Вам также может понравиться

- Aircraft Carriers - The Illustrated History of The World's Most Important Warships (PDFDrive) PDFДокумент243 страницыAircraft Carriers - The Illustrated History of The World's Most Important Warships (PDFDrive) PDFChronosGod100% (4)

- Shipping Practice - With a Consideration of the Law Relating TheretoОт EverandShipping Practice - With a Consideration of the Law Relating TheretoОценок пока нет

- Prolonged PregnancyДокумент41 страницаProlonged PregnancyArif Febrianto100% (1)

- Special Proceedings Case DigestДокумент14 страницSpecial Proceedings Case DigestDyan Corpuz-Suresca100% (1)

- Special Issues in International Law 2009 - 2019 International Law Bar Questions & Suggested Answers and International IssuesДокумент18 страницSpecial Issues in International Law 2009 - 2019 International Law Bar Questions & Suggested Answers and International IssuesAustine Campos100% (1)

- Dungo vs. People, G.R. No. 209464, July 1, 2015 (761 SCRA 375, 427-431)Документ1 страницаDungo vs. People, G.R. No. 209464, July 1, 2015 (761 SCRA 375, 427-431)Multi PurposeОценок пока нет

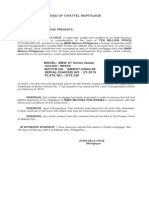

- Deed of Chattel MortgageДокумент2 страницыDeed of Chattel MortgageInnoKal100% (1)

- Macondary Co. v Commissioner of CustomsДокумент4 страницыMacondary Co. v Commissioner of CustomsPipoy AmyОценок пока нет

- NAVSEA SW010-AD-GTP-010 TM Small Arms Special Warfare AmmunitionДокумент376 страницNAVSEA SW010-AD-GTP-010 TM Small Arms Special Warfare Ammunitionsergey62Оценок пока нет

- Defender Of: Protector of Those at SeaДокумент2 страницыDefender Of: Protector of Those at SeaElenie100% (3)

- Transglobe InternationalДокумент7 страницTransglobe InternationalMaggieОценок пока нет

- En Banc: Petitioners vs. vs. RespondentДокумент6 страницEn Banc: Petitioners vs. vs. RespondentShairaCamilleGarciaОценок пока нет

- Bar Questions Property FinalsДокумент21 страницаBar Questions Property FinalsAustine CamposОценок пока нет

- Alliance in Motion Global Business Centers Across LuzonДокумент5 страницAlliance in Motion Global Business Centers Across LuzonDee Compiler100% (1)

- PgsДокумент7 страницPgsAustine CamposОценок пока нет

- FIFA World Cup Milestones, Facts & FiguresДокумент25 страницFIFA World Cup Milestones, Facts & FiguresAleks VОценок пока нет

- CIR VS. TOKYO SHIPPING TAX REFUNDДокумент5 страницCIR VS. TOKYO SHIPPING TAX REFUNDIshmael SalisipОценок пока нет

- Philippines Supreme Court Rules on Jurisdiction in Customs Forfeiture CaseДокумент4 страницыPhilippines Supreme Court Rules on Jurisdiction in Customs Forfeiture CaseCheryl ChurlОценок пока нет

- Tax DigestДокумент4 страницыTax DigestKristoffer Gabriel Laurio MadridОценок пока нет

- Customs - Cir Vs AgfhaДокумент9 страницCustoms - Cir Vs AgfhaKarla Marie TumulakОценок пока нет

- Farolan v. CTA (1993)Документ5 страницFarolan v. CTA (1993)Carlo MercadoОценок пока нет

- Transglobe International, Inc.,V. Court of AppealsДокумент6 страницTransglobe International, Inc.,V. Court of AppealsattyGezОценок пока нет

- Cases On Tax2Документ19 страницCases On Tax2XexAriasОценок пока нет

- Tariffs & Customs Code - C.T.a.Документ5 страницTariffs & Customs Code - C.T.a.JoAnne Yaptinchay ClaudioОценок пока нет

- Farolan V CTAДокумент6 страницFarolan V CTALyut SoroanОценок пока нет

- Court upholds fine for unmanifested cargoДокумент76 страницCourt upholds fine for unmanifested cargoNaika Ramos LofrancoОценок пока нет

- Farolan V CAДокумент11 страницFarolan V CAJoy NavalesОценок пока нет

- COC V CAДокумент17 страницCOC V CAJust a researcherОценок пока нет

- The Solicitor General For Petitioner. Jorge G. Macapagal Counsel For Respondent. Aurea Aragon-Casiano For Bagong Buhay TradingДокумент4 страницыThe Solicitor General For Petitioner. Jorge G. Macapagal Counsel For Respondent. Aurea Aragon-Casiano For Bagong Buhay TradingZachary BañezОценок пока нет

- Stare DecisisДокумент6 страницStare DecisisJackRio009Оценок пока нет

- Philippines Supreme Court Rules on Customs CaseДокумент6 страницPhilippines Supreme Court Rules on Customs CasejadestopaОценок пока нет

- 29) Phil First Ins Co., Inc. vs. Wallem Phils. Shipping, Inc., Et Al. G.R. No. 165647, March 26, 2009Документ7 страниц29) Phil First Ins Co., Inc. vs. Wallem Phils. Shipping, Inc., Et Al. G.R. No. 165647, March 26, 2009S.G.T.Оценок пока нет

- Court Rules Against Customs Forfeiture and Orders Release of GoodsДокумент8 страницCourt Rules Against Customs Forfeiture and Orders Release of GoodsKirby MalibiranОценок пока нет

- G.R. No. 42204 - Farolan V CTA PDFДокумент5 страницG.R. No. 42204 - Farolan V CTA PDFJericho UyОценок пока нет

- G.R. No. 128064 - R.V. Marzan Freight Inc. v. Court of AppealsДокумент13 страницG.R. No. 128064 - R.V. Marzan Freight Inc. v. Court of AppealsJAMES WILLIAM BALAOОценок пока нет

- CIR vs. Tokyo Shipping, GR#68252, May 26, 1995 224 SCRA 332Документ5 страницCIR vs. Tokyo Shipping, GR#68252, May 26, 1995 224 SCRA 332Khenlie VillaceranОценок пока нет

- Farolan v. CTA, 217 SCRA 298 (1993)Документ6 страницFarolan v. CTA, 217 SCRA 298 (1993)Bryan delimaОценок пока нет

- Supreme Court Rules in Favor of Importer in Customs Fraud CaseДокумент19 страницSupreme Court Rules in Favor of Importer in Customs Fraud CaseAustine CamposОценок пока нет

- The Solicitor General For Petitioner. Jorge G. Macapagal Counsel For Respondent. Aurea Aragon-Casiano For Bagong Buhay TradingДокумент4 страницыThe Solicitor General For Petitioner. Jorge G. Macapagal Counsel For Respondent. Aurea Aragon-Casiano For Bagong Buhay TradingTravis OpizОценок пока нет

- Shell v. Commr. of CustomsДокумент16 страницShell v. Commr. of Customspraning125Оценок пока нет

- Collector of Customs vs. Torres Gr. No. L-22977, May 31, 1972Документ11 страницCollector of Customs vs. Torres Gr. No. L-22977, May 31, 1972Ron LaurelОценок пока нет

- R.V. Marzan Freight v. CA and Sheila's ManufacturingДокумент11 страницR.V. Marzan Freight v. CA and Sheila's ManufacturingophiliamariedalonosОценок пока нет

- Case StudyДокумент50 страницCase StudyJaypee BallesterosОценок пока нет

- Tariif CasesДокумент25 страницTariif CasesJeLabu SabОценок пока нет

- Asian Terminals V RicaforteДокумент17 страницAsian Terminals V RicaforteJust a researcherОценок пока нет

- Farolan Vs Court of Tax AppealДокумент10 страницFarolan Vs Court of Tax AppealRussell John HipolitoОценок пока нет

- Cir Vs TokyoДокумент3 страницыCir Vs TokyoKimberly SendinОценок пока нет

- Farolan V CTAДокумент5 страницFarolan V CTAJericho UyОценок пока нет

- R. No. 128064 March 4, 2004 R.V. MARZAN FREIGHT, INC., Petitioner, Court of Appeals and Shiela'S Manufacturing, Inc., RespondentsДокумент22 страницыR. No. 128064 March 4, 2004 R.V. MARZAN FREIGHT, INC., Petitioner, Court of Appeals and Shiela'S Manufacturing, Inc., RespondentsTravis Opiz100% (1)

- Farolan vs. CtaДокумент5 страницFarolan vs. CtaRonald MorenoОценок пока нет

- WestWind vs. UCPB General InsuranceДокумент9 страницWestWind vs. UCPB General InsuranceAnalyn Grace Yongco BasayОценок пока нет

- Citadel Lines, Inc. Vs CAДокумент8 страницCitadel Lines, Inc. Vs CARhona MarasiganОценок пока нет

- CIR vs. Tokyo Shipping, 244 SCRA 332Документ5 страницCIR vs. Tokyo Shipping, 244 SCRA 332Machida AbrahamОценок пока нет

- 13 Farolan v. CTA Governmental function - unincorporated,Документ4 страницы13 Farolan v. CTA Governmental function - unincorporated,Caliliw NathanielОценок пока нет

- QuisumbingДокумент9 страницQuisumbingmar corОценок пока нет

- 10 Carara Marble Inc vs. CCДокумент4 страницы10 Carara Marble Inc vs. CCMaria Jela MoranОценок пока нет

- Common Carrier of Goods Fulltext Part 1Документ98 страницCommon Carrier of Goods Fulltext Part 1Jo-Al GealonОценок пока нет

- Choa Tiek Seng Vs CAДокумент8 страницChoa Tiek Seng Vs CAMark Daniel PadditОценок пока нет

- De Joya Vs Hon. Gregorio T. Lantin.Документ5 страницDe Joya Vs Hon. Gregorio T. Lantin.Jabar SabdullahОценок пока нет

- t1. Cir vs. Tokyo ShippingДокумент2 страницыt1. Cir vs. Tokyo ShippingMannor ModaОценок пока нет

- Asian Terminals vs. RicafortДокумент11 страницAsian Terminals vs. RicafortJohn FerarenОценок пока нет

- 4 InterprovincialДокумент10 страниц4 InterprovincialKEMPОценок пока нет

- G.R. No. 136888 June 29, 2005 Philippine Charter Insurance Corporation, Petitioner, Chemoil Lighterage Corporation, RespondentДокумент7 страницG.R. No. 136888 June 29, 2005 Philippine Charter Insurance Corporation, Petitioner, Chemoil Lighterage Corporation, RespondentHelen Grace M. BautistaОценок пока нет

- Associated Sugar Inc Et Al Vs Commissioner of Customs Et AlДокумент3 страницыAssociated Sugar Inc Et Al Vs Commissioner of Customs Et AlRyan Jhay YangОценок пока нет

- Rich Text Editor FileSeДокумент6 страницRich Text Editor FileSeAndy JoseОценок пока нет

- Westwind Vs UcpbДокумент5 страницWestwind Vs UcpbHiezll Wynn R. RiveraОценок пока нет

- Philippines First Insurance Co., Inc. v. Wallem Phils. Shipping, Inc. G.R. No. 165647. March 26, 2009Документ8 страницPhilippines First Insurance Co., Inc. v. Wallem Phils. Shipping, Inc. G.R. No. 165647. March 26, 2009Melle EscaroОценок пока нет

- 16 Citadel LinesДокумент4 страницы16 Citadel LinesMary Louise R. ConcepcionОценок пока нет

- De Joya Vs Hon. Gregorio TooooДокумент5 страницDe Joya Vs Hon. Gregorio TooooJabar SabdullahОценок пока нет

- Tax Midterm CasesДокумент33 страницыTax Midterm CasesCassey Koi FarmОценок пока нет

- Asian Terminals Inc. vs. Malayan Insurance Co. Inc.Документ21 страницаAsian Terminals Inc. vs. Malayan Insurance Co. Inc.Jessica mabungaОценок пока нет

- General Instructions for the Guidance of Post Office Inspectors in the Dominion of CanadaОт EverandGeneral Instructions for the Guidance of Post Office Inspectors in the Dominion of CanadaОценок пока нет

- Ratio: : 1. Kuroda Vs JalandoniДокумент8 страницRatio: : 1. Kuroda Vs JalandoniAustine CamposОценок пока нет

- Ip Digest Cases CH1Документ6 страницIp Digest Cases CH1Austine CamposОценок пока нет

- 4, 9, 14, 19, 24, 29, 34, 39, 44, 49, 54, 59, 64Документ9 страниц4, 9, 14, 19, 24, 29, 34, 39, 44, 49, 54, 59, 64Ronnieday AledoОценок пока нет

- Ratio: : 1. Kuroda Vs JalandoniДокумент8 страницRatio: : 1. Kuroda Vs JalandoniAustine CamposОценок пока нет

- Ip Digest Cases CH1Документ6 страницIp Digest Cases CH1Austine CamposОценок пока нет

- PNB Vs REFRIGERATIONДокумент8 страницPNB Vs REFRIGERATIONAustine CamposОценок пока нет

- Coloring Adult MPC DesignДокумент1 страницаColoring Adult MPC DesignAustine CamposОценок пока нет

- Manzano VS DespabiladerasДокумент12 страницManzano VS DespabiladerasAustine CamposОценок пока нет

- G.R. No. 195549. September 3, 2014. Willaware Products Corporation, Petitioner, vs. Jesichris Manufacturing Corporation, RespondentДокумент14 страницG.R. No. 195549. September 3, 2014. Willaware Products Corporation, Petitioner, vs. Jesichris Manufacturing Corporation, RespondentAustine CamposОценок пока нет

- LegalmaximДокумент6 страницLegalmaximAustine CamposОценок пока нет

- G.R. No. 195549. September 3, 2014. Willaware Products Corporation, Petitioner, vs. Jesichris Manufacturing Corporation, RespondentДокумент14 страницG.R. No. 195549. September 3, 2014. Willaware Products Corporation, Petitioner, vs. Jesichris Manufacturing Corporation, RespondentAustine CamposОценок пока нет

- 75 Pacioles vs. ChuatocoДокумент17 страниц75 Pacioles vs. ChuatocoAustine CamposОценок пока нет

- Taxation 2 Part Vi - Estate TaxДокумент15 страницTaxation 2 Part Vi - Estate TaxAustine CamposОценок пока нет

- Batist IsДокумент14 страницBatist IsAustine CamposОценок пока нет

- AMLA With AmendmentsДокумент15 страницAMLA With AmendmentsAustine CamposОценок пока нет

- Phil. Pharmawealth, Inc. V. Pfizer, Inc. & Pfizer (PHIL.), INC. G.R. NO. 167715, 17 NOVEMBER 2010Документ4 страницыPhil. Pharmawealth, Inc. V. Pfizer, Inc. & Pfizer (PHIL.), INC. G.R. NO. 167715, 17 NOVEMBER 2010Austine CamposОценок пока нет

- Accession With Respect To Movable PropertyДокумент2 страницыAccession With Respect To Movable PropertyAustine CamposОценок пока нет

- Castillo vs. Cruz PDFДокумент12 страницCastillo vs. Cruz PDFAustine CamposОценок пока нет

- Title 2Документ7 страницTitle 2Austine CamposОценок пока нет

- Ip 281Документ13 страницIp 281Austine CamposОценок пока нет

- Castillo vs. Cruz PDFДокумент12 страницCastillo vs. Cruz PDFAustine CamposОценок пока нет

- Succession SS Cases 1 8Документ5 страницSuccession SS Cases 1 8Austine CamposОценок пока нет

- Title 2Документ7 страницTitle 2Austine CamposОценок пока нет

- Reyes Et Al vs. CAДокумент12 страницReyes Et Al vs. CAAustine CamposОценок пока нет

- G.R. No. 195549. September 3, 2014. Willaware Products Corporation, Petitioner, vs. Jesichris Manufacturing Corporation, RespondentДокумент14 страницG.R. No. 195549. September 3, 2014. Willaware Products Corporation, Petitioner, vs. Jesichris Manufacturing Corporation, RespondentAustine CamposОценок пока нет

- Torts SyllabusДокумент13 страницTorts SyllabusAustine CamposОценок пока нет

- UycoДокумент7 страницUycoAustine CamposОценок пока нет

- Cifra Club - Ed Sheeran - PhotographДокумент2 страницыCifra Club - Ed Sheeran - PhotographAnonymous 3g5b91qОценок пока нет

- ANFFl LYERS2012Документ2 страницыANFFl LYERS2012Clifford ImsonОценок пока нет

- Judge Not Liable for Gross IgnoranceДокумент5 страницJudge Not Liable for Gross IgnoranceCoast Guard Frogman SogОценок пока нет

- PP vs. Gabrino - Ruling - LawphilДокумент5 страницPP vs. Gabrino - Ruling - LawphillalaОценок пока нет

- Joe Cocker - When The Night Comes ChordsДокумент2 страницыJoe Cocker - When The Night Comes ChordsAlan FordОценок пока нет

- 20101015121029lecture-7 - (Sem1!10!11) Feminism in MalaysiaДокумент42 страницы20101015121029lecture-7 - (Sem1!10!11) Feminism in Malaysiapeningla100% (1)

- Domovinski Rat Korica Za Knjigu 1 - Kor 2Документ1 страницаDomovinski Rat Korica Za Knjigu 1 - Kor 2api-3753366Оценок пока нет

- Suspense EssayДокумент3 страницыSuspense Essayapi-358049726Оценок пока нет

- Prophet Ibrahim Quizzes by Dalia Agha Year10 1Документ2 страницыProphet Ibrahim Quizzes by Dalia Agha Year10 1api-411887273Оценок пока нет

- What Is The Solo ParentДокумент5 страницWhat Is The Solo ParentAdrian MiraflorОценок пока нет

- Esguerra NotesДокумент38 страницEsguerra NotesjohnllenalcantaraОценок пока нет

- SC Reduces Death Penalty to Reclusion Perpetua in Rape CaseДокумент14 страницSC Reduces Death Penalty to Reclusion Perpetua in Rape CaseAndrew Neil R. NinoblaОценок пока нет

- Chevrolet Tahoe 2017 Power DistributionДокумент25 страницChevrolet Tahoe 2017 Power Distributionjorge antonio guillenОценок пока нет

- Natividad Vs DizonДокумент20 страницNatividad Vs DizonNotaly Mae Paja BadtingОценок пока нет

- Railway Recruitment Recruitment Cell, Central Railway RailwayДокумент14 страницRailway Recruitment Recruitment Cell, Central Railway RailwayAkash MhantaОценок пока нет

- Graduates Constituency Voters Enrollment Form 18Документ4 страницыGraduates Constituency Voters Enrollment Form 18DEEPAKОценок пока нет

- Christian History of AlbaniaДокумент10 страницChristian History of AlbaniaŞərif MəcidzadəОценок пока нет

- Rumun 2015 CommitteesДокумент4 страницыRumun 2015 Committeesapi-263920848Оценок пока нет

- Special Marriage Act provisions for interfaith unionsДокумент28 страницSpecial Marriage Act provisions for interfaith unionsVed AntОценок пока нет

- CSEC Tourism QuestionДокумент2 страницыCSEC Tourism QuestionJohn-Paul Mollineaux0% (1)

- You All Are The Temple of God - The Bible Project Blog - The Bible ProjectДокумент5 страницYou All Are The Temple of God - The Bible Project Blog - The Bible ProjectJoshua PrakashОценок пока нет