Вам также может понравиться

- Nature of Power To Grant Tax ExemptionДокумент4 страницыNature of Power To Grant Tax ExemptionRoschelle MiguelОценок пока нет

- Exemption From TaxationДокумент5 страницExemption From TaxationJerricha YuОценок пока нет

- ABAN Tax Reviewer 1Документ67 страницABAN Tax Reviewer 1angelomoragaОценок пока нет

- Aban Tax 1 Reviewer PDFДокумент67 страницAban Tax 1 Reviewer PDFborgyambulo50% (2)

- Aban Tax 1 Reviewer PDFДокумент67 страницAban Tax 1 Reviewer PDFcardeguzmanОценок пока нет

- TAXATION PRINCIPLESДокумент67 страницTAXATION PRINCIPLESPaolo_00100% (3)

- Taxation PPT 1 ReviewerДокумент15 страницTaxation PPT 1 Revieweredsonjayyago07Оценок пока нет

- Exemption From Taxation: Tax ExemptionsДокумент31 страницаExemption From Taxation: Tax ExemptionsJulius SisraconОценок пока нет

- Beda Tax ReviewerДокумент68 страницBeda Tax ReviewerAnonymous 40zhRk1Оценок пока нет

- Tax ReviewerДокумент9 страницTax ReviewercsncsncsnОценок пока нет

- ShimДокумент4 страницыShimHanna AyonОценок пока нет

- Business Law and Taxation with Laws affecting MSMEs Week 02 Hand-OutДокумент18 страницBusiness Law and Taxation with Laws affecting MSMEs Week 02 Hand-OutJohn Mar GaminoОценок пока нет

- Part IV TaxДокумент4 страницыPart IV TaxMichael SanchezОценок пока нет

- General Principles of Taxation Taxation DefinedДокумент10 страницGeneral Principles of Taxation Taxation DefinedGraceОценок пока нет

- Local Media7305767987836246830Документ20 страницLocal Media7305767987836246830John RellonОценок пока нет

- O Taxation: The Power by Which The Sovereign Raises Revenue To Defray The Necessary Expenses of TheДокумент19 страницO Taxation: The Power by Which The Sovereign Raises Revenue To Defray The Necessary Expenses of Theniani marieОценок пока нет

- C2015 Tax 1 Midterms Reviewer (Loriega)Документ52 страницыC2015 Tax 1 Midterms Reviewer (Loriega)Sabrito100% (1)

- Taxation+I+General+Principles+Reviewer+for+Atty +monteroДокумент27 страницTaxation+I+General+Principles+Reviewer+for+Atty +monteroMars SacdalanОценок пока нет

- Tax Ation San Beda College of LAW - ALABANGДокумент52 страницыTax Ation San Beda College of LAW - ALABANGKenneth Abarca SisonОценок пока нет

- Tax 1Документ18 страницTax 1Billie Jan Louie JardinОценок пока нет

- Tax DoctrinesДокумент8 страницTax DoctrinesLouОценок пока нет

- General Principles: Theory and Basis of TaxationДокумент15 страницGeneral Principles: Theory and Basis of TaxationRicarr ChiongОценок пока нет

- Taxation NotesДокумент127 страницTaxation NotesAlarich CatayocОценок пока нет

- MANGILIMAN, Neil Francel Domingo (Sep 28)Документ8 страницMANGILIMAN, Neil Francel Domingo (Sep 28)Neil Francel D. MangilimanОценок пока нет

- Tax 1 ReviewerДокумент52 страницыTax 1 Reviewervanessa3333333Оценок пока нет

- Tax 1 ReviewerДокумент52 страницыTax 1 Reviewerms_k_a_y_e96% (25)

- Tax Ation San Beda College of LAW - ALABANGДокумент52 страницыTax Ation San Beda College of LAW - ALABANGYour Public ProfileОценок пока нет

- Tax Ation San Beda College of LAW - ALABANGДокумент52 страницыTax Ation San Beda College of LAW - ALABANGLaine Mongan100% (1)

- Reviewer TaxДокумент52 страницыReviewer TaxRogelio Saguinsin IIIОценок пока нет

- Taxation terms and powers of the stateДокумент2 страницыTaxation terms and powers of the stateRina Bico AdvinculaОценок пока нет

- Taxpayer's Ability To PayДокумент53 страницыTaxpayer's Ability To PayDave A ValcarcelОценок пока нет

- Taxation - Day 01Документ2 страницыTaxation - Day 01Joyce Sherly Ann LuceroОценок пока нет

- Chapter 1 NotesДокумент12 страницChapter 1 NotesGerald Nitz PonceОценок пока нет

- Chapter 1 General Principles of TaxationДокумент4 страницыChapter 1 General Principles of TaxationAngelie Elizaga SuarezОценок пока нет

- 2019 Tax LMTДокумент26 страниц2019 Tax LMTchristineОценок пока нет

- Exclusions To Gross IncomeДокумент8 страницExclusions To Gross IncomeNishikata MaseoОценок пока нет

- 2019 Taxation Law Last Minute Tips PDFДокумент11 страниц2019 Taxation Law Last Minute Tips PDFz v100% (1)

- General Principles A. Definition and Attributes of TaxationДокумент10 страницGeneral Principles A. Definition and Attributes of TaxationLei StudОценок пока нет

- Tax 1 ReviewerДокумент52 страницыTax 1 ReviewerDrean TubislloОценок пока нет

- A. Concept, Underlying Basis, and Purpose: Part I - General PrinciplesДокумент5 страницA. Concept, Underlying Basis, and Purpose: Part I - General PrinciplesBadong SilvaОценок пока нет

- Understanding Taxation Powers and PrinciplesДокумент35 страницUnderstanding Taxation Powers and PrinciplesEustaquio Jr., Felix C.Оценок пока нет

- Income Taxation Assignment Discussion 1Документ5 страницIncome Taxation Assignment Discussion 1Evelyn LabhananОценок пока нет

- Taxation ReviewerДокумент53 страницыTaxation ReviewerDave A ValcarcelОценок пока нет

- TAX LAW PRINCIPLESДокумент5 страницTAX LAW PRINCIPLESShiela Mae VillaruzОценок пока нет

- Tax LawДокумент53 страницыTax LawDave A ValcarcelОценок пока нет

- TAX 1 1st ExamДокумент28 страницTAX 1 1st ExamXandredg Sumpt LatogОценок пока нет

- Benefits-Protection Theory or Doctrine of Symbiotic RelationshipДокумент10 страницBenefits-Protection Theory or Doctrine of Symbiotic RelationshipSpidermanОценок пока нет

- Tax Reviewer MGCДокумент52 страницыTax Reviewer MGCCalderón Gutiérrez Marlón PówanОценок пока нет

- General Principles: Theory and Basis of TaxationДокумент15 страницGeneral Principles: Theory and Basis of TaxationRicarr ChiongОценок пока нет

- Tax Midterms ReviewerДокумент9 страницTax Midterms ReviewerSherelyn Flores VillanuevaОценок пока нет

- General Principles of TaxationДокумент36 страницGeneral Principles of Taxationnicole5anne5ddddddОценок пока нет

- Taxation Bar ReviewerДокумент14 страницTaxation Bar ReviewerevangarethОценок пока нет

- Income Taxation Whole Book Cheat SheetДокумент121 страницаIncome Taxation Whole Book Cheat SheetMaryane Angela100% (1)

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeОт Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeРейтинг: 1 из 5 звезд1/5 (1)

- The Economic Policies of Alexander Hamilton: Works & Speeches of the Founder of American Financial SystemОт EverandThe Economic Policies of Alexander Hamilton: Works & Speeches of the Founder of American Financial SystemОценок пока нет

- Petitioners Vs Vs Respondents: Third DivisionДокумент13 страницPetitioners Vs Vs Respondents: Third DivisionjackyОценок пока нет

- John Alvin L. Maningding vs. Zia Nicole C. BersaminaДокумент2 страницыJohn Alvin L. Maningding vs. Zia Nicole C. BersaminaThereseSunico0% (1)

- Grade 5 English Lesson on Inferring Meaning from Clipped WordsДокумент4 страницыGrade 5 English Lesson on Inferring Meaning from Clipped WordsGlenda Manalo Coching100% (3)

- ENGLISH V - Second Quarter S.Y. - Summative Test No.1 Table of Specification (Tos)Документ2 страницыENGLISH V - Second Quarter S.Y. - Summative Test No.1 Table of Specification (Tos)ThereseSunicoОценок пока нет

- Item Analysis Form: Montserrat Elementary SchoolДокумент2 страницыItem Analysis Form: Montserrat Elementary SchoolThereseSunicoОценок пока нет

- 04 - Sheker vs. Estate of Alice 0 - ShekerДокумент6 страниц04 - Sheker vs. Estate of Alice 0 - ShekerGia MordenoОценок пока нет

- Quiazon V BelenДокумент7 страницQuiazon V BelenJade CoritanaОценок пока нет

- Republic of The Philippines Vs Carlito KhoДокумент1 страницаRepublic of The Philippines Vs Carlito KhoThereseSunicoОценок пока нет

- Ty Kong Tin Vs RepublicДокумент1 страницаTy Kong Tin Vs RepublicCarmille MagnoОценок пока нет

- Petitioners Vs Vs Respondents: Third DivisionДокумент13 страницPetitioners Vs Vs Respondents: Third DivisionjackyОценок пока нет

- Appointing a Regular Administrator in an Estate CaseДокумент3 страницыAppointing a Regular Administrator in an Estate CaseThereseSunicoОценок пока нет

- Hilado Vs CAДокумент8 страницHilado Vs CAKevs De EgurrolaОценок пока нет

- Second Division: Plaintiff-Appellee vs. vs. Accused-Appellant The Solicitor General Ernesto B. FloresДокумент7 страницSecond Division: Plaintiff-Appellee vs. vs. Accused-Appellant The Solicitor General Ernesto B. FloresThereseSunicoОценок пока нет

- Complainant vs. vs. Respondent: First DivisionДокумент8 страницComplainant vs. vs. Respondent: First DivisionThereseSunicoОценок пока нет

- 127801-1994-People v. Simon y Sunga20181109-5466-1vfex5fДокумент28 страниц127801-1994-People v. Simon y Sunga20181109-5466-1vfex5fOldAccountof Ed ThereseОценок пока нет

- Dunlao v. CAДокумент7 страницDunlao v. CAPamela BalindanОценок пока нет

- Sandiganbayan Ruling Overturned Due to Lack of EvidenceДокумент8 страницSandiganbayan Ruling Overturned Due to Lack of EvidenceAlyssa Fatima Guinto SaliОценок пока нет

- The Story of The ICJДокумент3 страницыThe Story of The ICJThereseSunicoОценок пока нет

- Appointing a Regular Administrator in an Estate CaseДокумент3 страницыAppointing a Regular Administrator in an Estate CaseThereseSunicoОценок пока нет

- First Division: Virginia Calanoc, - Court of Appeals and The Philippine American Life Insurance Co.Документ5 страницFirst Division: Virginia Calanoc, - Court of Appeals and The Philippine American Life Insurance Co.Inez Monika Carreon PadaoОценок пока нет

- Ballatan v. CA DigestДокумент3 страницыBallatan v. CA DigestNeil ChuaОценок пока нет

- 04 - Sheker vs. Estate of Alice 0 - ShekerДокумент6 страниц04 - Sheker vs. Estate of Alice 0 - ShekerGia MordenoОценок пока нет

- Cir Vs SolidbankДокумент1 страницаCir Vs SolidbankThereseSunicoОценок пока нет

- 22 Biagtan v. Insular Life Assurance Co. LTDДокумент12 страниц22 Biagtan v. Insular Life Assurance Co. LTDKaryl Eric BardelasОценок пока нет

- The Story of The ICJДокумент3 страницыThe Story of The ICJThereseSunicoОценок пока нет

- The Story of The ICJДокумент3 страницыThe Story of The ICJThereseSunicoОценок пока нет

- Property JurisprudenceДокумент2 страницыProperty JurisprudenceThereseSunicoОценок пока нет

- Abrenica Vs AbrenicaДокумент1 страницаAbrenica Vs AbrenicaThereseSunicoОценок пока нет

- More FunДокумент1 страницаMore FunThereseSunicoОценок пока нет

- Insurance To DigestДокумент4 страницыInsurance To DigestThereseSunicoОценок пока нет

- Configure Down Payment Processing Using Document ConditionsДокумент7 страницConfigure Down Payment Processing Using Document ConditionsJayakumarVasudevanОценок пока нет

- Bajaj Capital LimitedДокумент1 страницаBajaj Capital LimitedSunny JohnsonОценок пока нет

- Roger Weliner v. CirДокумент1 страницаRoger Weliner v. CirChiiОценок пока нет

- Essay On CorporationsДокумент2 страницыEssay On Corporationsabdul razakОценок пока нет

- Ram BillДокумент1 страницаRam BillHarish Babu N KОценок пока нет

- TAX REMEDIESДокумент15 страницTAX REMEDIESChristopher Jan DotimasОценок пока нет

- Harpreet Raikhy: Invoic EДокумент1 страницаHarpreet Raikhy: Invoic Edalip kumarОценок пока нет

- Easypaisa-All Pricing and CommissioningДокумент17 страницEasypaisa-All Pricing and Commissioningqaisar_murtaza50% (4)

- Cost Breakup of Indian Ride Sharing CabsДокумент3 страницыCost Breakup of Indian Ride Sharing CabsNNS RohitОценок пока нет

- Taxation ProjectДокумент15 страницTaxation ProjectTanya SinglaОценок пока нет

- Payroll Summary For The Month of AugustДокумент46 страницPayroll Summary For The Month of AugustAida MohammedОценок пока нет

- Invoice M112308296312009275Документ1 страницаInvoice M112308296312009275Bruh YooinkОценок пока нет

- Salary Slip of MR Indra Nath Mishra March 20Документ1 страницаSalary Slip of MR Indra Nath Mishra March 20Indra MishraОценок пока нет

- BOG Notice BG GOV SEC 2022 01 Notice On Use of Ghana Card For All Financial Transactions 1Документ2 страницыBOG Notice BG GOV SEC 2022 01 Notice On Use of Ghana Card For All Financial Transactions 1Sammy Ben HammondОценок пока нет

- Kuenzle Vs CIRДокумент2 страницыKuenzle Vs CIRHaroldDeLeon100% (1)

- Cir Vs GoodyearДокумент19 страницCir Vs GoodyearMary Anne Guanzon VitugОценок пока нет

- 03 Asset Rental Invoice and Receipt Daily v1Документ10 страниц03 Asset Rental Invoice and Receipt Daily v1vijay sainiОценок пока нет

- Consumer Bill - SNGPLДокумент1 страницаConsumer Bill - SNGPLmuhammad hassanОценок пока нет

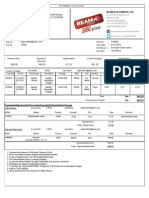

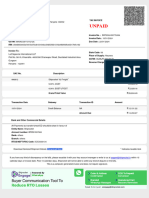

- Beam Telecom PVT LTD.: 8-2-610/A, Road No.10, Banjara Hills, Hyderabad-500034 Tel: +91-40-66272727Документ2 страницыBeam Telecom PVT LTD.: 8-2-610/A, Road No.10, Banjara Hills, Hyderabad-500034 Tel: +91-40-66272727Raghav Reddy NelloreОценок пока нет

- CIR Vs de La Salle UniversityДокумент20 страницCIR Vs de La Salle UniversityMoon BeamsОценок пока нет

- Combined Application Form SummaryДокумент14 страницCombined Application Form SummaryprastacharОценок пока нет

- Understanding MT 940 bank statement formatДокумент7 страницUnderstanding MT 940 bank statement formatpandu MОценок пока нет

- SRF2324 00772454Документ1 страницаSRF2324 00772454Aman PathakОценок пока нет

- Accounting Standard - 22Документ25 страницAccounting Standard - 22themeditator100% (1)

- 290 (80-Stn Smiley Ball)Документ2 страницы290 (80-Stn Smiley Ball)Sudhir GuptaОценок пока нет

- iCPA Practice Challenge Community Hi jbpedragosa23! 0 ePoints Log OutДокумент15 страницiCPA Practice Challenge Community Hi jbpedragosa23! 0 ePoints Log OutJericho PedragosaОценок пока нет

- Invoice JBL PDFДокумент1 страницаInvoice JBL PDFDhruv MishraОценок пока нет

- SOA-December 2022Документ4 страницыSOA-December 2022RYLYN JOY MAGSAYOОценок пока нет

- Tax On IndividualsДокумент9 страницTax On IndividualsshakiraОценок пока нет

- Quantity Description Category Weight (LB) Length (CM) Width (CM) Height (CM) Weight Vol. (LB)Документ1 страницаQuantity Description Category Weight (LB) Length (CM) Width (CM) Height (CM) Weight Vol. (LB)Ardiyansyah NugrahaОценок пока нет