Вам также может понравиться

- VO in Initiating Sep19Документ24 страницыVO in Initiating Sep19Ravi KiranОценок пока нет

- Apple Inc (Nas:Aapl) GurufocusДокумент7 страницApple Inc (Nas:Aapl) GurufocusKevinSunОценок пока нет

- Safety Measures During Oil Exploration & Drilling: DR Naveen RajДокумент22 страницыSafety Measures During Oil Exploration & Drilling: DR Naveen RajRATHOD AKASHОценок пока нет

- 1476783934daily Market Commentary - October 18 2016Документ2 страницы1476783934daily Market Commentary - October 18 2016Md Saiful Islam KhanОценок пока нет

- Perrigo Company: © Zacks Company Report As ofДокумент1 страницаPerrigo Company: © Zacks Company Report As ofjomanousОценок пока нет

- CPQ sp21 Set 1Документ73 страницыCPQ sp21 Set 1Priyanka SodhaniОценок пока нет

- BES 3qtr2023Документ24 страницыBES 3qtr2023Durdle DurdlerОценок пока нет

- Investment Proposal Tyre IndustryДокумент3 страницыInvestment Proposal Tyre IndustrySandeep KumarОценок пока нет

- Time TechnoplastДокумент8 страницTime Technoplastagrawal.minОценок пока нет

- Annex 21 - COST COMPARISON SHEETДокумент1 страницаAnnex 21 - COST COMPARISON SHEETLarimel ValdezОценок пока нет

- Auto Components Infographic November 2021Документ1 страницаAuto Components Infographic November 2021ROOHI SHARMA 19111037Оценок пока нет

- Relatório de ContasДокумент12 страницRelatório de ContasirlandoОценок пока нет

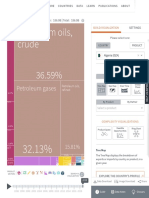

- U.S. Energy Consumption by Source and Sector, 2019Документ2 страницыU.S. Energy Consumption by Source and Sector, 2019rcmasterbОценок пока нет

- Daily Guide To The Markets (5-13)Документ19 страницDaily Guide To The Markets (5-13)Mike KaplanОценок пока нет

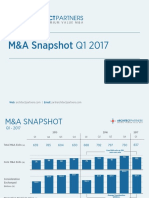

- AP M&A Q1 2017 SnapshotДокумент18 страницAP M&A Q1 2017 SnapshotArchitectPartnersОценок пока нет

- Raymond LTD: Key Financial IndicatorsДокумент4 страницыRaymond LTD: Key Financial IndicatorsteliumarОценок пока нет

- Il Processo EPCДокумент103 страницыIl Processo EPCAtha APОценок пока нет

- Defined Risk Strategy (DRS) : "Prophesy As Much As You Like, But Always Hedge." - Oliver Wendell Holmes, 1861Документ4 страницыDefined Risk Strategy (DRS) : "Prophesy As Much As You Like, But Always Hedge." - Oliver Wendell Holmes, 1861Hasita VinodОценок пока нет

- Etf Wealth RCH 0416fДокумент2 страницыEtf Wealth RCH 0416fMatt EbrahimiОценок пока нет

- Applied Optoelectronics Inc REPORT 11.29.23Документ3 страницыApplied Optoelectronics Inc REPORT 11.29.23physicallen1791Оценок пока нет

- HDFC Life 12M FY2022 Investor PresentationДокумент78 страницHDFC Life 12M FY2022 Investor Presentationamitmech.4987Оценок пока нет

- Ador Welding LTD.: Key Financial IndicatorsДокумент4 страницыAdor Welding LTD.: Key Financial IndicatorsRudra GoudОценок пока нет

- Alpha Low-Vy 30Документ2 страницыAlpha Low-Vy 30Ankit JoshiОценок пока нет

- CCN 1014402Документ11 страницCCN 1014402richard87bОценок пока нет

- VietnamДокумент5 страницVietnamYassine EL KouriОценок пока нет

- Stock Performance of Obour Land For Food Industries (OLFI - EGY)Документ1 страницаStock Performance of Obour Land For Food Industries (OLFI - EGY)body.helal2001Оценок пока нет

- Bangladesh S Intended Nationally Determined Contributions 'Документ2 страницыBangladesh S Intended Nationally Determined Contributions 'Tahmina SultanaОценок пока нет

- AxisCap - Sumitomo Chemicals - 24 Nov 2020Документ26 страницAxisCap - Sumitomo Chemicals - 24 Nov 2020Sriram RanganathanОценок пока нет

- Area de Influencia-Anta (3827)Документ1 страницаArea de Influencia-Anta (3827)Huereqq LambayeqОценок пока нет

- Httpsatlas Cid Harvard Eduexplorecountry 66&product Undefined&year 2019&productclass HS&target Product&partner Undefined&stДокумент1 страницаHttpsatlas Cid Harvard Eduexplorecountry 66&product Undefined&year 2019&productclass HS&target Product&partner Undefined&stJermiah AguilarОценок пока нет

- PubCo ValuationДокумент12 страницPubCo ValuationAlan Zhu100% (1)

- Never Seen BeforeДокумент336 страницNever Seen BeforepercheОценок пока нет

- How To Analyze CaseДокумент8 страницHow To Analyze CaseArpita GuptaОценок пока нет

- S1 P1 Saurabh Scenario of ECBC in IndiaДокумент20 страницS1 P1 Saurabh Scenario of ECBC in IndiaSUNIDHI VERMAОценок пока нет

- Lonsum Highlights 9M22Документ1 страницаLonsum Highlights 9M22Devina Ratna DewiОценок пока нет

- Urban Žitko : Primerjalnik Rezultatov TestaДокумент1 страницаUrban Žitko : Primerjalnik Rezultatov TestaeckartОценок пока нет

- DAY Investor: Thursday, May 24, 2018Документ167 страницDAY Investor: Thursday, May 24, 2018RaduОценок пока нет

- Renault - Fiscal Year 2005Документ97 страницRenault - Fiscal Year 2005Mateusz BłaszczakОценок пока нет

- Risk Management Plan2Документ1 страницаRisk Management Plan2Felicia GhicaОценок пока нет

- Axis Detailed Report - May 2020 PDFДокумент118 страницAxis Detailed Report - May 2020 PDFRohan AdlakhaОценок пока нет

- WAR (ACS) Aeropack - PB08-evaluated - 2023.0104Документ3 страницыWAR (ACS) Aeropack - PB08-evaluated - 2023.0104JuvyОценок пока нет

- Mi1602ao yДокумент27 страницMi1602ao yVОценок пока нет

- LPKR 290011-110211Документ10 страницLPKR 290011-110211Aditya WidiyadiОценок пока нет

- Ind Nifty 200Документ2 страницыInd Nifty 200Sagar V SoniОценок пока нет

- Ind Nifty 200Документ2 страницыInd Nifty 200Aman JainОценок пока нет

- AP Biology Chi - Square Practice ProblemsДокумент1 страницаAP Biology Chi - Square Practice ProblemsPaulus VillanuevaОценок пока нет

- October AccomplishmentДокумент17 страницOctober AccomplishmentReyma GalingganaОценок пока нет

- Ind Nifty 200Документ2 страницыInd Nifty 200badasserytechОценок пока нет

- Engineering Safety: Going Lower - Reducing Risk, Enhancing ProjectsДокумент58 страницEngineering Safety: Going Lower - Reducing Risk, Enhancing ProjectsHedi Ben MohamedОценок пока нет

- Evaluating Financial Performance: Irwin/Mcgraw-HillДокумент22 страницыEvaluating Financial Performance: Irwin/Mcgraw-HillJaved PatelОценок пока нет

- KF) V/F Ljt/0F S) GB - : CF J @) &%÷& Jflif (S LdiffДокумент16 страницKF) V/F Ljt/0F S) GB - : CF J @) &%÷& Jflif (S LdiffNikeshManandharОценок пока нет

- SPECTRUM - SRO-1812 Ficha TécnicaДокумент1 страницаSPECTRUM - SRO-1812 Ficha TécnicaJorge ArturoОценок пока нет

- Product and Market: Segment-Wise Market ShareДокумент11 страницProduct and Market: Segment-Wise Market ShareAmal PushpОценок пока нет

- Q122 HP Inc. Earnings SummaryДокумент2 страницыQ122 HP Inc. Earnings Summaryashokdb2kОценок пока нет

- Factsheet Nifty50 ShariahДокумент2 страницыFactsheet Nifty50 ShariahMonu GamerОценок пока нет

- LazardGlobalListedInfrastructureFund FactSheet 2024-02Документ3 страницыLazardGlobalListedInfrastructureFund FactSheet 2024-02yinjara.buyerОценок пока нет

- ACMA Presentation 2021 FYДокумент15 страницACMA Presentation 2021 FYAryan TanwarОценок пока нет

- Quant MF - Disclosure of Risk ParametersДокумент2 страницыQuant MF - Disclosure of Risk ParametersaarushkadamОценок пока нет

- Design Thinking for Business Growth: How to Design and Scale Business Models and Business EcosystemsОт EverandDesign Thinking for Business Growth: How to Design and Scale Business Models and Business EcosystemsОценок пока нет

- Profitability Analysis of Tata Motors: AbhinavДокумент8 страницProfitability Analysis of Tata Motors: AbhinavAman KhanОценок пока нет

- Second Term Exam-2070 Particulars Debit (RS.) Credit (RS.)Документ8 страницSecond Term Exam-2070 Particulars Debit (RS.) Credit (RS.)ragedskullОценок пока нет

- Chapter 14 Financial StatementsДокумент12 страницChapter 14 Financial StatementsAngelica Joy ManaoisОценок пока нет

- Battle For The Lead Analysis of Coca-Cola and PepsДокумент8 страницBattle For The Lead Analysis of Coca-Cola and Pepsnguyenkhanhlinh.p1.ddtОценок пока нет

- S4capital Annual Report and Accounts 2021Документ172 страницыS4capital Annual Report and Accounts 2021ignaciaОценок пока нет

- Intermediate Accountig AkuntansiДокумент46 страницIntermediate Accountig AkuntansiRika LerianiОценок пока нет

- VCF - Day 4 ReportДокумент10 страницVCF - Day 4 ReportSoon seng ChuОценок пока нет

- CitizensBank 2020Документ94 страницыCitizensBank 2020FarihaHaqueLikhi 1060Оценок пока нет

- BRIEF HISTORICAL VIEW OF MODERN TAX ADMINISTRATION IN ALBANIA, 1994-2011 - AL-TaxДокумент3 страницыBRIEF HISTORICAL VIEW OF MODERN TAX ADMINISTRATION IN ALBANIA, 1994-2011 - AL-TaxEduart GjokutajОценок пока нет

- Supply Chain Management (Gr1) (OM04) Amul: Post Graduate Diploma in Management (TERM 4 Batch 2019-21)Документ21 страницаSupply Chain Management (Gr1) (OM04) Amul: Post Graduate Diploma in Management (TERM 4 Batch 2019-21)Rahul KumarОценок пока нет

- Financial Analysis For Sapphire Fibres LimitedДокумент6 страницFinancial Analysis For Sapphire Fibres LimitedRashmeen NaeemОценок пока нет

- ABL Annual Report 2004 PDFДокумент55 страницABL Annual Report 2004 PDFAhmad ZafaryabОценок пока нет

- Practices For Lesson 2: Order To Cash OverviewДокумент12 страницPractices For Lesson 2: Order To Cash OverviewNatarajulu VadimgatiОценок пока нет

- Project Profile On Disinfectant FluidsДокумент8 страницProject Profile On Disinfectant FluidssanjaydeОценок пока нет

- Final Report of Engro PDF FreeДокумент58 страницFinal Report of Engro PDF FreeMadni Enterprises DGKОценок пока нет

- Test Bank SCFДокумент114 страницTest Bank SCFAnnabelle RafolsОценок пока нет

- Anhui Conch Cement Company LTD Annual Report 2013Документ274 страницыAnhui Conch Cement Company LTD Annual Report 2013hnmdungdqОценок пока нет

- W1-Unit 5 Assignment Brief V1.2 1 2Документ11 страницW1-Unit 5 Assignment Brief V1.2 1 2himanshusharma9435Оценок пока нет

- Accounting Principles: Nguyen La Soa SAAДокумент65 страницAccounting Principles: Nguyen La Soa SAAMai AnhОценок пока нет

- Chapter 4 and 5 ReviewerДокумент4 страницыChapter 4 and 5 ReviewerMildea Gabuya RabangОценок пока нет

- Ceka - Icmd 2009 (B01)Документ4 страницыCeka - Icmd 2009 (B01)IshidaUryuuОценок пока нет

- Top 20 Financial KPIs Every CFO Dashboard Should HaveДокумент5 страницTop 20 Financial KPIs Every CFO Dashboard Should HavekPrasad80% (1)

- 2-Impact of IFRS Adoption On The Financial Performance of NigerianДокумент12 страниц2-Impact of IFRS Adoption On The Financial Performance of NigerianGadaa TDhОценок пока нет

- Tailoring Performance Management Systems: A Sports Merchandiser's CaseДокумент16 страницTailoring Performance Management Systems: A Sports Merchandiser's CaseEarthAngel OrganicsОценок пока нет

- Internship Report On Financial PerformanДокумент55 страницInternship Report On Financial PerformanNiloyОценок пока нет

- BFIN 1quareter ExamДокумент29 страницBFIN 1quareter ExamMark Louie Suarez100% (1)

- Fdi by MC Donald Presented by Tarun JhalaniДокумент28 страницFdi by MC Donald Presented by Tarun Jhalanikhandelwalmba0% (1)

- Liabilities: Ransfer of An Economic ResourcesДокумент19 страницLiabilities: Ransfer of An Economic ResourcesSisiw WasyerОценок пока нет

- Accounting Policies in Bharat ElectronicsДокумент4 страницыAccounting Policies in Bharat ElectronicsNafis SiddiquiОценок пока нет

- Audits of Voluntary Health and Welfare Organizations (1967) Indu PDFДокумент74 страницыAudits of Voluntary Health and Welfare Organizations (1967) Indu PDFFate LauОценок пока нет