Вам также может понравиться

- MAS Handout CH4 DiffCostAnaДокумент2 страницыMAS Handout CH4 DiffCostAnaAbigail TumabaoОценок пока нет

- Income Tax On Individual TaxpayersДокумент7 страницIncome Tax On Individual TaxpayersYoite MiharuОценок пока нет

- MAS Bobadilla-Risk - Leverage PDFДокумент7 страницMAS Bobadilla-Risk - Leverage PDFrandyОценок пока нет

- 8 Capital Budgeting - Problems - With AnswersДокумент15 страниц8 Capital Budgeting - Problems - With AnswersIamnti domnateОценок пока нет

- 1.3 Responsibility Accounting Problems AnswersДокумент5 страниц1.3 Responsibility Accounting Problems AnswersAsnarizah PakinsonОценок пока нет

- Finals Manaco2Документ6 страницFinals Manaco2Kenneth Bryan Tegerero Tegio100% (1)

- Management Advisory Services Second Pre-Board Examinations Multiple Choice: Shade The Box Corresponding To Your Answer On The Answer SheetДокумент15 страницManagement Advisory Services Second Pre-Board Examinations Multiple Choice: Shade The Box Corresponding To Your Answer On The Answer SheetRhad EstoqueОценок пока нет

- General Ledger Would Always Be Current After Every Transaction But The Operating Efficiency May Be Affected Depending On The Size of The Company and The Number of Transactions That Are ProcessedДокумент2 страницыGeneral Ledger Would Always Be Current After Every Transaction But The Operating Efficiency May Be Affected Depending On The Size of The Company and The Number of Transactions That Are ProcessedRaca DesuОценок пока нет

- Capital BudgetingДокумент24 страницыCapital BudgetingInocencio Tiburcio100% (2)

- Reviewer For STANDARD COSTINGДокумент4 страницыReviewer For STANDARD COSTINGSajhieeОценок пока нет

- Cpa Review School of The Philippines: Management Advisory Services AGE OFДокумент9 страницCpa Review School of The Philippines: Management Advisory Services AGE OFJohn Carlo CruzОценок пока нет

- Management Advisory Services - Part 1Документ35 страницManagement Advisory Services - Part 1For AcadsОценок пока нет

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoДокумент6 страницManila Cavite Laguna Cebu Cagayan de Oro Davaovane rondinaОценок пока нет

- Assignment #1 OH Variance With SolutionДокумент14 страницAssignment #1 OH Variance With SolutionJeannet LagcoОценок пока нет

- CA 51014 - Strategic Cost Management Capital BudgetingДокумент9 страницCA 51014 - Strategic Cost Management Capital BudgetingMark FloresОценок пока нет

- San Sebastian College Recoletos de Cavite Management Accounting Finals Christopher C. LimДокумент5 страницSan Sebastian College Recoletos de Cavite Management Accounting Finals Christopher C. LimAllyssa Kassandra LucesОценок пока нет

- Mantuhac, Anthony BSA-3Документ3 страницыMantuhac, Anthony BSA-3Anthony Tunying MantuhacОценок пока нет

- SpoilageДокумент17 страницSpoilageBhawin DondaОценок пока нет

- Intercompany Sale of Depreciable AssetsДокумент2 страницыIntercompany Sale of Depreciable AssetsTriechia LaudОценок пока нет

- Kinney8e PPT Ch04Документ37 страницKinney8e PPT Ch04Michelle Rotairo0% (1)

- Financial Management MДокумент3 страницыFinancial Management MYaj CruzadaОценок пока нет

- Capital Budgeting Report FinalДокумент15 страницCapital Budgeting Report FinalCezar SabladОценок пока нет

- p2 Guerrero ch15Документ30 страницp2 Guerrero ch15Clarissa Teodoro100% (1)

- DocxДокумент40 страницDocxJamaica DavidОценок пока нет

- Ac4 CbaДокумент1 страницаAc4 CbaRobelyn Lacorte100% (1)

- Chapter 3 - Page 13 ROE Answer: C Diff: E 45. Tapley Dental Supply Company Has The Following DataДокумент2 страницыChapter 3 - Page 13 ROE Answer: C Diff: E 45. Tapley Dental Supply Company Has The Following DatapompomОценок пока нет

- Mock Deparmentals MASQДокумент6 страницMock Deparmentals MASQHannah Joyce MirandaОценок пока нет

- 208 BДокумент10 страниц208 BXulian ChanОценок пока нет

- CVP Exercise Ref. Bautista, Cancino, Rada, SarmientoДокумент5 страницCVP Exercise Ref. Bautista, Cancino, Rada, SarmientoRodolfo ManalacОценок пока нет

- Capital Budgeting Lecture UpdatedДокумент5 страницCapital Budgeting Lecture UpdatedMark Gelo WinchesterОценок пока нет

- Docx 1Документ10 страницDocx 1Anna Marie AlferezОценок пока нет

- Home Office BranchДокумент5 страницHome Office BranchMikaella SarmientoОценок пока нет

- Tandem Activity GE Allowable DeductionsДокумент6 страницTandem Activity GE Allowable DeductionsErin CruzОценок пока нет

- Cost Accounting SeatworkДокумент2 страницыCost Accounting SeatworkLorena TuazonОценок пока нет

- Management Advisory Services by Agamata Answer Key PDFДокумент11 страницManagement Advisory Services by Agamata Answer Key PDFJanine LerumОценок пока нет

- TAX004 Assignment 2.2: Taxable Net Gift and Donor's Tax: InstructionsДокумент1 страницаTAX004 Assignment 2.2: Taxable Net Gift and Donor's Tax: InstructionsGie MaeОценок пока нет

- Standard Costing and Variance Analysis: This Accounting Materials Are Brought To You byДокумент16 страницStandard Costing and Variance Analysis: This Accounting Materials Are Brought To You byChristian Bartolome LagmayОценок пока нет

- Drill Problems - Community Tax:: Mr. Lafa Mrs. LafaДокумент2 страницыDrill Problems - Community Tax:: Mr. Lafa Mrs. LafaRealEXcellenceОценок пока нет

- (Tax1) - Income Tax On Individuals - Discussion and ActivitiesДокумент12 страниц(Tax1) - Income Tax On Individuals - Discussion and ActivitiesKim EllaОценок пока нет

- Lesson 1-Relevant Cost Analysis-Strategic Cost Management-Sisc-Ay 2020-2021-Second Sem-Jason I. Trinidad, CpaДокумент13 страницLesson 1-Relevant Cost Analysis-Strategic Cost Management-Sisc-Ay 2020-2021-Second Sem-Jason I. Trinidad, CpaAira Jaimee Gonzales100% (1)

- INSTRUCTIONS: Select The Best Answer For Each of The Following Attempted. Mark Only One Answer For Each Item On The Answer SheetДокумент13 страницINSTRUCTIONS: Select The Best Answer For Each of The Following Attempted. Mark Only One Answer For Each Item On The Answer SheetMac Ferds100% (2)

- NPO-Multiple Choice Questions PART VIДокумент3 страницыNPO-Multiple Choice Questions PART VILorraineMartinОценок пока нет

- MAS - Cost of Capital 11pagesДокумент11 страницMAS - Cost of Capital 11pageskevinlim186100% (1)

- Assignment QuestionsДокумент13 страницAssignment QuestionsAiman KhanОценок пока нет

- (At) 01 - Preface, Framework, EtcДокумент8 страниц(At) 01 - Preface, Framework, EtcCykee Hanna Quizo LumongsodОценок пока нет

- P3.37 P3.s9 Controlling B.planning - D.pedormanceevaluation Focus C'Документ8 страницP3.37 P3.s9 Controlling B.planning - D.pedormanceevaluation Focus C'Maria LopezОценок пока нет

- MAS QuizДокумент6 страницMAS QuizGracelle Mae OrallerОценок пока нет

- Scheduler's ImpressiveДокумент7 страницScheduler's Impressivemaria ronoraОценок пока нет

- Mansci - Chapter 3Документ2 страницыMansci - Chapter 3Rae WorksОценок пока нет

- MS-11 (Cost of Capital, Leverage & Capital Structure)Документ8 страницMS-11 (Cost of Capital, Leverage & Capital Structure)Kim BanuelosОценок пока нет

- BFM 113 - Reviewer For Final Departmental Exam - Working Capital ManagementДокумент8 страницBFM 113 - Reviewer For Final Departmental Exam - Working Capital ManagementAudreyMaeОценок пока нет

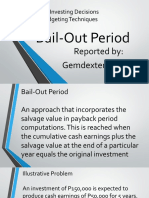

- The Firm's Investing Decisions Capital Budgeting Techniques: Bail-Out PeriodДокумент5 страницThe Firm's Investing Decisions Capital Budgeting Techniques: Bail-Out Periodgem dexter LlamesОценок пока нет

- MAS 14 Capital Budgeting With Investment Risks ReturnsДокумент16 страницMAS 14 Capital Budgeting With Investment Risks ReturnsPRINCESS ANN GENEROSO ALINGIGОценок пока нет

- Chapter 27 AnswerДокумент5 страницChapter 27 AnswerporchieeannОценок пока нет

- Cap Bud ProbДокумент9 страницCap Bud ProbJulie Mark JocsonОценок пока нет

- Capital Budgeting Notes (MBA FA - 2023)Документ10 страницCapital Budgeting Notes (MBA FA - 2023)kavyaОценок пока нет

- Capital Bud GettingДокумент27 страницCapital Bud Gettingcindysia000Оценок пока нет

- MAS Handout - Capital BudgetingДокумент7 страницMAS Handout - Capital BudgetingDivine VictoriaОценок пока нет

- FM Group AssignmentДокумент11 страницFM Group AssignmentHailemelekot TerefeОценок пока нет

- A. The Importance of Capital BudgetingДокумент34 страницыA. The Importance of Capital BudgetingMutevu SteveОценок пока нет

- Handout On Comparison of Ias 17 and Ifrs 16Документ3 страницыHandout On Comparison of Ias 17 and Ifrs 16ZEEKIRAОценок пока нет

- Chapter 13-Dayag-SolmanДокумент9 страницChapter 13-Dayag-SolmanZEEKIRAОценок пока нет

- Advacc Chapter 13& 14Документ80 страницAdvacc Chapter 13& 14ZEEKIRAОценок пока нет

- Solution Chapter 12 Advanced Accounting II 2014 by DayagДокумент20 страницSolution Chapter 12 Advanced Accounting II 2014 by DayagCindy Pausanos Paradela73% (11)

- Ocean Carriers Case: Executive SummaryДокумент5 страницOcean Carriers Case: Executive SummarykokoОценок пока нет

- Capital Budgeting of Googlosoft Technologies 1Документ16 страницCapital Budgeting of Googlosoft Technologies 1Dheeraj Y V S RОценок пока нет

- Export Crops OromiaДокумент29 страницExport Crops Oromiakashaaqaa100% (1)

- Profitability AnalysisДокумент29 страницProfitability AnalysisJocelyn CorpuzОценок пока нет

- Solution Manual For Managerial Economics Applications Strategy and Tactics 12th Edition by McGuiganДокумент7 страницSolution Manual For Managerial Economics Applications Strategy and Tactics 12th Edition by McGuigana2503568080% (2)

- Assignment 3 - Guide To WorkДокумент33 страницыAssignment 3 - Guide To WorkChristopher KipsangОценок пока нет

- Entrepreneur DevelOpment MCQSДокумент12 страницEntrepreneur DevelOpment MCQSHardik Solanki100% (3)

- Electrolysis Plant Size Optimization and Benefit Analysis of A Far Offshore Wind-Hydrogen System Based On Information Gap Decision Theory and Chance Constraints ProgrammingДокумент13 страницElectrolysis Plant Size Optimization and Benefit Analysis of A Far Offshore Wind-Hydrogen System Based On Information Gap Decision Theory and Chance Constraints ProgrammingHumberto van OolОценок пока нет

- Increase Cost Consciousness in Employees Through A Cost Competiveness Certification WorkshopДокумент16 страницIncrease Cost Consciousness in Employees Through A Cost Competiveness Certification WorkshopBalachandar SathananthanОценок пока нет

- Unit - 3 - Acma CMC 653Документ192 страницыUnit - 3 - Acma CMC 653sakshiОценок пока нет

- FIN5FMA Tutorial 4 SolutionsДокумент5 страницFIN5FMA Tutorial 4 SolutionsGauravsОценок пока нет

- Sec e - Cma Part 2Документ4 страницыSec e - Cma Part 2shreemant muniОценок пока нет

- AE May 2013 11 CS 4Документ3 страницыAE May 2013 11 CS 4tirockiОценок пока нет

- Financial Management at Beacon Pharmaceuticals LimitedДокумент24 страницыFinancial Management at Beacon Pharmaceuticals LimitedFarhanUddinAhmedОценок пока нет

- NTP Irr - SignedДокумент24 страницыNTP Irr - SignedPalanas A. VinceОценок пока нет

- Capital Budgeting Cibg.Документ36 страницCapital Budgeting Cibg.Frederick Gbli100% (1)

- GOB DPP FormatДокумент37 страницGOB DPP FormatWahidОценок пока нет

- Excel TipДокумент41 страницаExcel TipCeline AndersonОценок пока нет

- A Synopsis Report ON Investment Decision AT Icici Bank LTD: Submitted byДокумент9 страницA Synopsis Report ON Investment Decision AT Icici Bank LTD: Submitted byMOHAMMED KHAYYUMОценок пока нет

- GBS Group 7 - Blue Ridge SpainДокумент16 страницGBS Group 7 - Blue Ridge SpainAnurag YadavОценок пока нет

- Detailed Project Report ON Stenter Machine (7 Chamber) (Surat Textile Cluster)Документ44 страницыDetailed Project Report ON Stenter Machine (7 Chamber) (Surat Textile Cluster)DEVANG MISTRIОценок пока нет

- Mercantile Bank Working Capital ManagementДокумент20 страницMercantile Bank Working Capital ManagementMidul Khan100% (1)

- Cambridge Assessment International Education: Accounting 9706/32 May/June 2018Документ17 страницCambridge Assessment International Education: Accounting 9706/32 May/June 2018Tesa RudangtaОценок пока нет

- Investment AppraisalДокумент98 страницInvestment AppraisalIrene WambuiОценок пока нет

- The Capital Budgeting Decision: Mcgraw-Hill/IrwinДокумент44 страницыThe Capital Budgeting Decision: Mcgraw-Hill/IrwinLAMOUCHI RIMОценок пока нет

- 02 - Project Appraisal & AnalysisДокумент10 страниц02 - Project Appraisal & AnalysisHamza KhwajaОценок пока нет

- Capital Investment Analysis: Principles of Managerial AccountingДокумент79 страницCapital Investment Analysis: Principles of Managerial AccountingLucy UnОценок пока нет

- 05 Exercises On Capital BudgetingДокумент4 страницы05 Exercises On Capital BudgetingAnshuman AggarwalОценок пока нет

- Developing Financial Insights - Using A Future Value (FV) and A Present Value (PV) Approach PDFДокумент12 страницDeveloping Financial Insights - Using A Future Value (FV) and A Present Value (PV) Approach PDFShahzeb Ahmed50% (2)

- Energies 16 01914 With CoverДокумент19 страницEnergies 16 01914 With CoverPeyman AlizadehОценок пока нет