Вам также может понравиться

- Accounts Final PresentationДокумент30 страницAccounts Final PresentationRITIKAОценок пока нет

- Corporate FincanceДокумент9 страницCorporate Fincanceneha chodryОценок пока нет

- Chapter 20: Hybrid Financing: Preferred StockДокумент4 страницыChapter 20: Hybrid Financing: Preferred StockChaudhary AliОценок пока нет

- Company Acc - Issue of Debentures @CA - Study - NotesДокумент9 страницCompany Acc - Issue of Debentures @CA - Study - Notesbhawanar3950Оценок пока нет

- CHP 20 Fin 13Документ11 страницCHP 20 Fin 13Player OneОценок пока нет

- Hybrid Financing:: Preferred Stock, Leasing, Warrants, and ConvertiblesДокумент29 страницHybrid Financing:: Preferred Stock, Leasing, Warrants, and ConvertiblesAli HussainОценок пока нет

- Loan Capital - RPS and DebenturesДокумент23 страницыLoan Capital - RPS and Debenturesathirah jamaludinОценок пока нет

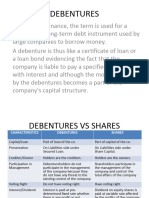

- Difference Between Debenture & SharesДокумент1 страницаDifference Between Debenture & SharespranavyesОценок пока нет

- Long Term FinancingДокумент7 страницLong Term FinancingKennedy Waweru100% (1)

- Long-Term CapitalДокумент13 страницLong-Term Capitalafoninadin81Оценок пока нет

- FINANCE MANAGEMENT FIN420 CHP 9Документ38 страницFINANCE MANAGEMENT FIN420 CHP 9Yanty IbrahimОценок пока нет

- Leac202 DebenturesДокумент75 страницLeac202 DebenturesMidhunidharОценок пока нет

- Note On Financial InstrumentsДокумент5 страницNote On Financial InstrumentsVismay GharatОценок пока нет

- L2 Source of FinanceДокумент26 страницL2 Source of FinanceZhiyu KamОценок пока нет

- Solutions Manual Corporate Finance RossДокумент11 страницSolutions Manual Corporate Finance RossRijalul KamalОценок пока нет

- Issue and Redemption of DebenturesДокумент78 страницIssue and Redemption of DebenturesApollo Institute of Hospital Administration50% (2)

- Dividends: 1.1 Definition of DividendДокумент11 страницDividends: 1.1 Definition of Dividendshiza sheikhОценок пока нет

- Dividends: 1.1 Definition of DividendДокумент11 страницDividends: 1.1 Definition of Dividendshiza sheikhОценок пока нет

- Real Options A New Way To ThinkДокумент20 страницReal Options A New Way To ThinkAjay TahilramaniОценок пока нет

- Cost of CapitalДокумент16 страницCost of CapitalParth BindalОценок пока нет

- Debt ManagementДокумент9 страницDebt ManagementAngelie AnilloОценок пока нет

- DebentureДокумент9 страницDebenturedrsurendrakumarОценок пока нет

- RWJ (9th Edition) Chapter 15Документ11 страницRWJ (9th Edition) Chapter 15CristinaОценок пока нет

- ChapterДокумент78 страницChaptershaannivasОценок пока нет

- Unit 4 B Note - Long Term Debt and Prefered StockДокумент18 страницUnit 4 B Note - Long Term Debt and Prefered StockRajendra LamsalОценок пока нет

- Types of DebenturesДокумент3 страницыTypes of DebenturesNidheesh TpОценок пока нет

- DEBENTURESДокумент5 страницDEBENTURESAnand S PОценок пока нет

- Chapter 7sДокумент96 страницChapter 7ssgangwar2005sgОценок пока нет

- BBA VI TH Sem Financial Institution & MarketsДокумент2 страницыBBA VI TH Sem Financial Institution & MarketsJordan ThapaОценок пока нет

- Current Liabilities Current (Or Short-Term) Liabilities Are Obligations Whose Settlement Requires The UseДокумент4 страницыCurrent Liabilities Current (Or Short-Term) Liabilities Are Obligations Whose Settlement Requires The UseKiki AmeliaОценок пока нет

- Company Acc Unit 3Документ39 страницCompany Acc Unit 3Megha DevanpalliОценок пока нет

- HW4 Group1Документ7 страницHW4 Group1jinklad47Оценок пока нет

- Dividend Policy & Long-Term Financing Overview: Session 10Документ17 страницDividend Policy & Long-Term Financing Overview: Session 10May CancinoОценок пока нет

- Engineering Economy Module 7Документ15 страницEngineering Economy Module 7shaitoОценок пока нет

- Intro To Finance NotesДокумент9 страницIntro To Finance NotesAzeemAhmedОценок пока нет

- Chapter 12: The Cost of Capital: Suggested SolutionsДокумент7 страницChapter 12: The Cost of Capital: Suggested Solutionsapi-3824657Оценок пока нет

- Debenture Accounting PDFДокумент75 страницDebenture Accounting PDFMuhammad Faran KhanОценок пока нет

- Debenture Vs Shares-2Документ19 страницDebenture Vs Shares-2nemewep527Оценок пока нет

- E BusinessfinanceДокумент15 страницE BusinessfinanceDipannita RoyОценок пока нет

- Technical Interview QuestionsДокумент6 страницTechnical Interview Questionsu0909098Оценок пока нет

- Capital Structure and Dividen PolicyДокумент23 страницыCapital Structure and Dividen PolicyChristian DavidОценок пока нет

- Summary Hybrid Financing (18!11!2021)Документ5 страницSummary Hybrid Financing (18!11!2021)Shafa EОценок пока нет

- 67188bos54090 Cp10u3Документ31 страница67188bos54090 Cp10u3Pawan TalrejaОценок пока нет

- Leac 202Документ75 страницLeac 202Ias Aspirant AbhiОценок пока нет

- Leac 202Документ69 страницLeac 202Aditya Singh RajputОценок пока нет

- Issue of DebenturesДокумент23 страницыIssue of Debenturesramandeep kaurОценок пока нет

- Chapter-8 Issue of Debentures: Debenture: The Word Debenture' Has Been Derived From A Latin Word Debere' WhichДокумент8 страницChapter-8 Issue of Debentures: Debenture: The Word Debenture' Has Been Derived From A Latin Word Debere' Whichramandeep kaurОценок пока нет

- Financing Decisions 2Документ12 страницFinancing Decisions 2PUTTU GURU PRASAD SENGUNTHA MUDALIARОценок пока нет

- Equity and LiabilitiesДокумент11 страницEquity and LiabilitiesLaston MilanziОценок пока нет

- Doc-20231220-Wa0002. 20231220 232817 0000Документ15 страницDoc-20231220-Wa0002. 20231220 232817 0000Khushdeep Kaur KaurОценок пока нет

- BAB 3 Analyzing Financing Activities 071016Документ64 страницыBAB 3 Analyzing Financing Activities 071016Haniedar NadifaОценок пока нет

- Chapter 9 HW SolutionsДокумент35 страницChapter 9 HW SolutionsemailericОценок пока нет

- Debenture PrintДокумент3 страницыDebenture PrintSuman DhunganaОценок пока нет

- Reporting and Analyzing Off-Balance Sheet FinancingДокумент31 страницаReporting and Analyzing Off-Balance Sheet FinancingmanoranjanpatraОценок пока нет

- Various Types of Corporate BondsДокумент7 страницVarious Types of Corporate BondsAbdul LatifОценок пока нет

- Unit 8 Corporate Finance IIДокумент4 страницыUnit 8 Corporate Finance IIpradeep ranaОценок пока нет

- Treasury Finals ReviewerДокумент5 страницTreasury Finals ReviewerGodween CruzОценок пока нет

- 015 - Quick-Notes - Financial Liabilities From Borrowings Part 2Документ3 страницы015 - Quick-Notes - Financial Liabilities From Borrowings Part 2Zatsumono YamamotoОценок пока нет

- Accounting of DebenturesДокумент24 страницыAccounting of Debenturesmanya singhОценок пока нет

- EWS Reservoir DatabaseДокумент40 страницEWS Reservoir DatabaseIsmaeel TarОценок пока нет

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Ab Jad Table Mystic LettersДокумент3 страницыAb Jad Table Mystic LettersSheikh Muhammad Abdullah Arshad Altaf Malik100% (1)

- Book2and3 HandoutsДокумент51 страницаBook2and3 HandoutsTruth SeekerОценок пока нет

- Birdie Hybrid MergerДокумент3 страницыBirdie Hybrid MergerIsmaeel TarОценок пока нет

- Assignment Calcs4Документ18 страницAssignment Calcs4Ismaeel TarОценок пока нет

- Mba Y2 Man Finance Final MMДокумент11 страницMba Y2 Man Finance Final MMIsmaeel TarОценок пока нет

- QueryДокумент2 страницыQueryIsmaeel TarОценок пока нет

- Abharī: Athīr Al Dīn Al Mufa Al Ibn Umar Ibn Al Mufa Al Al Samarqandī Al AbharīДокумент2 страницыAbharī: Athīr Al Dīn Al Mufa Al Ibn Umar Ibn Al Mufa Al Al Samarqandī Al AbharīIsmaeel TarОценок пока нет

- Mba (NQF 9) Year 1 PH Jan 2017Документ80 страницMba (NQF 9) Year 1 PH Jan 2017Ismaeel TarОценок пока нет

- 2016 2017 Catalog PDFДокумент59 страниц2016 2017 Catalog PDFIsmaeel TarОценок пока нет

- Annual Report September 2007 Part 1Документ16 страницAnnual Report September 2007 Part 1Ismaeel TarОценок пока нет

- Is and Goals-StrategyДокумент5 страницIs and Goals-StrategyIsmaeel TarОценок пока нет

- BBBBДокумент12 страницBBBBIsmaeel TarОценок пока нет

- Mayoral Dispute Resolved: Beginning A New YearДокумент16 страницMayoral Dispute Resolved: Beginning A New YearelauwitОценок пока нет

- Cruz vs. Bancom Finance Corporation, 379 SCRA 490, March 19, 2002Документ22 страницыCruz vs. Bancom Finance Corporation, 379 SCRA 490, March 19, 2002marvin ninoОценок пока нет

- Santana IPOДокумент246 страницSantana IPOyaoanmin2005Оценок пока нет

- Final Exam General Mathematics Grade 11 SHSДокумент5 страницFinal Exam General Mathematics Grade 11 SHSFelipe R. Illeses92% (13)

- The Star News January 22 2015Документ43 страницыThe Star News January 22 2015The Star NewsОценок пока нет

- Succession ReviewerДокумент96 страницSuccession ReviewerAylwin John Perez80% (5)

- PolicyДокумент17 страницPolicyowen100% (1)

- Bonded Labour System (Abolition) Act 1976Документ1 страницаBonded Labour System (Abolition) Act 1976anchal1987Оценок пока нет

- Inglês Empresarial PDFДокумент19 страницInglês Empresarial PDFFigFilhoОценок пока нет

- Commercial BankingДокумент1 страницаCommercial BankingPatrick JaneОценок пока нет

- FIls/RFPIs Can Now Invest Up To 100% Under PIS in M/s Veritas (India) Limited (Company Update)Документ13 страницFIls/RFPIs Can Now Invest Up To 100% Under PIS in M/s Veritas (India) Limited (Company Update)Shyam SunderОценок пока нет

- MR Holdings, Ltd. vs. Bajar, 380 SCRA 617, April 11, 2002Документ3 страницыMR Holdings, Ltd. vs. Bajar, 380 SCRA 617, April 11, 2002idolbondocОценок пока нет

- Pnoc Vs KeppelДокумент6 страницPnoc Vs KeppeljessapuerinОценок пока нет

- Principles of Business Law-Negotiable InstrumentДокумент16 страницPrinciples of Business Law-Negotiable Instrumentjohn wongОценок пока нет

- T3-Sample Answers-Consideration PDFДокумент10 страницT3-Sample Answers-Consideration PDF--bolabolaОценок пока нет

- PCE Sample Questions - SET 6 (ENG)Документ15 страницPCE Sample Questions - SET 6 (ENG)Raja Mohan100% (1)

- BPI Vs Vicente Victor C. Sanchez Et Al.Документ4 страницыBPI Vs Vicente Victor C. Sanchez Et Al.Ge-An Moiseah SaludОценок пока нет

- Presentation On Mathematics For FinanceДокумент14 страницPresentation On Mathematics For FinanceShakil Ahmed IsrafilОценок пока нет

- ABC Limited - PPT NBNДокумент19 страницABC Limited - PPT NBNNagarajNadigОценок пока нет

- CRA Exam ChecklistДокумент6 страницCRA Exam Checklistgeodatavision100% (2)

- Financial ManagementДокумент11 страницFinancial ManagementRuel VillanuevaОценок пока нет

- Trader's Royal Bank Vs CastañaresДокумент6 страницTrader's Royal Bank Vs CastañaresJonjon BeeОценок пока нет

- General Mathematics Grade11 SyllabuspdfДокумент11 страницGeneral Mathematics Grade11 SyllabuspdfCheska PerolОценок пока нет

- Corporate Finance: The Time Value of MoneyДокумент35 страницCorporate Finance: The Time Value of MoneyRodrigoОценок пока нет

- Rep. Lesser July 10 SEEC FilingДокумент231 страницаRep. Lesser July 10 SEEC FilingCassandra DayОценок пока нет

- Paylater - ToC - Traveloka PaylaterДокумент11 страницPaylater - ToC - Traveloka PaylaterkevincpcepОценок пока нет

- FN1623-2406 - Footnotes Levin-Coburn ReportДокумент1 036 страницFN1623-2406 - Footnotes Levin-Coburn ReportRick ThomaОценок пока нет

- Obligations and Contracts: FEBLE, Karen Gail BДокумент1 страницаObligations and Contracts: FEBLE, Karen Gail BGin FranciscoОценок пока нет

- Tender Notice: Integrated City Revenue Management System For Nairobi City CountyДокумент397 страницTender Notice: Integrated City Revenue Management System For Nairobi City CountyICT AUTHORITYОценок пока нет

- HQP-HLF-002 Checklist of Requirements For RL - PenconДокумент1 страницаHQP-HLF-002 Checklist of Requirements For RL - Penconmaxx villaОценок пока нет