Вам также может понравиться

- Chiok Vs PeopleДокумент2 страницыChiok Vs PeopleNICK CUNANANОценок пока нет

- CIR Vs Petron Corporation, G.R. No. 185568, March 21, 2012Документ4 страницыCIR Vs Petron Corporation, G.R. No. 185568, March 21, 2012NICK CUNANANОценок пока нет

- General Durable Springing Power of AttorneyДокумент4 страницыGeneral Durable Springing Power of AttorneyNICK CUNANANОценок пока нет

- Cir Vs Pal Full CasesДокумент17 страницCir Vs Pal Full CasesNICK CUNANANОценок пока нет

- Reviewer in Commercial Law Sundiang and Aquino 2013 PDFДокумент287 страницReviewer in Commercial Law Sundiang and Aquino 2013 PDFNICK CUNANAN57% (7)

- Meralco vs. Vera (1975) (Taxation Law)Документ1 страницаMeralco vs. Vera (1975) (Taxation Law)NICK CUNANANОценок пока нет

- Motion For Leave of Court FinalДокумент2 страницыMotion For Leave of Court FinalNICK CUNANAN100% (1)

- Case Digests - SalesДокумент2 страницыCase Digests - SalesNICK CUNANANОценок пока нет

- Stat Con WholeДокумент68 страницStat Con WholeNICK CUNANANОценок пока нет

- Formation of Corporations 1. Organizing The Corporation A. Promoters (Section 2 (R) of The Revised Securities Act (BP 178) )Документ1 страницаFormation of Corporations 1. Organizing The Corporation A. Promoters (Section 2 (R) of The Revised Securities Act (BP 178) )NICK CUNANANОценок пока нет

- P. JACINTO, Respondent, G.R. No. 154622, August 3, 2010: The Case - Land Bank of The Philippines, Petitioner, vs. RamonДокумент1 страницаP. JACINTO, Respondent, G.R. No. 154622, August 3, 2010: The Case - Land Bank of The Philippines, Petitioner, vs. RamonNICK CUNANANОценок пока нет

- Cases For Second MeetingДокумент50 страницCases For Second MeetingNICK CUNANANОценок пока нет

- Alegre Vs Collector of Customs Case Digest: FactsДокумент8 страницAlegre Vs Collector of Customs Case Digest: FactsNICK CUNANANОценок пока нет

- The CaseДокумент4 страницыThe CaseNICK CUNANANОценок пока нет

- Anti Fake News Act of 2018Документ6 страницAnti Fake News Act of 2018NICK CUNANANОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- MSAW U.S Tax GuideДокумент17 страницMSAW U.S Tax GuideHenri FontanaОценок пока нет

- New FORM 15H Applicable PY 2016-17Документ2 страницыNew FORM 15H Applicable PY 2016-17addsingh100% (1)

- Marcelo Steel Corporation vs. Collector of Internal RevenueДокумент2 страницыMarcelo Steel Corporation vs. Collector of Internal RevenuesakuraОценок пока нет

- Bahasa Inggris PPHДокумент9 страницBahasa Inggris PPHRiska UsmawardaniОценок пока нет

- Flipkart Labels 21 May 2023 01 21Документ5 страницFlipkart Labels 21 May 2023 01 21Nikhil BisuiОценок пока нет

- Clothing DNДокумент25 страницClothing DNUjjwal GuptaОценок пока нет

- TaxaoneДокумент20 страницTaxaonedianne ballonОценок пока нет

- Payslip 53801623060420151 19646Документ2 страницыPayslip 53801623060420151 19646adrianОценок пока нет

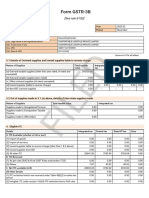

- Filed: Form GSTR-3BДокумент2 страницыFiled: Form GSTR-3Bkrishswat7912Оценок пока нет

- ICAI Nagapoor Branch - Relevent Case LawДокумент1 страницаICAI Nagapoor Branch - Relevent Case LawkrishnaОценок пока нет

- CHAPTER 11 Compensation IncomeДокумент15 страницCHAPTER 11 Compensation IncomeGIRLОценок пока нет

- JANANIДокумент1 страницаJANANIPETS HOMEОценок пока нет

- Nigeria Property Tax in Federal Capital TerritoryДокумент3 страницыNigeria Property Tax in Federal Capital TerritoryMark allenОценок пока нет

- References: Philippine Tax Code CREATE Law TRAIN Law Income Taxation, Banggawan RR8-2018Документ4 страницыReferences: Philippine Tax Code CREATE Law TRAIN Law Income Taxation, Banggawan RR8-2018Mark Lawrence YusiОценок пока нет

- Salary Slip May 2019Документ1 страницаSalary Slip May 2019Lalsiemlien HmarОценок пока нет

- Document PreviewДокумент1 страницаDocument PreviewMD. Omar AliОценок пока нет

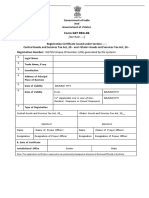

- Form GST REG-06: (See Rule - )Документ5 страницForm GST REG-06: (See Rule - )mohitОценок пока нет

- Class 27 - Depreciation and Income Taxes Contd..Документ33 страницыClass 27 - Depreciation and Income Taxes Contd..SwastikОценок пока нет

- 1 TAXF372-TaxinActionCASESTUDYandREQUIREDДокумент3 страницы1 TAXF372-TaxinActionCASESTUDYandREQUIREDrenette1010Оценок пока нет

- Vvneq1m5ymzryny1nuj2swrlwef0dz09 InvoiceДокумент2 страницыVvneq1m5ymzryny1nuj2swrlwef0dz09 InvoiceTYCS35 SIDDHESH PENDURKARОценок пока нет

- Passive Income and Capital GainsДокумент4 страницыPassive Income and Capital GainsTRISHAANN RUTAQUIOОценок пока нет

- Indian Income Tax Return Acknowledgement 2021-22: Assessment YearДокумент1 страницаIndian Income Tax Return Acknowledgement 2021-22: Assessment Yearvikas guptaОценок пока нет

- 3 BIR Ruling 103-96Документ2 страницы3 BIR Ruling 103-96Leia VeracruzОценок пока нет

- Answer Tutorial 5 Basis Period ChangesДокумент2 страницыAnswer Tutorial 5 Basis Period Changesathirah jamaludinОценок пока нет

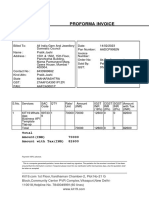

- Proforma-Invoice For WhatsApp Topup 14th Feb (1) .pdf-1Документ1 страницаProforma-Invoice For WhatsApp Topup 14th Feb (1) .pdf-1Harikrishan BhattОценок пока нет

- Residential Status and Tax Incidence: Dr. Niti SaxenaДокумент11 страницResidential Status and Tax Incidence: Dr. Niti SaxenaYusufОценок пока нет

- Total Amount Due: Tax InvoiceДокумент2 страницыTotal Amount Due: Tax InvoiceHikmat RahimovОценок пока нет

- Sanchar Communication P.I ScaleДокумент1 страницаSanchar Communication P.I Scaleiamdenny2024Оценок пока нет

- Credit Note: (Original For Recipient)Документ5 страницCredit Note: (Original For Recipient)Anchit SinglaОценок пока нет