Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Audit of Cash and Cash EquivalentsДокумент38 страницAudit of Cash and Cash Equivalentsxxxxxxxxx86% (81)

- Auditing TheoryДокумент10 страницAuditing TheoryAnna Mae SanchezОценок пока нет

- Case Digest Week 5 6 PDFДокумент4 страницыCase Digest Week 5 6 PDFFaye Michelle RegisОценок пока нет

- Auditing Theory 250 QuestionsДокумент39 страницAuditing Theory 250 Questionsxxxxxxxxx75% (4)

- CHAPTER 7 Caselette - Audit of PPEДокумент34 страницыCHAPTER 7 Caselette - Audit of PPErochielanciola60% (5)

- Audit Cash and EquivalentsДокумент16 страницAudit Cash and EquivalentsErnest Andales0% (1)

- BS ACCOUNTANCY Course RequirementsДокумент4 страницыBS ACCOUNTANCY Course RequirementsMegumi HideyukiОценок пока нет

- Jardeleza v. JBC Due Process Ruling (2014Документ5 страницJardeleza v. JBC Due Process Ruling (2014Emir Mendoza100% (1)

- Palileo v. CosioДокумент4 страницыPalileo v. CosioHency TanbengcoОценок пока нет

- Judicial Affidavit of PetitionerДокумент7 страницJudicial Affidavit of PetitionerJonathan Accounting100% (1)

- 1 Interpleader Cases 1 10Документ11 страниц1 Interpleader Cases 1 10Anonymous fnlSh4KHIgОценок пока нет

- Bitoy Javier Vs Fly AceДокумент2 страницыBitoy Javier Vs Fly AceEdu RiparipОценок пока нет

- CIS Passport BlankДокумент3 страницыCIS Passport BlankIgor Basquerotto de CarvalhoОценок пока нет

- Audt 01Документ3 страницыAudt 01Megumi HideyukiОценок пока нет

- CH 9 Answers 2008Документ3 страницыCH 9 Answers 2008ergiesonaОценок пока нет

- Draft OBE Curriculum - AccountancyДокумент31 страницаDraft OBE Curriculum - AccountancyDymphna Ann CalumpianoОценок пока нет

- Auditor Responsibilities Material InconsistenciesДокумент5 страницAuditor Responsibilities Material InconsistenciesMegumi HideyukiОценок пока нет

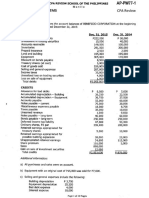

- Computation of Cash and Cash EquivalentsДокумент10 страницComputation of Cash and Cash EquivalentsMegumi HideyukiОценок пока нет

- Ap Q PDFДокумент14 страницAp Q PDFMegumi HideyukiОценок пока нет

- Taxation. JoyДокумент3 страницыTaxation. JoyMegumi HideyukiОценок пока нет

- TaxationДокумент3 страницыTaxationMegumi HideyukiОценок пока нет

- Bsa CurriculumДокумент2 страницыBsa CurriculumMegumi HideyukiОценок пока нет

- Accountancy XUДокумент3 страницыAccountancy XURob VillaluzОценок пока нет

- Bsacctcy 2014Документ7 страницBsacctcy 2014Ryan Joseph Agluba DimacaliОценок пока нет

- Social Security System: Collection List Summary For The Month of September 2018Документ2 страницыSocial Security System: Collection List Summary For The Month of September 2018Megumi HideyukiОценок пока нет

- Social Security System vs. Jarque Vda. de BailonДокумент16 страницSocial Security System vs. Jarque Vda. de BailonQueenie SabladaОценок пока нет

- Eviction Notice Filed Against Curtis Coats in Gwinnett County, Ga. - June 2017Документ2 страницыEviction Notice Filed Against Curtis Coats in Gwinnett County, Ga. - June 2017Anonymous Pb39klJОценок пока нет

- Syllabus UST PDFДокумент5 страницSyllabus UST PDFJyrus CimatuОценок пока нет

- Gonzales V Gonzales 90 Phil 444 1951Документ7 страницGonzales V Gonzales 90 Phil 444 1951Jordine UmayamОценок пока нет

- The Castle DoctrineДокумент5 страницThe Castle DoctrineChris WalkerОценок пока нет

- The Veil of Corporate Fiction : Federico B. MorenoДокумент24 страницыThe Veil of Corporate Fiction : Federico B. Morenohiroshika wsabiОценок пока нет

- BIR clarifies audit program and tax agent responsibilitiesДокумент2 страницыBIR clarifies audit program and tax agent responsibilitiesCkey ArОценок пока нет

- HRTO Perjury Lawsuit Internet Version Krishnan Venkatakrishnan Maurice Yeates Cathy Faye Elizabeth Kosmidis Judith Allen RyersonДокумент12 страницHRTO Perjury Lawsuit Internet Version Krishnan Venkatakrishnan Maurice Yeates Cathy Faye Elizabeth Kosmidis Judith Allen Ryersonsid_senadheeraОценок пока нет

- Dennis Gabionza Vs CAДокумент2 страницыDennis Gabionza Vs CAanailabucaОценок пока нет

- Of First Instance of Rizal, Branch V, and The Chief of Police of Quezon CityДокумент1 страницаOf First Instance of Rizal, Branch V, and The Chief of Police of Quezon CityPlaneteer Prana100% (1)

- Luzan VS SiaДокумент1 страницаLuzan VS SiaBenedict AlvarezОценок пока нет

- Introduction To Military Life: (Legal Basis)Документ8 страницIntroduction To Military Life: (Legal Basis)Joseph Neil TacataniОценок пока нет

- De Silva Cruz V People Anthony de Silva Cruz vs. People of The PhilippinesДокумент9 страницDe Silva Cruz V People Anthony de Silva Cruz vs. People of The PhilippinesAdrian KitОценок пока нет

- Atty. Ortega EthicsДокумент2 страницыAtty. Ortega EthicsKitem Kadatuan Jr.Оценок пока нет

- Protection of Famous Marks in AustraliaДокумент73 страницыProtection of Famous Marks in Australiaj3r1c0d5Оценок пока нет

- Bail 9-C Faizan HCДокумент5 страницBail 9-C Faizan HCKashif Abbas0% (1)

- Intellectual Property LawsДокумент19 страницIntellectual Property LawsPrathap SankarОценок пока нет

- Nevada Reports 1978 (94 Nev.) PDFДокумент776 страницNevada Reports 1978 (94 Nev.) PDFthadzigsОценок пока нет

- Alternative Dispute Resolution System: Concept and History of Adr in IndiaДокумент10 страницAlternative Dispute Resolution System: Concept and History of Adr in IndiaTanu0% (1)

- Cybercrime ManuscriptДокумент10 страницCybercrime ManuscriptNikko San QuimioОценок пока нет

- Ray Gordon Parker Opposition To Rule 11 Motion For SanctionsДокумент69 страницRay Gordon Parker Opposition To Rule 11 Motion For SanctionsAdam SteinbaughОценок пока нет

- J. Tiosejo Investment Corp. Vs AngДокумент15 страницJ. Tiosejo Investment Corp. Vs AngnaldsdomingoОценок пока нет

- MDY Industries, LLC v. Blizzard Entertainment, Inc. Et Al - Document No. 25Документ4 страницыMDY Industries, LLC v. Blizzard Entertainment, Inc. Et Al - Document No. 25Justia.comОценок пока нет