Вам также может понравиться

- DILG - Rationalizing The Local Planning System of The PhilippinesДокумент222 страницыDILG - Rationalizing The Local Planning System of The PhilippinesMia Monica Fojas Loyola100% (4)

- FAQ On SALN Final March2016Документ8 страницFAQ On SALN Final March2016Julius AlemanОценок пока нет

- Secretary CertificateДокумент1 страницаSecretary CertificateDominique TanОценок пока нет

- Bid Docs 2020-03-001 PDFДокумент20 страницBid Docs 2020-03-001 PDFAmanakeОценок пока нет

- Coe - Driver 1ST Batch PDFДокумент1 страницаCoe - Driver 1ST Batch PDFAmanake100% (1)

- Bid Docs 2020-03-001 PDFДокумент20 страницBid Docs 2020-03-001 PDFAmanakeОценок пока нет

- FAQ On SALN Final March2016Документ8 страницFAQ On SALN Final March2016Julius AlemanОценок пока нет

- SAMPLE - Student Intern Performance EvaluationДокумент1 страницаSAMPLE - Student Intern Performance EvaluationChristian BaseaОценок пока нет

- JOY IPO TM Search Result PDFДокумент2 страницыJOY IPO TM Search Result PDFAmanakeОценок пока нет

- Account Opening Manual For Foreign-Based CorporationsДокумент12 страницAccount Opening Manual For Foreign-Based CorporationsAmanakeОценок пока нет

- Form 2.16.3Документ9 страницForm 2.16.30307aliОценок пока нет

- Camino 2019Документ41 страницаCamino 2019AmanakeОценок пока нет

- DILG - Rationalizing The Local Planning System of The PhilippinesДокумент222 страницыDILG - Rationalizing The Local Planning System of The PhilippinesMia Monica Fojas Loyola100% (4)

- 2018 Fulbright Classic LoRДокумент2 страницы2018 Fulbright Classic LoRAvegail TolentinoОценок пока нет

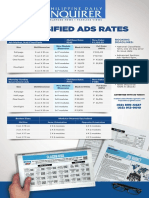

- PDI RatesДокумент1 страницаPDI RatesAmanakeОценок пока нет

- Chiropractic Application Form: Section A: Contact InformationДокумент6 страницChiropractic Application Form: Section A: Contact InformationAmanakeОценок пока нет

- CCRIFSPC HostOrganization InternAssessment FormДокумент3 страницыCCRIFSPC HostOrganization InternAssessment FormAmanakeОценок пока нет

- Board Resolution To Establish A BranchДокумент1 страницаBoard Resolution To Establish A BranchSyed Muhammad Ali SadiqОценок пока нет

- 2018 Fulbright Classic LoRДокумент2 страницы2018 Fulbright Classic LoRAvegail TolentinoОценок пока нет

- Chanrobles Lawnet, Inc.: de La Salle University (Dlsu) - College of LawДокумент3 страницыChanrobles Lawnet, Inc.: de La Salle University (Dlsu) - College of LawAkosiabandoned JorjeОценок пока нет

- Form Mm18 Editable1Документ2 страницыForm Mm18 Editable1AmanakeОценок пока нет

- Notification Form Foreign CorporationДокумент2 страницыNotification Form Foreign CorporationJenel ChuОценок пока нет

- N-lc-03 HSBC V NSC & City TrustДокумент4 страницыN-lc-03 HSBC V NSC & City TrustAndrew Gallardo100% (1)

- MCF JAR 10 (C) Motion To Allow Compliant Replacement AffidavitsДокумент3 страницыMCF JAR 10 (C) Motion To Allow Compliant Replacement AffidavitsAmanakeОценок пока нет

- MCF 3.17 Motion To Substitute Public OfficerДокумент3 страницыMCF 3.17 Motion To Substitute Public OfficerTricia CruzОценок пока нет

- Private Retirement Plans in The PhilippinesДокумент55 страницPrivate Retirement Plans in The Philippineschane15100% (2)

- MCF 58 Application For Writ of Preliminary InjunctionДокумент3 страницыMCF 58 Application For Writ of Preliminary InjunctionAndro DayaoОценок пока нет

- MCF 2.6 Motion To Sever Misjoined Cause of ActionДокумент2 страницыMCF 2.6 Motion To Sever Misjoined Cause of ActionpolbisenteОценок пока нет

- MCF Am No. 11-1-6-Sc-Philja Motion To Retain JDRДокумент2 страницыMCF Am No. 11-1-6-Sc-Philja Motion To Retain JDRAmanakeОценок пока нет

- MCF Am No. 11-1-6-Sc-Philja Motion To Retain JDRДокумент2 страницыMCF Am No. 11-1-6-Sc-Philja Motion To Retain JDRAmanakeОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Internet Banking ScopeДокумент21 страницаInternet Banking ScopeAhsan ZamanОценок пока нет

- Business Tax Reviewer IДокумент5 страницBusiness Tax Reviewer IMariefel Irish Jimenez KhuОценок пока нет

- Wricefs Requirements (Workflows, Reports, Interfaces, Conversions, Enhancements, Forms)Документ6 страницWricefs Requirements (Workflows, Reports, Interfaces, Conversions, Enhancements, Forms)aliОценок пока нет

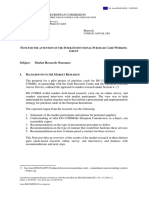

- Market Research Outcomes Note FinalДокумент27 страницMarket Research Outcomes Note FinalBraila RoОценок пока нет

- US Internal Revenue Service: I940 - 1999Документ6 страницUS Internal Revenue Service: I940 - 1999IRSОценок пока нет

- Special Instruction For Authorised Branches: Special Instruction For Authorised Branches: Special Instruction For Authorised BranchesДокумент1 страницаSpecial Instruction For Authorised Branches: Special Instruction For Authorised Branches: Special Instruction For Authorised BranchesAbdul WahabОценок пока нет

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceДокумент4 страницыStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceAman DosaniОценок пока нет

- Npower Example BillДокумент1 страницаNpower Example BillHridoy33% (3)

- India Tile Gallery 404 29-Apr-23 Immrdiate 28-Apr-23: CGST SGST Round OffДокумент1 страницаIndia Tile Gallery 404 29-Apr-23 Immrdiate 28-Apr-23: CGST SGST Round OffManya BhosaleОценок пока нет

- Tahun 4 - Peperiksaan Pertengahan Tahun - Jawapan PDFДокумент2 страницыTahun 4 - Peperiksaan Pertengahan Tahun - Jawapan PDFKanang UsopОценок пока нет

- Alan Dickeast Africa LTD: Bill-202401OC0000070796Документ1 страницаAlan Dickeast Africa LTD: Bill-202401OC0000070796jaredОценок пока нет

- Direct Taxes Sem-Iii-20Документ22 страницыDirect Taxes Sem-Iii-20Pranita MandlekarОценок пока нет

- Solved Shannon Signs A 100 000 Contract To Develop A Plan ForДокумент1 страницаSolved Shannon Signs A 100 000 Contract To Develop A Plan ForAnbu jaromiaОценок пока нет

- Seabank Statement GiselaДокумент4 страницыSeabank Statement Giseladeajohn093Оценок пока нет

- Microtek Microtek Line Interactive UPS Legend 650 Ups Legend 650 UpsДокумент1 страницаMicrotek Microtek Line Interactive UPS Legend 650 Ups Legend 650 UpsAriОценок пока нет

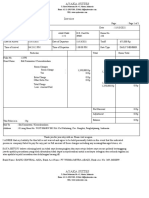

- Invoice Letter 11 Nov 2021Документ8 страницInvoice Letter 11 Nov 2021Suvi AzkaОценок пока нет

- List of Document TypesДокумент2 страницыList of Document Typesjay_kbОценок пока нет

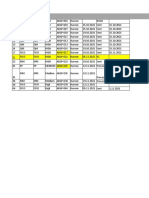

- May 2023Документ13 страницMay 2023djz24txj48Оценок пока нет

- 01 Seep 1Документ19 страниц01 Seep 1van phanОценок пока нет

- Sales Invoice PDFДокумент50 страницSales Invoice PDFAnu TinviОценок пока нет

- Analysis of The Use of Electronic Money in Efforts ToДокумент10 страницAnalysis of The Use of Electronic Money in Efforts ToFery FebriansyahОценок пока нет

- Appendix 33 - Instructions - PayrollДокумент1 страницаAppendix 33 - Instructions - Payrollpdmu regionixОценок пока нет

- Fabm 2 Module 10 Vat OptДокумент5 страницFabm 2 Module 10 Vat OptJOHN PAUL LAGAOОценок пока нет

- Capital GainДокумент4 страницыCapital GainrichaОценок пока нет

- Commercial Invoice .Документ1 страницаCommercial Invoice .krishna PatelОценок пока нет

- Cancellation List From Date 04 Nov To 04 Dec 2019 - Consolidate of Premium RefundДокумент3 страницыCancellation List From Date 04 Nov To 04 Dec 2019 - Consolidate of Premium RefundTi BetoОценок пока нет

- Jan-19 PDFДокумент2 страницыJan-19 PDFPriya Gujar100% (1)

- Taxation Reviewer FAPДокумент85 страницTaxation Reviewer FAPReyrhye RopaОценок пока нет

- PDF Format Quotation Q B H 2122 167 1Документ1 страницаPDF Format Quotation Q B H 2122 167 1Gunjan PatelОценок пока нет

- DeductionsДокумент4 страницыDeductionsDianna RabadonОценок пока нет