Вам также может понравиться

- Robin Sharma Weekly Design SystemДокумент1 страницаRobin Sharma Weekly Design Systemgmsbhat100% (5)

- Chapter 16: Additional Question Practice: Three of TheДокумент18 страницChapter 16: Additional Question Practice: Three of TheHankhnilОценок пока нет

- 40 Strategic Questions To Ask To Evaluate Company DirectionДокумент7 страниц40 Strategic Questions To Ask To Evaluate Company DirectionShailendra Kelani100% (1)

- Company Profit and LossДокумент6 страницCompany Profit and LossFazal Rehman Mandokhail50% (2)

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeОт EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeОценок пока нет

- High-Impact Leadership Transitions PDFДокумент16 страницHigh-Impact Leadership Transitions PDFShailendra KelaniОценок пока нет

- PartnersДокумент13 страницPartnersvaloruroОценок пока нет

- Advanced Accounting QN 1,7 & 8Документ18 страницAdvanced Accounting QN 1,7 & 8MAGOMU DAN DAVIDОценок пока нет

- Uk3 2009 Dec AДокумент6 страницUk3 2009 Dec AApple ChinОценок пока нет

- T3uk 2009 Jun AДокумент8 страницT3uk 2009 Jun AApple ChinОценок пока нет

- Uk3 2010 Jun AДокумент7 страницUk3 2010 Jun AApple ChinОценок пока нет

- Uk3 2011 Jun AДокумент7 страницUk3 2011 Jun AApple ChinОценок пока нет

- Madaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Документ17 страницMadaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Maryjoy KilonzoОценок пока нет

- IPFMPSFR - Solutions 3 2023 Final - AAДокумент31 страницаIPFMPSFR - Solutions 3 2023 Final - AASabОценок пока нет

- Acounting Revision QuestionsДокумент10 страницAcounting Revision QuestionsJoseph KabiruОценок пока нет

- IA3 Chapter 14 Problem 31Документ3 страницыIA3 Chapter 14 Problem 31Bea TumulakОценок пока нет

- Intacc Cash Flow SolutionДокумент3 страницыIntacc Cash Flow SolutionMila MercadoОценок пока нет

- Accounting Assigment 01 IndividualДокумент2 страницыAccounting Assigment 01 IndividualOmari MaugaОценок пока нет

- Felix Fernando - C13-Q2Документ3 страницыFelix Fernando - C13-Q2Steve IdnОценок пока нет

- Jawaban Soal Latihan Ch.11Документ2 страницыJawaban Soal Latihan Ch.11Wira DinataОценок пока нет

- 4.3.2.3 Elaborate - Preparing Adjusting Entries From Unadjusted and Adjusted Trial BalanceДокумент3 страницы4.3.2.3 Elaborate - Preparing Adjusting Entries From Unadjusted and Adjusted Trial BalanceMa Fe Tabasa100% (2)

- Book1 xlsx1Документ4 страницыBook1 xlsx1Pian NasutionОценок пока нет

- 2009 S3 Ase2007Документ15 страниц2009 S3 Ase2007May CcmОценок пока нет

- Bba 122 Fai 11 AnswerДокумент12 страницBba 122 Fai 11 AnswerTomi Wayne Malenga100% (1)

- Tutorial 10 CH 5.3.6 SolutionДокумент5 страницTutorial 10 CH 5.3.6 SolutionenglishlessonsОценок пока нет

- QuizДокумент4 страницыQuizRinconada Benori ReynalynОценок пока нет

- T4 - (Assets) - Qs and SolutionДокумент22 страницыT4 - (Assets) - Qs and SolutionCalvin MaОценок пока нет

- Applied Auditing-Prelim FinalДокумент3 страницыApplied Auditing-Prelim FinalDominic E. BoticarioОценок пока нет

- Review2 Ch01 AДокумент1 страницаReview2 Ch01 AMayy ElleОценок пока нет

- Answer On AccountingДокумент6 страницAnswer On AccountingShahid MahmudОценок пока нет

- Worksheet 4Документ6 страницWorksheet 4Sneha KumariОценок пока нет

- MT2 Ch02Документ24 страницыMT2 Ch02api-3725162Оценок пока нет

- Asm ACCOUNTINGДокумент16 страницAsm ACCOUNTINGVũ Khánh HuyềnОценок пока нет

- Acctg. Equation Puring CompanyДокумент8 страницAcctg. Equation Puring CompanyAngelОценок пока нет

- Comprehensive Audit of Balance Sheet and Income Statement AccountsДокумент25 страницComprehensive Audit of Balance Sheet and Income Statement AccountsLuigi Enderez Balucan100% (1)

- Analysis of Financial StatementsДокумент27 страницAnalysis of Financial StatementsnickcrokОценок пока нет

- CH 2 Answers PDFДокумент5 страницCH 2 Answers PDFLian Blakely CousinОценок пока нет

- Mark Scheme (Results) January 2014Документ19 страницMark Scheme (Results) January 2014Fahrin NehaОценок пока нет

- Chapter 4 - Intermediate Accounting Volume 1Документ8 страницChapter 4 - Intermediate Accounting Volume 1Buenaventura, Elijah B.Оценок пока нет

- Solutionchapter 18 - Advacc Solutionchapter 18 - AdvaccДокумент68 страницSolutionchapter 18 - Advacc Solutionchapter 18 - AdvaccDvcLouisОценок пока нет

- Answers To Extra QuestionsДокумент8 страницAnswers To Extra QuestionsHashani KumarasingheОценок пока нет

- Genuime Company Required 1 Debit CreditДокумент15 страницGenuime Company Required 1 Debit CreditAnonnОценок пока нет

- Accountancy 12 - DS2 - Set - 1Документ15 страницAccountancy 12 - DS2 - Set - 1Deepa Saravana KumarОценок пока нет

- Sesi 11 & 12 SharedДокумент28 страницSesi 11 & 12 SharedDian Permata SariОценок пока нет

- Receivables Practice SolvingДокумент15 страницReceivables Practice SolvingddalgisznОценок пока нет

- Intermediate Accounting 1 Second Grading Examination Key AnswersДокумент12 страницIntermediate Accounting 1 Second Grading Examination Key AnswersAbegail Joy De GuzmanОценок пока нет

- Adobe Scan Mar 16, 2023Документ20 страницAdobe Scan Mar 16, 2023Renalyn Ps MewagОценок пока нет

- Ans June 2018 Far410Документ8 страницAns June 2018 Far4102022478048Оценок пока нет

- NyayДокумент3 страницыNyayJunneth Pearl HomocОценок пока нет

- Suggested Solutions June 2007Документ12 страницSuggested Solutions June 2007kalowekamoОценок пока нет

- June 2009 Fa4a1Документ9 страницJune 2009 Fa4a1ksakala58Оценок пока нет

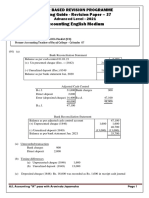

- Accounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Документ6 страницAccounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Malar SrirengarajahОценок пока нет

- Quiz For Week 7 Answer Key PR 1 and 4Документ3 страницыQuiz For Week 7 Answer Key PR 1 and 4Joshuakenallen ricabuertaОценок пока нет

- Taxation - I: (Please Turn Over)Документ3 страницыTaxation - I: (Please Turn Over)Laskar REAZ100% (1)

- 08chap 8 NP Farming Solutions 2020Документ3 страницы08chap 8 NP Farming Solutions 202044v8ct8cdyОценок пока нет

- MQP ANS 01 NДокумент13 страницMQP ANS 01 NAVINASH ROYОценок пока нет

- Irc Kit JJ20Документ35 страницIrc Kit JJ20Amir ArifОценок пока нет

- Sol. Man. - Chapter 4 - Accounts Receivable - Ia Part 1aДокумент19 страницSol. Man. - Chapter 4 - Accounts Receivable - Ia Part 1aMiguel AmihanОценок пока нет

- Partnership Accounts:: Assets Revaluation, Dissolution & Conversion To Limited CompanyДокумент47 страницPartnership Accounts:: Assets Revaluation, Dissolution & Conversion To Limited CompanyWen Xin GanОценок пока нет

- F2 Past Paper - Ans12-2006Документ8 страницF2 Past Paper - Ans12-2006ArsalanACCAОценок пока нет

- Review of The Accounting Process Problems 2-1. (Tiger Company)Документ5 страницReview of The Accounting Process Problems 2-1. (Tiger Company)Pauline Kisha CastroОценок пока нет

- Cash Flow Statement ProblemДокумент2 страницыCash Flow Statement Problemapi-3842194100% (2)

- AC191 Autumn 2011 FINALДокумент9 страницAC191 Autumn 2011 FINALgerlaniamelgacoОценок пока нет

- Where Will Your Strategy Guru Lead YouДокумент2 страницыWhere Will Your Strategy Guru Lead YouShailendra KelaniОценок пока нет

- Life LessonsДокумент4 страницыLife LessonsShailendra KelaniОценок пока нет

- Toy Stories - Association For Psychological Science - APSДокумент5 страницToy Stories - Association For Psychological Science - APSShailendra KelaniОценок пока нет

- Life/Work Lessons: These Behaviors Can Improve Your Performance and Value To Your OrganizationДокумент1 страницаLife/Work Lessons: These Behaviors Can Improve Your Performance and Value To Your OrganizationShailendra KelaniОценок пока нет

- Annexures Entreprenure QuestionnaireДокумент7 страницAnnexures Entreprenure QuestionnaireShailendra KelaniОценок пока нет

- No33 Maximizingbenefitsofself-Assess GoodДокумент8 страницNo33 Maximizingbenefitsofself-Assess GoodShailendra KelaniОценок пока нет

- Super Productivity WorksheetДокумент2 страницыSuper Productivity WorksheetShailendra Kelani0% (1)

- Entrepreneurship and Entrepreneurial Motivation: Nadire YimamuДокумент45 страницEntrepreneurship and Entrepreneurial Motivation: Nadire YimamuShailendra KelaniОценок пока нет

- Organizational Assessment: A Review of Experience: Universalia Occasional Paper No. 31, October 1998Документ16 страницOrganizational Assessment: A Review of Experience: Universalia Occasional Paper No. 31, October 1998Shailendra KelaniОценок пока нет

- Memory TechniquesДокумент9 страницMemory TechniquesShailendra Kelani100% (3)

- The Great TransformerДокумент2 страницыThe Great TransformerShailendra KelaniОценок пока нет

- Daily Check List QuestionДокумент1 страницаDaily Check List QuestionShailendra KelaniОценок пока нет

- 9.5 Self Discovery Questions 2Документ2 страницы9.5 Self Discovery Questions 2Shailendra KelaniОценок пока нет

- 2015 Bio Verne HarnishДокумент1 страница2015 Bio Verne HarnishShailendra KelaniОценок пока нет

- Staying Small SMEДокумент9 страницStaying Small SMEShailendra KelaniОценок пока нет

- Antar Mouna HandoutДокумент2 страницыAntar Mouna HandoutShailendra KelaniОценок пока нет

- Leadership Lessons From The Animal Kingdom: and Sik-Liong Ang, MBAДокумент9 страницLeadership Lessons From The Animal Kingdom: and Sik-Liong Ang, MBAShailendra KelaniОценок пока нет

- Wisdom of AlexДокумент4 страницыWisdom of AlexShailendra KelaniОценок пока нет

- All Topics - The Multiplier Mindset BlogДокумент2 страницыAll Topics - The Multiplier Mindset BlogShailendra KelaniОценок пока нет

- Article Leadership LessonДокумент3 страницыArticle Leadership LessonShailendra KelaniОценок пока нет

- Grandparents 2Документ13 страницGrandparents 2api-288503311Оценок пока нет

- Ancient Greek LanguageДокумент35 страницAncient Greek LanguageGheşea Georgiana0% (1)

- Student Notice 2023-07-15 Attention All StudentsДокумент1 страницаStudent Notice 2023-07-15 Attention All StudentsTanmoy SinghaОценок пока нет

- The River Systems of India Can Be Classified Into Four GroupsДокумент14 страницThe River Systems of India Can Be Classified Into Four Groupsem297Оценок пока нет

- Pearbudget: (Easy Budgeting For Everyone)Документ62 страницыPearbudget: (Easy Budgeting For Everyone)iPakistan100% (3)

- Aud Prob Compilation 1Документ31 страницаAud Prob Compilation 1Chammy TeyОценок пока нет

- Randy C de Lara 2.1Документ2 страницыRandy C de Lara 2.1Jane ParaisoОценок пока нет

- Internship Final Students CircularДокумент1 страницаInternship Final Students CircularAdi TyaОценок пока нет

- Republic Act. 10157Документ24 страницыRepublic Act. 10157roa yusonОценок пока нет

- Aquarium Aquarius Megalomania: Danish Norwegian Europop Barbie GirlДокумент2 страницыAquarium Aquarius Megalomania: Danish Norwegian Europop Barbie GirlTuan DaoОценок пока нет

- Oracle IRecruitment Setup V 1.1Документ14 страницOracle IRecruitment Setup V 1.1Irfan AhmadОценок пока нет

- Traditions and Encounters 3Rd Edition Bentley Test Bank Full Chapter PDFДокумент49 страницTraditions and Encounters 3Rd Edition Bentley Test Bank Full Chapter PDFsinhhanhi7rp100% (7)

- Public Administration and Governance: Esther RandallДокумент237 страницPublic Administration and Governance: Esther RandallShazaf KhanОценок пока нет

- The Champion Legal Ads 04-01-21Документ45 страницThe Champion Legal Ads 04-01-21Donna S. SeayОценок пока нет

- Cmvli DigestsДокумент7 страницCmvli Digestsbeth_afanОценок пока нет

- KGBV Bassi Profile NewДокумент5 страницKGBV Bassi Profile NewAbhilash MohapatraОценок пока нет

- Petersen S 4 Wheel Off Road December 2015Документ248 страницPetersen S 4 Wheel Off Road December 20154lexx100% (1)

- 2016-10-26 Memo Re Opposition To MTDДокумент64 страницы2016-10-26 Memo Re Opposition To MTDWNYT NewsChannel 13Оценок пока нет

- Intro To OptionsДокумент9 страницIntro To OptionsAntonio GenОценок пока нет

- Exercises 1-3 Corporate PlanningДокумент17 страницExercises 1-3 Corporate Planningmarichu apiladoОценок пока нет

- MC - Unit 2Документ3 страницыMC - Unit 2pnpt2801Оценок пока нет

- CorinnamunteanДокумент2 страницыCorinnamunteanapi-211075103Оценок пока нет

- Housing Project Process GuideДокумент52 страницыHousing Project Process GuideLelethu NgwenaОценок пока нет

- BlompmДокумент208 страницBlompmswiftvishnulalОценок пока нет

- Personal LoanДокумент49 страницPersonal Loantodkarvijay50% (6)

- Vespers Conversion of Saint PaulДокумент7 страницVespers Conversion of Saint PaulFrancis Carmelle Tiu DueroОценок пока нет

- Budget Finance For Law Enforcement Module 7 Ggonzales 2Документ9 страницBudget Finance For Law Enforcement Module 7 Ggonzales 2api-526672985Оценок пока нет

- LWB Manual PDFДокумент1 страницаLWB Manual PDFKhalid ZgheirОценок пока нет

- S F R S (I) 1 - 2 1: Accounting For The Effects of Changes in Foreign Currency Exchange RatesДокумент40 страницS F R S (I) 1 - 2 1: Accounting For The Effects of Changes in Foreign Currency Exchange RatesRilo WiloОценок пока нет

- Bakst - Music and Soviet RealismДокумент9 страницBakst - Music and Soviet RealismMaurício FunciaОценок пока нет