Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- TOGAF 9 Template - Architecture DefinitionДокумент70 страницTOGAF 9 Template - Architecture DefinitionAhmadОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Hansson ReportДокумент2 страницыHansson ReportFatima NazОценок пока нет

- Cchem 87 2 0155Документ4 страницыCchem 87 2 0155GeorgetaОценок пока нет

- Cchem 87 2 0162Документ5 страницCchem 87 2 0162GeorgetaОценок пока нет

- Mixolab Rosell 2007Документ11 страницMixolab Rosell 2007GeorgetaОценок пока нет

- PCR ErgosterolДокумент10 страницPCR ErgosterolGeorgetaОценок пока нет

- WheatProteins2005 UnlockedДокумент20 страницWheatProteins2005 UnlockedGeorgetaОценок пока нет

- Planning For GrowthДокумент22 страницыPlanning For GrowthGeorgetaОценок пока нет

- Principles of Risk Management and Insurance 13th Edition Rejda Solutions ManualДокумент36 страницPrinciples of Risk Management and Insurance 13th Edition Rejda Solutions Manualoutlying.pedantry.85yc100% (23)

- Spe/Iadc: SPE/IADC 21900 Incentive Contract: A Contractor's ViewpointДокумент7 страницSpe/Iadc: SPE/IADC 21900 Incentive Contract: A Contractor's Viewpointjoo123456789Оценок пока нет

- 2023 Oxy HSE Program Evaluation ChecklistДокумент2 страницы2023 Oxy HSE Program Evaluation ChecklistJibu GeorgeОценок пока нет

- 1statement of Standard 1Документ23 страницы1statement of Standard 1Ivan de Jesus Candelero MoralesОценок пока нет

- Cochrane Handbook 21-2019Документ24 страницыCochrane Handbook 21-2019Gilda BBTTОценок пока нет

- Working Platforms To BRE or Not To BRE Is The Question Mar 16 AG PDFДокумент11 страницWorking Platforms To BRE or Not To BRE Is The Question Mar 16 AG PDFnearmonkeyОценок пока нет

- Guía de Validación de Limpieza para APIsДокумент62 страницыGuía de Validación de Limpieza para APIsJosuePerezОценок пока нет

- Finance ChecklistДокумент30 страницFinance ChecklistMehaboob BashaОценок пока нет

- The Adolescent Brain: B.J. C, R M. J, T A. HДокумент16 страницThe Adolescent Brain: B.J. C, R M. J, T A. HTOOBA KANWALОценок пока нет

- Lehman Brothers Kerkhof Inflation Derivatives Explained Markets Products and PricingДокумент81 страницаLehman Brothers Kerkhof Inflation Derivatives Explained Markets Products and Pricingvolcom808Оценок пока нет

- Measuring ResilienceДокумент51 страницаMeasuring ResilienceLogmanОценок пока нет

- 4 - AIS ReviewerДокумент1 страница4 - AIS ReviewerAira Jaimee GonzalesОценок пока нет

- NSR and Bulk ShippingДокумент7 страницNSR and Bulk ShippingLea BrooklynОценок пока нет

- Isa 200Документ5 страницIsa 200baabasaamОценок пока нет

- 12 Day OfficersДокумент13 страниц12 Day Officerslazuli29100% (4)

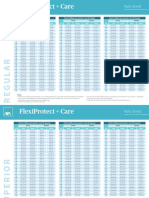

- Flexi+Care Rate SheetДокумент3 страницыFlexi+Care Rate SheetNeil MijaresОценок пока нет

- Digital Transformation Cyber Security PDFДокумент40 страницDigital Transformation Cyber Security PDFPrashant MahajanОценок пока нет

- A-Ehs-I-002 Hiradc Table, Rev.AДокумент3 страницыA-Ehs-I-002 Hiradc Table, Rev.ATrio Budi SantosoОценок пока нет

- Liquidity Cascades - Newfound Research PDFДокумент19 страницLiquidity Cascades - Newfound Research PDFrwmortell3580Оценок пока нет

- Bridge Protective Ship CollisionДокумент200 страницBridge Protective Ship CollisionJuniorJavier Olivo FarreraОценок пока нет

- Ba7205-Information Management Notes RejinpaulДокумент166 страницBa7205-Information Management Notes RejinpaulChinthana Jeremey100% (1)

- On Operational Risk at UbsДокумент23 страницыOn Operational Risk at UbsSai KrishnaОценок пока нет

- Module 1 Financial MGT 2Документ16 страницModule 1 Financial MGT 2Rey Phoenix PasilanОценок пока нет

- AWS Auditing Security Checklist PDFДокумент28 страницAWS Auditing Security Checklist PDFnandaanujОценок пока нет

- Funeral Poverty Individual AssingmentДокумент10 страницFuneral Poverty Individual AssingmentMuhamad Nur HijirahОценок пока нет

- CoP - 20.0 - Safety in Design (Construction)Документ13 страницCoP - 20.0 - Safety in Design (Construction)Niel Brian VillarazoОценок пока нет

- Responsible Use of Media and Information and Evolution of MediaДокумент35 страницResponsible Use of Media and Information and Evolution of MediaERICKA GRACE DA SILVAОценок пока нет

- On Cheating in Examinations: A Letter T O A H I G H School PrincipalДокумент5 страницOn Cheating in Examinations: A Letter T O A H I G H School PrincipalWynzyl Albien ElojaОценок пока нет