Вам также может понравиться

- 30 Income Tax Objective Type QuestionsДокумент25 страниц30 Income Tax Objective Type QuestionsRakesh Sharma50% (6)

- Economics AssignmentДокумент16 страницEconomics AssignmentPushpit Khare100% (1)

- Income Tax MCQ 1Документ9 страницIncome Tax MCQ 1mohammedumair100% (3)

- Calculate An EXW Import - Cargo SalesДокумент2 страницыCalculate An EXW Import - Cargo SalesKinzah AtharОценок пока нет

- Pricing: Understanding and Capturing Customer ValueДокумент31 страницаPricing: Understanding and Capturing Customer ValueAlrifai Ziad Ahmed100% (2)

- CA Final GST MCQДокумент111 страницCA Final GST MCQMayur Savakiya100% (1)

- Chapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxДокумент25 страницChapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxSonu KumarОценок пока нет

- C3-Fundamentals of Business MAthsДокумент305 страницC3-Fundamentals of Business MAthsscamardela790% (1)

- VI Sem. - Income Tax and GST MCQДокумент26 страницVI Sem. - Income Tax and GST MCQsamreen fathimaОценок пока нет

- Agricultural Licensure Examination ReviewerДокумент31 страницаAgricultural Licensure Examination ReviewerRuebenson Acabal100% (13)

- Auditing MCQsДокумент39 страницAuditing MCQsHaroon AkhtarОценок пока нет

- DT MCQs For June DecДокумент208 страницDT MCQs For June DecnaveedamurnaveedamurОценок пока нет

- MCQ of GSTДокумент23 страницыMCQ of GSTOnline tally guide100% (2)

- Goods and Services Tax: Multiple Choice QuestionsДокумент20 страницGoods and Services Tax: Multiple Choice QuestionsDhruti AthaОценок пока нет

- GST Special Question MCQ PDFДокумент11 страницGST Special Question MCQ PDFSachin SoniОценок пока нет

- Cost Accounting MCQ With Answer PDFДокумент3 страницыCost Accounting MCQ With Answer PDFMijanur Rahman100% (2)

- MCQ On GSTДокумент21 страницаMCQ On GSTSanket MhetreОценок пока нет

- Income Tax MCQ Compilation PDFДокумент76 страницIncome Tax MCQ Compilation PDFjesurajajosephОценок пока нет

- Maruti SM Project Complete AnalysisДокумент48 страницMaruti SM Project Complete AnalysisBhavin Nilesh PandyaОценок пока нет

- Cost Accounting Objective (MCQ)Документ243 страницыCost Accounting Objective (MCQ)mirjapur0% (1)

- Important MCQS-GSTДокумент47 страницImportant MCQS-GSTHrishit Raj SardaОценок пока нет

- HubSpot: Inbound Marketing and Web 2.0Документ3 страницыHubSpot: Inbound Marketing and Web 2.0test100% (1)

- Conduct ProcurementДокумент3 страницыConduct ProcurementAdrian RubicoОценок пока нет

- IPCC Audit MCQs by Vinit Mishra Sir PDFДокумент125 страницIPCC Audit MCQs by Vinit Mishra Sir PDFPrakash Gaurav100% (3)

- GST MCQДокумент73 страницыGST MCQtongocharliОценок пока нет

- Key Logistics ActivitiesДокумент2 страницыKey Logistics ActivitiesVikash Ranjan33% (3)

- Accntncy MCQs For SAS CAGДокумент12 страницAccntncy MCQs For SAS CAGDeepak Kumar PandaОценок пока нет

- ZaraДокумент5 страницZarardprawitasari100% (1)

- Custom Mcq's For Aug & Dec 2021 Exams by CA Vivek GabaДокумент35 страницCustom Mcq's For Aug & Dec 2021 Exams by CA Vivek GabaSpidy Mac100% (1)

- GST - IMP D.Tax (AKD) - 2Документ15 страницGST - IMP D.Tax (AKD) - 2algoscale techОценок пока нет

- Model Question Paper - IGST Act.: (2 Marks Each) Multiple Choice QuestionsДокумент25 страницModel Question Paper - IGST Act.: (2 Marks Each) Multiple Choice QuestionsShyam Prasad100% (1)

- MCQ'S - 1 To 50Документ12 страницMCQ'S - 1 To 50varunendra pandeyОценок пока нет

- GST Mcq'sДокумент43 страницыGST Mcq'sSuraj PawarОценок пока нет

- MCQ - Unit 2Документ15 страницMCQ - Unit 2Niraj PandeyОценок пока нет

- MCQ Module 1Документ4 страницыMCQ Module 1mohanraokp2279Оценок пока нет

- Goods-And-Services-Tax-Gst Solved MCQs (Set-4)Документ8 страницGoods-And-Services-Tax-Gst Solved MCQs (Set-4)Ayushi BhardwajОценок пока нет

- MCQ (ICAI Study Material)Документ6 страницMCQ (ICAI Study Material)Sanket Mhetre67% (3)

- GSTДокумент51 страницаGSTINDERDEEPОценок пока нет

- MCQs in Regulation of Audit AccountsДокумент17 страницMCQs in Regulation of Audit AccountsDeepankarОценок пока нет

- CA Final Direct Tax Laws - MCQ On HUFДокумент3 страницыCA Final Direct Tax Laws - MCQ On HUFAadish JainОценок пока нет

- Bank - Multiple Choice Questions (MCQS) : Unit 1: To International TradeДокумент38 страницBank - Multiple Choice Questions (MCQS) : Unit 1: To International Tradeprathmesh surveОценок пока нет

- Income Tax II B Com Sem 6 MCQДокумент23 страницыIncome Tax II B Com Sem 6 MCQdpfsopfopsfhop100% (1)

- MCQs Input Tax CreditДокумент10 страницMCQs Input Tax CreditAman GoyalОценок пока нет

- Chrome: Built For Business: Ncert Books PDFДокумент14 страницChrome: Built For Business: Ncert Books PDFRISHABH TOMARОценок пока нет

- MCQ Acc. EpfoДокумент43 страницыMCQ Acc. EpfoArushi SinghОценок пока нет

- Fill in The Blanks, True & False MCQs (Accounting Manuals)Документ13 страницFill in The Blanks, True & False MCQs (Accounting Manuals)Ratnesh RajanyaОценок пока нет

- General Financial Rules 2017 - Chapter 6: Procurement of Goods and ServicesДокумент18 страницGeneral Financial Rules 2017 - Chapter 6: Procurement of Goods and ServicesProf. Manpreet Singh GillОценок пока нет

- Auditing MCQ Unit 1 To Unit 4Документ6 страницAuditing MCQ Unit 1 To Unit 4amitОценок пока нет

- It MCQДокумент31 страницаIt MCQbigbulleye6078Оценок пока нет

- Auditing 1 PDFДокумент30 страницAuditing 1 PDFRama Krishna100% (1)

- FAQs and MCQs On GST Sep18 PDFДокумент523 страницыFAQs and MCQs On GST Sep18 PDFGiri SukumarОценок пока нет

- SET-1 Public Procurement Rule - 2004 MCQ'sДокумент3 страницыSET-1 Public Procurement Rule - 2004 MCQ'sSafiullah S/O Muhammad Asif100% (1)

- IDT MCQ's - June 21 & Dec 21 ExamsДокумент99 страницIDT MCQ's - June 21 & Dec 21 ExamsDinesh GadkariОценок пока нет

- Tally MCQДокумент7 страницTally MCQAatm Prakash100% (1)

- MCQs of Residential Status - Incidence of Tax by CA Kishan KR SirДокумент13 страницMCQs of Residential Status - Incidence of Tax by CA Kishan KR SirHetvi VoraОценок пока нет

- Ncert Books PDF: General Financial Rules 2017: WORKSДокумент3 страницыNcert Books PDF: General Financial Rules 2017: WORKSRISHABH TOMARОценок пока нет

- T.Y. B. Com Auditing (MCQ'S) by Asst. Prof. Pravin Kad (M. Com., SET, NET) 8788167249 (Документ13 страницT.Y. B. Com Auditing (MCQ'S) by Asst. Prof. Pravin Kad (M. Com., SET, NET) 8788167249 (Kadam KartikeshОценок пока нет

- Auditing and Taxation: Ty Bcom - Auditing and Taxation - MCQ - Question Bank - Compiled by Manoj VoraДокумент7 страницAuditing and Taxation: Ty Bcom - Auditing and Taxation - MCQ - Question Bank - Compiled by Manoj VoraSample Use67% (3)

- PC-5 Constitution of India, Acts and Regulation: Prepared by Deepak Kumar Rahi, AAO (AMG V/Patna)Документ34 страницыPC-5 Constitution of India, Acts and Regulation: Prepared by Deepak Kumar Rahi, AAO (AMG V/Patna)Exam Preparation Coaching ClassesОценок пока нет

- MCQ On Rti ActДокумент4 страницыMCQ On Rti ActmuthuОценок пока нет

- MCQ On TDS, TCS & Advance TaxДокумент15 страницMCQ On TDS, TCS & Advance TaxPrakhar GuptaОценок пока нет

- Account's MCQДокумент7 страницAccount's MCQMohitTagotraОценок пока нет

- Accounting Cycle McqsДокумент7 страницAccounting Cycle McqsasfandiyarОценок пока нет

- MCQ CAG StandardsДокумент11 страницMCQ CAG StandardsAjay Singh PhogatОценок пока нет

- Pension Procedure MCQ S Set-1Документ6 страницPension Procedure MCQ S Set-1Atiq0% (2)

- PC8 Answer: Capsule 16: Prepared by Deepak Kumar Rahi, AAO (LAD/Patna)Документ2 страницыPC8 Answer: Capsule 16: Prepared by Deepak Kumar Rahi, AAO (LAD/Patna)bibhorji Rusiya100% (1)

- 300+ TOP Companies Act 2013 MCQs and Answers 2021Документ11 страниц300+ TOP Companies Act 2013 MCQs and Answers 2021Bhagat DeepakОценок пока нет

- Online Bus Ticket BookingДокумент42 страницыOnline Bus Ticket BookingMythili InnconОценок пока нет

- Tybms Indirect Taxes Sem 6 Internals Sample QuestionsДокумент6 страницTybms Indirect Taxes Sem 6 Internals Sample QuestionsSarvesh MishraОценок пока нет

- MCQ - GST Answer KeyДокумент22 страницыMCQ - GST Answer KeyrupalОценок пока нет

- Project PPT (ASHA V S)Документ18 страницProject PPT (ASHA V S)vineethkmenonОценок пока нет

- Journal of Destination Marketing & Management: Giacomo Del Chiappa, Rodolfo BaggioДокумент6 страницJournal of Destination Marketing & Management: Giacomo Del Chiappa, Rodolfo BaggiovineethkmenonОценок пока нет

- How To Cite: Marikyan, D. & Papagiannidis, S. (2022) Technology Acceptance Model: AДокумент12 страницHow To Cite: Marikyan, D. & Papagiannidis, S. (2022) Technology Acceptance Model: AvineethkmenonОценок пока нет

- Chapter 14 Foundations of Behavior: True/False QuestionsДокумент35 страницChapter 14 Foundations of Behavior: True/False QuestionsvineethkmenonОценок пока нет

- Emotional Finance: Financial Anxiety Among Salaried Individuals With Special Reference To Life InsuranceДокумент13 страницEmotional Finance: Financial Anxiety Among Salaried Individuals With Special Reference To Life InsurancevineethkmenonОценок пока нет

- PG Project PPT (Revathykrishna PS)Документ24 страницыPG Project PPT (Revathykrishna PS)vineethkmenonОценок пока нет

- Camel AnalysisДокумент12 страницCamel AnalysisvineethkmenonОценок пока нет

- KMRL ProjectДокумент48 страницKMRL Projectvineethkmenon80% (10)

- Performance Evaluation of Systematic Investment Plans in Top Rated Conservative Hybrid Mutual Funds During 2016-18Документ4 страницыPerformance Evaluation of Systematic Investment Plans in Top Rated Conservative Hybrid Mutual Funds During 2016-18vineethkmenonОценок пока нет

- Teaching Aptitude For UGCДокумент13 страницTeaching Aptitude For UGCvineethkmenonОценок пока нет

- Bcom - Semester V1 Cm06Baa02 - Practcal Auditing Multiple Choice QuestionsДокумент19 страницBcom - Semester V1 Cm06Baa02 - Practcal Auditing Multiple Choice Questionsvineethkmenon100% (2)

- Bcom - Semester V Cm05Baa02 - Special Accounting Multiple Choice QuestionsДокумент14 страницBcom - Semester V Cm05Baa02 - Special Accounting Multiple Choice QuestionsvineethkmenonОценок пока нет

- Sruthy Vineeth STC Full PaperДокумент5 страницSruthy Vineeth STC Full PapervineethkmenonОценок пока нет

- Accounting For Managerial DecisionsДокумент22 страницыAccounting For Managerial DecisionsvineethkmenonОценок пока нет

- Kerala Service Rules Full - Uploaded by T James Joseph Adhikarathil, Deputy Collector Alappuzha.Документ215 страницKerala Service Rules Full - Uploaded by T James Joseph Adhikarathil, Deputy Collector Alappuzha.James AdhikaramОценок пока нет

- Core 13 Applied Ethics (4) 20 - 02Документ3 страницыCore 13 Applied Ethics (4) 20 - 02vineethkmenonОценок пока нет

- KFC FORM 7 Report of Transfer of Charge PDFДокумент2 страницыKFC FORM 7 Report of Transfer of Charge PDFvineethkmenon100% (1)

- Famous Festivals in Kerala PDFДокумент19 страницFamous Festivals in Kerala PDFvineethkmenonОценок пока нет

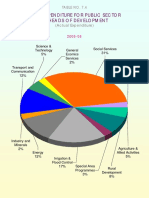

- Five Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentДокумент1 страницаFive Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentvineethkmenonОценок пока нет

- UG Model QP MergedДокумент93 страницыUG Model QP MergedvineethkmenonОценок пока нет

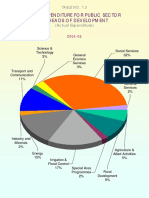

- Five Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentДокумент1 страницаFive Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentvineethkmenonОценок пока нет

- Kwÿm/ Ktωf/W: D∂X Hnzym-'Ymk A≤Ym-) I KwlwДокумент2 страницыKwÿm/ Ktωf/W: D∂X Hnzym-'Ymk A≤Ym-) I KwlwvineethkmenonОценок пока нет

- BritanniaДокумент18 страницBritanniagargharsh1988Оценок пока нет

- On Dabur Chayawanprash by Nitin Kapoor (BBA V) HДокумент17 страницOn Dabur Chayawanprash by Nitin Kapoor (BBA V) HNitsky Kpr50% (2)

- Reaction Paper FlywheelДокумент2 страницыReaction Paper FlywheelJason OsunaОценок пока нет

- InvoiceДокумент1 страницаInvoicewidya fotoОценок пока нет

- 23-Pro-0001178 Sumber Keselamatan CirebonДокумент2 страницы23-Pro-0001178 Sumber Keselamatan CirebonazharinsanОценок пока нет

- Narrative Report in PracticumДокумент8 страницNarrative Report in PracticumMichelleCanlasDavidОценок пока нет

- From Brands To IconsДокумент18 страницFrom Brands To Iconsmodyboy100% (1)

- Tax 2 Prefi Transcript Reduced FontДокумент81 страницаTax 2 Prefi Transcript Reduced FontPhil JaramilloОценок пока нет

- Tax Advice For Inheriting Real EstateДокумент2 страницыTax Advice For Inheriting Real EstatehafuchieОценок пока нет

- Misindia Cosamb (F)Документ28 страницMisindia Cosamb (F)Suman KumarОценок пока нет

- Balaji WafersДокумент9 страницBalaji Wafersagarwalsagar88100% (1)

- Business Environment ProjectДокумент13 страницBusiness Environment ProjectRaakshas GamingОценок пока нет

- Terral River Service BrochureДокумент12 страницTerral River Service BrochureTerral River ServiceОценок пока нет

- Promotional Tools 2Документ6 страницPromotional Tools 2Trương Võ Quỳnh HươngОценок пока нет

- PM Skincare Case StudyДокумент8 страницPM Skincare Case StudyUmesh GuptaОценок пока нет

- Dabur Marketing Strategy of Dabur Vatika Hair Oil & Dabur CHДокумент58 страницDabur Marketing Strategy of Dabur Vatika Hair Oil & Dabur CHNitin Solanki100% (1)

- C R I PumpsДокумент36 страницC R I PumpsAnil RajОценок пока нет

- CPIM LS Module Content A4 RДокумент1 страницаCPIM LS Module Content A4 RmfaizanzahidОценок пока нет

- A.G.Barr P.L.C.: Company ProfileДокумент23 страницыA.G.Barr P.L.C.: Company ProfileÖzil8Оценок пока нет

- Project Report On Marketing Strategies of Consumer DurablesДокумент21 страницаProject Report On Marketing Strategies of Consumer DurablesSiddhartha Durga0% (2)