок пока нет

- Sectors and Styles: A New Approach to Outperforming the MarketОт EverandSectors and Styles: A New Approach to Outperforming the MarketРейтинг: 1 из 5 звезд1/5 (1)

- The - Implied - Order - Book Squeeze MetricsДокумент12 страницThe - Implied - Order - Book Squeeze MetricsSohail Ghanchi100% (1)

- Double Calendar Spreads, How Can We Use Them?Документ6 страницDouble Calendar Spreads, How Can We Use Them?John Klein120% (2)

- Trading Volatility PresentationДокумент24 страницыTrading Volatility PresentationJesse DavisОценок пока нет

- Trading Volatility2 Capturing The VRMДокумент9 страницTrading Volatility2 Capturing The VRMlibra11Оценок пока нет

- Pairs TradingДокумент47 страницPairs TradingMilind KhargeОценок пока нет

- IronbutterplyДокумент3 страницыIronbutterplyCiliaОценок пока нет

- 3 Advantages of Spread TradingДокумент3 страницы3 Advantages of Spread TradingzhaozilongОценок пока нет

- The Implied Order BookДокумент12 страницThe Implied Order Booklife_enjoyОценок пока нет

- Gs Volatility SwapsДокумент56 страницGs Volatility SwapsSangwoo Kim100% (2)

- Advanced Option TraderДокумент1 страницаAdvanced Option TradergauravroongtaОценок пока нет

- Trading Volatility Ny 2016Документ84 страницыTrading Volatility Ny 2016sebab1Оценок пока нет

- Us Ted SpreadДокумент40 страницUs Ted SpreadlmietraderОценок пока нет

- Trading The VXXДокумент9 страницTrading The VXX43stang100% (1)

- Gamma Hedging Absorption PDFДокумент45 страницGamma Hedging Absorption PDFPipi QuquОценок пока нет

- Volatility VolatilityДокумент12 страницVolatility Volatilitywegerg123343Оценок пока нет

- IronCondors CBOEДокумент11 страницIronCondors CBOEPablo OrellanaОценок пока нет

- Derivatives Strategy - November'99 - The Sensitivity of VegaДокумент4 страницыDerivatives Strategy - November'99 - The Sensitivity of VegaLameuneОценок пока нет

- Hedging With OptionsДокумент23 страницыHedging With OptionsMichael YukОценок пока нет

- Pub - Trading Index Options PDFДокумент318 страницPub - Trading Index Options PDF9510501537Оценок пока нет

- Delta Hedging PDFДокумент29 страницDelta Hedging PDFLê AnhОценок пока нет

- Volatility Trading and Managing RiskДокумент5 страницVolatility Trading and Managing Riskpyrole1100% (1)

- Options Trade Evaluation Case StudyДокумент7 страницOptions Trade Evaluation Case Studyrbgainous2199Оценок пока нет

- Strategies For Trading Inverse VolatilityДокумент6 страницStrategies For Trading Inverse VolatilityLogical InvestОценок пока нет

- Barrier OptionsДокумент13 страницBarrier Optionsabhishek210585Оценок пока нет

- The Art of Put Selling PDFДокумент23 страницыThe Art of Put Selling PDFChidambara StОценок пока нет

- Volatility Trading StrategiesДокумент16 страницVolatility Trading StrategiesAvik Banerjee100% (2)

- Cottle BWBДокумент68 страницCottle BWBam13469679Оценок пока нет

- Market MicrostructureДокумент15 страницMarket MicrostructureBen Gdna100% (2)

- Gamma ScalpingДокумент3 страницыGamma Scalpingprivatelogic33% (3)

- VOLATILITYДокумент13 страницVOLATILITYOberoi MalhOtra MeenakshiОценок пока нет

- Trading Volatility PDFДокумент317 страницTrading Volatility PDFGautam Praveen88% (8)

- Natenberg - Weithers RMC 2010 Notes PDFДокумент50 страницNatenberg - Weithers RMC 2010 Notes PDFElvio ATОценок пока нет

- Calendar SpreadДокумент7 страницCalendar SpreadJames LiuОценок пока нет

- Vix N NiftyДокумент11 страницVix N Niftyrahul.ztbОценок пока нет

- Ryan Road Trip Trade PresentationДокумент32 страницыRyan Road Trip Trade PresentationHernan DiazОценок пока нет

- Gamma Trade OptionsДокумент40 страницGamma Trade Optionssnowbash50% (2)

- The VIX Futures Basis - Evidence and Trading StrategiesДокумент41 страницаThe VIX Futures Basis - Evidence and Trading StrategiesPhil MironenkoОценок пока нет

- Global Equity Momentum A Craftsmans PerspectiveДокумент39 страницGlobal Equity Momentum A Craftsmans Perspectivelife_enjoyОценок пока нет

- What Is Double Diagonal Spread - FidelityДокумент8 страницWhat Is Double Diagonal Spread - FidelityanalystbankОценок пока нет

- Volatility Handbook FinalДокумент49 страницVolatility Handbook Finalmarj100% (1)

- Index Option Trading Activity and Market ReturnsДокумент59 страницIndex Option Trading Activity and Market ReturnsRamasamyShenbagaraj100% (1)

- Bull or Bear, We Don'T Care !: Resource Guide For Trading Without Predicting Market DirectionДокумент7 страницBull or Bear, We Don'T Care !: Resource Guide For Trading Without Predicting Market DirectionRuler ForGood2Оценок пока нет

- Joe Ross - Spread Trading PDFДокумент79 страницJoe Ross - Spread Trading PDFRazvanCristian100% (1)

- (BNP Paribas) Volatility Investing HandbookДокумент43 страницы(BNP Paribas) Volatility Investing Handbooktv1s100% (3)

- HFT Bibliography 2015Документ59 страницHFT Bibliography 2015ZerohedgeОценок пока нет

- SMB - Options - Tribe - 8!20!2013 (Jeff Augen - Short Butterfly)Документ8 страницSMB - Options - Tribe - 8!20!2013 (Jeff Augen - Short Butterfly)Peter Guardian100% (4)

- Livevol Database StructureДокумент15 страницLivevol Database StructureJuan LamadridОценок пока нет

- Option Market Making : Part 1, An Introduction: Extrinsiq Advanced Options Trading Guides, #3От EverandOption Market Making : Part 1, An Introduction: Extrinsiq Advanced Options Trading Guides, #3Оценок пока нет

- The Ethnicity of The AntichristДокумент6 страницThe Ethnicity of The AntichristGennady NeymanОценок пока нет

- CFTC Part 4 Exemption Easy Reference GuideДокумент2 страницыCFTC Part 4 Exemption Easy Reference GuideGennady NeymanОценок пока нет

- Understanding-RAUM 2020Документ17 страницUnderstanding-RAUM 2020Gennady NeymanОценок пока нет

- Understanding-RAUM 2020Документ17 страницUnderstanding-RAUM 2020Gennady NeymanОценок пока нет

- How Etfs Work: Authorized Participants (Ap) and The Creation of Fund SharesДокумент3 страницыHow Etfs Work: Authorized Participants (Ap) and The Creation of Fund SharesGennady NeymanОценок пока нет

- FT - How Schonfeld Fell Into Millennium's EmbraceДокумент4 страницыFT - How Schonfeld Fell Into Millennium's EmbraceGennady NeymanОценок пока нет

- CPO and CTA Registration Requirements For Hedge Fund ManagersДокумент5 страницCPO and CTA Registration Requirements For Hedge Fund ManagersGennady NeymanОценок пока нет

- Put-Call Parity and The Law PDFДокумент32 страницыPut-Call Parity and The Law PDFGennady NeymanОценок пока нет

- SSRN Id274824Документ36 страницSSRN Id274824Gennady NeymanОценок пока нет

- PIMCO in Depth Bhansali Inflation Tail Risk Hedging May2013 PDFДокумент20 страницPIMCO in Depth Bhansali Inflation Tail Risk Hedging May2013 PDFGennady NeymanОценок пока нет

- Viewpoint Etf Primary Trading Role of Authorized Participants March 2017Документ11 страницViewpoint Etf Primary Trading Role of Authorized Participants March 2017ColterNateОценок пока нет

- Integrated Tail Risk HedgingДокумент9 страницIntegrated Tail Risk HedgingGennady NeymanОценок пока нет

- CT Top 20 Offshore Funds 0 0Документ4 страницыCT Top 20 Offshore Funds 0 0Gennady NeymanОценок пока нет

- White Paper Sound Practices For Hedge Fund MangersДокумент10 страницWhite Paper Sound Practices For Hedge Fund MangersGennady NeymanОценок пока нет

- Vontobel Investing in Liquid Alternatives Pure Strategies enДокумент12 страницVontobel Investing in Liquid Alternatives Pure Strategies enGennady NeymanОценок пока нет

- 20 Habits of Wealthy Traders - Part 1: What Does It Really Take To Succeed?Документ5 страниц20 Habits of Wealthy Traders - Part 1: What Does It Really Take To Succeed?Gennady NeymanОценок пока нет

- Margolis Advisory GroupДокумент5 страницMargolis Advisory GroupGennady NeymanОценок пока нет

- DM Finance - Brexit Case StudyДокумент2 страницыDM Finance - Brexit Case StudyGennady NeymanОценок пока нет

- Liquid Alternatives - More Than Return PotentialДокумент5 страницLiquid Alternatives - More Than Return PotentialGennady NeymanОценок пока нет

- Calpers ReviewДокумент5 страницCalpers ReviewGennady NeymanОценок пока нет

- Moodys HF GovernanceДокумент8 страницMoodys HF GovernanceGennady NeymanОценок пока нет

- 2013 Manager's Guide To Launching A HFДокумент42 страницы2013 Manager's Guide To Launching A HFmarketcipherОценок пока нет

- Riding The Yield Curve in Up and Down MarketsДокумент6 страницRiding The Yield Curve in Up and Down MarketsGennady NeymanОценок пока нет

- Goldman Sachs Derivatives Research - SPX Volatility Continuing To Outpace Global Indices'Документ9 страницGoldman Sachs Derivatives Research - SPX Volatility Continuing To Outpace Global Indices'Gennady NeymanОценок пока нет

- Goldman Sachs Derivatives Research - Top 25 Tactical Trades For Earnings SeasonДокумент25 страницGoldman Sachs Derivatives Research - Top 25 Tactical Trades For Earnings SeasonGennady NeymanОценок пока нет

- Towers Watson Tail Risk Management Strategies Oct2015Документ14 страницTowers Watson Tail Risk Management Strategies Oct2015Gennady NeymanОценок пока нет

- Vix Paper EfmaДокумент35 страницVix Paper EfmaGennady NeymanОценок пока нет

- Mba Anna University PPT Material For MBFS 2012Документ39 страницMba Anna University PPT Material For MBFS 2012mail2nsathish67% (3)

- Knight Capital Group, Inc.: Sandler O'Neill Global Exchange and Brokerage Conference - June 7, 2012Документ13 страницKnight Capital Group, Inc.: Sandler O'Neill Global Exchange and Brokerage Conference - June 7, 2012JohnОценок пока нет

- L Project of FiiДокумент53 страницыL Project of Fiimanisha_mithibaiОценок пока нет

- EBIT EPS AnalysisДокумент29 страницEBIT EPS Analysisshalini swarajОценок пока нет

- History of Stock BrokingДокумент4 страницыHistory of Stock BrokingDiwakar SinghОценок пока нет

- Dalmia Scam PresentationДокумент15 страницDalmia Scam PresentationNishantОценок пока нет

- Order in The Matter of Snowcem India Ltd. (Now Known As SIL Business Enterprises LTD.)Документ2 страницыOrder in The Matter of Snowcem India Ltd. (Now Known As SIL Business Enterprises LTD.)Shyam SunderОценок пока нет

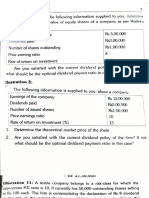

- Assignment of SFM 02-Feb-2022Документ6 страницAssignment of SFM 02-Feb-2022Sandhya MudaliarОценок пока нет

- Lamp IranДокумент53 страницыLamp IranMushanokoji ShienОценок пока нет

- A Financial Statement Analysis of SBS Philippines Corporation For The Years 2014-2016Документ11 страницA Financial Statement Analysis of SBS Philippines Corporation For The Years 2014-2016sephОценок пока нет

- Davis 2022Документ36 страницDavis 2022Heru SylvanataОценок пока нет

- 01-A Color-Based System For Short-Term Trading PDFДокумент4 страницы01-A Color-Based System For Short-Term Trading PDFNathan ChrisОценок пока нет

- Problem 1Документ4 страницыProblem 1andrei jude matullanoОценок пока нет

- Motilal Oswal Nifty 200 Momentum 30 ETFДокумент22 страницыMotilal Oswal Nifty 200 Momentum 30 ETFbapianshumanОценок пока нет

- Ranald C. Michie - The London Stock Exchange - A History (2000)Документ697 страницRanald C. Michie - The London Stock Exchange - A History (2000)miguelip01Оценок пока нет

- The Art of Put Selling PDFДокумент23 страницыThe Art of Put Selling PDFChidambara StОценок пока нет

- Fundamental Equity Analysis - Nasdaq 100 Index Members (NDX Index)Документ205 страницFundamental Equity Analysis - Nasdaq 100 Index Members (NDX Index)Q.M.S Advisors LLCОценок пока нет

- The Financial Market EnvironmentДокумент45 страницThe Financial Market EnvironmentThenappan Ganesen100% (1)

- The Capitalism DistributionДокумент5 страницThe Capitalism DistributionecrittОценок пока нет

- 10 Tech Stocks That Could Triple The - Perfect 10 - Portfolio - InvestorPlaceДокумент5 страниц10 Tech Stocks That Could Triple The - Perfect 10 - Portfolio - InvestorPlaceJorge VasconcelosОценок пока нет

- Imt 09Документ4 страницыImt 09nikhilanand13Оценок пока нет

- Indicate The Correct Answer To Each of The Questions From 1 To 10Документ5 страницIndicate The Correct Answer To Each of The Questions From 1 To 10Hoang Thi Hong ThomОценок пока нет

- Market Ratios - Practice QuestionsДокумент16 страницMarket Ratios - Practice QuestionsOsama Saleem0% (1)

- ZOTA 15062023165216 Outcome15062023Документ7 страницZOTA 15062023165216 Outcome15062023Ankk TenderzОценок пока нет

- Financial Planning EbookДокумент51 страницаFinancial Planning EbookSiddharth PatilОценок пока нет

- CTH 10 THD InvestasiДокумент17 страницCTH 10 THD Investasinoel_manroeОценок пока нет

- A Summer Internship ReportДокумент33 страницыA Summer Internship ReportPrateek BissaОценок пока нет

- Financial Market Trader - Intern: Bearstreet Research and Analysis PVT LTD 1 - 6 Yrs Delhi NCRДокумент2 страницыFinancial Market Trader - Intern: Bearstreet Research and Analysis PVT LTD 1 - 6 Yrs Delhi NCRCesar De JesusОценок пока нет

- Vanguard FTSE Canada Index ETF VCE: December 31, 2019Документ2 страницыVanguard FTSE Canada Index ETF VCE: December 31, 2019ChrisОценок пока нет

- Problem 9-4: Name: Section: ScoreДокумент5 страницProblem 9-4: Name: Section: ScoreMohd ZuhairОценок пока нет