Вам также может понравиться

- Digest of MIAA v. CA (G.R. No. 155650)Документ2 страницыDigest of MIAA v. CA (G.R. No. 155650)Rafael Pangilinan100% (12)

- Practical Accounting of Cash Flow From Operating ActivitiesДокумент13 страницPractical Accounting of Cash Flow From Operating ActivitiesDJ Nicart63% (8)

- Question #1 of 94: Distinguishable From The Company's Other Lines of BusinessДокумент43 страницыQuestion #1 of 94: Distinguishable From The Company's Other Lines of BusinessShahd OkashaОценок пока нет

- Business and Income Taxation For Non-Accountant Seminar - WorkshopДокумент7 страницBusiness and Income Taxation For Non-Accountant Seminar - WorkshopJohn ManahanОценок пока нет

- Den Broadband Limited: Biller DetailДокумент1 страницаDen Broadband Limited: Biller DetailDeepak Dahiya100% (1)

- Fake PaystubДокумент1 страницаFake PaystubBrandon CarpenterОценок пока нет

- RCPI vs. Provincial Assesor of South Cotabato (G.R. No. 144486. April 13, 2005) - 4 H DIGESTДокумент2 страницыRCPI vs. Provincial Assesor of South Cotabato (G.R. No. 144486. April 13, 2005) - 4 H DIGESTHarleneОценок пока нет

- Rcpi VS Provincial AssessorДокумент3 страницыRcpi VS Provincial AssessorKath LeenОценок пока нет

- RCPI vs. Provincial Assesor of South Cotabato (G.R. No. 144486. April 13, 2005) - H DIGESTДокумент1 страницаRCPI vs. Provincial Assesor of South Cotabato (G.R. No. 144486. April 13, 2005) - H DIGESTHarleneОценок пока нет

- G.R. No. 144486 13 April 2005: Radio Communications of The Philippines, Inc. Provincial Assessor of South CotabatoДокумент17 страницG.R. No. 144486 13 April 2005: Radio Communications of The Philippines, Inc. Provincial Assessor of South CotabatoPatatas SayoteОценок пока нет

- CD - 20. RCPI v. Provincial AssessorДокумент1 страницаCD - 20. RCPI v. Provincial AssessorAlyssa Alee Angeles JacintoОценок пока нет

- Section 13. Privileges of Graded Films. - Films Which Have Obtained An "A" or "B"Документ7 страницSection 13. Privileges of Graded Films. - Films Which Have Obtained An "A" or "B"Kat VillanuevaОценок пока нет

- Mcia vs. Lapu-Lapu CityДокумент3 страницыMcia vs. Lapu-Lapu CitySharon BakerОценок пока нет

- MCIAA vs. Lapu-LapuДокумент3 страницыMCIAA vs. Lapu-LapukaiaceegeesОценок пока нет

- The National Government, Which Historically Merely Delegated To Local Governments The Power To TaxДокумент37 страницThe National Government, Which Historically Merely Delegated To Local Governments The Power To Taxlleiryc7Оценок пока нет

- Mciaa Vs LapulapuДокумент23 страницыMciaa Vs LapulapuKobe Bullmastiff100% (1)

- Property Law Case DigestДокумент19 страницProperty Law Case Digestmilcah valenciaОценок пока нет

- Admin Cases Set 2Документ34 страницыAdmin Cases Set 2Kelvin ZabatОценок пока нет

- Property Law Cases LackingДокумент25 страницProperty Law Cases LackingPRECIOUS GRACE DAROYОценок пока нет

- Property Law Cases LackingДокумент26 страницProperty Law Cases LackingTungoranОценок пока нет

- Pascual Vs Secretary of Works Refer To ShekinaДокумент5 страницPascual Vs Secretary of Works Refer To ShekinaNorman jOyeОценок пока нет

- MCIAA v. City of Lapu LapuДокумент26 страницMCIAA v. City of Lapu LapuMassabielleОценок пока нет

- Real Property Taxation CasesДокумент7 страницReal Property Taxation CasesRyan AcostaОценок пока нет

- Real Property Case DigestsДокумент45 страницReal Property Case DigestsKristine Jay Perez-CabusogОценок пока нет

- G.R. No. 149110 April 9, 2003 National Power Corporation, Petitioner, CITY OF CABANATUAN, Respondent. PUNO, J.Документ12 страницG.R. No. 149110 April 9, 2003 National Power Corporation, Petitioner, CITY OF CABANATUAN, Respondent. PUNO, J.Samuel John CahimatОценок пока нет

- C. National Power Corporation Vs City of Cabanatuan, G.R. No. 149110, April 09, 2003Документ26 страницC. National Power Corporation Vs City of Cabanatuan, G.R. No. 149110, April 09, 2003MirafelОценок пока нет

- Philippine Amusement and Gaming Corporation, 197 SCRA 52, Where It Was Held ThatДокумент28 страницPhilippine Amusement and Gaming Corporation, 197 SCRA 52, Where It Was Held ThatLj Brazas SortigosaОценок пока нет

- Pub Corp DigestДокумент14 страницPub Corp DigestJohn Lloyd MacuñatОценок пока нет

- Maceda Vs MacaraigДокумент4 страницыMaceda Vs MacaraigJovy Balangue MacadaegОценок пока нет

- MCIAA Vs LAPU LAPU CITYДокумент5 страницMCIAA Vs LAPU LAPU CITYJep Echon TilosОценок пока нет

- NPC v. CITY OF CABANATUANДокумент12 страницNPC v. CITY OF CABANATUANMuhammadIshahaqBinBenjaminОценок пока нет

- I-B1 Topic: Tax Returns and Other Administrative Requirements Paseo Realty and Development Corp. Vs - Court of Appealsg.R. No. 119286 October 13, 2004factsДокумент4 страницыI-B1 Topic: Tax Returns and Other Administrative Requirements Paseo Realty and Development Corp. Vs - Court of Appealsg.R. No. 119286 October 13, 2004factsRon AceroОценок пока нет

- Dungo V LopenaДокумент14 страницDungo V LopenaJonathan DancelОценок пока нет

- 54 City Government of QC V BayantelДокумент2 страницы54 City Government of QC V BayantelCelest AtasОценок пока нет

- PHILIPPINE BASKETBALL ASSOCIATION Vs CAДокумент4 страницыPHILIPPINE BASKETBALL ASSOCIATION Vs CADesire RufinОценок пока нет

- 11 - Meralco Vs CAДокумент53 страницы11 - Meralco Vs CAthelawanditscomplexitiesОценок пока нет

- 292 NPC v. City of CabanatuanДокумент6 страниц292 NPC v. City of CabanatuanclarkorjaloОценок пока нет

- Property Case Manila Electric Company V City AssessorДокумент30 страницProperty Case Manila Electric Company V City AssessorWahida TatoОценок пока нет

- MCIA vs. City CouncilДокумент4 страницыMCIA vs. City CouncilKeisha Camille OliverosОценок пока нет

- Tax Cases B NatureДокумент13 страницTax Cases B NatureammeОценок пока нет

- Posted On January 26, 2018 by ARDEEND Leave A CommentДокумент3 страницыPosted On January 26, 2018 by ARDEEND Leave A CommentOliveros DMОценок пока нет

- 03 MCIAA V City of Lapu-LapuДокумент2 страницы03 MCIAA V City of Lapu-LapuKim CajucomОценок пока нет

- Tax CasesДокумент12 страницTax CasesLito IngatanОценок пока нет

- Compiled Cases in PropertyДокумент96 страницCompiled Cases in PropertydianepndvlaОценок пока нет

- City Government of Quezon City Vs Bayantel GR NO 162015 MARCH 06 2006 FactsДокумент14 страницCity Government of Quezon City Vs Bayantel GR NO 162015 MARCH 06 2006 Factsa7bkn100% (1)

- National Power Corp. vs. City of Cabanatuan, 401 SCRA 409Документ16 страницNational Power Corp. vs. City of Cabanatuan, 401 SCRA 409Machida AbrahamОценок пока нет

- Taxation Case Digest 3Документ9 страницTaxation Case Digest 3seentherellaaaОценок пока нет

- B. Section 14 of R.A. 9167 Constitutes An Undue Limitation of The Taxing Power of LgusДокумент4 страницыB. Section 14 of R.A. 9167 Constitutes An Undue Limitation of The Taxing Power of LgusNika RojasОценок пока нет

- H. Taxation Other Inherent To Escape From Taxation CasesДокумент36 страницH. Taxation Other Inherent To Escape From Taxation CasesErwin April MidsapakОценок пока нет

- Pubcorp Digests 2Документ27 страницPubcorp Digests 2Dana DОценок пока нет

- MCIAA Vs MARCOSДокумент4 страницыMCIAA Vs MARCOSJep Echon TilosОценок пока нет

- 05 City Government of Quezon City V Bayan Telecommunications PDFДокумент2 страницы05 City Government of Quezon City V Bayan Telecommunications PDFCarla CucuecoОценок пока нет

- Power To Create Sources of FundsДокумент3 страницыPower To Create Sources of FundsCarla Louise Bulacan BayquenОценок пока нет

- Supreme Court: Charges by Government and Governmental Instrumentalities.-The Corporation Shall Be Non-Profit and ShallДокумент10 страницSupreme Court: Charges by Government and Governmental Instrumentalities.-The Corporation Shall Be Non-Profit and ShallRYWELLE BRAVOОценок пока нет

- Mactan-Cebu International Airport Authority (MCIAA) v. City of Lapu-Lapu and PacaldoДокумент2 страницыMactan-Cebu International Airport Authority (MCIAA) v. City of Lapu-Lapu and PacaldoJoshua Borres100% (1)

- Real Personal Property Classification Treatment Title Facts Issue/s Held MEC Vs The City AssessorДокумент7 страницReal Personal Property Classification Treatment Title Facts Issue/s Held MEC Vs The City AssessorEller-Jed Manalac MendozaОценок пока нет

- Icard Vs Council of Baguio Facts:: ViresДокумент41 страницаIcard Vs Council of Baguio Facts:: ViresNLainie OmarОценок пока нет

- Renato Diaz Vs Secretary of FinanceДокумент5 страницRenato Diaz Vs Secretary of FinanceLouis BelarmaОценок пока нет

- RPT CasesДокумент13 страницRPT CasesSNLTОценок пока нет

- Film Development Council vs. Colon HeritageДокумент2 страницыFilm Development Council vs. Colon HeritageIsay YasonОценок пока нет

- 4 Tax2 Cases FinalsДокумент25 страниц4 Tax2 Cases FinalsVincent TanОценок пока нет

- Tax2 Meeting 2 - 17novemberДокумент108 страницTax2 Meeting 2 - 17novemberBobby Olavides SebastianОценок пока нет

- Meralco v. City AssessorДокумент35 страницMeralco v. City AssessorErl RoseteОценок пока нет

- 042 - Republic v. ICCДокумент3 страницы042 - Republic v. ICCjrvyeeОценок пока нет

- Basic Law of the Macao Special Administrative Region of the People' s Republic of ChinaОт EverandBasic Law of the Macao Special Administrative Region of the People' s Republic of ChinaОценок пока нет

- Customs and Excise Act 20 of 1998Документ103 страницыCustoms and Excise Act 20 of 1998André Le RouxОценок пока нет

- Ca MGN 303 LpuДокумент6 страницCa MGN 303 LpuAvinash BeheraОценок пока нет

- Present Scenario of Holding Tax Management of Local Government in Bangladesh - A Study On Union Parishad of Bogura DistrictДокумент9 страницPresent Scenario of Holding Tax Management of Local Government in Bangladesh - A Study On Union Parishad of Bogura DistrictMohiuddin Khan AL AminОценок пока нет

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Документ1 страницаTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Pragyakta SinghОценок пока нет

- Puyat and Sons Vs City of ManilaДокумент4 страницыPuyat and Sons Vs City of ManilaJohn Jeffrey L. Ramirez100% (1)

- A Rothschild Plan For World GovernmentДокумент31 страницаA Rothschild Plan For World GovernmentZsi GaОценок пока нет

- 11 12 (Eng. Med) : Join The Best To Be The BestДокумент31 страница11 12 (Eng. Med) : Join The Best To Be The BestDhrumil DesaiОценок пока нет

- GX Tracking The Trends 2022 DigitalДокумент61 страницаGX Tracking The Trends 2022 DigitalJuan Manuel PardalОценок пока нет

- Kiplinger's Personal Finance - January 2018 PDFДокумент74 страницыKiplinger's Personal Finance - January 2018 PDFjkavinОценок пока нет

- Final Level Advanced Taxation 2: ObjectiveДокумент5 страницFinal Level Advanced Taxation 2: Objectiveadibahhanaffi01Оценок пока нет

- Acc324 MidsДокумент8 страницAcc324 MidsAccounting GuyОценок пока нет

- Account Opening Documents For Bob JyotiДокумент9 страницAccount Opening Documents For Bob JyotiAmol KumarОценок пока нет

- Optional Standard Deduction OSDДокумент28 страницOptional Standard Deduction OSDLes EvangeListaОценок пока нет

- CIR v. San Miguel CorporationДокумент1 страницаCIR v. San Miguel CorporationKym AlgarmeОценок пока нет

- Webull Tax DocumentДокумент10 страницWebull Tax DocumentHimer VerdeОценок пока нет

- PPM 8Документ110 страницPPM 8Nilima LudbeОценок пока нет

- Chapter 2 The Demands of Global E-CommerceДокумент3 страницыChapter 2 The Demands of Global E-CommercePaw VerdilloОценок пока нет

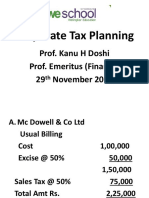

- Tax Planning PPT For 1 NovДокумент28 страницTax Planning PPT For 1 NovDivyaОценок пока нет

- Subject: PRF192-PFC Workshop 02: ObjectivesДокумент5 страницSubject: PRF192-PFC Workshop 02: ObjectivesTuan SuriОценок пока нет

- Texas Taxpayer Student Fairness Coalition FilingДокумент17 страницTexas Taxpayer Student Fairness Coalition FilingPaul MastersОценок пока нет

- Answer Any FOUR Questions From The Remaining FIVE QuestionsДокумент6 страницAnswer Any FOUR Questions From The Remaining FIVE QuestionsRahul GuptaОценок пока нет

- 201743-2016-InG Bank N.V. v. Commissioner of InternalДокумент11 страниц201743-2016-InG Bank N.V. v. Commissioner of Internalaspiringlawyer1234Оценок пока нет

- Ola Cabs 197986805Документ1 страницаOla Cabs 197986805Lakshmi MuvvalaОценок пока нет

- Delish NutrishДокумент54 страницыDelish NutrishNael ChiraghОценок пока нет

- Final ProjectДокумент5 страницFinal ProjectAkshayОценок пока нет