Вам также может понравиться

- Adobe Systems Inc: Stock Report - August 12, 2017 - NNM Symbol: ADBE - ADBE Is in The S&P 500Документ9 страницAdobe Systems Inc: Stock Report - August 12, 2017 - NNM Symbol: ADBE - ADBE Is in The S&P 500Santi11052009Оценок пока нет

- Goldman Sachs Group Inc (The) : Stock Report - September 24, 2016 - NYS Symbol: GS - GS Is in The S&P 500Документ11 страницGoldman Sachs Group Inc (The) : Stock Report - September 24, 2016 - NYS Symbol: GS - GS Is in The S&P 500derek_2010Оценок пока нет

- S&P - AbxДокумент11 страницS&P - Abxderek_2010Оценок пока нет

- Reports CRMДокумент11 страницReports CRMderek_2010Оценок пока нет

- Reports F SLRДокумент11 страницReports F SLRderek_2010Оценок пока нет

- ExpeditorsДокумент11 страницExpeditorsderek_2010100% (1)

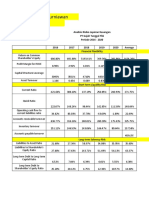

- Screenshot 2023-03-07 at 10.17.13 PMДокумент3 страницыScreenshot 2023-03-07 at 10.17.13 PMmanojmarri007Оценок пока нет

- Old Mutual Albaraka Balanced Fund: Fund Information Fund Performance As at 31/08/2021Документ2 страницыOld Mutual Albaraka Balanced Fund: Fund Information Fund Performance As at 31/08/2021Sam AbdurahimОценок пока нет

- Alphabet Inc: Stock Report - October 6, 2015 - NNM Symbol: GOOGL - GOOGL Is in The S&P 500Документ11 страницAlphabet Inc: Stock Report - October 6, 2015 - NNM Symbol: GOOGL - GOOGL Is in The S&P 500derek_2010Оценок пока нет

- Reports GGДокумент11 страницReports GGderek_2010Оценок пока нет

- Options As A Strategic Investment PDFДокумент5 страницOptions As A Strategic Investment PDFArjun Bora100% (1)

- RWC Global Emerging Equity Fund: 30th June 2020Документ2 страницыRWC Global Emerging Equity Fund: 30th June 2020Nat BanyatpiyaphodОценок пока нет

- DSP Mid Cap Fund Aug 2023Документ7 страницDSP Mid Cap Fund Aug 2023RajОценок пока нет

- RBC - ARCC - Revision - 3Q20 Review - 13 PagesДокумент13 страницRBC - ARCC - Revision - 3Q20 Review - 13 PagesSagar PatelОценок пока нет

- Apr 20, 2018 AtlassianCorporationPlc TEAMVeryGood, AgainstGreatExpectationsДокумент9 страницApr 20, 2018 AtlassianCorporationPlc TEAMVeryGood, AgainstGreatExpectationsPradeep RaghunathanОценок пока нет

- OMAlbaraka Equity FundДокумент2 страницыOMAlbaraka Equity FundArdine FickОценок пока нет

- SCHW - ZackДокумент10 страницSCHW - ZackJessyОценок пока нет

- NESTLE BHD Financial Analysis: Group 4Документ14 страницNESTLE BHD Financial Analysis: Group 4Ct TanОценок пока нет

- Kossan Rubber Industries Berhad :FY09 Core Earnings Surged 62% YoY, Beating Estimates - 01/03/2010Документ3 страницыKossan Rubber Industries Berhad :FY09 Core Earnings Surged 62% YoY, Beating Estimates - 01/03/2010Rhb InvestОценок пока нет

- OMAlbaraka Balanced FundДокумент2 страницыOMAlbaraka Balanced FundArdine FickОценок пока нет

- Return On Invested Capital (ROIC)Документ4 страницыReturn On Invested Capital (ROIC)VinodSinghОценок пока нет

- SBI initiates coverage with performer ratingДокумент20 страницSBI initiates coverage with performer ratingPraharsh SinghОценок пока нет

- HSBC Holdings PLCДокумент9 страницHSBC Holdings PLCAnonymous P73cUg73LОценок пока нет

- Patel Brijeshkumar MukeshbhaiДокумент23 страницыPatel Brijeshkumar MukeshbhaiBhaskar NapteОценок пока нет

- UTI Large Cap Fund (Formerly UTI Mastershare Unit Scheme)Документ28 страницUTI Large Cap Fund (Formerly UTI Mastershare Unit Scheme)rinkuparekh13Оценок пока нет

- Monthly investment update for Pure Stock Fund in December 2022Документ11 страницMonthly investment update for Pure Stock Fund in December 2022Rakesh Dey sarkarОценок пока нет

- Initiating Coverage by JefferiesДокумент42 страницыInitiating Coverage by JefferiesSumantha SahaОценок пока нет

- Old Mutual Top 40 Index Fund: Fund Information Fund Performance As at 31/12/2021Документ2 страницыOld Mutual Top 40 Index Fund: Fund Information Fund Performance As at 31/12/2021Ardine FickОценок пока нет

- DSP Small Cap Fund Aug 2023Документ7 страницDSP Small Cap Fund Aug 2023RajОценок пока нет

- Old Mutual Albaraka Equity Fund: Fund Information Fund Performance As at 31/08/2021Документ2 страницыOld Mutual Albaraka Equity Fund: Fund Information Fund Performance As at 31/08/2021Sam AbdurahimОценок пока нет

- EMBRAC.B - RedEyeДокумент16 страницEMBRAC.B - RedEyeJacksonОценок пока нет

- Apr 18, 2018 AtlassianCorporationPlc TEAMThoughtsAheadoftheQuarterPositiveFundamentals, RaisingTargetPriceДокумент10 страницApr 18, 2018 AtlassianCorporationPlc TEAMThoughtsAheadoftheQuarterPositiveFundamentals, RaisingTargetPricePradeep RaghunathanОценок пока нет

- Spandana Sphoorty - Stock Update - 010124Документ11 страницSpandana Sphoorty - Stock Update - 010124sapguru.inОценок пока нет

- First Resources Limited Berhad: Exponential Earnings Growth at Inexpensive - 3/6/2010Документ8 страницFirst Resources Limited Berhad: Exponential Earnings Growth at Inexpensive - 3/6/2010Rhb InvestОценок пока нет

- BTG Pactual JBSДокумент7 страницBTG Pactual JBSRodolphe JoveОценок пока нет

- For those who play to win moreДокумент4 страницыFor those who play to win moreABCОценок пока нет

- Allianz SE ResearchДокумент17 страницAllianz SE Researchphilip davisОценок пока нет

- ZENSARTECH StockReport 20240123 0818Документ13 страницZENSARTECH StockReport 20240123 0818Proton CongoОценок пока нет

- Bonesupport q4 Uncalled Share Drop Gives Attractive Entry Points 2024-02-16Документ17 страницBonesupport q4 Uncalled Share Drop Gives Attractive Entry Points 2024-02-16Antonio Rodríguez de la TorreОценок пока нет

- New O/W: Back To The Future: Countplus (CUP)Документ6 страницNew O/W: Back To The Future: Countplus (CUP)Muhammad ImranОценок пока нет

- FSD CH0497631082 SWC CH enДокумент6 страницFSD CH0497631082 SWC CH enshuzefaОценок пока нет

- Equinix, Inc.: Neutral/ModerateДокумент19 страницEquinix, Inc.: Neutral/ModerateashishkrishОценок пока нет

- Aberdeen Standard Global Emerging Markets Fund: Key Facts ObjectiveДокумент4 страницыAberdeen Standard Global Emerging Markets Fund: Key Facts ObjectiveMiknoos PutinОценок пока нет

- Eastern Pacific Industrial Corporation Berhad: No Surprises - 27/04/2010Документ3 страницыEastern Pacific Industrial Corporation Berhad: No Surprises - 27/04/2010Rhb InvestОценок пока нет

- Bfund Fund Fact Sheet For July - 2017Документ1 страницаBfund Fund Fact Sheet For July - 2017Quofi SeliОценок пока нет

- VBL StockReport 20230907 1553Документ14 страницVBL StockReport 20230907 1553Sangeethasruthi SОценок пока нет

- Etf Wealth RCH 0416fДокумент2 страницыEtf Wealth RCH 0416fMatt EbrahimiОценок пока нет

- Muthoot Finance Pick of the Week ResearchДокумент10 страницMuthoot Finance Pick of the Week ResearchPuneet367Оценок пока нет

- Kinsteel Berhad: in Line Anticipating Weaker 2H-26/05/2010Документ3 страницыKinsteel Berhad: in Line Anticipating Weaker 2H-26/05/2010Rhb InvestОценок пока нет

- XYZ Financial ModelДокумент278 страницXYZ Financial Modelhema.navaniОценок пока нет

- HKTVmall Proposal - S001 ProposalДокумент37 страницHKTVmall Proposal - S001 Proposalas7Оценок пока нет

- Factsheet - Feb 2023Документ2 страницыFactsheet - Feb 2023Vinh NguyenОценок пока нет

- OKE - ArgusДокумент5 страницOKE - ArgusJeff SturgeonОценок пока нет

- Birla Sun Life MNC FundДокумент1 страницаBirla Sun Life MNC Fundellyacool2319Оценок пока нет

- Texchem Resources Berhad: Below Expectations - 01/03/2010Документ3 страницыTexchem Resources Berhad: Below Expectations - 01/03/2010Rhb InvestОценок пока нет

- INF204K01HY3 - Reliance Smallcap FundДокумент1 страницаINF204K01HY3 - Reliance Smallcap FundKiran ChilukaОценок пока нет

- Qatar Electric Water Co 05oct11Документ24 страницыQatar Electric Water Co 05oct11xtrooz abiОценок пока нет

- MFS U.S. Growth Segregated FundДокумент1 страницаMFS U.S. Growth Segregated Fundarrow1714445dongxinОценок пока нет

- VAM World Growth B Fund Fact Sheet - April 2020Документ3 страницыVAM World Growth B Fund Fact Sheet - April 2020Ian ThaiОценок пока нет

- Irb Needle Roller Bearings 2016Документ6 страницIrb Needle Roller Bearings 2016grupa2904Оценок пока нет

- Ariete Multi Vapor Compact 4146Документ2 страницыAriete Multi Vapor Compact 4146grupa2904Оценок пока нет

- Irb Ball Joints 2016Документ1 245 страницIrb Ball Joints 2016Paulo Antonio Mora RojasОценок пока нет

- BR5 015 Link Belt S Series Intermediate Duty Ball Bearings FAQs Product SheetДокумент4 страницыBR5 015 Link Belt S Series Intermediate Duty Ball Bearings FAQs Product Sheetgrupa2904Оценок пока нет

- Why Choose Rexnord?: Valuable ExpertiseДокумент4 страницыWhy Choose Rexnord?: Valuable Expertisegrupa2904Оценок пока нет

- GBC About News Jun2011 r5Документ6 страницGBC About News Jun2011 r5grupa2904Оценок пока нет

- Inch Series Ball BearingsДокумент1 страницаInch Series Ball Bearingsgrupa2904Оценок пока нет

- Why Choose Rexnord?: Valuable ExpertiseДокумент4 страницыWhy Choose Rexnord?: Valuable Expertisegrupa2904Оценок пока нет

- Slide Bearing For Electricar Machines BrochureДокумент6 страницSlide Bearing For Electricar Machines BrochureGabriel BolívarОценок пока нет

- Renk Slide Bearings Foot Mounted ER EG 34-45 SizesДокумент8 страницRenk Slide Bearings Foot Mounted ER EG 34-45 Sizesgrupa2904Оценок пока нет

- BR5 014 Link Belt S, W Series Intermediate Duty Ball Bearings Product SheetДокумент2 страницыBR5 014 Link Belt S, W Series Intermediate Duty Ball Bearings Product Sheetgrupa2904Оценок пока нет

- Renk Slide Bearings Type GДокумент6 страницRenk Slide Bearings Type Ggrupa2904Оценок пока нет

- 1046311Документ6 страниц1046311Jose Antonio VazquezОценок пока нет

- BR5 013 Link Belt Klean Gard Ball Bearings FAQs Product SheetДокумент4 страницыBR5 013 Link Belt Klean Gard Ball Bearings FAQs Product Sheetgrupa2904Оценок пока нет

- Innovative Power Transmission Slide BearingsДокумент6 страницInnovative Power Transmission Slide BearingsharosalesvОценок пока нет

- SKF Tih220m ManualДокумент116 страницSKF Tih220m Manualgrupa2904Оценок пока нет

- Renk Slide Bearings Type HGДокумент4 страницыRenk Slide Bearings Type HGgrupa2904Оценок пока нет

- Renk Slide Bearings Type EFДокумент6 страницRenk Slide Bearings Type EFgrupa2904100% (1)

- NTN Wireless Linear Measuring SystemДокумент12 страницNTN Wireless Linear Measuring Systemgrupa2904Оценок пока нет

- RENK Slide Bearings Type EДокумент20 страницRENK Slide Bearings Type Eagnostic0750% (2)

- 3/14/2012 Quote Tabulation (09/12/2011) Page 1 of 1Документ1 страница3/14/2012 Quote Tabulation (09/12/2011) Page 1 of 1grupa2904Оценок пока нет

- SKF Standard Jaw Pullers TMMP MROДокумент2 страницыSKF Standard Jaw Pullers TMMP MROgrupa2904Оценок пока нет

- NTN Linear Axis NewsДокумент54 страницыNTN Linear Axis Newsgrupa2904Оценок пока нет

- Link Pumps Equipment Datasheet: Pump Number: PCE736Документ2 страницыLink Pumps Equipment Datasheet: Pump Number: PCE736grupa2904Оценок пока нет

- NTN Linear ModulesДокумент136 страницNTN Linear Modulesgrupa2904Оценок пока нет

- NTN Linear Ball BushingsДокумент84 страницыNTN Linear Ball Bushingsgrupa2904Оценок пока нет

- NTN Linear Axis RangeДокумент2 страницыNTN Linear Axis Rangegrupa2904Оценок пока нет

- SKF Standard Jaw Pullers TMMP MROДокумент2 страницыSKF Standard Jaw Pullers TMMP MROgrupa2904Оценок пока нет

- Timken Dial IndicatorДокумент2 страницыTimken Dial Indicatorgrupa2904Оценок пока нет

- Timken Induction Heater VHIN900Документ2 страницыTimken Induction Heater VHIN900grupa2904Оценок пока нет

- Tire City Case AnalysisДокумент10 страницTire City Case AnalysisVASANTADA SRIKANTH (PGP 2016-18)Оценок пока нет

- Fi32rk14 LR PDFДокумент44 страницыFi32rk14 LR PDFGina JamesОценок пока нет

- تمارين +الحل اداريةДокумент14 страницتمارين +الحل اداريةaec216320136Оценок пока нет

- Chapter 11 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Документ141 страницаChapter 11 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Awais Azeemi67% (3)

- DocumentДокумент26 страницDocumentLorraine Miralles33% (3)

- CAPE Accounting MCQДокумент10 страницCAPE Accounting MCQBradlee Singh100% (1)

- Income Statement: Case 1: RevenuesДокумент3 страницыIncome Statement: Case 1: RevenuesRajivОценок пока нет

- TOA Midterm Exam 2010Документ22 страницыTOA Midterm Exam 2010Patrick WaltersОценок пока нет

- Installment Liquidation Cash Priority ProgramsДокумент9 страницInstallment Liquidation Cash Priority ProgramsAtarom9Оценок пока нет

- Assignment On GAAP, AccountingДокумент7 страницAssignment On GAAP, AccountingAsma Hameed50% (2)

- Test Bank For Structure and Function of The Body 14th Edition ThibodeauДокумент24 страницыTest Bank For Structure and Function of The Body 14th Edition ThibodeauJamesNewmanazpy100% (27)

- Preparing SFP from Trial BalanceДокумент11 страницPreparing SFP from Trial BalanceRance Gerwyn OpialaОценок пока нет

- FAR q1q2Документ7 страницFAR q1q2Leane MarcoletaОценок пока нет

- Plantillas Excel Vio - IiДокумент29 страницPlantillas Excel Vio - IiEduardo Lopez-vegue DiezОценок пока нет

- 002 MAS FS Analysis Rev00 PDFДокумент5 страниц002 MAS FS Analysis Rev00 PDFCyvee Joy Hongayo OcheaОценок пока нет

- Project Report of RILДокумент53 страницыProject Report of RILeakta100% (4)

- Preliminary Income Statement and Balance Sheet for Accounting RecordsДокумент35 страницPreliminary Income Statement and Balance Sheet for Accounting RecordsRomee SinghОценок пока нет

- Appendic 5C-1 - Summarized Disclosure ChecklistДокумент8 страницAppendic 5C-1 - Summarized Disclosure ChecklistLuis Enrique Altamar RamosОценок пока нет

- PT Gajah Tunggal Tbk Financial Risk Analysis 2016-2020Документ26 страницPT Gajah Tunggal Tbk Financial Risk Analysis 2016-2020Ananda LukmanОценок пока нет

- PT Semen Indonesia Q1 2019 Consolidated Financial StatementsДокумент191 страницаPT Semen Indonesia Q1 2019 Consolidated Financial StatementsIka WinantiОценок пока нет

- Collectibles Spreadsheet AnswerДокумент26 страницCollectibles Spreadsheet Answeremre8506Оценок пока нет

- CH 13Документ45 страницCH 13Licia SalimОценок пока нет

- 11 Accountancy t2 Sp01Документ19 страниц11 Accountancy t2 Sp01Lakshy BishtОценок пока нет

- Admission of A New PartnerДокумент36 страницAdmission of A New PartnerSreekanth DogiparthiОценок пока нет

- Kotler SummaryДокумент27 страницKotler Summaryshriya2413Оценок пока нет

- Responsibility Accounting SystemДокумент13 страницResponsibility Accounting SystemTsundere DoradoОценок пока нет

- CH 2 - Financial Statements For Decision MakingДокумент38 страницCH 2 - Financial Statements For Decision MakingAwais JavedОценок пока нет

- Chapter 16-Financial Statement Analysis: Multiple ChoiceДокумент19 страницChapter 16-Financial Statement Analysis: Multiple ChoiceRodОценок пока нет

- Fair Value Measurement and ReportingДокумент79 страницFair Value Measurement and ReportingMai TrầnОценок пока нет

- Basic MasДокумент5 страницBasic MasLycka Bernadette MarceloОценок пока нет