Вам также может понравиться

- Chapter 1 - Statement of Financial Position: Problem 1-1 (IFRS)Документ38 страницChapter 1 - Statement of Financial Position: Problem 1-1 (IFRS)Asi Cas Jav0% (1)

- Audit of LiabilitiesДокумент33 страницыAudit of Liabilitiesxxxxxxxxx96% (28)

- Acctg Problem 7Документ4 страницыAcctg Problem 7Salvie Perez Utana57% (14)

- 10 FS Analysis Sample Exam Discussion KEYДокумент10 страниц10 FS Analysis Sample Exam Discussion KEYrav danoОценок пока нет

- Exercise 6 June 1Документ3 страницыExercise 6 June 1Jonna Mae Bandoquillo100% (1)

- HO No. 1 - Financial Statements AnalysisДокумент3 страницыHO No. 1 - Financial Statements AnalysisJOHANNAОценок пока нет

- FS AnalysisДокумент1 страницаFS AnalysisJoeОценок пока нет

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeОт EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeОценок пока нет

- Income Statement SimДокумент5 страницIncome Statement Simjustwon100% (1)

- CMA Formula Part 1 FinalДокумент47 страницCMA Formula Part 1 FinalMohammed Kashif100% (1)

- Mas M 1404 Financial Statements AnalysisДокумент22 страницыMas M 1404 Financial Statements Analysisxxx101xxxОценок пока нет

- FS Analysis Ans KeyДокумент5 страницFS Analysis Ans KeyTeofel John Alvizo PantaleonОценок пока нет

- Forecasting 2Документ4 страницыForecasting 2Gva Umayam0% (1)

- Second Quiz On FS Analysis PDFДокумент2 страницыSecond Quiz On FS Analysis PDFRandy ManzanoОценок пока нет

- MOD2 Statement of Cash FlowsДокумент2 страницыMOD2 Statement of Cash FlowsGemma DenolanОценок пока нет

- Additional Cash Flow ProblemsДокумент3 страницыAdditional Cash Flow ProblemsChelle HullezaОценок пока нет

- For Questions 6Документ3 страницыFor Questions 6Meghan Kaye LiwenОценок пока нет

- Advanced AccountingДокумент10 страницAdvanced AccountingLhyn Cantal CalicaОценок пока нет

- P 1Документ13 страницP 1Ryan Joseph Agluba DimacaliОценок пока нет

- Final Examination AK (60 COPIES)Документ9 страницFinal Examination AK (60 COPIES)Sittie Ainna A. UnteОценок пока нет

- PRACTICEДокумент4 страницыPRACTICEGleeson Jay NiedoОценок пока нет

- Module 9 and 10Документ9 страницModule 9 and 10French Jame RianoОценок пока нет

- Exercise 2 Statement of Financial PositionДокумент8 страницExercise 2 Statement of Financial Positionjumawaymichaeljeffrey65Оценок пока нет

- Afar. Diagnostic: Response: Correct Answer: Score: 1 Out of 1 YesДокумент31 страницаAfar. Diagnostic: Response: Correct Answer: Score: 1 Out of 1 YesMitch MinglanaОценок пока нет

- Cbea FAR 01 Lecture 02Документ16 страницCbea FAR 01 Lecture 02Osirisheen Aizle CubacubОценок пока нет

- AC15 Quiz 1 Test PaperДокумент6 страницAC15 Quiz 1 Test PaperKristine Esplana ToraldeОценок пока нет

- Teamprtc Mock Board Oct 2020 Afar PDFДокумент16 страницTeamprtc Mock Board Oct 2020 Afar PDFBryle EscosaОценок пока нет

- AccountingДокумент9 страницAccountingTakuriОценок пока нет

- Business CombinationДокумент3 страницыBusiness Combinationlov3m3Оценок пока нет

- Module 1 - Financial Statement Analysis - P2Документ4 страницыModule 1 - Financial Statement Analysis - P2Jose Eduardo GumafelixОценок пока нет

- Assignment 1Документ2 страницыAssignment 1Mitch wongОценок пока нет

- Review On FinmanДокумент7 страницReview On FinmanMoira C. VilogОценок пока нет

- Josie B. Aguila, Mbmba: Financial Accounting For IeДокумент6 страницJosie B. Aguila, Mbmba: Financial Accounting For IeCATHERINE FRANCE LALUCISОценок пока нет

- AcctgДокумент11 страницAcctgsarahbee100% (2)

- Handouts ConsolidationSubsequent To Date of AcquisitionДокумент5 страницHandouts ConsolidationSubsequent To Date of AcquisitionCPAОценок пока нет

- Practical Accounting 2 (P2)Документ12 страницPractical Accounting 2 (P2)Nico evansОценок пока нет

- Homework: Working Capital Management 2021coardbulji: ActivityДокумент3 страницыHomework: Working Capital Management 2021coardbulji: ActivityMa Teresa B. CerezoОценок пока нет

- TERMINAL OUTPUT FOR THE FINAL TERM EditedДокумент3 страницыTERMINAL OUTPUT FOR THE FINAL TERM EditedMillen Austria0% (1)

- ACC212 - FSA Black BoardДокумент1 страницаACC212 - FSA Black Boardjuztine dofitasОценок пока нет

- Act 102 FinalsДокумент5 страницAct 102 FinalsJamii Dalidig MacarambonОценок пока нет

- Handouts ConsolidationIntercompany Sale of Plant AssetsДокумент3 страницыHandouts ConsolidationIntercompany Sale of Plant AssetsCPAОценок пока нет

- Activity 3 - Financial RatiosДокумент3 страницыActivity 3 - Financial RatiosNCF- Student Assistants' OrganizationОценок пока нет

- FINANCIAL STATEMENT ANALYSIS - Practice Set PDFДокумент4 страницыFINANCIAL STATEMENT ANALYSIS - Practice Set PDFDwight Manikan EchagueОценок пока нет

- Cfas Pfa 01Документ194 страницыCfas Pfa 01Kimberly Claire Atienza100% (1)

- Review Notes #2 - Comprehensive Problem PDFДокумент3 страницыReview Notes #2 - Comprehensive Problem PDFtankofdoom 4Оценок пока нет

- FAR2Документ8 страницFAR2Kenneth DiabordoОценок пока нет

- Cash FlowДокумент15 страницCash FlowCandy BayonaОценок пока нет

- FAR Activity Feb 19 With AnswersДокумент16 страницFAR Activity Feb 19 With AnswersCybill AiraОценок пока нет

- Far Reviewer QualiДокумент124 страницыFar Reviewer Qualijestoni alvezОценок пока нет

- Afar 2019Документ9 страницAfar 2019TakuriОценок пока нет

- Quiz - Solution - PAS - 1 - and - PAS - 2.pdf Filename - UTF-8''Quiz (Solution) % PDFДокумент3 страницыQuiz - Solution - PAS - 1 - and - PAS - 2.pdf Filename - UTF-8''Quiz (Solution) % PDFSamuel BandibasОценок пока нет

- Accounting For Business CombinationsДокумент5 страницAccounting For Business CombinationsJohn JackОценок пока нет

- PRE BATTERY EXAM 2018 Part 1 FARДокумент11 страницPRE BATTERY EXAM 2018 Part 1 FARFrl RizalОценок пока нет

- Sevilla - Unit 1 - IA3Документ14 страницSevilla - Unit 1 - IA3Hensel SevillaОценок пока нет

- Tax ProblemsДокумент14 страницTax Problemsrav dano100% (1)

- AFARДокумент9 страницAFARRed Christian PalustreОценок пока нет

- Module No. 1 - Week 1 Businessn CombinationДокумент5 страницModule No. 1 - Week 1 Businessn CombinationJayaAntolinAyusteОценок пока нет

- Dayag BusinessCombДокумент3 страницыDayag BusinessCombtaherehОценок пока нет

- First Quiz On Liquidity and Solvency Ratios PDFДокумент2 страницыFirst Quiz On Liquidity and Solvency Ratios PDFRandy ManzanoОценок пока нет

- Topic 10 - Practice ProblemsДокумент2 страницыTopic 10 - Practice ProblemsAnna Mariyaahh DeblosanОценок пока нет

- Finance ProblemsДокумент2 страницыFinance Problemsjaydee magalangОценок пока нет

- Wealth Management Planning: The UK Tax PrinciplesОт EverandWealth Management Planning: The UK Tax PrinciplesРейтинг: 4.5 из 5 звезд4.5/5 (2)

- Equity Valuation: Models from Leading Investment BanksОт EverandEquity Valuation: Models from Leading Investment BanksJan ViebigОценок пока нет

- Internal Control of Fixed Assets: A Controller and Auditor's GuideОт EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideРейтинг: 4 из 5 звезд4/5 (1)

- 2004 Metrobank-MTAP Division Elimination - Grade 5Документ6 страниц2004 Metrobank-MTAP Division Elimination - Grade 5Imelda Arreglo-AgripaОценок пока нет

- 2002 Metrobank-MTAP Division Elimination - Grade 5Документ5 страниц2002 Metrobank-MTAP Division Elimination - Grade 5Michael Edward Nepomuceno DeVillaОценок пока нет

- 2002 Metrobank-MTAP Division Elimination - Grade 5Документ5 страниц2002 Metrobank-MTAP Division Elimination - Grade 5Michael Edward Nepomuceno DeVillaОценок пока нет

- IFRS 16 Effects Analysis PDFДокумент104 страницыIFRS 16 Effects Analysis PDFKaren LiebheartОценок пока нет

- TBCH03Документ10 страницTBCH03PatrickBeronaОценок пока нет

- XAppendixIII - Inventory ManagementДокумент3 страницыXAppendixIII - Inventory Managementronin214Оценок пока нет

- Financial Managemenent 6 Financial Statement AnalysisДокумент9 страницFinancial Managemenent 6 Financial Statement Analysisvincevelasquez0% (1)

- SCIENCE ReviewerДокумент7 страницSCIENCE ReviewervincevelasquezОценок пока нет

- Mas Quizzer1Документ30 страницMas Quizzer1vincevelasquezОценок пока нет

- Arwana Citramulia TBK - BillingualДокумент87 страницArwana Citramulia TBK - BillingualJefri Formen PangaribuanОценок пока нет

- What Kind of Numericals Are Asked in Finance Paper (Phase-2) of RBI Grade B Exam - QuoraДокумент12 страницWhat Kind of Numericals Are Asked in Finance Paper (Phase-2) of RBI Grade B Exam - QuoravidursenОценок пока нет

- Project: Jay FarmsДокумент12 страницProject: Jay FarmsSivanesan RamamoorthyОценок пока нет

- Alco Sec 17Q Q3 2021 - Fin - PseДокумент69 страницAlco Sec 17Q Q3 2021 - Fin - PseOIdjnawoifhaoifОценок пока нет

- Exam 2Документ19 страницExam 2SHE50% (2)

- Question 5: Ias 7 Statements of Cash FlowsДокумент4 страницыQuestion 5: Ias 7 Statements of Cash FlowsShiza ArifОценок пока нет

- Answers To True or False, Relating To SFP, With ExplanationsДокумент3 страницыAnswers To True or False, Relating To SFP, With ExplanationsPATRICIA SANTOS100% (1)

- The Role of Accounting in Decision Making: Transaction AnalysisДокумент10 страницThe Role of Accounting in Decision Making: Transaction AnalysisHashara WarnasooriyaОценок пока нет

- FAR460 - S - June 2018 - StudentsДокумент6 страницFAR460 - S - June 2018 - StudentsRuzaikha razaliОценок пока нет

- Comprehensive ProblemДокумент2 страницыComprehensive ProblemErik NavarroОценок пока нет

- Problems On Redemption of Pref SharesДокумент7 страницProblems On Redemption of Pref SharesYashitha CaverammaОценок пока нет

- Presentation of Financial Statements: IASB Documents Published To Accompany Ias 1Документ30 страницPresentation of Financial Statements: IASB Documents Published To Accompany Ias 1Kemala Putri AyundaОценок пока нет

- P3 4Документ3 страницыP3 4Nam Nguyen100% (1)

- Ilovepdf MergedДокумент9 страницIlovepdf MergedGARTMiawОценок пока нет

- Balance Sheet of RaymondДокумент5 страницBalance Sheet of RaymondRachana Yashwant PatneОценок пока нет

- Income Statement: Company NameДокумент9 страницIncome Statement: Company NameAkshay SinghОценок пока нет

- Chapter 15Документ12 страницChapter 15Nikki GarciaОценок пока нет

- CiplaДокумент5 страницCiplaSantosh AgarwalОценок пока нет

- CH9 Long-Lived AssetsДокумент42 страницыCH9 Long-Lived AssetsStudent Sokha ChanchesdaОценок пока нет

- Week 1 Practice Questions and TemplateДокумент8 страницWeek 1 Practice Questions and TemplatealexandraОценок пока нет

- Khandelwal CmaДокумент40 страницKhandelwal CmaraviОценок пока нет

- CORPORATION LIQUIDATION - AcctnfДокумент2 страницыCORPORATION LIQUIDATION - AcctnfJewel CabigonОценок пока нет

- More SCF Topics and EBITDA Slides 3 3 2 V2Документ25 страницMore SCF Topics and EBITDA Slides 3 3 2 V2Yash DiwakarОценок пока нет

- Exercises On Hyperinflation and Cost AccountingДокумент4 страницыExercises On Hyperinflation and Cost AccountingMaan CabolesОценок пока нет

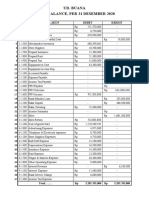

- Jawaban Buku Besar UD. BUANA P3Документ10 страницJawaban Buku Besar UD. BUANA P3HusniBaroqОценок пока нет

- D.G Khan Cement Company Limited Income StatementДокумент25 страницD.G Khan Cement Company Limited Income StatementadnanjeeОценок пока нет