Вам также может понравиться

- Internal Control On Notes PayableДокумент13 страницInternal Control On Notes PayableAmelia LadromaОценок пока нет

- Revenue Cycle Audit Program Final 140810Документ11 страницRevenue Cycle Audit Program Final 140810Pushkar Deodhar100% (1)

- Objectives and Phases of Operational AuditsДокумент12 страницObjectives and Phases of Operational AuditsJacqueline Ortega100% (2)

- HOMEWORK/RECITATION IN AUDITING CIS ENVIRONMENTДокумент7 страницHOMEWORK/RECITATION IN AUDITING CIS ENVIRONMENTAdam SmithОценок пока нет

- Internal Audit Engagement MemoДокумент2 страницыInternal Audit Engagement MemoJane Pham67% (3)

- Audit in CIS ModuleДокумент23 страницыAudit in CIS Modulecarl fuerzas100% (1)

- Course Title: Auditing and Assurance: Concepts and Applications 2 Course DescriptionДокумент1 страницаCourse Title: Auditing and Assurance: Concepts and Applications 2 Course DescriptionMichael Arevalo100% (1)

- Basic Concepts of Internal ControlДокумент9 страницBasic Concepts of Internal ControlRichard de LeonОценок пока нет

- Audit Planning MemoДокумент9 страницAudit Planning MemoJerald Oliver Macabaya100% (1)

- Correction of Error LECTUREДокумент3 страницыCorrection of Error LECTUREKobe bryantОценок пока нет

- CG13-CORP GOV & AUDITSДокумент18 страницCG13-CORP GOV & AUDITSjhienellОценок пока нет

- PrE5 - Auditing in A CIS EnvironmentДокумент14 страницPrE5 - Auditing in A CIS EnvironmentGlynnis EscobarОценок пока нет

- Case Study RCBCДокумент7 страницCase Study RCBCedwardoОценок пока нет

- Managing The Internal Auditing ActivityДокумент32 страницыManaging The Internal Auditing Activityoliver50% (2)

- Strategic Business AnalysisДокумент4 страницыStrategic Business AnalysisRogen Paul Geromo100% (1)

- Module 2 - Audit Process - For LMSДокумент71 страницаModule 2 - Audit Process - For LMSKrystalah CañizaresОценок пока нет

- Operational AuditsДокумент13 страницOperational Auditspankaj verma100% (2)

- CBA Rural Bank HR Strategies During the PandemicДокумент4 страницыCBA Rural Bank HR Strategies During the PandemicJamaica Elopre100% (1)

- RA 9298 Powerpoint PresentationДокумент61 страницаRA 9298 Powerpoint PresentationPUNK BEARОценок пока нет

- ACC 103 Conceptual Framework & Accounting Stds OBE SyllabusДокумент7 страницACC 103 Conceptual Framework & Accounting Stds OBE SyllabusMarco Gabriel Resñgit BeninОценок пока нет

- Chapter 1 Professional Practice of AccountancyДокумент44 страницыChapter 1 Professional Practice of AccountancyVanjo MuñozОценок пока нет

- Chapter1Документ4 страницыChapter1Keanne Armstrong100% (1)

- ACT1202.Case Study No. 1 Answer SheetДокумент4 страницыACT1202.Case Study No. 1 Answer SheetDonise Ronadel SantosОценок пока нет

- Internal Control QuestionnaireДокумент2 страницыInternal Control Questionnairepeterpancanfly100% (3)

- Chapter 20 The Computer EnvironmentДокумент13 страницChapter 20 The Computer EnvironmentClar Aaron Bautista100% (1)

- Completed Revenue CycleДокумент44 страницыCompleted Revenue CycleMir Hossain Ekram92% (13)

- Development of Financial Reporting Framework, Standard-Setting Bodies and RegulationДокумент7 страницDevelopment of Financial Reporting Framework, Standard-Setting Bodies and RegulationNoella Marie Baron100% (1)

- Cash and Cash Equivalents - Substantive Tests of Details of BalancesДокумент34 страницыCash and Cash Equivalents - Substantive Tests of Details of Balancesyen clave0% (1)

- Subjects Icare Resa: MAS FAR Afar TOA TAX RFBT AT APДокумент14 страницSubjects Icare Resa: MAS FAR Afar TOA TAX RFBT AT APlloydОценок пока нет

- Theory of Accounts - Valix - CinEquityДокумент10 страницTheory of Accounts - Valix - CinEquityMaryrose Gestoso0% (1)

- Philippine SEC Mandate and FunctionsДокумент2 страницыPhilippine SEC Mandate and FunctionsfccarlosОценок пока нет

- Strategic Tax Management ReviewerДокумент47 страницStrategic Tax Management ReviewerJoyce Macatangay100% (1)

- IT Database Systems Audit GuideДокумент9 страницIT Database Systems Audit GuideAngeline SahagunОценок пока нет

- Ethics, Fraud, and Internal ControlДокумент49 страницEthics, Fraud, and Internal ControlAzizah Syarif100% (3)

- Audit in Computerized EnvironmentДокумент2 страницыAudit in Computerized Environmentrajahmati_280% (1)

- True & FalseДокумент13 страницTrue & FalseYasir Ali Gillani100% (2)

- Chapter 2 OpaudДокумент5 страницChapter 2 OpaudMelissa Kayla ManiulitОценок пока нет

- Strategic Cost Management GuideДокумент27 страницStrategic Cost Management GuideGabrielle Anne MagsanocОценок пока нет

- PAS-PFRS FinalДокумент107 страницPAS-PFRS FinalPaul Christian H. BelaosОценок пока нет

- 2.agency Problem Principal-AgentДокумент6 страниц2.agency Problem Principal-AgentJudith Castro100% (1)

- Independent Analysis of Pharmally FinancialsДокумент12 страницIndependent Analysis of Pharmally FinancialsNami BuanОценок пока нет

- Practice Set Module 3 INTERNAL CONTROLSДокумент59 страницPractice Set Module 3 INTERNAL CONTROLSKrystalah CañizaresОценок пока нет

- Chapter 25 - Substantive Test of LiabilitiesДокумент10 страницChapter 25 - Substantive Test of LiabilitiesQuijano GpokskieОценок пока нет

- Activity-3 WongCarmelaДокумент1 страницаActivity-3 WongCarmelaCarmela WongОценок пока нет

- IIA Working PapersДокумент4 страницыIIA Working Papersboludu100% (1)

- Internal Control Systems at Seven ElevenДокумент5 страницInternal Control Systems at Seven ElevenFaisal KhanОценок пока нет

- Audit Theory Case AnalysisДокумент2 страницыAudit Theory Case AnalysisSheila Mary GregorioОценок пока нет

- Classwork - Valuations 011621 PDFДокумент2 страницыClasswork - Valuations 011621 PDFJasmine Acta0% (2)

- Audit Liabilities Completeness ProceduresДокумент3 страницыAudit Liabilities Completeness ProceduresJobby Jaranilla100% (1)

- Chapter 2 IT Governance and Management of ITДокумент125 страницChapter 2 IT Governance and Management of ITchelle100% (1)

- Introduction to Assurance, Auditing and Related ServicesДокумент4 страницыIntroduction to Assurance, Auditing and Related ServicesmymyОценок пока нет

- Auditing in Specialized Industries (Notes)Документ10 страницAuditing in Specialized Industries (Notes)Jene LmОценок пока нет

- NFJPIA Online Preboard Exam Tax UnformattedДокумент22 страницыNFJPIA Online Preboard Exam Tax UnformattedYietОценок пока нет

- Activity-Based CostingДокумент2 страницыActivity-Based CostingClaire BarbaОценок пока нет

- Understanding Internal ControlsДокумент4 страницыUnderstanding Internal ControlsGlaizzaОценок пока нет

- Summary of Pas 36Документ5 страницSummary of Pas 36Elijah MontefalcoОценок пока нет

- SOX and ERPДокумент10 страницSOX and ERPVanshika KhannaОценок пока нет

- Lesson 1 Governance Additional NotesДокумент6 страницLesson 1 Governance Additional NotesCarmela Tuquib RebundasОценок пока нет

- Oil Deregulation in The PhilippinesДокумент4 страницыOil Deregulation in The PhilippinesJОценок пока нет

- Deadlines TaxДокумент3 страницыDeadlines TaxLouremie Delos Reyes MalabayabasОценок пока нет

- Tax Study PlanДокумент2 страницыTax Study PlanJamesОценок пока нет

- Study Smarter and Remember More With The Power of Learning ScienceДокумент23 страницыStudy Smarter and Remember More With The Power of Learning ScienceJОценок пока нет

- Taxation LAW: I. General PrinciplesДокумент5 страницTaxation LAW: I. General PrinciplesclarizzzОценок пока нет

- Pas 24 Related Party DisclosuresДокумент1 страницаPas 24 Related Party DisclosuresJОценок пока нет

- Investment in Debt or EquityДокумент67 страницInvestment in Debt or EquityVeeresh HugarОценок пока нет

- Malong Filipino ArtДокумент1 страницаMalong Filipino ArtJОценок пока нет

- Management QB (Ecco, Law)Документ8 страницManagement QB (Ecco, Law)JОценок пока нет

- Finding Correcting ErrorsДокумент6 страницFinding Correcting ErrorsJОценок пока нет

- Pas 2 InventoryДокумент8 страницPas 2 InventoryMark Lord Morales BumagatОценок пока нет

- Auditing Theory - WILEYДокумент21 страницаAuditing Theory - WILEYCyd Chary Limbaga BiadnesОценок пока нет

- NFJPIA Mockboard 2011 P1Документ7 страницNFJPIA Mockboard 2011 P1jhefster_81Оценок пока нет

- Basic Accounting 1: WorksheetДокумент1 страницаBasic Accounting 1: WorksheetJОценок пока нет

- Management Consultancy Finals ReviewДокумент20 страницManagement Consultancy Finals ReviewGerlie89% (9)

- Management QB (Ecco, Law)Документ8 страницManagement QB (Ecco, Law)JОценок пока нет

- Far JpiaДокумент14 страницFar JpiaJОценок пока нет

- FAR Test BankДокумент36 страницFAR Test BankMangoStarr Aibelle VegasОценок пока нет

- Advanced Accounting Baker Test Bank - Chap014Документ34 страницыAdvanced Accounting Baker Test Bank - Chap014donkazotey100% (1)

- Budget TerminologiesДокумент3 страницыBudget TerminologiesYsabelle TagarumaОценок пока нет

- Advanced Accounting Baker Test Bank - Chap020Документ31 страницаAdvanced Accounting Baker Test Bank - Chap020donkazotey100% (2)

- Management QB (Ecco, Law)Документ8 страницManagement QB (Ecco, Law)JОценок пока нет

- Using HoweverДокумент2 страницыUsing Howeverj0r1zОценок пока нет

- GlossaryДокумент16 страницGlossaryEmmanuel AbadОценок пока нет

- Abs-Cbn Broadcasting Corporation, Petitioners,: vs. Honorable Court of Appeals, RepublicДокумент19 страницAbs-Cbn Broadcasting Corporation, Petitioners,: vs. Honorable Court of Appeals, RepublicJОценок пока нет

- Intermediate Accounting Millan Solution Manual PDFДокумент3 страницыIntermediate Accounting Millan Solution Manual PDFRoldan Hiano Manganip13% (8)

- Notes On Depreciation Class-11Документ5 страницNotes On Depreciation Class-11Suresh Kumar100% (1)

- FIN254 Project NSU (Excel File)Документ6 страницFIN254 Project NSU (Excel File)Sirazum SaadОценок пока нет

- Financial Statements GuideДокумент18 страницFinancial Statements GuideNadjmeah AbdillahОценок пока нет

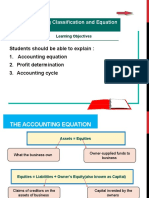

- Accounting Equation and Profit DeterminationДокумент19 страницAccounting Equation and Profit DeterminationNor LailyОценок пока нет

- Topic 3 - Impairment - SVДокумент4 страницыTopic 3 - Impairment - SVHuỳnh Minh Gia Hào100% (2)

- Pas32 & 39Документ27 страницPas32 & 39LynDioquinoОценок пока нет

- Governance in Financial Institutions (GFI) - Question SolutionДокумент11 страницGovernance in Financial Institutions (GFI) - Question Solutionnajneen khatunОценок пока нет

- Cfas ReviewerДокумент7 страницCfas ReviewerDarlene Angela IcasiamОценок пока нет

- CGT F6 Fa 20Документ35 страницCGT F6 Fa 20Wajih RehmanОценок пока нет

- SJD Online: Instructions ManualДокумент12 страницSJD Online: Instructions ManualClke OGОценок пока нет

- Midterm - ReviewerДокумент11 страницMidterm - Reviewerangel ciiiОценок пока нет

- Government AccountingДокумент2 страницыGovernment AccountingJoody CatacutanОценок пока нет

- CRS Index & FormatsДокумент24 страницыCRS Index & FormatsVenkat UppalapatiОценок пока нет

- Mgt101 - 1 - Basics of Financial AccountingДокумент64 страницыMgt101 - 1 - Basics of Financial AccountingMT MalikОценок пока нет

- F. Financial Aspect-FinalДокумент16 страницF. Financial Aspect-FinalRedier Red100% (1)

- Student Number (UWL Registration Number) : 21452742 Assignment Name: Consolidation and Analysis On The MusicalДокумент19 страницStudent Number (UWL Registration Number) : 21452742 Assignment Name: Consolidation and Analysis On The MusicalSavithri NandadasaОценок пока нет

- Single 287967086580186410492Документ13 страницSingle 287967086580186410492carlОценок пока нет

- JDW Accounts 2010Документ74 страницыJDW Accounts 2010Atif Ahmad Khan100% (1)

- Paparan Proses Bisnis Divisi Bisnis Strategis & Investasi LangsungДокумент26 страницPaparan Proses Bisnis Divisi Bisnis Strategis & Investasi LangsungNadya AsmarantakaОценок пока нет

- Subsidiaries of The Brink's CompanyДокумент6 страницSubsidiaries of The Brink's Companyradu victor TapuОценок пока нет

- How To Account For Investment in Gold Under IFRS - CPDbox - Making IFRS EasyДокумент13 страницHow To Account For Investment in Gold Under IFRS - CPDbox - Making IFRS Easytunlinoo.067433Оценок пока нет

- ReillyBrown IAPM 11e PPT Ch08Документ97 страницReillyBrown IAPM 11e PPT Ch08rocky wongОценок пока нет

- Module Two QuizzerДокумент23 страницыModule Two QuizzerFery AnnОценок пока нет

- Finlord Traders RatiosДокумент6 страницFinlord Traders RatiosMUINDI MUASYA KENNEDY D190/18836/2020Оценок пока нет

- Investment Criterias: Concept Questions and Exercisescorporate Finance 11E by Ross, Westerfield, JaffeДокумент8 страницInvestment Criterias: Concept Questions and Exercisescorporate Finance 11E by Ross, Westerfield, JaffeAnh Tram100% (1)

- The Manufacturers Life Insurance Co., Plaintiff-Internal Revenue, Defendant-AppelleeДокумент6 страницThe Manufacturers Life Insurance Co., Plaintiff-Internal Revenue, Defendant-AppelleeJade ClementeОценок пока нет

- Preference Share Capital Does Not Decrease Outstanding Shares Does Not Decrease Declaration Outstanding Shares Treasury Shares, RFHBДокумент2 страницыPreference Share Capital Does Not Decrease Outstanding Shares Does Not Decrease Declaration Outstanding Shares Treasury Shares, RFHBMaryrose SumulongОценок пока нет

- Introduction To Business Finance: An OverviewДокумент48 страницIntroduction To Business Finance: An OverviewEllen Mae PrincipeОценок пока нет

- Dividends and Other Payouts: Chapter NineteenДокумент53 страницыDividends and Other Payouts: Chapter NineteenAli AhmadОценок пока нет