Вам также может понравиться

- Capital BudgetingДокумент60 страницCapital BudgetingMujeeb U RahmanОценок пока нет

- Capital Budgeting Techniques Capital Budgeting TechniquesДокумент31 страницаCapital Budgeting Techniques Capital Budgeting Techniquesharis123pОценок пока нет

- pp13Документ65 страницpp13Tejashree NirgudeОценок пока нет

- Capital Budgeting Techniques Capital Budgeting TechniquesДокумент60 страницCapital Budgeting Techniques Capital Budgeting Techniquesahmad_ranjhaОценок пока нет

- Capital Budgeting Tehnique-KHДокумент42 страницыCapital Budgeting Tehnique-KHyana mulyonoОценок пока нет

- Capital Budgeting Techniques Pp13Документ65 страницCapital Budgeting Techniques Pp13ErosОценок пока нет

- Project Budgeting TechniqueДокумент15 страницProject Budgeting Techniquesshahriar2001Оценок пока нет

- WBSLive Lecture 9 Slides Pres VevoxДокумент21 страницаWBSLive Lecture 9 Slides Pres VevoxabhirejanilОценок пока нет

- Capital Budgeting Techniques Pp13Документ65 страницCapital Budgeting Techniques Pp13anishaОценок пока нет

- Project Concept and FormulationДокумент56 страницProject Concept and FormulationWP 2-1-PR Katubedda-CESLОценок пока нет

- Capital BudgetingДокумент67 страницCapital BudgetingAhmad VohraОценок пока нет

- Capital BudgetingДокумент48 страницCapital BudgetingVIVEK JAISWAL100% (1)

- Mportance OF Apital UdgetingДокумент16 страницMportance OF Apital UdgetingtsayuriОценок пока нет

- Capital Budget Report-FINALДокумент35 страницCapital Budget Report-FINALMikaОценок пока нет

- Material No. 3: Capital Budgeting: Laguna State Polytechnic University-Los Baños Laguna (LSPU-LBC)Документ7 страницMaterial No. 3: Capital Budgeting: Laguna State Polytechnic University-Los Baños Laguna (LSPU-LBC)Kristine Joy NolloraОценок пока нет

- Capital Budgeting - FINAL (A)Документ59 страницCapital Budgeting - FINAL (A)nikhilnegi1704Оценок пока нет

- Capital Budgeting Techniques Capital Budgeting TechniquesДокумент58 страницCapital Budgeting Techniques Capital Budgeting TechniquesMuhammad ZeeshanОценок пока нет

- Capital Budgeting Techniques Capital Budgeting TechniquesДокумент59 страницCapital Budgeting Techniques Capital Budgeting TechniquesMuhammad FarooqОценок пока нет

- Capital Budgeting 2Документ49 страницCapital Budgeting 2Naman LadhaОценок пока нет

- Chapter 13Документ65 страницChapter 13Abdullah khanОценок пока нет

- Capital BudgetingДокумент61 страницаCapital BudgetingEyael ShimleasОценок пока нет

- Captal Budgeting (1) PPT Type NotesДокумент50 страницCaptal Budgeting (1) PPT Type NotesPrabalОценок пока нет

- Chapter Four Part Two: Importance of Capital BudgetingДокумент12 страницChapter Four Part Two: Importance of Capital Budgetingnahu a dinОценок пока нет

- Capital Budgeting RK 2019Документ53 страницыCapital Budgeting RK 2019Ishaan TandonОценок пока нет

- Capital Budgeting TechniquesДокумент60 страницCapital Budgeting Techniquesaxl11Оценок пока нет

- Capital-Budgeting-Techniques 1. Gamestop Corporation Has Three Projects Under Consideration. The Cash Flows For Each of Them Are Shown in The Following Table. The Firm Has A 16% Cost of CapitalДокумент6 страницCapital-Budgeting-Techniques 1. Gamestop Corporation Has Three Projects Under Consideration. The Cash Flows For Each of Them Are Shown in The Following Table. The Firm Has A 16% Cost of CapitalEvangeline RemedilloОценок пока нет

- Assessment 1 October 2021 POCFДокумент2 страницыAssessment 1 October 2021 POCFAakanksha ChughОценок пока нет

- Chapter-4 (Capital Budgeting)Документ26 страницChapter-4 (Capital Budgeting)Milad AkbariОценок пока нет

- Answers To Warm-Up Exercises: AnswerДокумент21 страницаAnswers To Warm-Up Exercises: AnswerMeyzla Ativa HuslikОценок пока нет

- © 2010 Financial Management Prepared By: Amyn WahidДокумент66 страниц© 2010 Financial Management Prepared By: Amyn Wahidfatimasal33m100% (1)

- Ch-13-Capital Budgeting Technique AmendedДокумент77 страницCh-13-Capital Budgeting Technique AmendedMirza hamdhaniОценок пока нет

- 202005021259597527vijayshankarpandey Capital Budgeting TechniquesДокумент49 страниц202005021259597527vijayshankarpandey Capital Budgeting TechniquesanishaОценок пока нет

- Capital Budgeting MCQs - Accountancy KnowledgeДокумент7 страницCapital Budgeting MCQs - Accountancy KnowledgeTahir Rehman0% (1)

- 04 Investment Appraisal MNGДокумент5 страниц04 Investment Appraisal MNGabinet getnet mamoОценок пока нет

- Capital BudgetingДокумент60 страницCapital BudgetingAce DesabilleОценок пока нет

- Cash FLowДокумент60 страницCash FLowSakshi SharmaОценок пока нет

- Capital Budgeting Techniques Capital Budgeting TechniquesДокумент50 страницCapital Budgeting Techniques Capital Budgeting TechniquesMoqadus SeharОценок пока нет

- ch13Документ60 страницch13Ains M. BantuasОценок пока нет

- Capital Budgeting: BA 217: Financial ManagementДокумент46 страницCapital Budgeting: BA 217: Financial ManagementyanaОценок пока нет

- Capital Budgeting Techniques Capital Budgeting TechniquesДокумент65 страницCapital Budgeting Techniques Capital Budgeting Techniquesarslan shahОценок пока нет

- Chapter 10 PostДокумент41 страницаChapter 10 PostTONITOОценок пока нет

- Capital BudgetingДокумент31 страницаCapital BudgetinggulafridiОценок пока нет

- Capital Budgeting Decisions NotesДокумент15 страницCapital Budgeting Decisions NotesEbbyОценок пока нет

- Capital BudgetingДокумент75 страницCapital Budgetingsubroshakar gamerОценок пока нет

- Chap 13Документ53 страницыChap 13axl11Оценок пока нет

- Financial Analysis of Final)Документ28 страницFinancial Analysis of Final)Mangesh GulhaneОценок пока нет

- Project ManagementxxДокумент34 страницыProject ManagementxxAli Akand AsifОценок пока нет

- Capital Budgeting Techniques + IRRДокумент20 страницCapital Budgeting Techniques + IRRHumzaОценок пока нет

- MS11 - Capital BudgetingДокумент8 страницMS11 - Capital BudgetingElsie GenovaОценок пока нет

- FMTII Session 4&5 Capital BudgetingДокумент56 страницFMTII Session 4&5 Capital Budgetingbhushankankariya5Оценок пока нет

- CH 9Документ59 страницCH 9bbbhaha12Оценок пока нет

- L-4 Project AppraisalДокумент9 страницL-4 Project Appraisalattitudefirstpankaj8625Оценок пока нет

- 3 Capital Budgeting TechniquesДокумент42 страницы3 Capital Budgeting TechniquesfnhshafiraОценок пока нет

- Project Appraisal-1 PDFДокумент23 страницыProject Appraisal-1 PDFFareha RiazОценок пока нет

- Project Appraisal 1Документ23 страницыProject Appraisal 1Fareha RiazОценок пока нет

- Qtouto 1492176702 1Документ4 страницыQtouto 1492176702 1Christy AngkouwОценок пока нет

- C29400.doc 320185331Документ16 страницC29400.doc 320185331Anushtha singhОценок пока нет

- v1 2015cfa强化一级班 企业理财 权益衍生 其他1Документ250 страницv1 2015cfa强化一级班 企业理财 权益衍生 其他1Mario XieОценок пока нет

- Capital Asset Investment: Strategy, Tactics and ToolsОт EverandCapital Asset Investment: Strategy, Tactics and ToolsРейтинг: 1 из 5 звезд1/5 (1)

- TOGAF® 10 Level 2 Enterprise Arch Part 2 Exam Wonder Guide Volume 2: TOGAF 10 Level 2 Scenario Strategies, #2От EverandTOGAF® 10 Level 2 Enterprise Arch Part 2 Exam Wonder Guide Volume 2: TOGAF 10 Level 2 Scenario Strategies, #2Рейтинг: 5 из 5 звезд5/5 (1)

- FCF CH 12 - Historical Return PDFДокумент6 страницFCF CH 12 - Historical Return PDFEvangelystha Lumban TobingОценок пока нет

- Chapter 8 PRN PDFДокумент17 страницChapter 8 PRN PDFEvangelystha Lumban TobingОценок пока нет

- 275-Article Text-1179-1-10-20170727Документ17 страниц275-Article Text-1179-1-10-20170727Evangelystha Lumban TobingОценок пока нет

- BhukmДокумент23 страницыBhukmEvangelystha Lumban TobingОценок пока нет

- ch04 Account ManagementДокумент23 страницыch04 Account ManagementEvangelystha Lumban TobingОценок пока нет

- Customer Value Sebagai Sumberdaya: Informasi Bagi PerusahaanДокумент10 страницCustomer Value Sebagai Sumberdaya: Informasi Bagi PerusahaanEvangelystha Lumban TobingОценок пока нет

- Chap009 - Analysis BS IsДокумент56 страницChap009 - Analysis BS IsEvangelystha Lumban TobingОценок пока нет

- Sales CH 8Документ23 страницыSales CH 8Evangelystha Lumban TobingОценок пока нет

- Managing International Business (MIB) : Culture Environments Facing Business Cross-National Cooperation and AgreementsДокумент36 страницManaging International Business (MIB) : Culture Environments Facing Business Cross-National Cooperation and AgreementsEvangelystha Lumban TobingОценок пока нет

- SEI INVESTMENTS CO 10-K (Annual Reports) 2009-02-25Документ113 страницSEI INVESTMENTS CO 10-K (Annual Reports) 2009-02-25http://secwatch.comОценок пока нет

- Study Material of Corporate Reporting Practice and ASДокумент57 страницStudy Material of Corporate Reporting Practice and ASnidhi goel0% (1)

- Notes of WCS (2017-2018) PDFДокумент33 страницыNotes of WCS (2017-2018) PDFNiruОценок пока нет

- Accounting Cheat SheetДокумент7 страницAccounting Cheat Sheetopty100% (15)

- 1.3 MUTUAL FUNDS - Valdez, KatrinaДокумент16 страниц1.3 MUTUAL FUNDS - Valdez, KatrinaRyna Miguel MasaОценок пока нет

- Hedge Fund FactsheetДокумент2 страницыHedge Fund Factsheetyahoooo1234Оценок пока нет

- F 13 Financial Accounting CpaДокумент9 страницF 13 Financial Accounting CpaMarcellin MarcaОценок пока нет

- Fixed Asset Register Tracking Excel Format Template DownloadДокумент4 страницыFixed Asset Register Tracking Excel Format Template DownloadRuan Joubert (Owen)Оценок пока нет

- SoftwareДокумент38 страницSoftwareRaven R. LabiosОценок пока нет

- Analysis Solutions Acc 411Документ13 страницAnalysis Solutions Acc 411dre_emОценок пока нет

- Bacc 402 Financial Stat 1Документ9 страницBacc 402 Financial Stat 1ItdarareОценок пока нет

- Module 6 - Operating SegmentsДокумент3 страницыModule 6 - Operating SegmentsChristine Joyce BascoОценок пока нет

- CH 07Документ19 страницCH 07Ahmed Al EkamОценок пока нет

- Chapter 10 INTERNATIONAL BUSINESS AND TRADEДокумент5 страницChapter 10 INTERNATIONAL BUSINESS AND TRADEgian reyesОценок пока нет

- BUSE Company Law Notes 1Документ111 страницBUSE Company Law Notes 1Phebieon Mukwenha100% (1)

- 10-11-04 SEC V BAC (1:09-cv-06829) at The US District Court, Southern District of New York - Records Downloaded From The Fair Fund Distribution Administrator's Website-SДокумент78 страниц10-11-04 SEC V BAC (1:09-cv-06829) at The US District Court, Southern District of New York - Records Downloaded From The Fair Fund Distribution Administrator's Website-SHuman Rights Alert - NGO (RA)Оценок пока нет

- Chapter 2 - Statement of Comprehensive IncomeДокумент12 страницChapter 2 - Statement of Comprehensive IncomeVictor TucoОценок пока нет

- CIMA F3 Notes - Financial Strategy - Chapters 1 and 2 PDFДокумент29 страницCIMA F3 Notes - Financial Strategy - Chapters 1 and 2 PDFLuzuko Terence Nelani100% (8)

- 5 Rules of Debit and CreditДокумент4 страницы5 Rules of Debit and CreditKen DiОценок пока нет

- Topic1 Introductionto Financial Market and SecuritiesДокумент19 страницTopic1 Introductionto Financial Market and SecuritiesMirza VejzagicОценок пока нет

- Investing Tips: Lesson 18: Student Activity Sheet 1Документ3 страницыInvesting Tips: Lesson 18: Student Activity Sheet 1GONZALO JIMENEZ MORALESОценок пока нет

- 2020 1 Accounting in Organisations and Society Assignment-3Документ7 страниц2020 1 Accounting in Organisations and Society Assignment-3Abs PangaderОценок пока нет

- On January 1 2013 Stamford Reacquires 8 000 of The OutstandingДокумент1 страницаOn January 1 2013 Stamford Reacquires 8 000 of The OutstandingMiroslav GegoskiОценок пока нет

- Accounting and Finance Set 2Документ6 страницAccounting and Finance Set 2Folegwe FolegweОценок пока нет

- MBE - BFAR (1st Sem, 2021-2022)Документ11 страницMBE - BFAR (1st Sem, 2021-2022)Bai Dianne BagundangОценок пока нет

- BFL LAS Product Note INTERNAL 27.04.17Документ3 страницыBFL LAS Product Note INTERNAL 27.04.17Prachi PatwariОценок пока нет

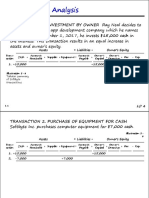

- Transaction Analysis: Transaction 1. Investment by Owner Ray Neal Decides ToДокумент31 страницаTransaction Analysis: Transaction 1. Investment by Owner Ray Neal Decides ToSophia LocreОценок пока нет

- Definition of WACCДокумент6 страницDefinition of WACCMMОценок пока нет

- Accounting Equation & Accounting Classification: Prepared By: Nurul Hassanah Binti HamzahДокумент12 страницAccounting Equation & Accounting Classification: Prepared By: Nurul Hassanah Binti HamzahNur Amira NadiaОценок пока нет

- Portfolio ManagementДокумент31 страницаPortfolio Managementharjot singhОценок пока нет