Вам также может понравиться

- Petroleum Exploration and Exploitation in NorwayОт EverandPetroleum Exploration and Exploitation in NorwayРейтинг: 5 из 5 звезд5/5 (1)

- THE DETERMINANTS OF PRICES OF NEWBUILDING IN THE VERY LARGE CRUDE CARRIERS (VLCC) SECTORОт EverandTHE DETERMINANTS OF PRICES OF NEWBUILDING IN THE VERY LARGE CRUDE CARRIERS (VLCC) SECTORОценок пока нет

- MackeyMike Cvte2002opt PDFДокумент21 страницаMackeyMike Cvte2002opt PDFPuri PurwantariОценок пока нет

- Study of Changes in Patterns of LNG Tanker Operation: Research ObjectiveДокумент26 страницStudy of Changes in Patterns of LNG Tanker Operation: Research Objectivejbloggs2007Оценок пока нет

- Presentation On LNG For Pip Seminar in Pso HouseДокумент26 страницPresentation On LNG For Pip Seminar in Pso HouseRASHID AHMED SHAIKHОценок пока нет

- Morgan Stanley Oil PDFДокумент19 страницMorgan Stanley Oil PDFTinuoye Folusho OmotayoОценок пока нет

- LNG ShippingДокумент46 страницLNG ShippingmekulaОценок пока нет

- Market Reserch Report-Marine Equipment - IndiaДокумент30 страницMarket Reserch Report-Marine Equipment - IndiaManoj KhankaОценок пока нет

- Cole Transportation Issues Inland&Ocean FreightДокумент15 страницCole Transportation Issues Inland&Ocean Freightjoescribd55Оценок пока нет

- ITEM 1.1.2:: Imbalances in The Shipbuilding Industry: Magnitude, Causes & Potential Policy ImplicationsДокумент24 страницыITEM 1.1.2:: Imbalances in The Shipbuilding Industry: Magnitude, Causes & Potential Policy Implicationsshannel jacksonОценок пока нет

- Propulsion Trends in Bulk CarriersДокумент28 страницPropulsion Trends in Bulk CarriersbpidkhhОценок пока нет

- Platou Monthly December 2009bДокумент11 страницPlatou Monthly December 2009bWisnu KertaningnagoroОценок пока нет

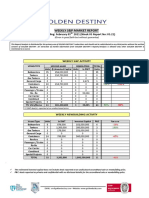

- Weekly SP Market Report Week Ending January 22nd 2021 Week 3 Report No 03.21Документ8 страницWeekly SP Market Report Week Ending January 22nd 2021 Week 3 Report No 03.21Sandesh Tukaram GhandatОценок пока нет

- Articulo Traduccido - Nano-P AsphДокумент16 страницArticulo Traduccido - Nano-P AsphJuanDiegoRayoОценок пока нет

- Arctic Shipping Route-1 - No - Video - With - Supplement - Oct15Документ24 страницыArctic Shipping Route-1 - No - Video - With - Supplement - Oct15eyaoОценок пока нет

- Capex - 1Документ21 страницаCapex - 1Leandro FagundesОценок пока нет

- Juan Camilo Aguilar Maya de OtroДокумент15 страницJuan Camilo Aguilar Maya de OtroJuan Camilo Aguilar MayaОценок пока нет

- Pea Petroleum EconomicsДокумент68 страницPea Petroleum EconomicsShehzad khan100% (1)

- Indian Shipbuilding Industry and Its Future ProspectsДокумент22 страницыIndian Shipbuilding Industry and Its Future ProspectsRocki100% (1)

- The Valuation of Ship, Art and Science - Roger BartlettДокумент36 страницThe Valuation of Ship, Art and Science - Roger BartlettWisnu KertaningnagoroОценок пока нет

- Adam HedayatДокумент13 страницAdam Hedayatbayu nurdiОценок пока нет

- Borna Petrovic Roro Market From A Brokers PerspectiveДокумент24 страницыBorna Petrovic Roro Market From A Brokers PerspectiveNNMSAОценок пока нет

- Henghe Materials (Catalogue)Документ45 страницHenghe Materials (Catalogue)juanrosonОценок пока нет

- Danish Shipping Facts and FiguresДокумент29 страницDanish Shipping Facts and FiguresMarc AseanОценок пока нет

- 2017 06 07 Experiences With Methanol in Dual Fuel Operation On Stena Germanica LewenhauptДокумент19 страниц2017 06 07 Experiences With Methanol in Dual Fuel Operation On Stena Germanica LewenhauptAkram FaisalОценок пока нет

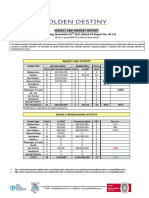

- Weekly SP Market Report Week Ending February 05th 2021 Week 5 Report No 05.21Документ8 страницWeekly SP Market Report Week Ending February 05th 2021 Week 5 Report No 05.21Sandesh Tukaram GhandatОценок пока нет

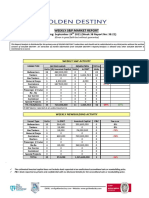

- Weekly SP Market Report Week Ending November 05th 2021 Week 44 Report No 44.21Документ8 страницWeekly SP Market Report Week Ending November 05th 2021 Week 44 Report No 44.21Sandesh Tukaram GhandatОценок пока нет

- Programme: LNG Shipping - Recent Trends and ProspectsДокумент16 страницProgramme: LNG Shipping - Recent Trends and Prospectsturtletrader123456Оценок пока нет

- Oil and Natural Gas LogisticsДокумент7 страницOil and Natural Gas LogisticsAl JawadОценок пока нет

- Freight RatesДокумент17 страницFreight RatesAmit KumarОценок пока нет

- LNGДокумент52 страницыLNGRama Moorthy100% (6)

- Weekly SP Market Report Week Ending March 19th 2021 Week 11 Report No 11.21Документ8 страницWeekly SP Market Report Week Ending March 19th 2021 Week 11 Report No 11.21Sandesh Tukaram GhandatОценок пока нет

- Attachment - Fuel Demand Calculation For Marina VesselsДокумент1 страницаAttachment - Fuel Demand Calculation For Marina VesselsFranz OttОценок пока нет

- Dry Bulk Shipping-An Opportunity or An Illusion - Yu Jiang LisarainДокумент17 страницDry Bulk Shipping-An Opportunity or An Illusion - Yu Jiang LisarainInstitute for Global Maritime Studies Greek ChapterОценок пока нет

- 43 - Simple Model For Newbuilding Cost PDFДокумент12 страниц43 - Simple Model For Newbuilding Cost PDFRianОценок пока нет

- Weekly SP Market Report Week Ending September 24th 2021 Week 38 Report No 38.21Документ7 страницWeekly SP Market Report Week Ending September 24th 2021 Week 38 Report No 38.21Sandesh Tukaram GhandatОценок пока нет

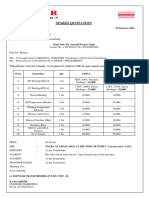

- Spares QuotationДокумент1 страницаSpares QuotationSaurabh Kumar SinghОценок пока нет

- LNG & LPG Shipping Fundamentals PDFДокумент15 страницLNG & LPG Shipping Fundamentals PDFRafi Algawi100% (1)

- Standardised Vessel Dataset SVD For Noon ReportsДокумент20 страницStandardised Vessel Dataset SVD For Noon ReportsSanthosh DhandapaniОценок пока нет

- Risk Assessment and Loss Prevention of LNG Carriers - KS WanglДокумент58 страницRisk Assessment and Loss Prevention of LNG Carriers - KS WanglJean MarieОценок пока нет

- Seafish Fleet Economic Performance Dataset 2007-2017 (Excel Tables)Документ131 страницаSeafish Fleet Economic Performance Dataset 2007-2017 (Excel Tables)Santhosh DhandapaniОценок пока нет

- Weekly SP Market Report Week Ending January 29th 2021 Week 4 Report No 04.21Документ7 страницWeekly SP Market Report Week Ending January 29th 2021 Week 4 Report No 04.21Sandesh Tukaram GhandatОценок пока нет

- Pensana PLC Corporate Presentation Spring 2022Документ24 страницыPensana PLC Corporate Presentation Spring 202210evenwoodcloseОценок пока нет

- Morgan Stanley OilДокумент19 страницMorgan Stanley Oilephraim_tammyОценок пока нет

- Weekly SP Market Report Week Ending June 18th 2021 Week 24 Report No 24.21Документ7 страницWeekly SP Market Report Week Ending June 18th 2021 Week 24 Report No 24.21Sandesh Tukaram GhandatОценок пока нет

- LNG Bunkering Concepts To Suit Local InfrastructureДокумент24 страницыLNG Bunkering Concepts To Suit Local InfrastructureNAV KOLОценок пока нет

- National Variables (Session 15) : Fundamental Studies Head Universidad Privada BolivianaДокумент44 страницыNational Variables (Session 15) : Fundamental Studies Head Universidad Privada BolivianaFabio RizzoОценок пока нет

- Analysis of The World Cruise IndustryДокумент12 страницAnalysis of The World Cruise IndustryGaryОценок пока нет

- Thierry ClementДокумент29 страницThierry ClementBagus WinarkoОценок пока нет

- I01 Douglas-Westwood - Calvin Ling - APAC Pipeline Market OutlookДокумент15 страницI01 Douglas-Westwood - Calvin Ling - APAC Pipeline Market OutlookandrairawanОценок пока нет

- 1 - Petrobras - DeepWater Gas LiftДокумент36 страниц1 - Petrobras - DeepWater Gas LiftNisar KhanОценок пока нет

- Weekly SP Market Report Week Ending July 2nd 2021 Week 26 Report No 26.21Документ7 страницWeekly SP Market Report Week Ending July 2nd 2021 Week 26 Report No 26.21Sandesh Tukaram GhandatОценок пока нет

- Weekly SP Market Report Week Ending February 26th 2021 Week 8 Report No 08.21Документ8 страницWeekly SP Market Report Week Ending February 26th 2021 Week 8 Report No 08.21Sandesh Tukaram GhandatОценок пока нет

- Een Hydrogen Economy Roadmap CPark FinalДокумент22 страницыEen Hydrogen Economy Roadmap CPark FinalVanVuAnhОценок пока нет

- Affinity Research Crude Oil Tanker Outlook 2016-11-16Документ64 страницыAffinity Research Crude Oil Tanker Outlook 2016-11-16LondonguyОценок пока нет

- Modern Offshore Support Vessels ClassДокумент18 страницModern Offshore Support Vessels ClassAqif IsaОценок пока нет

- Weekly SP Market Report Week Ending May 28th 2021 Week 21 Report No 21.21Документ7 страницWeekly SP Market Report Week Ending May 28th 2021 Week 21 Report No 21.21Sandesh Tukaram GhandatОценок пока нет

- Concept DefinitionДокумент1 страницаConcept DefinitionYan LaksanaОценок пока нет

- Methanol OverviewДокумент3 страницыMethanol OverviewYan LaksanaОценок пока нет

- ADB Prospectus Indonesia For DistributionДокумент12 страницADB Prospectus Indonesia For DistributionYan LaksanaОценок пока нет

- Cooling and Water ScenarioДокумент6 страницCooling and Water ScenarioYan LaksanaОценок пока нет

- The Cost of DesalinationДокумент16 страницThe Cost of DesalinationYan LaksanaОценок пока нет

- Fertilizer PresentationДокумент7 страницFertilizer PresentationYan LaksanaОценок пока нет

- Indonesia Salary Guide Ebook PDFДокумент22 страницыIndonesia Salary Guide Ebook PDFteguh_setiono100% (2)

- No. Chemical Product Proposed Plant Capacity (MTPA)Документ1 страницаNo. Chemical Product Proposed Plant Capacity (MTPA)Yan LaksanaОценок пока нет

- Concept DefinitionДокумент1 страницаConcept DefinitionYan LaksanaОценок пока нет

- New Gold SummaryДокумент1 страницаNew Gold SummaryYan LaksanaОценок пока нет

- Daftar Pltu RiДокумент6 страницDaftar Pltu Rirahmatrasit7742Оценок пока нет

- 4.1.3 Properties of Coals PDFДокумент7 страниц4.1.3 Properties of Coals PDFJaco KotzeОценок пока нет

- NRDC Consolidated Coal Renewable Database 2017Документ38 страницNRDC Consolidated Coal Renewable Database 2017Yan LaksanaОценок пока нет

- Presentasi PipingДокумент45 страницPresentasi PipingYan LaksanaОценок пока нет

- Fpso Design Document: Marie C. Mcgraw Roberto J. Mel Endez Javier A. RamosДокумент20 страницFpso Design Document: Marie C. Mcgraw Roberto J. Mel Endez Javier A. RamosYan Laksana100% (2)

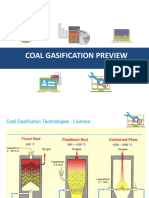

- Coal Gasification PreviewДокумент4 страницыCoal Gasification PreviewYan LaksanaОценок пока нет

- Pinang 5900 Coal Quality: According To ISO Methods, Except HGI, Trace Elements and Ash Analysis To ASTMДокумент1 страницаPinang 5900 Coal Quality: According To ISO Methods, Except HGI, Trace Elements and Ash Analysis To ASTMYan LaksanaОценок пока нет

- Global Dimethyl Ether Emerging Markets - DMEДокумент27 страницGlobal Dimethyl Ether Emerging Markets - DMEUci UtamiОценок пока нет

- Fuel Rekonsiliasi 2013Документ41 страницаFuel Rekonsiliasi 2013Yan LaksanaОценок пока нет

- GTL TechnologyДокумент3 страницыGTL TechnologyYan LaksanaОценок пока нет

- Chap4lowres PDFДокумент28 страницChap4lowres PDFshazniSОценок пока нет

- Reburning Renewable Biomass For Emissions Control and Ash Deposition Effects in Power Generation PDFДокумент250 страницReburning Renewable Biomass For Emissions Control and Ash Deposition Effects in Power Generation PDFYan LaksanaОценок пока нет

- G20 Subsidies - ChinaДокумент22 страницыG20 Subsidies - ChinaYan LaksanaОценок пока нет

- Synfuel TechnologyДокумент9 страницSynfuel TechnologyYan LaksanaОценок пока нет

- CBM Book IntroДокумент1 страницаCBM Book IntroRihamОценок пока нет

- Study On Ecological and Highly Efficient Combustion Technology For Upgraded Brown Coal PDFДокумент137 страницStudy On Ecological and Highly Efficient Combustion Technology For Upgraded Brown Coal PDFYan LaksanaОценок пока нет

- Pemurnian Metanol Dari Kandungan Tri Methyl Amine Di PT. Kaltim Methanol Industri - Bontang KaltimДокумент7 страницPemurnian Metanol Dari Kandungan Tri Methyl Amine Di PT. Kaltim Methanol Industri - Bontang KaltimSylvia ChavezОценок пока нет

- Centrifugal PumpsДокумент117 страницCentrifugal PumpsYan LaksanaОценок пока нет

- Annual Report 2019Документ306 страницAnnual Report 2019Faris Ahmad AdliОценок пока нет

- Boiler Fuel Firing SystemДокумент44 страницыBoiler Fuel Firing Systemrashm006ranjanОценок пока нет

- Selecting Best Technology Lineup For Designing Gas Processing Units PDFДокумент21 страницаSelecting Best Technology Lineup For Designing Gas Processing Units PDFSatria 'igin' Girindra Nugraha100% (1)

- LPG Energy Efficiency Report PDFДокумент50 страницLPG Energy Efficiency Report PDFFERNANDO JOSE NOVAESОценок пока нет

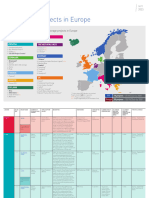

- CO2 Storage Projects in Europe Map 120919Документ10 страницCO2 Storage Projects in Europe Map 120919av1986362Оценок пока нет

- Industrial Policy 10-15Документ36 страницIndustrial Policy 10-15Rameswara ReddyОценок пока нет

- Overveiw of The Nefter IndusryДокумент3 страницыOverveiw of The Nefter Indusryyesuplus2Оценок пока нет

- Ali DaДокумент8 страницAli DaBudhaditya GoswamiОценок пока нет

- Research ProjectДокумент30 страницResearch ProjectYasser AshourОценок пока нет

- Argentina-World Development IndicatorsДокумент522 страницыArgentina-World Development IndicatorsbodyfullОценок пока нет

- Revoil WhitepaperДокумент32 страницыRevoil WhitepaperИлья ТеркОценок пока нет

- Loss PotentialGAP 8.0.1.1Документ9 страницLoss PotentialGAP 8.0.1.1Victor VazquezОценок пока нет

- PHL Power Generation IssuesДокумент39 страницPHL Power Generation IssuesdskymaximusОценок пока нет

- Stoichiometry 2 StudentsДокумент1 страницаStoichiometry 2 StudentsJackielyn EugenioОценок пока нет

- Hang Hy Van - 19ED10130Документ85 страницHang Hy Van - 19ED10130van hangОценок пока нет

- Intra ReportДокумент73 страницыIntra ReportAin TieyОценок пока нет

- BP 33-PetroleumДокумент7 страницBP 33-PetroleumMyra De GuzmanОценок пока нет

- Calibration of Brittleness To Elastic Rock Properties Via Mineralogy Logs in Unconventional ReservoirsДокумент32 страницыCalibration of Brittleness To Elastic Rock Properties Via Mineralogy Logs in Unconventional ReservoirsJuanMa TurraОценок пока нет

- Fertiliser Technology MCQs PDFДокумент23 страницыFertiliser Technology MCQs PDFRao Muhammad AhmadОценок пока нет

- Well PlanningДокумент18 страницWell PlanningBrahim Letaief100% (3)

- ProjectДокумент12 страницProjectAamer MansoorОценок пока нет

- Emission Factors From Cross Sector Tools (August 2012)Документ158 страницEmission Factors From Cross Sector Tools (August 2012)Yasnaa HerNandooОценок пока нет

- Cheniere Energy Presentation 2023 Q1Документ22 страницыCheniere Energy Presentation 2023 Q1SteveОценок пока нет

- Recovery of Spent CatalystДокумент4 страницыRecovery of Spent CatalystUtsav PatelОценок пока нет

- 22 RNG PDFДокумент41 страница22 RNG PDFJuan DomaniczkyОценок пока нет

- Presentasi AkhirДокумент27 страницPresentasi AkhirHanggoro Tri Aditya100% (1)

- Section 7 - Nitrogen Carbon DioxideДокумент57 страницSection 7 - Nitrogen Carbon Dioxidejesus alberto juarez churioОценок пока нет

- Shell Business Areas PDF Final 2Документ19 страницShell Business Areas PDF Final 2嘉雯吳Оценок пока нет

- SIC CodesДокумент77 страницSIC Codesmejocoba82Оценок пока нет

- WaukeshaBrochure1079 NUEVOДокумент18 страницWaukeshaBrochure1079 NUEVOMatthew BrownОценок пока нет