Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Art-Tech Requirement: Updated: March 25, 2002 Yayoi MarunoДокумент7 страницArt-Tech Requirement: Updated: March 25, 2002 Yayoi MarunoTHATGUYtmОценок пока нет

- POWERVC Quick Deployment GuideДокумент7 страницPOWERVC Quick Deployment GuideAhmed (Mash) MashhourОценок пока нет

- A Survey of FPGA-Based Robotic ComputingДокумент27 страницA Survey of FPGA-Based Robotic ComputingjjoossiiffОценок пока нет

- Virtual Memory Management Using Memory BallooningДокумент5 страницVirtual Memory Management Using Memory BallooningsoniathalavoorОценок пока нет

- DX3224H (DX3224HV) Multi-Channel Encoder Spec 2019.6.27Документ3 страницыDX3224H (DX3224HV) Multi-Channel Encoder Spec 2019.6.27Ahmad MuzayyinОценок пока нет

- Brian C. Houlihan: 1413 SW 11th Street Cape Coral, FL 33991Документ1 страницаBrian C. Houlihan: 1413 SW 11th Street Cape Coral, FL 33991Brian HoulihanОценок пока нет

- Ryan B. Harvey's ResumeДокумент1 страницаRyan B. Harvey's ResumeRyan B HarveyОценок пока нет

- SZL Tensioner For Kawasaki Barako 175, 9857-278 - Lazada PHДокумент2 страницыSZL Tensioner For Kawasaki Barako 175, 9857-278 - Lazada PHjenn besana TataОценок пока нет

- SCAN Skills Assessment - Packet Tracer: CCNA Routing and Switching Switched NetworksДокумент7 страницSCAN Skills Assessment - Packet Tracer: CCNA Routing and Switching Switched NetworksJerome De GuzmanОценок пока нет

- Manik and An Parthasarathy ProfileДокумент4 страницыManik and An Parthasarathy ProfileManikandan ParthasarathyОценок пока нет

- Cambridge International AS & A Level: Computer Science 9608/11Документ16 страницCambridge International AS & A Level: Computer Science 9608/11Zaki JrОценок пока нет

- Figure 4-35. Modelsim Altera Starter Edition: Hello World!Документ5 страницFigure 4-35. Modelsim Altera Starter Edition: Hello World!ali alilouОценок пока нет

- Simulate ONTAP 8.2 Step-by-Step Installation (Nau-Final) PDFДокумент53 страницыSimulate ONTAP 8.2 Step-by-Step Installation (Nau-Final) PDFKishore ChowdaryОценок пока нет

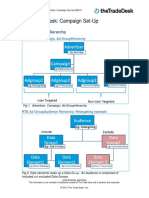

- The Trade DeskДокумент13 страницThe Trade DeskAmpLiveОценок пока нет

- PKS UserGuide PDFДокумент53 страницыPKS UserGuide PDFrigaut74Оценок пока нет

- Ping, TnspingДокумент3 страницыPing, TnspingKrzysztof PrzedniczekОценок пока нет

- Programmable Terminal NP-Designer: User'S ManualДокумент298 страницProgrammable Terminal NP-Designer: User'S ManualGustavo BalderramaОценок пока нет

- Computer NetworkingДокумент5 страницComputer NetworkingJINALОценок пока нет

- Neural NetworksДокумент57 страницNeural Networksalexaalex100% (1)

- Historical ETH data from 2013-2018Документ130 страницHistorical ETH data from 2013-2018wesamОценок пока нет

- Family Budget (Monthly) 1Документ5 страницFamily Budget (Monthly) 1Jesiél Da RochaОценок пока нет

- Carleton U Inglis Technology ReportДокумент10 страницCarleton U Inglis Technology ReportMarcelo RufinoОценок пока нет

- Temu Explore The Latest Clothing, Beauty, Home, Jewelry & MoreДокумент1 страницаTemu Explore The Latest Clothing, Beauty, Home, Jewelry & MoreiamjameschapmanОценок пока нет

- Useful CommandsДокумент61 страницаUseful CommandsPradeep KoyiladaОценок пока нет

- Linux Boot Loader and Boot in Raspberry Pi: Jonne SoininenДокумент6 страницLinux Boot Loader and Boot in Raspberry Pi: Jonne SoininenGabriel Astudillo MuñozОценок пока нет

- Online Admission Management SystemДокумент12 страницOnline Admission Management System30- rohan kirjatОценок пока нет

- Energy Conservation Building Code For Residential BuildingsДокумент23 страницыEnergy Conservation Building Code For Residential BuildingsAnonymous Qm0zbNkОценок пока нет

- UiPath Robotic Process Automation ProjectsДокумент380 страницUiPath Robotic Process Automation ProjectsBaloo100% (1)

- Handy Unix Commands For A DBAДокумент3 страницыHandy Unix Commands For A DBAmdrajivОценок пока нет

- Oracle Mobile Application Server Changes in Release 12: Administrator's GuideДокумент13 страницOracle Mobile Application Server Changes in Release 12: Administrator's GuideIonut MargaritescuОценок пока нет