Вам также может понравиться

- SERIES 24 EXAM STUDY GUIDE 2021 + TEST BANKОт EverandSERIES 24 EXAM STUDY GUIDE 2021 + TEST BANKОценок пока нет

- MF Sample Paper 01Документ69 страницMF Sample Paper 01mirza_ajmalОценок пока нет

- Nism Book Summary: Nismtop500 - Series Iiia-Securities Intr ComplianceДокумент44 страницыNism Book Summary: Nismtop500 - Series Iiia-Securities Intr Compliancebhavani sankar areОценок пока нет

- Concept and Role of Mutual FundДокумент23 страницыConcept and Role of Mutual FundChetana SoniОценок пока нет

- Nism X B Caselet 7Документ8 страницNism X B Caselet 7Finware 1Оценок пока нет

- Mutual Fund-Question BankДокумент32 страницыMutual Fund-Question Bankapi-3706352Оценок пока нет

- FIMDDA Debt Module1Документ7 страницFIMDDA Debt Module1Kirti SahniОценок пока нет

- Solution For Ca Final SFM Nov 15 Paper (Practical Questions) by Ca Praviin MahajanДокумент18 страницSolution For Ca Final SFM Nov 15 Paper (Practical Questions) by Ca Praviin MahajanPravinn_Mahajan50% (2)

- Chapter 19 Mutual FundsДокумент20 страницChapter 19 Mutual FundsdurgaselvamОценок пока нет

- Certificate Course MCQ Answers PDFДокумент17 страницCertificate Course MCQ Answers PDFSijal KhanОценок пока нет

- Portfolio Management Through Mutual FundsДокумент14 страницPortfolio Management Through Mutual FundsMedha SinghОценок пока нет

- Nism Mutual Fund VaДокумент24 страницыNism Mutual Fund VaKanikaa B KaliyaОценок пока нет

- Ccra Level 2 SyllabusДокумент8 страницCcra Level 2 SyllabusPavan ValishettyОценок пока нет

- NISM Series v-A-Mutual Fund Distributors Workbook - 2020Документ341 страницаNISM Series v-A-Mutual Fund Distributors Workbook - 2020prachiОценок пока нет

- ICFAI University MBA Paper 2Документ18 страницICFAI University MBA Paper 2Rihaan ShakeelОценок пока нет

- CA Final Audit (New) Question Paper Suggested AnswerДокумент15 страницCA Final Audit (New) Question Paper Suggested AnswerSri PavanОценок пока нет

- Mutual Fund Distributor Exam Nism Study Material PDFДокумент56 страницMutual Fund Distributor Exam Nism Study Material PDFamita YadavОценок пока нет

- Chapter-1: Issue Issue / Stock SplitДокумент21 страницаChapter-1: Issue Issue / Stock SplitNidheesh BabuОценок пока нет

- SFM CA Final Mutual FundДокумент7 страницSFM CA Final Mutual FundShrey KunjОценок пока нет

- NISM Sample Question-1Документ7 страницNISM Sample Question-1nanda100% (1)

- Currency (1) 222 PDFДокумент81 страницаCurrency (1) 222 PDFSoumitra NaiyaОценок пока нет

- Icfai2008 - 1307514033 Security AnalysisДокумент17 страницIcfai2008 - 1307514033 Security AnalysisJatin GoyalОценок пока нет

- Series-V-A: Mutual Fund Distributors Certification ExaminationДокумент218 страницSeries-V-A: Mutual Fund Distributors Certification ExaminationAjithreddy BasireddyОценок пока нет

- CFP - Module 1 - IIFP - StudentsДокумент269 страницCFP - Module 1 - IIFP - StudentsmodisahebОценок пока нет

- 2 - Integrated L&SCMДокумент1 страница2 - Integrated L&SCMsukumaran321Оценок пока нет

- Caiib Rmmodb Nov08Документ24 страницыCaiib Rmmodb Nov08Gaurav Singh100% (1)

- NSDL NotesДокумент14 страницNSDL NotesAnmol RahangdaleОценок пока нет

- WWW - Modelexam.in Offers Online Model Exams For NISM, NCFM & BCFM Exams. Register Now!Документ24 страницыWWW - Modelexam.in Offers Online Model Exams For NISM, NCFM & BCFM Exams. Register Now!SATISH BHARADWAJОценок пока нет

- Group-6 Presentation On FIIДокумент42 страницыGroup-6 Presentation On FIIPankaj Kumar Bothra100% (1)

- Characteristic Features of Financial InstrumentsДокумент17 страницCharacteristic Features of Financial Instrumentsmanoranjanpatra93% (15)

- Clearing and Settlement: Financial DerivativesДокумент28 страницClearing and Settlement: Financial DerivativesnarunsankarОценок пока нет

- FRM 5 Market Risk Related RisksДокумент38 страницFRM 5 Market Risk Related RisksLoraОценок пока нет

- 1164914469ls 1Документ112 страниц1164914469ls 1krishnan bhuvaneswariОценок пока нет

- HSBC Amfi Mock Test-2Документ12 страницHSBC Amfi Mock Test-2Ankit SharmaОценок пока нет

- Icfai Model PapersДокумент23 страницыIcfai Model Papersshubhamjain45Оценок пока нет

- Mutual Funds: Presented By: Saurabh Tamrakar Ravikant Tiwari Prateek DevraДокумент25 страницMutual Funds: Presented By: Saurabh Tamrakar Ravikant Tiwari Prateek DevraChanchal KansalОценок пока нет

- Derivative Securities MarketsДокумент20 страницDerivative Securities MarketsPatrick Earl T. PintacОценок пока нет

- Pass 4 Sure NotesДокумент76 страницPass 4 Sure NotesNarendar KumarОценок пока нет

- Merchant BankingДокумент19 страницMerchant BankingMiral PatelОценок пока нет

- 1.2 Doc-20180120-Wa0002Документ23 страницы1.2 Doc-20180120-Wa0002Prachet KulkarniОценок пока нет

- Mutual Fund Question Bank-2Документ33 страницыMutual Fund Question Bank-2api-3773732Оценок пока нет

- ICFAI MIFA Course Group C Financial Markets Exam - Paper1Документ27 страницICFAI MIFA Course Group C Financial Markets Exam - Paper1Ameya RanadiveОценок пока нет

- Sample Exam QuestionsДокумент16 страницSample Exam QuestionsMadina SuleimenovaОценок пока нет

- Level 2 300 QuestionДокумент207 страницLevel 2 300 QuestionAshish shrivastava100% (1)

- WWW - Modelexam.in: Study Notes For Nism - Investment Adviser Level 1 - Series Xa (10A)Документ29 страницWWW - Modelexam.in: Study Notes For Nism - Investment Adviser Level 1 - Series Xa (10A)sharadОценок пока нет

- Basics of EquityДокумент27 страницBasics of EquityVikas Jeshnani100% (1)

- Introduction To Financial Systems and Financial MarketsДокумент22 страницыIntroduction To Financial Systems and Financial MarketsDiana Rose L. BautistaОценок пока нет

- HSBC Amfi Mock Test-1Документ10 страницHSBC Amfi Mock Test-1Ankit Sharma100% (1)

- Amfi Advisors Module NotesДокумент57 страницAmfi Advisors Module NotesMahekОценок пока нет

- CML Vs SMLДокумент9 страницCML Vs SMLnasir abdulОценок пока нет

- Finance Mid TermДокумент4 страницыFinance Mid TermbloodinawineglasОценок пока нет

- Nism 8 - Equity Derivatives - Practice Test 2Документ19 страницNism 8 - Equity Derivatives - Practice Test 2complaints.tradeОценок пока нет

- Problems Sub-IfДокумент11 страницProblems Sub-IfChintakunta PreethiОценок пока нет

- Non-Banking Financial CompaniesДокумент59 страницNon-Banking Financial CompaniesFarhan JagirdarОценок пока нет

- NISM Key Learning PointsДокумент24 страницыNISM Key Learning PointsAmmaji GopaluniОценок пока нет

- Mock 12Документ28 страницMock 12Manan SharmaОценок пока нет

- Introduction To DerivativesДокумент7 страницIntroduction To DerivativesRashwanth TcОценок пока нет

- Investment (Index Model)Документ29 страницInvestment (Index Model)Quoc Anh NguyenОценок пока нет

- Foundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsОт EverandFoundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsОценок пока нет

- Accounts & Adv Account BookДокумент308 страницAccounts & Adv Account Bookvishnuverma100% (1)

- Harshad Jaju Vouching For IpccДокумент80 страницHarshad Jaju Vouching For IpccvishnuvermaОценок пока нет

- Smart Investment English (E-Copy)Документ48 страницSmart Investment English (E-Copy)vishnuvermaОценок пока нет

- DT Memory BookДокумент30 страницDT Memory Bookvishnuverma100% (1)

- Standards Full by Prof. Khushboo SanghaviДокумент76 страницStandards Full by Prof. Khushboo Sanghavivishnuverma100% (4)

- Inter SA Compact BookДокумент46 страницInter SA Compact Bookvishnuverma0% (1)

- CA Final SA Concept by Siddharth AgarwalДокумент54 страницыCA Final SA Concept by Siddharth Agarwalvishnuverma100% (1)

- Sbilife Q2fy19 Jbwa 261018Документ7 страницSbilife Q2fy19 Jbwa 261018vishnuvermaОценок пока нет

- IBC May 19 Arpita MamДокумент58 страницIBC May 19 Arpita Mamvishnuverma100% (8)

- GST Scanner by DG SirДокумент41 страницаGST Scanner by DG SirvishnuvermaОценок пока нет

- Vol 1. SampleДокумент41 страницаVol 1. SamplevishnuvermaОценок пока нет

- Vol 2. SampleДокумент23 страницыVol 2. SamplevishnuvermaОценок пока нет

- Auditing The Ultimate ShortДокумент13 страницAuditing The Ultimate ShortvishnuvermaОценок пока нет

- Chapter 1: Business Process Management and IT - : CA IPCC CourseДокумент44 страницыChapter 1: Business Process Management and IT - : CA IPCC CoursevishnuvermaОценок пока нет

- Ind As ChartsДокумент20 страницInd As ChartsvishnuvermaОценок пока нет

- Century TextileДокумент108 страницCentury TextilevishnuvermaОценок пока нет

- CA Inter Audit JKSCДокумент358 страницCA Inter Audit JKSCvishnuverma50% (2)

- Chapter 1: Business Process Management and IT - : Intermediate (IPC) CourseДокумент31 страницаChapter 1: Business Process Management and IT - : Intermediate (IPC) CoursevishnuvermaОценок пока нет

- Law Sebi MCQДокумент6 страницLaw Sebi MCQvishnuvermaОценок пока нет

- Miles Cma Review: Prospective Schedule For November 25, 2018, CMA Batch at MUMBAIДокумент1 страницаMiles Cma Review: Prospective Schedule For November 25, 2018, CMA Batch at MUMBAIvishnuvermaОценок пока нет

- Chapter 5: Vouching: Intermediate (IPC) CourseДокумент35 страницChapter 5: Vouching: Intermediate (IPC) CoursevishnuvermaОценок пока нет

- Cma 2018 New DetailДокумент7 страницCma 2018 New DetailvishnuvermaОценок пока нет

- Chapter 3: Preparation For An Audit - Audit Sampling: CA .Kamal GargДокумент27 страницChapter 3: Preparation For An Audit - Audit Sampling: CA .Kamal GargvishnuvermaОценок пока нет

- Chapter 1: Business Process Management and IT - : CA Intermediate (IPC) CourseДокумент25 страницChapter 1: Business Process Management and IT - : CA Intermediate (IPC) CoursevishnuvermaОценок пока нет

- NteДокумент8 страницNtevishnuvermaОценок пока нет

- CMA Pop Quiz #103: Part 1: Planning, Budgeting, and ForecastingДокумент3 страницыCMA Pop Quiz #103: Part 1: Planning, Budgeting, and ForecastingvishnuvermaОценок пока нет

- Chapter 10Документ14 страницChapter 10Nil PatilОценок пока нет

- TNB Electricity Supply Application Handbook ESAHДокумент130 страницTNB Electricity Supply Application Handbook ESAHnasbiwm100% (1)

- Share Subscription Agreement For Mbaegbu EbukaДокумент17 страницShare Subscription Agreement For Mbaegbu EbukaEkeoma VivianОценок пока нет

- BRELAДокумент2 страницыBRELAKiobya M KiobyaОценок пока нет

- 1 Digested Kapatiran NG Mga Naglilingkod Sa Pamahalaan V TanДокумент2 страницы1 Digested Kapatiran NG Mga Naglilingkod Sa Pamahalaan V TanRoli Sitjar Arangote100% (1)

- Employee Non Disclosure PDFДокумент2 страницыEmployee Non Disclosure PDFstitchieОценок пока нет

- Barangay Tax Ordinance N0. 7 2022Документ3 страницыBarangay Tax Ordinance N0. 7 2022Marielle Cate100% (2)

- Studies in COT DataДокумент100 страницStudies in COT Databrufpot100% (2)

- Survey Form 82A ISM Company Audit v2 1Документ12 страницSurvey Form 82A ISM Company Audit v2 1fghОценок пока нет

- Managing Director Product Management in New York City Resume Anthony ThalmanДокумент2 страницыManaging Director Product Management in New York City Resume Anthony ThalmanAnthony ThalmanОценок пока нет

- Guidelines For A Non-Agriculturist of Himachal Pradesh Who Desires To Purchase - Acquire Land in Himachal Pradesh Under Section PDFДокумент5 страницGuidelines For A Non-Agriculturist of Himachal Pradesh Who Desires To Purchase - Acquire Land in Himachal Pradesh Under Section PDFNavotna ShuklaОценок пока нет

- Managing Cyber Security V1 (Level-3)Документ20 страницManaging Cyber Security V1 (Level-3)venky_akella100% (2)

- Gift of SharesДокумент5 страницGift of SharesTaxpert Professionals Private LimitedОценок пока нет

- Dangerous SitproДокумент12 страницDangerous SitproClarence PieterszОценок пока нет

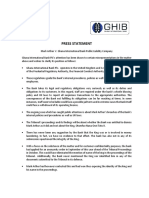

- Ghana International Bank's Press Statement On Otumfuor Money Laundering ScandalДокумент2 страницыGhana International Bank's Press Statement On Otumfuor Money Laundering ScandalGhanaWebОценок пока нет

- CE LawДокумент12 страницCE LawAarth CadavosОценок пока нет

- Method Statement For Installation of Telephone ManholeДокумент4 страницыMethod Statement For Installation of Telephone ManholemujtiobamaliblОценок пока нет

- Reg. BNR 5.2013 - ENДокумент219 страницReg. BNR 5.2013 - ENolteanunbogdanОценок пока нет

- 1-Rock Anchor PolicyДокумент3 страницы1-Rock Anchor PolicyManimaran PОценок пока нет

- GR 152613 and 152628Документ6 страницGR 152613 and 152628Marifel LagareОценок пока нет

- Audit ProcessAudit Process: How To Successfully Plan AuditДокумент8 страницAudit ProcessAudit Process: How To Successfully Plan AuditComplianceOnlineОценок пока нет

- IMPRESSIVE CONVEYANCING NOTES - by Onguto and KokiДокумент89 страницIMPRESSIVE CONVEYANCING NOTES - by Onguto and Kokikate80% (5)

- BUL 501 - Company Law 1Документ20 страницBUL 501 - Company Law 1kzrdur100% (1)

- 808A New Rotary Club Application enДокумент4 страницы808A New Rotary Club Application enEms San AntonioОценок пока нет

- How To Conduct An Internal Compliance InvestigationДокумент5 страницHow To Conduct An Internal Compliance InvestigationSunilОценок пока нет

- Maintenance Control Manual - Iss 3 Rev 00 - 21sept2015 PDFДокумент256 страницMaintenance Control Manual - Iss 3 Rev 00 - 21sept2015 PDFjorge100% (1)

- I A Just and Dynamic Social OrderДокумент17 страницI A Just and Dynamic Social OrderJen DeeОценок пока нет

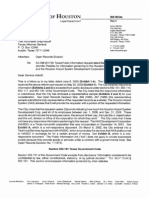

- Houston Airport System Letter To Texas Attorney General Regarding Payroll RecordsДокумент5 страницHouston Airport System Letter To Texas Attorney General Regarding Payroll RecordsjpeeblesОценок пока нет

- Classification of Public Lands Open To DispositionДокумент6 страницClassification of Public Lands Open To DispositionJoe LimОценок пока нет

- TheurimainareportДокумент22 страницыTheurimainareportVoke Magnus DigeratusОценок пока нет