Вам также может понравиться

- Case 1 Case 2 Case 3Документ8 страницCase 1 Case 2 Case 3Biyan Ardana100% (1)

- Cases CH 3Документ2 страницыCases CH 3ejaaejoОценок пока нет

- Akuntansi Tugas 4Документ2 страницыAkuntansi Tugas 4Biyan ArdanaОценок пока нет

- Question and Answer - 11Документ30 страницQuestion and Answer - 11acc-expertОценок пока нет

- Task AccountingДокумент13 страницTask AccountingYordan LawijayaОценок пока нет

- 9165c46e55b3c94881023e5273552304_934c2b7d81261f58f1850f8a973dcd60Документ4 страницы9165c46e55b3c94881023e5273552304_934c2b7d81261f58f1850f8a973dcd60Christy Angkouw0% (1)

- Be16 P16 2aДокумент7 страницBe16 P16 2aLisa Hammerle ClarkОценок пока нет

- Statistika Ekonomi Bisnis Anderson 11th Edition, Chapter 1-6Документ56 страницStatistika Ekonomi Bisnis Anderson 11th Edition, Chapter 1-6yunitaknОценок пока нет

- Supplemental Homework ProblemsДокумент64 страницыSupplemental Homework ProblemsRolando E. CaserОценок пока нет

- 7001 Assignment #3Документ9 страниц7001 Assignment #3南玖Оценок пока нет

- Calculate ROI, EVA, Residual Income for Company DivisionsДокумент3 страницыCalculate ROI, EVA, Residual Income for Company DivisionsDhiva Rianitha ManurungОценок пока нет

- Firda Arfianti - LC53 - Consolidated Workpaper, Wholly Owned SubsidiaryДокумент3 страницыFirda Arfianti - LC53 - Consolidated Workpaper, Wholly Owned SubsidiaryFirdaОценок пока нет

- Income statement and schedule of cost of goods manufacturedДокумент3 страницыIncome statement and schedule of cost of goods manufacturedMarjorie PalmaОценок пока нет

- Kelompok Ii Tugas Kelompok Manajemen Keuangan Lanjutan No. P9-4Документ9 страницKelompok Ii Tugas Kelompok Manajemen Keuangan Lanjutan No. P9-4RoyОценок пока нет

- Acc3 5Документ4 страницыAcc3 5dinda ardiyaniОценок пока нет

- MUH - SYUKUR - A031191077) AKUNTANSI MANAJEMEN-PROBLEM 11-18 Return On Investment (ROI) and Residual IncomeДокумент3 страницыMUH - SYUKUR - A031191077) AKUNTANSI MANAJEMEN-PROBLEM 11-18 Return On Investment (ROI) and Residual IncomeRismayantiОценок пока нет

- A Case Study of D'Leon IncДокумент13 страницA Case Study of D'Leon IncTimОценок пока нет

- Excercise 19Документ7 страницExcercise 19raihan aqilОценок пока нет

- Income Tax DTL - DTAДокумент10 страницIncome Tax DTL - DTASagita RajagukgukОценок пока нет

- Maynard Company Balance Sheets"TITLE "TITLE Maynard Company June Income StatementДокумент2 страницыMaynard Company Balance Sheets"TITLE "TITLE Maynard Company June Income Statementriya lakhotiaОценок пока нет

- Transfer Pricng SolutionДокумент3 страницыTransfer Pricng SolutionchandraprakashОценок пока нет

- Chapter 12Документ7 страницChapter 12RBОценок пока нет

- Tugas AKM II Minggu 10 E24.2 Dan E24.3 - Clarissa Nastania (441354)Документ2 страницыTugas AKM II Minggu 10 E24.2 Dan E24.3 - Clarissa Nastania (441354)Clarissa NastaniaОценок пока нет

- Tugas Akuntansi Keuangan LanjutanДокумент8 страницTugas Akuntansi Keuangan LanjutanMin DaeguОценок пока нет

- (Case 12) GE Bets On The Internet of Things and Big Data AnalyticsДокумент9 страниц(Case 12) GE Bets On The Internet of Things and Big Data Analyticsberliana setyawatiОценок пока нет

- Intercompany transactions elimination for consolidated financial statementsДокумент13 страницIntercompany transactions elimination for consolidated financial statementsicadeliciafebОценок пока нет

- Tugas Chapter 14Документ7 страницTugas Chapter 14irga ayudiasОценок пока нет

- Week13 SolutionsДокумент14 страницWeek13 SolutionsRian RorresОценок пока нет

- To What Extent Was The Internet Revenue Contribution of Around 90 Per Cent Achieved More by Luck Than Judgement'?Документ8 страницTo What Extent Was The Internet Revenue Contribution of Around 90 Per Cent Achieved More by Luck Than Judgement'?Suraj BanОценок пока нет

- Cost Accounting Chapter 17Документ4 страницыCost Accounting Chapter 17Yordan Lawijaya100% (1)

- Calculus Company Makes Calculators For StudentsДокумент2 страницыCalculus Company Makes Calculators For StudentsElliot RichardОценок пока нет

- CH 11+16th+globalДокумент37 страницCH 11+16th+globalAmina SultangaliyevaОценок пока нет

- Profitability of Products and Relative ProfitabilityДокумент5 страницProfitability of Products and Relative Profitabilityshaun3187Оценок пока нет

- Accounting For Mana Control Ch5 ExampleДокумент3 страницыAccounting For Mana Control Ch5 Exampledmorey213Оценок пока нет

- Chapter 7 Problem 7.3 Nathali, Jeffrey, TasyaДокумент6 страницChapter 7 Problem 7.3 Nathali, Jeffrey, Tasyavtech netОценок пока нет

- Hydrochem PDFДокумент7 страницHydrochem PDFSaransh KejriwalОценок пока нет

- Case 7 - An Introduction To Debt Policy and ValueДокумент5 страницCase 7 - An Introduction To Debt Policy and ValueAnthony Kwo100% (2)

- The Controller of The Ijiri Company Wants You To Estimate A Cost Function From The Following Two Observations in A General Ledger Account Called MaintenanceДокумент3 страницыThe Controller of The Ijiri Company Wants You To Estimate A Cost Function From The Following Two Observations in A General Ledger Account Called MaintenanceElliot RichardОценок пока нет

- Pittman Company Is A Small But Growing Manufacturer of Telecommunications Equipment.Документ12 страницPittman Company Is A Small But Growing Manufacturer of Telecommunications Equipment.Kailash KumarОценок пока нет

- Case Study 2 Maria ChavezДокумент8 страницCase Study 2 Maria ChavezCheveem Grace Emnace100% (1)

- P11Документ7 страницP11Arif RahmanОценок пока нет

- Soln SSP S1Документ12 страницSoln SSP S1Marjorie PalmaОценок пока нет

- Kelompok 6 - Tugas Week 11 - Akuntansi Manajemen - LДокумент4 страницыKelompok 6 - Tugas Week 11 - Akuntansi Manajemen - LRictu SempakОценок пока нет

- Decision Tree Analysis: Merck & Co. Case StudyДокумент8 страницDecision Tree Analysis: Merck & Co. Case StudyFadhila Hanif100% (1)

- Soal AkmДокумент5 страницSoal AkmCarvin HarisОценок пока нет

- Jawaban BE15 - AKMДокумент3 страницыJawaban BE15 - AKMMazz BadruezОценок пока нет

- Tugas 5 - AKL 1Документ3 страницыTugas 5 - AKL 1Geroro D'PhoenixОценок пока нет

- Comprehensive Problems Solution Answer Key Mid TermДокумент5 страницComprehensive Problems Solution Answer Key Mid TermGabriel Aaron DionneОценок пока нет

- Contoh Soal - Ch15Документ52 страницыContoh Soal - Ch15Nurhanifah SoedarsОценок пока нет

- Go Green Lawn adjusting entriesДокумент2 страницыGo Green Lawn adjusting entriesMd. Rokon KhanОценок пока нет

- Exercise - Dilutive Securities - AdillaikhsaniДокумент4 страницыExercise - Dilutive Securities - Adillaikhsaniaidil fikri ikhsanОценок пока нет

- Advanced Accounting: Corporate Liquidations and ReorganizationsДокумент43 страницыAdvanced Accounting: Corporate Liquidations and ReorganizationsitaОценок пока нет

- The Central Valley Company Has Prepared Department Overhead Budgets For BudgetedДокумент4 страницыThe Central Valley Company Has Prepared Department Overhead Budgets For BudgetedElliot RichardОценок пока нет

- Cost Accounting Systems and Product Costing OverviewДокумент61 страницаCost Accounting Systems and Product Costing OverviewNicolas ErnestoОценок пока нет

- Tugas AklДокумент8 страницTugas AklFebryanthi SNОценок пока нет

- Wahyudi-Syaputra Assignment-2 Akl-IiДокумент4 страницыWahyudi-Syaputra Assignment-2 Akl-IiWahyudi SyaputraОценок пока нет

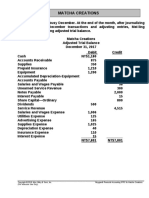

- MC4 Matcha Creations: (For Instructor Use Only)Документ2 страницыMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraОценок пока нет

- MC4 Matcha Creations: (For Instructor Use Only)Документ2 страницыMC4 Matcha Creations: (For Instructor Use Only)QUANG LE DO MINHОценок пока нет

- Wey Ifrs 2e CCCДокумент19 страницWey Ifrs 2e CCCAnonymous 1SUDEbgFОценок пока нет

- PA-HW Chap3 + 4Документ8 страницPA-HW Chap3 + 4Hà Anh ĐỗОценок пока нет

- Blue Ocean StrategyДокумент7 страницBlue Ocean StrategyMuhammad Helmi Faisal0% (2)

- Solution Manual Chapter 4 Intermediate Accounting - KIYOSIДокумент13 страницSolution Manual Chapter 4 Intermediate Accounting - KIYOSIIndra AminudinОценок пока нет

- (2018) MM5003-Marketing Management FinalДокумент16 страниц(2018) MM5003-Marketing Management FinalRivai Vai SОценок пока нет

- CH 01Документ50 страницCH 01IsuluapОценок пока нет

- Bulletin No 18 August 16 2019 - PassДокумент770 страницBulletin No 18 August 16 2019 - PassNithyashree T100% (1)

- CEILLI Trial Ques EnglishДокумент15 страницCEILLI Trial Ques EnglishUSCОценок пока нет

- Criminal Revision 11 of 2019Документ2 страницыCriminal Revision 11 of 2019wanyamaОценок пока нет

- Ad Intelligence BДокумент67 страницAd Intelligence BSyed IqbalОценок пока нет

- 10th Parliament BookДокумент86 страниц10th Parliament BookLilian JumaОценок пока нет

- Garcia v. Social Security CommissionДокумент3 страницыGarcia v. Social Security CommissionJD JasminОценок пока нет

- AE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBДокумент7 страницAE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBArly Kurt TorresОценок пока нет

- CorpF ReviseДокумент5 страницCorpF ReviseTrang DangОценок пока нет

- Euro MedДокумент3 страницыEuro MedAndrolf CaparasОценок пока нет

- Test 3 - Part 5Документ4 страницыTest 3 - Part 5hiếu võ100% (1)

- Heirs dispute over lands owned by their fatherДокумент23 страницыHeirs dispute over lands owned by their fatherVeraNataaОценок пока нет

- Zoleta Vs SandiganbayanДокумент9 страницZoleta Vs SandiganbayanMc Alaine Ligan100% (1)

- Module 3 Accounting Cycle Journal EntriesДокумент18 страницModule 3 Accounting Cycle Journal EntriesRoel CababaoОценок пока нет

- 17Mb221 Industrial Relations and Labour LawsДокумент2 страницы17Mb221 Industrial Relations and Labour LawsshubhamОценок пока нет

- Final Exam - 2013 BTC1110Документ3 страницыFinal Exam - 2013 BTC1110ThomasMann100% (1)

- Tutang Sinampay:: Jerzon Senador Probably Wants To Be Famous and Show The World How Naughty He Is by Hanging HisДокумент2 страницыTutang Sinampay:: Jerzon Senador Probably Wants To Be Famous and Show The World How Naughty He Is by Hanging HisClaire Anne BernardoОценок пока нет

- JMRC Vacancy Circular For DeputationДокумент20 страницJMRC Vacancy Circular For DeputationSumit AgrawalОценок пока нет

- Judy Carter - George Irani - Vamık D. Volkan - Regional and Ethnic Conflicts - Perspectives From The Front Lines, Coursesmart Etextbook-Routledge (2008)Документ564 страницыJudy Carter - George Irani - Vamık D. Volkan - Regional and Ethnic Conflicts - Perspectives From The Front Lines, Coursesmart Etextbook-Routledge (2008)abdurakhimovamaftuna672Оценок пока нет

- United States Bankruptcy Court Southern District of New YorkДокумент21 страницаUnited States Bankruptcy Court Southern District of New YorkChapter 11 DocketsОценок пока нет

- Cignal: Residential Service Application FormДокумент10 страницCignal: Residential Service Application FormJUDGE MARLON JAY MONEVAОценок пока нет

- BC t?ng tr??ng User Internet Banking có g?n TK TGTT- Xu?t chi ti?tДокумент12 страницBC t?ng tr??ng User Internet Banking có g?n TK TGTT- Xu?t chi ti?tMy TruongОценок пока нет

- V - 62 Caroni, Trinidad, Thursday 5th January, 2023-Price $1.00 N - 2Документ8 страницV - 62 Caroni, Trinidad, Thursday 5th January, 2023-Price $1.00 N - 2ERSKINE LONEYОценок пока нет

- U.S. vs. Macaspac, G.R. No. 3878, November 16, 1907-1Документ2 страницыU.S. vs. Macaspac, G.R. No. 3878, November 16, 1907-1Abby PerezОценок пока нет

- Salary Loan Application FormДокумент2 страницыSalary Loan Application FormRyan PangaluanОценок пока нет

- 4 2 Pure BendingДокумент13 страниц4 2 Pure BendingRubayet AlamОценок пока нет

- SAP ACH ConfigurationДокумент49 страницSAP ACH ConfigurationMohammadGhouse100% (4)

- VMware VSphere ICM 6.7 Lab ManualДокумент142 страницыVMware VSphere ICM 6.7 Lab Manualitnetman93% (29)

- NC LiabilitiesДокумент12 страницNC LiabilitiesErin LumogdangОценок пока нет

- A Chronology of Key Events of US HistoryДокумент5 страницA Chronology of Key Events of US Historyanon_930849151Оценок пока нет

- Diaz Vs AdiongДокумент2 страницыDiaz Vs AdiongCharise MacalinaoОценок пока нет

- Poker: A Beginners Guide To No Limit Texas Holdem and Understand Poker Strategies in Order to Win the Games of PokerОт EverandPoker: A Beginners Guide To No Limit Texas Holdem and Understand Poker Strategies in Order to Win the Games of PokerРейтинг: 5 из 5 звезд5/5 (49)

- The Best Gambling Addiction Cure on the Planet: How to Stop Gambling Addiction in 7 Days or LessОт EverandThe Best Gambling Addiction Cure on the Planet: How to Stop Gambling Addiction in 7 Days or LessРейтинг: 1 из 5 звезд1/5 (1)

- POKER MATH: Strategy and Tactics for Mastering Poker Mathematics and Improving Your Game (2022 Guide for Beginners)От EverandPOKER MATH: Strategy and Tactics for Mastering Poker Mathematics and Improving Your Game (2022 Guide for Beginners)Оценок пока нет

- Poker Satellite Strategy: How to qualify for the main events of high stakes live and online poker tournamentsОт EverandPoker Satellite Strategy: How to qualify for the main events of high stakes live and online poker tournamentsРейтинг: 4 из 5 звезд4/5 (7)

- Alchemy Elementals: A Tool for Planetary Healing: An Immersive Audio Experience for Spiritual AwakeningОт EverandAlchemy Elementals: A Tool for Planetary Healing: An Immersive Audio Experience for Spiritual AwakeningРейтинг: 5 из 5 звезд5/5 (3)

- Molly's Game: The True Story of the 26-Year-Old Woman Behind the Most Exclusive, High-Stakes Underground Poker Game in the WorldОт EverandMolly's Game: The True Story of the 26-Year-Old Woman Behind the Most Exclusive, High-Stakes Underground Poker Game in the WorldРейтинг: 3.5 из 5 звезд3.5/5 (129)

- Poker: How to Play Texas Hold'em Poker: A Beginner's Guide to Learn How to Play Poker, the Rules, Hands, Table, & ChipsОт EverandPoker: How to Play Texas Hold'em Poker: A Beginner's Guide to Learn How to Play Poker, the Rules, Hands, Table, & ChipsРейтинг: 4.5 из 5 звезд4.5/5 (6)

- Gambling Strategies Bundle: 3 in 1 Bundle, Gambling, Poker and Poker BooksОт EverandGambling Strategies Bundle: 3 in 1 Bundle, Gambling, Poker and Poker BooksОценок пока нет

- Phil Gordon's Little Green Book: Lessons and Teachings in No Limit Texas Hold'emОт EverandPhil Gordon's Little Green Book: Lessons and Teachings in No Limit Texas Hold'emРейтинг: 4 из 5 звезд4/5 (64)

- The Book of Card Games: The Complete Rules to the Classics, Family Favorites, and Forgotten GamesОт EverandThe Book of Card Games: The Complete Rules to the Classics, Family Favorites, and Forgotten GamesОценок пока нет

- Phil Gordon's Little Gold Book: Advanced Lessons for Mastering Poker 2.0От EverandPhil Gordon's Little Gold Book: Advanced Lessons for Mastering Poker 2.0Рейтинг: 3.5 из 5 звезд3.5/5 (6)

- How to Play Blackjack: Best Beginner's Guide to Learning the Basics of the Blackjack Game! Rules, Odds, Winner Strategies and a Whole Lot More...От EverandHow to Play Blackjack: Best Beginner's Guide to Learning the Basics of the Blackjack Game! Rules, Odds, Winner Strategies and a Whole Lot More...Оценок пока нет

- THE POKER MATH BIBLE : Achieve your goals developing a good poker mind. Micro and Small StakesОт EverandTHE POKER MATH BIBLE : Achieve your goals developing a good poker mind. Micro and Small StakesРейтинг: 3.5 из 5 звезд3.5/5 (14)

- Poker: The Best Techniques for Making You a Better PlayerОт EverandPoker: The Best Techniques for Making You a Better PlayerРейтинг: 4.5 из 5 звезд4.5/5 (73)

- Positively Fifth Street: Murderers, Cheetahs, and Binion's World Series of PokerОт EverandPositively Fifth Street: Murderers, Cheetahs, and Binion's World Series of PokerРейтинг: 3.5 из 5 звезд3.5/5 (188)

- Macdougall on Dice and Cards - Modern Rules, Odds, Hints and Warnings for Craps, Poker, Gin Rummy and BlackjackОт EverandMacdougall on Dice and Cards - Modern Rules, Odds, Hints and Warnings for Craps, Poker, Gin Rummy and BlackjackРейтинг: 2 из 5 звезд2/5 (1)

- How to Play Whist: A Beginner’s Guide to Learning the Rules, Bidding, & StrategiesОт EverandHow to Play Whist: A Beginner’s Guide to Learning the Rules, Bidding, & StrategiesРейтинг: 1 из 5 звезд1/5 (1)