Вам также может понравиться

- Philippine Health Insurance Corporation vs. Commission On Audit (Full Text, Word Version)Документ18 страницPhilippine Health Insurance Corporation vs. Commission On Audit (Full Text, Word Version)Emir MendozaОценок пока нет

- COA Decision On Philhealth Allowances Worth P83,062,385.27Документ4 страницыCOA Decision On Philhealth Allowances Worth P83,062,385.27purpleromeroОценок пока нет

- Cases Touching On Non-Diminution of BenefitsДокумент36 страницCases Touching On Non-Diminution of BenefitsCliffordОценок пока нет

- Philippine International Trading Corporation v. COA, G.R. 205837 (November 21, 2017)Документ8 страницPhilippine International Trading Corporation v. COA, G.R. 205837 (November 21, 2017)Richelle GraceОценок пока нет

- Appeals Commission Audit Decision on ECC BenefitsДокумент10 страницAppeals Commission Audit Decision on ECC BenefitsHaryeth CamsolОценок пока нет

- NAPOCOR Board vs. COAДокумент17 страницNAPOCOR Board vs. COALexa ClarkeОценок пока нет

- Philippine Health Insurance Corporation, Petitioner, vs. Commission On Audit, Hon. Michael G. Aguinaldo, ChairpersonДокумент19 страницPhilippine Health Insurance Corporation, Petitioner, vs. Commission On Audit, Hon. Michael G. Aguinaldo, ChairpersonAshly Kate DaulayanОценок пока нет

- Philippine Mining vs. AguinaldoДокумент21 страницаPhilippine Mining vs. AguinaldoKey ClamsОценок пока нет

- 309 SCRA 177 Phil Inter-Island Trading Corp Vs COAДокумент7 страниц309 SCRA 177 Phil Inter-Island Trading Corp Vs COAPanda CatОценок пока нет

- 2016 Philippine Health Insurance Corp. v.20170104 672 10iryhwДокумент23 страницы2016 Philippine Health Insurance Corp. v.20170104 672 10iryhwocpgensan ocpgensanОценок пока нет

- PMDC v. COAДокумент24 страницыPMDC v. COAAizaLizaОценок пока нет

- Pastrana v. COAДокумент25 страницPastrana v. COAAizaLizaОценок пока нет

- COA Decision-2018-388Документ3 страницыCOA Decision-2018-388MariaRizzaMontalboGuizzaganОценок пока нет

- Asia Trust V CIRДокумент2 страницыAsia Trust V CIRReena Ma100% (1)

- GSIS Allowances Under Salary Standardization LawДокумент17 страницGSIS Allowances Under Salary Standardization LawJessica Melle GaliasОценок пока нет

- Labor Secretary's ruling on Skyway workers upheldДокумент6 страницLabor Secretary's ruling on Skyway workers upheldekangОценок пока нет

- SSS v. COA, G.R. No. 243278, November 03, 2020Документ7 страницSSS v. COA, G.R. No. 243278, November 03, 2020sophiaОценок пока нет

- GSIS v. COA, G.R. No. 138381, November 10, 2004Документ19 страницGSIS v. COA, G.R. No. 138381, November 10, 2004sunsetsailor85Оценок пока нет

- 7 - Philippine Health Insurance Corporation v. Commission On Audit G.R. No. 213453Документ23 страницы7 - Philippine Health Insurance Corporation v. Commission On Audit G.R. No. 213453Shash BernardezОценок пока нет

- B T Gsis - V: FactsДокумент16 страницB T Gsis - V: FactsHoward MacaraegОценок пока нет

- Ambros v. Commission On AuditДокумент20 страницAmbros v. Commission On Auditgregandaman079Оценок пока нет

- PITC Vs COAДокумент7 страницPITC Vs COAbogoldoyОценок пока нет

- 02 - Trade and Investment Corp v. Civil Service CommissionДокумент12 страниц02 - Trade and Investment Corp v. Civil Service CommissionBernadette PedroОценок пока нет

- Asiatrust Development Bank, Inc. vs. CIR, GR No. April 19, 2017Документ4 страницыAsiatrust Development Bank, Inc. vs. CIR, GR No. April 19, 2017daybarbaОценок пока нет

- Proper Interpretation of Sections 12 and 17 of R.A. 6758Документ49 страницProper Interpretation of Sections 12 and 17 of R.A. 6758Jd G. AgbayaniОценок пока нет

- Petitioners Vs Vs Respondents The Government Corporate Counsel For Petitioners. The Solicitor General For RespondentsДокумент6 страницPetitioners Vs Vs Respondents The Government Corporate Counsel For Petitioners. The Solicitor General For RespondentsChristine VillanuevaОценок пока нет

- Maritime Industry V COAДокумент4 страницыMaritime Industry V COAGwynneth Grace LasayОценок пока нет

- G.R. No. 222710 Philippine Health Insurance Corp v. Commission On AuditДокумент31 страницаG.R. No. 222710 Philippine Health Insurance Corp v. Commission On AuditKarla KarlaОценок пока нет

- Avila vs. CoaДокумент8 страницAvila vs. CoaEunice Panopio LopezОценок пока нет

- BFAR Employees Union Issued Resolution No. 01 Requesting The BFAR CentralДокумент1 страницаBFAR Employees Union Issued Resolution No. 01 Requesting The BFAR Centralaudrich carlo agustinОценок пока нет

- Ppa Employee v. CoaДокумент10 страницPpa Employee v. CoaZach Matthew GalendezОценок пока нет

- PEZA V COAДокумент12 страницPEZA V COARyan Christian LuposОценок пока нет

- Phil International Trading Vs CoaДокумент9 страницPhil International Trading Vs CoaRocky CadizОценок пока нет

- Philippine Interntaional Trading Corporation v. Commission On AuditДокумент8 страницPhilippine Interntaional Trading Corporation v. Commission On AuditJey RhyОценок пока нет

- External Training ReportДокумент6 страницExternal Training ReportReia RuecoОценок пока нет

- GR No. 168129 (CIR V Phil Health Care) (Nonretroactivity)Документ12 страницGR No. 168129 (CIR V Phil Health Care) (Nonretroactivity)Archie GuevarraОценок пока нет

- CASE 17 - NHA vs. Commission On Audit, G.R. Nos. 239936 & 252584, 2022Документ2 страницыCASE 17 - NHA vs. Commission On Audit, G.R. Nos. 239936 & 252584, 2022Reyna Bernadeth ReyalaОценок пока нет

- Gen San Vs COA en Banc G.R. No. 199439 April 22, 2014Документ20 страницGen San Vs COA en Banc G.R. No. 199439 April 22, 2014herbs22225847Оценок пока нет

- Adjudication Order in Respect of Nature India Communique LimitedДокумент10 страницAdjudication Order in Respect of Nature India Communique LimitedShyam SunderОценок пока нет

- Case DigestДокумент3 страницыCase DigestMaica MagbitangОценок пока нет

- City of GenSan vs. COAДокумент2 страницыCity of GenSan vs. COAJay-r TumamakОценок пока нет

- Agra vs. CoadocxДокумент2 страницыAgra vs. CoadocxDane Pauline Adora100% (1)

- BFAR Employees Allowed Food Basket AllowanceДокумент7 страницBFAR Employees Allowed Food Basket AllowancegheljoshОценок пока нет

- Philippine International Trading Corporation Vs COAДокумент8 страницPhilippine International Trading Corporation Vs COAmondaytuesday17Оценок пока нет

- Philippine Health Insurance Corporation vs. Commission On Audit DigestДокумент3 страницыPhilippine Health Insurance Corporation vs. Commission On Audit DigestEmir Mendoza100% (1)

- AJJJJJJJJJJJJJJJДокумент2 страницыAJJJJJJJJJJJJJJJanthony paduaОценок пока нет

- Petitioner Vs Vs Respondent: en BancДокумент11 страницPetitioner Vs Vs Respondent: en BancKyle AgustinОценок пока нет

- COA Upholds Disallowance of BFAR Food Basket AllowanceДокумент6 страницCOA Upholds Disallowance of BFAR Food Basket AllowanceRoze JustinОценок пока нет

- TESDA v. COAДокумент8 страницTESDA v. COAacherreraОценок пока нет

- G.R. No. 196110Документ10 страницG.R. No. 196110Anonymous KgPX1oCfrОценок пока нет

- Blue Bar Coconut Vs TantuicoДокумент14 страницBlue Bar Coconut Vs TantuicoAbigael DemdamОценок пока нет

- 1656658970-6153 Narayan IndustriesДокумент20 страниц1656658970-6153 Narayan IndustriesAshish GoelОценок пока нет

- MWSS v. COAДокумент8 страницMWSS v. COAAra KimОценок пока нет

- Service Tax Recovery CircularДокумент9 страницService Tax Recovery CircularsrinivaspanchakarlaОценок пока нет

- Asiatrust V. Cir G.R. No. 201530 / G.R. Nos. 201680-81 April 19, 2017 REMДокумент3 страницыAsiatrust V. Cir G.R. No. 201530 / G.R. Nos. 201680-81 April 19, 2017 REMRein GallardoОценок пока нет

- COA Denies PITC Request to Amend 2010 Audit Report on Retirement BenefitsДокумент8 страницCOA Denies PITC Request to Amend 2010 Audit Report on Retirement BenefitsChristopher AdvinculaОценок пока нет

- An Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersОт EverandAn Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersОценок пока нет

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisОт EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisОценок пока нет

- Emilio Aguinaldo College - Cavite Campus School of Business AdministrationДокумент9 страницEmilio Aguinaldo College - Cavite Campus School of Business AdministrationKarlayaanОценок пока нет

- Positive Accounting TheoryДокумент6 страницPositive Accounting TheoryAndi IrwanОценок пока нет

- Accepting and EngagementДокумент4 страницыAccepting and EngagementC E DОценок пока нет

- Intro To P3M3Документ67 страницIntro To P3M3Ary EppelОценок пока нет

- Chapter Six Strategy Analysis and Choice/Strategy FormulationДокумент12 страницChapter Six Strategy Analysis and Choice/Strategy FormulationmedrekОценок пока нет

- Ffa Past Paper 3 (F3)Документ21 страницаFfa Past Paper 3 (F3)Shereka EllisОценок пока нет

- PropertyGuru 2020 Financial StatementДокумент115 страницPropertyGuru 2020 Financial StatementTerence LeeОценок пока нет

- Presentation On Walmart StoresДокумент16 страницPresentation On Walmart StoresBhumika PatelОценок пока нет

- Strategic Plan Document: FOR Deposit Protection CorporationДокумент43 страницыStrategic Plan Document: FOR Deposit Protection CorporationTINOTENDA PRIVILEDGE ZILILOОценок пока нет

- Ps Chapter 1 Final 100113Документ12 страницPs Chapter 1 Final 100113api-233596763Оценок пока нет

- Clearlake City Council Agenda PacketДокумент151 страницаClearlake City Council Agenda PacketLakeCoNewsОценок пока нет

- 01 Introduction To Cost Accounting PDFДокумент31 страница01 Introduction To Cost Accounting PDFemman neriОценок пока нет

- Tax Remdeies Under Nirc NotesДокумент24 страницыTax Remdeies Under Nirc NotesJulzОценок пока нет

- Government Procurement 101 GuideДокумент60 страницGovernment Procurement 101 GuideClaudine Carie SalomsonОценок пока нет

- Analysis of financial ratios of 5 years for current assets, liabilities, liquidity, asset turnover and capital structureДокумент7 страницAnalysis of financial ratios of 5 years for current assets, liabilities, liquidity, asset turnover and capital structureNIKHIL MATHEWОценок пока нет

- ISSAI 1220: Quality Control For An Audit of Financial StatementsДокумент28 страницISSAI 1220: Quality Control For An Audit of Financial StatementsCharlie MaineОценок пока нет

- Accounting Rules in MacedoniaДокумент1 страницаAccounting Rules in MacedoniaZiko_66Оценок пока нет

- Applied Indirect Taxation PDFДокумент352 страницыApplied Indirect Taxation PDFjerciОценок пока нет

- Financial Due DiligenceДокумент9 страницFinancial Due DiligenceNehal MehtaОценок пока нет

- AT 3rdbatch 1stPBДокумент12 страницAT 3rdbatch 1stPBvangieolalia100% (2)

- Kenya construction industry actorsДокумент11 страницKenya construction industry actorsISAAC KIPSEREMОценок пока нет

- Sumal Perera's Access To Mahinda RajapaksaДокумент8 страницSumal Perera's Access To Mahinda RajapaksaThavam RatnaОценок пока нет

- Accounting 14 - Applied Auditing OkДокумент12 страницAccounting 14 - Applied Auditing OkNico evansОценок пока нет

- List of Courses (Management)Документ2 страницыList of Courses (Management)Andrian PratamaОценок пока нет

- Adjusting Entries GuideДокумент11 страницAdjusting Entries GuideMoses IrunguОценок пока нет

- Question and Answer - 58Документ30 страницQuestion and Answer - 58acc-expertОценок пока нет

- 5.1 Questions: Chapter 5 Relevant Information For Decision Making With A Focus On Pricing DecisionsДокумент37 страниц5.1 Questions: Chapter 5 Relevant Information For Decision Making With A Focus On Pricing DecisionsLiyana ChuaОценок пока нет

- Bir Form No. 1907Документ1 страницаBir Form No. 1907Kim ValenciaОценок пока нет

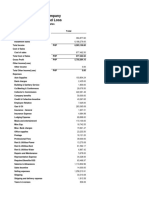

- XYZ Company Profit and Loss: All DatesДокумент2 страницыXYZ Company Profit and Loss: All DatesMatt Kelvin ParaisoОценок пока нет

- IS 14011 (Part 2) : 1991 IS0 10011-2: Bureau of Indian StandardsДокумент10 страницIS 14011 (Part 2) : 1991 IS0 10011-2: Bureau of Indian StandardsproxywarОценок пока нет