Вам также может понравиться

- DD Regina CapitalДокумент7 страницDD Regina CapitalzpmellaОценок пока нет

- Polaris Software Laboratories LTDДокумент23 страницыPolaris Software Laboratories LTDwebrohanОценок пока нет

- NewletterДокумент2 страницыNewletterdianedkjОценок пока нет

- Emkay 20080122 Hindustan ConstructionДокумент6 страницEmkay 20080122 Hindustan ConstructionAnkita DasotОценок пока нет

- Pricol Limited - Broker Research - 2017 PDFДокумент25 страницPricol Limited - Broker Research - 2017 PDFnishthaОценок пока нет

- Broker Report ViewДокумент3 страницыBroker Report ViewEdrian PentadoОценок пока нет

- GodrejProperties 1308472713Документ1 страницаGodrejProperties 1308472713Sabine SmittersОценок пока нет

- Wipro CompanyUpdate22Nov21 ResearchДокумент6 страницWipro CompanyUpdate22Nov21 Researchde natureshopОценок пока нет

- OTB - 170623 - Still A Nice Cup of Coffee - ADBSДокумент10 страницOTB - 170623 - Still A Nice Cup of Coffee - ADBSNishanth K SОценок пока нет

- RIDДокумент8 страницRIDrobpatel408Оценок пока нет

- Bharati Airtel 2Документ3 страницыBharati Airtel 2Srinivas NandikantiОценок пока нет

- JM Financial - Initiating CoverageДокумент11 страницJM Financial - Initiating Coveragerchawdhry123Оценок пока нет

- Value Investor Insight Jan 31 2021Документ20 страницValue Investor Insight Jan 31 2021Gabriel AntonieОценок пока нет

- Pidilite Industries: Robust Recovery Margin Pressure AheadДокумент15 страницPidilite Industries: Robust Recovery Margin Pressure AheadIS group 7Оценок пока нет

- Official ProjectДокумент10 страницOfficial ProjectMOVIES SHOPОценок пока нет

- Dixon Q1 Result UpdateДокумент7 страницDixon Q1 Result UpdateshrikantbodkeОценок пока нет

- Voltas FirstcallДокумент25 страницVoltas Firstcallrajivkum@indiatimes.com100% (1)

- ASIA IVALUE Business ProfileДокумент9 страницASIA IVALUE Business ProfileDidiek PriambudiОценок пока нет

- Aditya Birla Nuvo 2008 2009Документ172 страницыAditya Birla Nuvo 2008 2009RamaОценок пока нет

- Anant Raj Limited321Документ12 страницAnant Raj Limited321Siddharth ShekharОценок пока нет

- Pandora Media Init Jul 18Документ20 страницPandora Media Init Jul 18Dave LiОценок пока нет

- Star River Electronics Ltd.Документ26 страницStar River Electronics Ltd.Zairah AcuñaОценок пока нет

- Ambani OrganicsДокумент3 страницыAmbani OrganicsSam vermОценок пока нет

- Care Ratings Limited (Care) : Background Stock Performance DetailsДокумент5 страницCare Ratings Limited (Care) : Background Stock Performance DetailsAshutosh GuptaОценок пока нет

- STFC Corporate Presentation Q1 FY17 June 2016Документ43 страницыSTFC Corporate Presentation Q1 FY17 June 2016Aman SinghОценок пока нет

- PratibhaInd 18 Jan 2010Документ6 страницPratibhaInd 18 Jan 2010atmaram9999Оценок пока нет

- 5 - Cost of Cap UploadДокумент4 страницы5 - Cost of Cap UploadMayank RanjanОценок пока нет

- Spec - Progress Residential - Senior Vice President, Investments - 2019Документ6 страницSpec - Progress Residential - Senior Vice President, Investments - 2019michael zОценок пока нет

- Buy Reliance CapitalДокумент3 страницыBuy Reliance Capitaldps_virusОценок пока нет

- CMP: Rs. 444 Weight:7%: Dilip Buildcon LTDДокумент9 страницCMP: Rs. 444 Weight:7%: Dilip Buildcon LTDMehran AvОценок пока нет

- Indian Real Estate - Competitive Analysis - VikramJethwaniДокумент10 страницIndian Real Estate - Competitive Analysis - VikramJethwaniVikramJethwani100% (2)

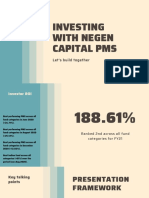

- Investing With Negen Capital PMS: Let's Build TogetherДокумент12 страницInvesting With Negen Capital PMS: Let's Build TogetherSumit SagarОценок пока нет

- Professional Landscape Company ProfileДокумент1 страницаProfessional Landscape Company Profilesreekumar sОценок пока нет

- Saratoga Investor Relation Presentation 9M19 Final - PublicДокумент15 страницSaratoga Investor Relation Presentation 9M19 Final - Publicsigitsutoko8765Оценок пока нет

- Barclays WMG U.S. Media - DIS - Still Early in The Reset PhaseДокумент27 страницBarclays WMG U.S. Media - DIS - Still Early in The Reset PhaseraymanОценок пока нет

- FSB - 01 - Idcl (1) 2Документ3 страницыFSB - 01 - Idcl (1) 2Siri VallabhaneniОценок пока нет

- PGDM QP Cval Set 1Документ2 страницыPGDM QP Cval Set 1sanket patilОценок пока нет

- LPX - RBC Deep DiveДокумент36 страницLPX - RBC Deep DiveBryan DavisОценок пока нет

- JP Morgan Singapore DevelopersДокумент55 страницJP Morgan Singapore DevelopersShadow_Warrior88Оценок пока нет

- Pantaloon Retail (India) LTD (PANRET) : Healthy Same-Store Sales GrowthДокумент7 страницPantaloon Retail (India) LTD (PANRET) : Healthy Same-Store Sales Growthavi_kamathОценок пока нет

- RHB Equity 360° - 19 October 2010 (ILB, Public Bank Technical: Ann Joo)Документ3 страницыRHB Equity 360° - 19 October 2010 (ILB, Public Bank Technical: Ann Joo)Rhb InvestОценок пока нет

- Sea Ltd. (SE) - Earnings Review - Upbeat Guidance, Strong Growth Buy (On CL)Документ12 страницSea Ltd. (SE) - Earnings Review - Upbeat Guidance, Strong Growth Buy (On CL)Poen, Chris ChouОценок пока нет

- Stock Update: Divis LaboratoriesДокумент3 страницыStock Update: Divis LaboratoriesdarshanmadeОценок пока нет

- SpiceJet Q2 Results Net Loss Narrows To Rs 449 CДокумент1 страницаSpiceJet Q2 Results Net Loss Narrows To Rs 449 Cmuhammedrafick98Оценок пока нет

- BP Equities Keystone Realtors LTD IPO Note Subscribe 13th Nov 2022Документ4 страницыBP Equities Keystone Realtors LTD IPO Note Subscribe 13th Nov 2022al.ramasamyОценок пока нет

- Motilal Oswal 12th Wealth Creation Study 2007Документ48 страницMotilal Oswal 12th Wealth Creation Study 2007motilaloswalwcsОценок пока нет

- Gaining Loan Momentum: Yes BankДокумент13 страницGaining Loan Momentum: Yes BankYGОценок пока нет

- Apea Asia Philippines Hall of Fame PH 2018 Reyes Tacandong CoДокумент3 страницыApea Asia Philippines Hall of Fame PH 2018 Reyes Tacandong CoSéan NuñezaОценок пока нет

- Pengaruh Perputaran Modal Kerja, Kebijakan Deviden Dan Rasio Hutang Terhadap Nilai Perusahaandengan Profitabilitas Sebagai VariabelinterveningДокумент16 страницPengaruh Perputaran Modal Kerja, Kebijakan Deviden Dan Rasio Hutang Terhadap Nilai Perusahaandengan Profitabilitas Sebagai Variabelinterveningchristin lingОценок пока нет

- Dubai Real Times Jul 09Документ50 страницDubai Real Times Jul 09Fa Hian100% (4)

- Team - K - CFA - Challenge - 84 - 8 (LOCALIZA)Документ29 страницTeam - K - CFA - Challenge - 84 - 8 (LOCALIZA)Giovanna WaldОценок пока нет

- Piramal Enterprises - MOStДокумент8 страницPiramal Enterprises - MOStdarshanmadeОценок пока нет

- Investor Deck Citi 2019Документ43 страницыInvestor Deck Citi 2019Sodade TourОценок пока нет

- 733pgdm QP Cval Set 1Документ3 страницы733pgdm QP Cval Set 1sanket patilОценок пока нет

- Chruch Ill DownsДокумент17 страницChruch Ill DownsMichael OzanianОценок пока нет

- Enrichment-Situational Analysis: Performance Task 1Документ4 страницыEnrichment-Situational Analysis: Performance Task 1Nekojay Almadrones100% (1)

- GOCH Report - WordДокумент18 страницGOCH Report - WordMattОценок пока нет

- Curing Corporate Short-Termism: Future Growth vs. Current EarningsОт EverandCuring Corporate Short-Termism: Future Growth vs. Current EarningsОценок пока нет

- Raising Venture Capital for the Serious EntrepreneurОт EverandRaising Venture Capital for the Serious EntrepreneurРейтинг: 3 из 5 звезд3/5 (4)

- The DAP Strategy: A New Way of Working to De-Risk & Accelerate Your Digital TransformationОт EverandThe DAP Strategy: A New Way of Working to De-Risk & Accelerate Your Digital TransformationОценок пока нет

- China Inflation Monitor (Jan 16) PDFДокумент2 страницыChina Inflation Monitor (Jan 16) PDFzpmellaОценок пока нет

- Commodities Weekly Wrap (8th Jan 2016) PDFДокумент5 страницCommodities Weekly Wrap (8th Jan 2016) PDFzpmellaОценок пока нет

- China Economics Update - RMB, Outflows (Jan 16) PDFДокумент1 страницаChina Economics Update - RMB, Outflows (Jan 16) PDFzpmellaОценок пока нет

- Weekly Farmgate, Wholesale and Retail Prices of Palay, Rice and Corn, July 2018 (Week 4)Документ2 страницыWeekly Farmgate, Wholesale and Retail Prices of Palay, Rice and Corn, July 2018 (Week 4)zpmellaОценок пока нет

- China Economics Update - Growth Vs Markets (Jan 16) PDFДокумент1 страницаChina Economics Update - Growth Vs Markets (Jan 16) PDFzpmellaОценок пока нет

- Weekly Farmgate, Wholesale and Retail Prices of Palay, Rice and Corn, by Region, August 2018 (Week 4)Документ3 страницыWeekly Farmgate, Wholesale and Retail Prices of Palay, Rice and Corn, by Region, August 2018 (Week 4)zpmellaОценок пока нет

- Cover Sheet: Company NameДокумент74 страницыCover Sheet: Company NamezpmellaОценок пока нет

- Weekly Farmgate, Wholesale and Retail Prices of Palay, Rice and Corn, August 2018 (Week 4)Документ2 страницыWeekly Farmgate, Wholesale and Retail Prices of Palay, Rice and Corn, August 2018 (Week 4)zpmellaОценок пока нет

- CMOHistorical Data MonthlyДокумент295 страницCMOHistorical Data MonthlyzpmellaОценок пока нет

- Weekly Farmgate, Wholesale and Retail Prices of Palay, Rice and Corn, July 2018 (Week 4)Документ2 страницыWeekly Farmgate, Wholesale and Retail Prices of Palay, Rice and Corn, July 2018 (Week 4)zpmellaОценок пока нет

- Weekly Farmgate, Wholesale and Retail Prices of Palay, Rice and Corn, June 2018 (Week 5)Документ2 страницыWeekly Farmgate, Wholesale and Retail Prices of Palay, Rice and Corn, June 2018 (Week 5)zpmellaОценок пока нет

- Global Policy Uncertainty DataДокумент6 страницGlobal Policy Uncertainty DatazpmellaОценок пока нет

- MZMSLДокумент15 страницMZMSLzpmellaОценок пока нет

- INDPROДокумент22 страницыINDPRODan McОценок пока нет

- US Policy Uncertainty DataДокумент24 страницыUS Policy Uncertainty DatazpmellaОценок пока нет

- Xurpas Inc - 2018 Gis08162018180414 PDFДокумент10 страницXurpas Inc - 2018 Gis08162018180414 PDFzpmellaОценок пока нет

- US Historical EPU DataДокумент66 страницUS Historical EPU DatazpmellaОценок пока нет

- 2016 STORM Flex Report-Min PDFДокумент10 страниц2016 STORM Flex Report-Min PDFzpmellaОценок пока нет

- Cover Sheet: Company NameДокумент79 страницCover Sheet: Company NamezpmellaОценок пока нет

- Xurpas Inc. 2016 Annual Report PDFДокумент165 страницXurpas Inc. 2016 Annual Report PDFzpmellaОценок пока нет

- 1QFS 2017 Final PDFДокумент77 страниц1QFS 2017 Final PDFzpmellaОценок пока нет

- Xurpas - 2Q 2018 Consolidated FS FINAL PDFДокумент84 страницыXurpas - 2Q 2018 Consolidated FS FINAL PDFzpmellaОценок пока нет

- Xurpas Inc. SEC 18-A PDFДокумент5 страницXurpas Inc. SEC 18-A PDFzpmellaОценок пока нет

- Xurpas - 2Q 2018 Consolidated FS FINAL PDFДокумент84 страницыXurpas - 2Q 2018 Consolidated FS FINAL PDFzpmellaОценок пока нет

- Xis 2Q2016 17Q Final PDFДокумент70 страницXis 2Q2016 17Q Final PDFzpmellaОценок пока нет

- 2Q 2018 Xurpas Analyst Briefing Transcript PDFДокумент6 страниц2Q 2018 Xurpas Analyst Briefing Transcript PDFzpmellaОценок пока нет

- 1Q 2018 Xurpas Analyst Briefing PDFДокумент3 страницы1Q 2018 Xurpas Analyst Briefing PDFzpmellaОценок пока нет

- How Emotionally Intelligent Are You Wong and Law Emotional Intelligence Scale WLEISДокумент2 страницыHow Emotionally Intelligent Are You Wong and Law Emotional Intelligence Scale WLEISIsabela Bică100% (2)

- Phed 239 Syllabus s14-1st Half-3Документ7 страницPhed 239 Syllabus s14-1st Half-3api-249627241Оценок пока нет

- Visual Development Milestones and Visual Acuity Assessment in ChildrenДокумент2 страницыVisual Development Milestones and Visual Acuity Assessment in ChildrenNikhil Maha DevanОценок пока нет

- Ir21 Geomt 2022-01-28Документ23 страницыIr21 Geomt 2022-01-28Master MasterОценок пока нет

- Hormones MTFДокумент19 страницHormones MTFKarla Dreams71% (7)

- John Zink - Flare - Upstream - ProductionДокумент20 страницJohn Zink - Flare - Upstream - ProductionJose Bijoy100% (2)

- Information Analyzer Data Quality Rules Implementations Standard Practices - 01052012Документ94 страницыInformation Analyzer Data Quality Rules Implementations Standard Practices - 01052012abreddy2003Оценок пока нет

- Breast Stimulation Susilowati 2004138Документ11 страницBreast Stimulation Susilowati 2004138Ahmad SaifuddinОценок пока нет

- IEM Notes Unit-2Документ2 страницыIEM Notes Unit-2Ashish YadavОценок пока нет

- Malatras ChristosДокумент13 страницMalatras Christosdimco2007Оценок пока нет

- Thesis Report On: Bombax InsigneДокумент163 страницыThesis Report On: Bombax InsigneShazedul Islam SajidОценок пока нет

- A Beginner Guide To Website Speed OptimazationДокумент56 страницA Beginner Guide To Website Speed OptimazationVijay KumarОценок пока нет

- Contents:: 1. Introduction To Neural NetworksДокумент27 страницContents:: 1. Introduction To Neural NetworksKarthik VanamОценок пока нет

- 112-1 中英筆譯Документ15 страниц112-1 中英筆譯beenbenny825Оценок пока нет

- Find and Replace in Ms WordДокумент4 страницыFind and Replace in Ms WordMahroof YounasОценок пока нет

- Assessment - Manage Quality Customer Service - BSBCUS501 PDFДокумент29 страницAssessment - Manage Quality Customer Service - BSBCUS501 PDFEricKang26% (19)

- IA Feedback Template RevisedДокумент1 страницаIA Feedback Template RevisedtyrramОценок пока нет

- National Social Protection Strategy GhanaДокумент95 страницNational Social Protection Strategy GhanaSisiraPinnawalaОценок пока нет

- Life Cycle For GilletteДокумент12 страницLife Cycle For Gillettesonia100% (1)

- Civil Law - Persons FamilyДокумент59 страницCivil Law - Persons FamilyCharmaine MejiaОценок пока нет

- 2 Cor 37Документ2 страницы2 Cor 37M. Div ChoudhrayОценок пока нет

- Kerala University PHD Course Work Exam SyllabusДокумент4 страницыKerala University PHD Course Work Exam Syllabuslozuzimobow3100% (2)

- Answers For TimesetДокумент11 страницAnswers For TimesetMuntazirОценок пока нет

- Report Why EvolveДокумент11 страницReport Why EvolveMirela OlarescuОценок пока нет

- Word FormationДокумент3 страницыWord Formationamalia9bochisОценок пока нет

- Gender Roles As Seen Through Wedding Rituals in A Rural Uyghur Community, in The Southern Oases of The Taklamakan Desert (#463306) - 541276Документ26 страницGender Roles As Seen Through Wedding Rituals in A Rural Uyghur Community, in The Southern Oases of The Taklamakan Desert (#463306) - 541276Akmurat MeredovОценок пока нет

- Social Defence Vision 2020: Dr. Hira Singh Former Director National Institute of Social DefenceДокумент19 страницSocial Defence Vision 2020: Dr. Hira Singh Former Director National Institute of Social DefencePASION Jovelyn M.Оценок пока нет

- All IL Corporate Filings by The Save-A-Life Foundation (SALF) Including 9/17/09 Dissolution (1993-2009)Документ48 страницAll IL Corporate Filings by The Save-A-Life Foundation (SALF) Including 9/17/09 Dissolution (1993-2009)Peter M. HeimlichОценок пока нет

- Pain Assessment AND Management: Mr. Swapnil Wanjari Clinical InstructorДокумент27 страницPain Assessment AND Management: Mr. Swapnil Wanjari Clinical InstructorSWAPNIL WANJARIОценок пока нет

- Pedagogue in The ArchiveДокумент42 страницыPedagogue in The ArchivePaula LombardiОценок пока нет