Вам также может понравиться

- IMF Study Guide SMUN2030Документ15 страницIMF Study Guide SMUN2030kimaОценок пока нет

- Futuristic United Nations General Assembly Background GuideДокумент33 страницыFuturistic United Nations General Assembly Background GuideazharОценок пока нет

- Ecofin BG PDFДокумент12 страницEcofin BG PDFBarathy KolappanОценок пока нет

- Beyond the Developmental State: Industrial Policy into the Twenty-first CenturyОт EverandBeyond the Developmental State: Industrial Policy into the Twenty-first CenturyОценок пока нет

- Ecosoc Guide 2Документ6 страницEcosoc Guide 2Pepe RamirezОценок пока нет

- Midterm Contemporary Global GovernanceДокумент14 страницMidterm Contemporary Global GovernanceBINIBINING KOLEHIYALAОценок пока нет

- Contemporary Global GovernanceДокумент7 страницContemporary Global GovernanceNiorun Aruna QuinnОценок пока нет

- BGG EcoosocДокумент16 страницBGG EcoosocPAOLA EDITH RODRIGUEZ TARINОценок пока нет

- UNHRCДокумент17 страницUNHRCAshhab KhanОценок пока нет

- Structure of GlobalizationДокумент23 страницыStructure of GlobalizationLea HaberОценок пока нет

- Sismun Ecofin Study GuideДокумент14 страницSismun Ecofin Study GuideShivank MenonОценок пока нет

- 2023 IMUNC ProspectusДокумент10 страниц2023 IMUNC Prospectusjanice sugiОценок пока нет

- Jmcmun'20 InviteДокумент12 страницJmcmun'20 InviteAnubha GuptaОценок пока нет

- Background Guide - UNHRC - UMUN'22Документ13 страницBackground Guide - UNHRC - UMUN'22Karan JainОценок пока нет

- Contemporary Global GovernanceДокумент12 страницContemporary Global Governancejonalyn alsadoОценок пока нет

- Hon M Kirby AC CMG "International Symposium On The Public Voice and The Development of International Cryptography Policy"Документ11 страницHon M Kirby AC CMG "International Symposium On The Public Voice and The Development of International Cryptography Policy"Journal of Law, Information & ScienceОценок пока нет

- Economic & Social Council - Background GuideДокумент17 страницEconomic & Social Council - Background GuideAkshat Jain EfiОценок пока нет

- A United Nations Renaissance: What the UN is, and what it could beОт EverandA United Nations Renaissance: What the UN is, and what it could beОценок пока нет

- The Contemporary World ReviewerДокумент14 страницThe Contemporary World ReviewerArabella Consulta BrugadaОценок пока нет

- Combating Cyber ThreatОт EverandCombating Cyber ThreatP K SinghОценок пока нет

- C2d Contemporary Global GovernanceДокумент7 страницC2d Contemporary Global GovernanceBeautiful LifeОценок пока нет

- UNHCR Background Guide Rotaract MUN Change The World New YorkДокумент10 страницUNHCR Background Guide Rotaract MUN Change The World New YorkAdrian Dan PopОценок пока нет

- Slspmun 24 BrochureДокумент12 страницSlspmun 24 Brochurerani.ishwar1986Оценок пока нет

- Licensed larceny: Infrastructure, financial extraction and the global SouthОт EverandLicensed larceny: Infrastructure, financial extraction and the global SouthРейтинг: 4.5 из 5 звезд4.5/5 (2)

- The Amounts and The Effects of Money LaunderingДокумент187 страницThe Amounts and The Effects of Money LaunderingPetros ArvanitisОценок пока нет

- Ecosoc Brochure enДокумент2 страницыEcosoc Brochure enAnkit AnandОценок пока нет

- A Voice For Global Citizens. A UN World Citizens InitiativeДокумент80 страницA Voice For Global Citizens. A UN World Citizens InitiativeRavana KaifОценок пока нет

- A4. Geo3-Global Interstate SystemДокумент16 страницA4. Geo3-Global Interstate SystemMENONG, SHARA AMORОценок пока нет

- Structures of Globalization: Module DescriptionДокумент8 страницStructures of Globalization: Module DescriptionyowОценок пока нет

- Diplomacy and International Relations - Sample Questions and AnswersДокумент4 страницыDiplomacy and International Relations - Sample Questions and AnswersLumina Hazellyn100% (1)

- Administrative HandbookДокумент11 страницAdministrative Handbookapi-246792700Оценок пока нет

- Lesson 4 Global Interstate System PDFДокумент15 страницLesson 4 Global Interstate System PDFJervyn Guianan33% (3)

- UNGA Background GuideДокумент20 страницUNGA Background GuideFascinating FactОценок пока нет

- Sponsor HandbookДокумент377 страницSponsor Handbookapi-238639222Оценок пока нет

- Principality of Monaco: Combined Delegation of TheДокумент2 страницыPrincipality of Monaco: Combined Delegation of TheHELEN SHARPEОценок пока нет

- CBITMUN'24 UNGA-SOCHUM Background GuideДокумент25 страницCBITMUN'24 UNGA-SOCHUM Background Guideaditihaasini13Оценок пока нет

- Human Rights in The Global Economy - Colloquium Report 2010Документ28 страницHuman Rights in The Global Economy - Colloquium Report 2010International Council on Human Rights PolicyОценок пока нет

- ECOSOCДокумент24 страницыECOSOCAyushmaan SharmaОценок пока нет

- Political Science Project 1Документ12 страницPolitical Science Project 1Aadhitya100% (2)

- Chimni 2004 PDFДокумент37 страницChimni 2004 PDF王储Оценок пока нет

- Edited Biscmun 2017 Conference HandbookДокумент26 страницEdited Biscmun 2017 Conference Handbookapi-302308551Оценок пока нет

- Mun Guide FinalДокумент35 страницMun Guide FinalAnusha Mahtani100% (2)

- Contemporary Module 2 PDFДокумент15 страницContemporary Module 2 PDFCharleen RomeroОценок пока нет

- Unga-Plenary Study GuideДокумент14 страницUnga-Plenary Study Guidejyotiarko1122Оценок пока нет

- ContemporaryДокумент10 страницContemporaryDan Jezreel EsguerraОценок пока нет

- Kenya Affidavit Website VersionДокумент25 страницKenya Affidavit Website Versionmosadsd.saОценок пока нет

- NeCon BrochureДокумент27 страницNeCon BrochureAditya MОценок пока нет

- UNIT I: Human Rights & UN Module 3: Economic and Social Council (ECOSOC)Документ12 страницUNIT I: Human Rights & UN Module 3: Economic and Social Council (ECOSOC)Zeeshan AhmadОценок пока нет

- G8 CountriesДокумент29 страницG8 CountriesDaranОценок пока нет

- The Globalizers: The IMF, the World Bank, and Their BorrowersОт EverandThe Globalizers: The IMF, the World Bank, and Their BorrowersРейтинг: 4 из 5 звезд4/5 (2)

- The Ideal Within: A Discourse and Hegemony Theoretical Analysis of the International Anticorruption DiscourseОт EverandThe Ideal Within: A Discourse and Hegemony Theoretical Analysis of the International Anticorruption DiscourseОценок пока нет

- Redesigning the World Trade Organization for the Twenty-first CenturyОт EverandRedesigning the World Trade Organization for the Twenty-first CenturyОценок пока нет

- OIC and Its RelevanceДокумент6 страницOIC and Its RelevanceQasim Javaid BokhariОценок пока нет

- OIC EssayДокумент6 страницOIC EssayQasim Javaid BokhariОценок пока нет

- Cfmun Position Paper: NAME: Juanita Galvis Vélez. COMMISSION: Security Council (SC) COUNTRY: KenyaДокумент5 страницCfmun Position Paper: NAME: Juanita Galvis Vélez. COMMISSION: Security Council (SC) COUNTRY: KenyaFr4nc0288Оценок пока нет

- IDCMUN 1.0 Delegate InvitationДокумент10 страницIDCMUN 1.0 Delegate InvitationSameer VishwakarmaОценок пока нет

- A Critical History of Poverty Finance: Colonial Roots and Neoliberal FailuresОт EverandA Critical History of Poverty Finance: Colonial Roots and Neoliberal FailuresОценок пока нет

- Counter-Terrorism, Policy Laundering' and The FATF: Legalising Surveillance, Regulating Civil SocietyДокумент68 страницCounter-Terrorism, Policy Laundering' and The FATF: Legalising Surveillance, Regulating Civil SocietyIndian Social Action Forum - INSAFОценок пока нет

- Globalization and PoliticsДокумент10 страницGlobalization and PoliticsMuzaffar Abbas SipraОценок пока нет

- Balikbayan Box Companies Accredited by DTI in 2016 - NewsДокумент15 страницBalikbayan Box Companies Accredited by DTI in 2016 - NewsEdward OropezaОценок пока нет

- ITIL MALC Case Study 1 v1.1 PDFДокумент7 страницITIL MALC Case Study 1 v1.1 PDFGrzegorz Urbanowicz100% (2)

- Semester: B. Com - V Semester Name of The Subject: Financial Market & Institutions Unit-1Документ61 страницаSemester: B. Com - V Semester Name of The Subject: Financial Market & Institutions Unit-1Sparsh JainОценок пока нет

- Membership Application FormДокумент1 страницаMembership Application FormProutist Universal MaltaОценок пока нет

- 2nd Mate OOW For Ratings STC UKДокумент5 страниц2nd Mate OOW For Ratings STC UKFabian MascarenhasОценок пока нет

- Insurance Broking BusinessДокумент56 страницInsurance Broking Businesshardikpawar100% (4)

- PB 2019-035 Noodregeling Banco Del Orinoco ENG BDO 20190906Документ1 страницаPB 2019-035 Noodregeling Banco Del Orinoco ENG BDO 20190906Knipselkrant CuracaoОценок пока нет

- Mortgages 2019Документ60 страницMortgages 2019Ivana JayОценок пока нет

- AsdadasДокумент13 страницAsdadasSwindlerОценок пока нет

- CA Short Form Deed of TrustДокумент3 страницыCA Short Form Deed of TrustAxisvipОценок пока нет

- ShipRocket ProposalДокумент7 страницShipRocket ProposalShashi Bhushan SinghОценок пока нет

- Easypaisa Money Transfer To Any Mobile NumberДокумент2 страницыEasypaisa Money Transfer To Any Mobile NumberBryan WalkerОценок пока нет

- Nmims Final Report123 PDFДокумент46 страницNmims Final Report123 PDFHimanshu KhandelwalОценок пока нет

- Accounting NotesДокумент23 страницыAccounting NotesboiroyОценок пока нет

- SF 8.10A Audit Certificate For The Month of - (1st Month), 2020Документ1 страницаSF 8.10A Audit Certificate For The Month of - (1st Month), 2020praveenitplОценок пока нет

- Barings CaseДокумент3 страницыBarings CaseAnonymous LC5kFdtcОценок пока нет

- TRAIN Law BriefingДокумент30 страницTRAIN Law BriefingJoselito PabatangОценок пока нет

- MULTIPLE CHOICE. Choose The One Alternative That Best Completes The Statement or Answers The QuestionДокумент3 страницыMULTIPLE CHOICE. Choose The One Alternative That Best Completes The Statement or Answers The QuestionMohammad Abu LailОценок пока нет

- OidhvohsДокумент10 страницOidhvohsDeepak ShastriОценок пока нет

- A111actuarial Mathematics #1 - Single Premium Life InsuranceДокумент13 страницA111actuarial Mathematics #1 - Single Premium Life Insuranceolim275Оценок пока нет

- Comparative Financial Statement Analysis of The Big Three Banks Operating in Finland 2015-2016Документ49 страницComparative Financial Statement Analysis of The Big Three Banks Operating in Finland 2015-2016Eugene Rugo AОценок пока нет

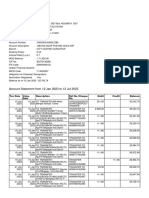

- Account Statement From 12 Jan 2023 To 12 Jul 2023Документ10 страницAccount Statement From 12 Jan 2023 To 12 Jul 2023SouravDeyОценок пока нет

- Aehbl Shae1705167Документ2 страницыAehbl Shae1705167idris_ali_7Оценок пока нет

- PDFДокумент3 страницыPDFArchanaNitinОценок пока нет

- Bank Reconciliation StatementДокумент40 страницBank Reconciliation StatementPrashant100% (1)

- MACN-A018 Universal Affidavit of Termination of All CORPORATEДокумент4 страницыMACN-A018 Universal Affidavit of Termination of All CORPORATEJabir Habib Bey33% (3)

- Annual Rep Eng 09Документ214 страницAnnual Rep Eng 09amitgoyal1972Оценок пока нет

- FIN036 AssignmentДокумент25 страницFIN036 AssignmentSandeep BholahОценок пока нет

- Working of Post Offices and Measures To Improve ItДокумент17 страницWorking of Post Offices and Measures To Improve ItsuchethatiaОценок пока нет

- A Cheque Is A DocumentДокумент15 страницA Cheque Is A Documentmi06bba030Оценок пока нет