Вам также может понравиться

- Paper 19Документ6 страницPaper 19mohanraj parthasarathyОценок пока нет

- Public Sector Accounting & Finance 2.5Документ20 страницPublic Sector Accounting & Finance 2.5financial reportingОценок пока нет

- Public Sector Accounting & Finance 2.5 PDFДокумент20 страницPublic Sector Accounting & Finance 2.5 PDFHaddy Gaye100% (2)

- Executive Summary: A. IntroductionДокумент7 страницExecutive Summary: A. IntroductionJoy AcostaОценок пока нет

- Public Sector Exam Report Breaks Down WeaknessesДокумент27 страницPublic Sector Exam Report Breaks Down WeaknessesGen AbulkhairОценок пока нет

- © The Institute of Chartered Accountants of IndiaДокумент13 страниц© The Institute of Chartered Accountants of IndiaRohit SadhukhanОценок пока нет

- Empire Brandy FSДокумент4 страницыEmpire Brandy FSStephanie DoceОценок пока нет

- Cma. Cia. 3Документ37 страницCma. Cia. 3Usha KarkiОценок пока нет

- Independent Audit Report CIA 1Документ5 страницIndependent Audit Report CIA 1Kalyani JayakrishnanОценок пока нет

- FABM2-Chapter4 NДокумент10 страницFABM2-Chapter4 NArchie CampomanesОценок пока нет

- Balance Sheet CompanyДокумент16 страницBalance Sheet CompanyNidhi ShahОценок пока нет

- Indian Accounting Standard 101Документ19 страницIndian Accounting Standard 101RITZ BROWNОценок пока нет

- 69587bos55533-P1.pdf 2Документ46 страниц69587bos55533-P1.pdf 2pittujb2002Оценок пока нет

- CPA 13 - Public Financial ManagementДокумент15 страницCPA 13 - Public Financial ManagementManit MehtaОценок пока нет

- Topic 2 - Af09101 - Financial StatementsДокумент42 страницыTopic 2 - Af09101 - Financial Statementsarusha afroОценок пока нет

- BSc Business Finance Exam QuestionsДокумент9 страницBSc Business Finance Exam QuestionsRukshani RefaiОценок пока нет

- Construction Industry Authority of The Philippines Executive Summary 2021Документ4 страницыConstruction Industry Authority of The Philippines Executive Summary 2021Jeypee De GeeОценок пока нет

- Financial RatiosДокумент13 страницFinancial RatiosAaron Coutinho0% (1)

- PSA Mock Questionnov 2019 PDFДокумент31 страницаPSA Mock Questionnov 2019 PDFmaterials downloadОценок пока нет

- 03-OVP2022 Executive SummaryДокумент6 страниц03-OVP2022 Executive SummaryarchaosdesigngroupОценок пока нет

- Basic Accounting Lesson 7: Worksheet and Financial StatementsДокумент33 страницыBasic Accounting Lesson 7: Worksheet and Financial StatementsGutierrez Ronalyn Y.Оценок пока нет

- Civil Aeronautics Board Executive Summary 2020Документ7 страницCivil Aeronautics Board Executive Summary 2020Carlo OlivarОценок пока нет

- Caf 8 Aud Autumn 2021Документ5 страницCaf 8 Aud Autumn 2021Huma BashirОценок пока нет

- Preparation of A Cash Flow Statement FromДокумент22 страницыPreparation of A Cash Flow Statement FromUddish BagriОценок пока нет

- 1st Semester Dec 2021 PDFДокумент8 страниц1st Semester Dec 2021 PDFroshanОценок пока нет

- PNC INFRATECH - ASM ProjectДокумент11 страницPNC INFRATECH - ASM ProjectAbhijeet kohatОценок пока нет

- Cashflowstatement 150402074118 Conversion Gate01Документ30 страницCashflowstatement 150402074118 Conversion Gate01vini2710Оценок пока нет

- VietstockFinance BBC Bao Cao Tai Chinh LCTT 20220626 222838Документ9 страницVietstockFinance BBC Bao Cao Tai Chinh LCTT 20220626 222838hlm84359Оценок пока нет

- Essay Part 2Документ58 страницEssay Part 2Silvia alfonsОценок пока нет

- Resume 1Документ15 страницResume 1MariaОценок пока нет

- MaterialityДокумент9 страницMaterialityBenedict KaruruОценок пока нет

- TIA FINANCIAL ACCOUNTING EXAMДокумент9 страницTIA FINANCIAL ACCOUNTING EXAMSebastian MlingwaОценок пока нет

- Financial Reporting Tutorial QSN Solutions 2021 JC JaftoДокумент31 страницаFinancial Reporting Tutorial QSN Solutions 2021 JC JaftoInnocent GwangwaraОценок пока нет

- Corporate Law CIA - 1 - AДокумент11 страницCorporate Law CIA - 1 - AShefali TailorОценок пока нет

- ACCT 451 Advanced Accounting Trial ExamДокумент4 страницыACCT 451 Advanced Accounting Trial ExamPrince-SimonJohnMwanzaОценок пока нет

- ICAN MAY 2018 DIET FINANCIAL REPORTING SKILLS LEVEL EXAMДокумент155 страницICAN MAY 2018 DIET FINANCIAL REPORTING SKILLS LEVEL EXAMOgunmola femiОценок пока нет

- 1-F-A Auditing - (E)Документ4 страницы1-F-A Auditing - (E)Hamid MahmoodОценок пока нет

- © The Institute of Chartered Accountants of India: TH STДокумент46 страниц© The Institute of Chartered Accountants of India: TH STheikОценок пока нет

- Afa A2Документ9 страницAfa A2Segarambal MasilamoneyОценок пока нет

- Exam 3Документ22 страницыExam 3Darynn F. Linggon100% (2)

- Module 2 - Financial StatementsДокумент6 страницModule 2 - Financial Statementskemifawole13Оценок пока нет

- May 2019 Professional Examinations Public Sector Accounting & Finance (Paper 2.5) Chief Examiner'S Report, Questions and Marking SchemeДокумент24 страницыMay 2019 Professional Examinations Public Sector Accounting & Finance (Paper 2.5) Chief Examiner'S Report, Questions and Marking SchemeMahama JinaporОценок пока нет

- Jalib Industruies QДокумент2 страницыJalib Industruies Qmichealcorleone1923Оценок пока нет

- Assignment For Finanacial Management IДокумент12 страницAssignment For Finanacial Management IHailu DemekeОценок пока нет

- Accountingtools: Balance Sheet DefinitionДокумент5 страницAccountingtools: Balance Sheet DefinitionHosty PuffОценок пока нет

- Finance, Accounting and Risk Management: Code: AMIL38Документ9 страницFinance, Accounting and Risk Management: Code: AMIL38ilayanambiОценок пока нет

- Final Grace CorpДокумент14 страницFinal Grace CorpKarl Chua100% (1)

- Week 2 Tutorial SolutionsДокумент23 страницыWeek 2 Tutorial SolutionsalexandraОценок пока нет

- ExerciseДокумент13 страницExerciseemanmamdouh596Оценок пока нет

- Statement of Changes in Financial PositionДокумент19 страницStatement of Changes in Financial Positionankitkhanijo100% (1)

- Presidential Commission For The Urban Poor Executive Summary 2021Документ7 страницPresidential Commission For The Urban Poor Executive Summary 2021Vincent ArnadoОценок пока нет

- IMP 2225 Advance Accounts Prelims QUESTION PAPERДокумент8 страницIMP 2225 Advance Accounts Prelims QUESTION PAPERArnik AgarwalОценок пока нет

- Ca Inter Advanced Accounts Imp Questions BookletДокумент112 страницCa Inter Advanced Accounts Imp Questions BookletUdaykiran BheemaganiОценок пока нет

- Cap II Group I RTP Dec2023Документ84 страницыCap II Group I RTP Dec2023pratyushmudbhari340Оценок пока нет

- CARO 2020 Question BankДокумент12 страницCARO 2020 Question BankVINUS DHANKHARОценок пока нет

- Far410 Chapter 3 Fin StatementsДокумент17 страницFar410 Chapter 3 Fin Statementsmr.nazir.shahidanОценок пока нет

- Capital University of Science and Technology: Honor StatementДокумент7 страницCapital University of Science and Technology: Honor StatementPak KhОценок пока нет

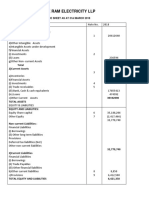

- Shree Ram Electricity LLP: 1) Non-Current AssetsДокумент5 страницShree Ram Electricity LLP: 1) Non-Current AssetsSaba MullaОценок пока нет

- Ican Pilot Pe 2Документ183 страницыIcan Pilot Pe 2sylv00975% (4)

- pp07-Chapter7EditedДокумент70 страницpp07-Chapter7EditedTolulola Olusegun LawalОценок пока нет

- FASB Ends Pooling of Interests in Accounting For Mergers and Acquisitions at Riker DanzigДокумент2 страницыFASB Ends Pooling of Interests in Accounting For Mergers and Acquisitions at Riker DanzigTolulola Olusegun LawalОценок пока нет

- Elementis plc2010 PDFДокумент94 страницыElementis plc2010 PDFTolulola Olusegun LawalОценок пока нет

- Elementis plc2010 PDFДокумент94 страницыElementis plc2010 PDFTolulola Olusegun LawalОценок пока нет

- Chapter 01 Practice QuizДокумент3 страницыChapter 01 Practice QuizSalemОценок пока нет

- Eli Lilly & CoДокумент14 страницEli Lilly & Corohitmahnot1989100% (3)

- Income Tax Guide UgandaДокумент13 страницIncome Tax Guide UgandaMoses LubangakeneОценок пока нет

- United States Court of Appeals: For The First CircuitДокумент24 страницыUnited States Court of Appeals: For The First CircuitScribd Government DocsОценок пока нет

- Capex Vs Opex Template 00Документ6 страницCapex Vs Opex Template 00viola fabiantoОценок пока нет

- Strategic Management of Amazon's DiversificationДокумент13 страницStrategic Management of Amazon's Diversificationrajesshpatel50% (2)

- WEST BENGAL UNIVERSITY OF TECHNOLOGY Summer Proj AyanДокумент38 страницWEST BENGAL UNIVERSITY OF TECHNOLOGY Summer Proj AyanMukesh Kumar SinghОценок пока нет

- Contingencies and Events After Balance Sheet DateДокумент64 страницыContingencies and Events After Balance Sheet DateRujan BajracharyaОценок пока нет

- Chapter 18 International Capital BudgetingДокумент26 страницChapter 18 International Capital BudgetingBharat NayyarОценок пока нет

- Prudent Private Wealth Company ProfileДокумент5 страницPrudent Private Wealth Company ProfilepratikОценок пока нет

- Brown-Forman Corporation Business Transformation StudyДокумент2 страницыBrown-Forman Corporation Business Transformation StudyAvinash MalladhiОценок пока нет

- L02 - Mundell Fleming ModelДокумент39 страницL02 - Mundell Fleming ModelanufacebookОценок пока нет

- Midterm Macro 2Документ22 страницыMidterm Macro 2chang vicОценок пока нет

- FTIL Annual Report 2009Документ180 страницFTIL Annual Report 2009Alwyn FurtadoОценок пока нет

- Week 1 - Lecture Prinsip Perakaunan Principles of Accounting (Bt11003)Документ30 страницWeek 1 - Lecture Prinsip Perakaunan Principles of Accounting (Bt11003)sitinazirah_gadiskecikОценок пока нет

- Hollywood Rules: Kellogg School of Management Cases January 2017Документ10 страницHollywood Rules: Kellogg School of Management Cases January 2017Faraz AnsariОценок пока нет

- The Meaning of Strategic MarketingДокумент14 страницThe Meaning of Strategic MarketingAderonke OgunsakinОценок пока нет

- Companies (Prospectus and Allotment of Securities) Rules, 2014.Документ31 страницаCompanies (Prospectus and Allotment of Securities) Rules, 2014.Khushi SharmaОценок пока нет

- Form AR01 Annual ReturnДокумент14 страницForm AR01 Annual Returnaglondon100Оценок пока нет

- Business ValuationДокумент5 страницBusiness ValuationAppraiser PhilippinesОценок пока нет

- Mona AbdelMonsef - Cafe Kenya Case AnalysisДокумент8 страницMona AbdelMonsef - Cafe Kenya Case AnalysisMona AbdelMonsefОценок пока нет

- Credit Risk ManagementДокумент78 страницCredit Risk ManagementSanjida100% (1)

- Oecd Frascati ManualДокумент402 страницыOecd Frascati Manualmarquez182Оценок пока нет

- Types of Banks in Nepal: Yogesh BaniyaДокумент7 страницTypes of Banks in Nepal: Yogesh Baniyaanon_665535262Оценок пока нет

- Case Study Liquidation ValueДокумент3 страницыCase Study Liquidation ValueTheodor ToncaОценок пока нет

- Bogleheads Forum Discussion on Buying Precious Metals from APMEXДокумент18 страницBogleheads Forum Discussion on Buying Precious Metals from APMEXambasyapare1Оценок пока нет

- Price Discovery and Causality in The Indian Derivatives MarketДокумент4 страницыPrice Discovery and Causality in The Indian Derivatives MarketmeetwithsanjayОценок пока нет

- Private Retirement Plans in The PhilippinesДокумент55 страницPrivate Retirement Plans in The Philippineschane15100% (2)

- Trading DayДокумент15 страницTrading DaydmidОценок пока нет