Вам также может понравиться

- Regional Rural Banks of India: Evolution, Performance and ManagementОт EverandRegional Rural Banks of India: Evolution, Performance and ManagementОценок пока нет

- SWOT Analysis of Banking IndustryДокумент13 страницSWOT Analysis of Banking IndustryApoorv94% (18)

- Modes of Investment of IBBLДокумент53 страницыModes of Investment of IBBLMussa Ratul100% (2)

- MCQ Central BankingДокумент5 страницMCQ Central BankingYogesh GharpureОценок пока нет

- SWOT ANALYSIS of PICIC BankДокумент4 страницыSWOT ANALYSIS of PICIC BankWasimOrakzai100% (3)

- Internship Report On Departments and Subsidiaries Branches of ICBДокумент37 страницInternship Report On Departments and Subsidiaries Branches of ICBNafiz FahimОценок пока нет

- Internship Report On BRAC Bank Ltd.Документ93 страницыInternship Report On BRAC Bank Ltd.Md. Likhon82% (17)

- Mobile Banking Prospects in BangladeshДокумент17 страницMobile Banking Prospects in BangladeshRobin SarkerОценок пока нет

- Internship Report On Credit Management Published by RahulДокумент78 страницInternship Report On Credit Management Published by Rahulrahulpalit126Оценок пока нет

- Role of Pune District Central Cooperative Bank in Rural DevelopmentДокумент16 страницRole of Pune District Central Cooperative Bank in Rural Developmentshubham jagtap100% (1)

- South Bangla Agriculture & Commerce Bank LTDДокумент35 страницSouth Bangla Agriculture & Commerce Bank LTDNafiz Niaz50% (4)

- Boro - Effect of Mobile Banking On Financial Inclusion in KenyaДокумент61 страницаBoro - Effect of Mobile Banking On Financial Inclusion in Kenyaedu mainaОценок пока нет

- Individual Assignment - On - COMPANY - STRATEGIC - ANALYSIS.Документ14 страницIndividual Assignment - On - COMPANY - STRATEGIC - ANALYSIS.Adanech100% (1)

- INTERNSHIP PROPOSAL On Green BankingДокумент7 страницINTERNSHIP PROPOSAL On Green Bankingsourav4730Оценок пока нет

- My Internship ProposalДокумент7 страницMy Internship Proposalsourav4730Оценок пока нет

- Basel NormsДокумент23 страницыBasel NormsPranu PranuОценок пока нет

- Project Report ON: Foreign Exchange Operation: A Study On Social Islami Bank Limited Submitted ToДокумент55 страницProject Report ON: Foreign Exchange Operation: A Study On Social Islami Bank Limited Submitted ToJannatul FerdousОценок пока нет

- Analyzing Customer Satisfaction of Sonali BankДокумент40 страницAnalyzing Customer Satisfaction of Sonali Bankbabu rahman aliОценок пока нет

- Slide - Open Case Discussion (Sample) - Disney Adds Value Using A Related Diversification StrategyДокумент22 страницыSlide - Open Case Discussion (Sample) - Disney Adds Value Using A Related Diversification StrategySumon iqbalОценок пока нет

- Brief history of the Indian banking systemДокумент61 страницаBrief history of the Indian banking systemRavi VishwakarmaОценок пока нет

- Corporate Finance Paper MidДокумент2 страницыCorporate Finance Paper MidAjmal KhanОценок пока нет

- Internship Report On Credit Risk Management of Jamuna Bank LimitedДокумент22 страницыInternship Report On Credit Risk Management of Jamuna Bank LimitedZunaid Hasan57% (7)

- Porter Five Forces banking sector PakistanДокумент2 страницыPorter Five Forces banking sector Pakistansyed tayyab sherazi100% (1)

- Executive Summary of e BankingДокумент24 страницыExecutive Summary of e BankingKiranShetty0% (1)

- FinTech in Bangladesh: An Emerging IndustryДокумент27 страницFinTech in Bangladesh: An Emerging IndustryIshtiaq ShushaanОценок пока нет

- Sample QuestionnaireДокумент4 страницыSample QuestionnaireAnonymous F17qIBHxОценок пока нет

- Adoption of Open Banking in the PhilippinesДокумент21 страницаAdoption of Open Banking in the PhilippinesWendelynn Giannina AngОценок пока нет

- Effect of Credit Risk Management On The Performance of Commercial Banks in Nigeria 1 To 3Документ57 страницEffect of Credit Risk Management On The Performance of Commercial Banks in Nigeria 1 To 3MajestyОценок пока нет

- Bangladesh Krishi Bank report overviewДокумент39 страницBangladesh Krishi Bank report overviewDebashish Chakraborty75% (4)

- Research Proposal On BankingДокумент23 страницыResearch Proposal On Bankingrujuta88% (8)

- B LawДокумент240 страницB LawShaheer MalikОценок пока нет

- SME Financing Performance of Banks in BangladeshДокумент42 страницыSME Financing Performance of Banks in BangladeshDrubo Sobur100% (1)

- MicrofinanceДокумент79 страницMicrofinanceBasti96% (27)

- Managing human resources internationallyДокумент3 страницыManaging human resources internationallyWasifОценок пока нет

- Assessing The Effectiveness of The Internal Control System in The Commercial Banks of Ethiopia: A Case of Hawassa CityДокумент5 страницAssessing The Effectiveness of The Internal Control System in The Commercial Banks of Ethiopia: A Case of Hawassa CityIjsrnet EditorialОценок пока нет

- A Study On Consumer Perception Towards Mobile Banking Services of State Bank of IndiaДокумент45 страницA Study On Consumer Perception Towards Mobile Banking Services of State Bank of IndiaVijaya Anandhan100% (1)

- Sonali Bank LTD Customer Satisfaction EditДокумент37 страницSonali Bank LTD Customer Satisfaction Editbabu rahman ali0% (1)

- Challenges and Opportunities of Expansion of Islamic Banks in Ethiopia: Case of Commercial Bank of Ethiopian Dire Dawa Interest Free BranchДокумент9 страницChallenges and Opportunities of Expansion of Islamic Banks in Ethiopia: Case of Commercial Bank of Ethiopian Dire Dawa Interest Free BranchNejash Abdo Issa100% (1)

- Financial Progress at SUBCO BankДокумент79 страницFinancial Progress at SUBCO BankAnushree AnuОценок пока нет

- FCCBДокумент8 страницFCCBRadha RampalliОценок пока нет

- Asset Liability Management in Indian Banking SectorДокумент63 страницыAsset Liability Management in Indian Banking SectorSami Zama100% (2)

- Research ProposalДокумент22 страницыResearch ProposalHABTEMARIAM ERTBANОценок пока нет

- Indian Banking System ReportДокумент55 страницIndian Banking System ReportPinky KusumaОценок пока нет

- Deposit MobiliziationДокумент454 страницыDeposit MobiliziationperkisasОценок пока нет

- Idoc - Pub - Internship Report On Financial Performance Analysis of Sonali Bank LimitedДокумент47 страницIdoc - Pub - Internship Report On Financial Performance Analysis of Sonali Bank LimitedFahimОценок пока нет

- Electronic Banking in BangladeshДокумент19 страницElectronic Banking in BangladeshjonneymanОценок пока нет

- ZION Corporate Management & Consultanc yДокумент26 страницZION Corporate Management & Consultanc yGetnat Bahiru100% (3)

- Financial Inclusion Study on Rocket Mobile BankingДокумент56 страницFinancial Inclusion Study on Rocket Mobile BankingTanjin UrmiОценок пока нет

- TYBBI - Financial Reporting AnalysisДокумент18 страницTYBBI - Financial Reporting AnalysisNandhiniОценок пока нет

- Term Paper On APEX FOODS LTD. Samina Sultana-8451Документ45 страницTerm Paper On APEX FOODS LTD. Samina Sultana-8451pranta senОценок пока нет

- Swot Analysis of Faysal Bank LimitedДокумент3 страницыSwot Analysis of Faysal Bank LimitedOsama Bilwani50% (2)

- Internet Banking IntroductionДокумент4 страницыInternet Banking Introductionaihjaaz a71% (7)

- Credit Risk ManagementДокумент16 страницCredit Risk Managementkrishnalohia9Оценок пока нет

- Mobile Banking (Banking in Your Hand)Документ82 страницыMobile Banking (Banking in Your Hand)Dipock Mondal67% (12)

- Evaluation of Mobile Banking Operation of Dutch Bangla Bank LimitedДокумент72 страницыEvaluation of Mobile Banking Operation of Dutch Bangla Bank LimitedSaydur Rahman Sayeed100% (7)

- Scenario of Satisfaction Among Employees of Agrani Bank Limited of and Its Impact On BankingДокумент51 страницаScenario of Satisfaction Among Employees of Agrani Bank Limited of and Its Impact On BankingNina Hooper0% (1)

- Financial System in BangladeshДокумент30 страницFinancial System in BangladeshS.E Chowdhury90% (31)

- Internet Banking in SBI - Preeti Pawar 357358Документ90 страницInternet Banking in SBI - Preeti Pawar 357358pawarprateek100% (3)

- Investmentmodes of IbblДокумент4 страницыInvestmentmodes of IbblangelОценок пока нет

- Default Loan-Cancer For The Banking Sector of BangladeshДокумент5 страницDefault Loan-Cancer For The Banking Sector of BangladeshTanjila TombyОценок пока нет

- Group 1-VikingsДокумент23 страницыGroup 1-VikingsangelОценок пока нет

- Investment Avenues Available in BangladeshДокумент16 страницInvestment Avenues Available in BangladeshangelОценок пока нет

- 2011017040.biman ChowdhuryДокумент23 страницы2011017040.biman ChowdhuryangelОценок пока нет

- COVID-19 IMPACT ON EMPLOYMENT IN BANGLADESHДокумент18 страницCOVID-19 IMPACT ON EMPLOYMENT IN BANGLADESHangelОценок пока нет

- Developing A Multinational Sporting Goods CorporationДокумент3 страницыDeveloping A Multinational Sporting Goods CorporationangelОценок пока нет

- An Assignment On "Covid 19 and Its Impact On Employment: Bangladesh Perspective"Документ26 страницAn Assignment On "Covid 19 and Its Impact On Employment: Bangladesh Perspective"angelОценок пока нет

- 2011017038.shahriar Ahmed ChowdhuryДокумент19 страниц2011017038.shahriar Ahmed ChowdhuryangelОценок пока нет

- All Students Must Be Present During Presentation of Each GroupДокумент1 страницаAll Students Must Be Present During Presentation of Each GroupangelОценок пока нет

- Exposure To International Flow of FundsДокумент7 страницExposure To International Flow of FundsangelОценок пока нет

- Assignment On "Covid 19 and It's Impacts On Employment-International Perspective"Документ16 страницAssignment On "Covid 19 and It's Impacts On Employment-International Perspective"angelОценок пока нет

- COVID-19's Impact on HRMДокумент22 страницыCOVID-19's Impact on HRMangelОценок пока нет

- 2011017044.lima Akther Dilruba PDFДокумент19 страниц2011017044.lima Akther Dilruba PDFangelОценок пока нет

- An Assignment On: Covid 19 and Its Impacts On Employment-International PerspectiveДокумент19 страницAn Assignment On: Covid 19 and Its Impacts On Employment-International Perspectiveangel100% (1)

- Covid-19 Impact on Global EmploymentДокумент32 страницыCovid-19 Impact on Global EmploymentangelОценок пока нет

- Problems and Prospects of Tailoring Shops in SylhetДокумент5 страницProblems and Prospects of Tailoring Shops in SylhetangelОценок пока нет

- 2011017001.avishek Talukder DiproДокумент18 страниц2011017001.avishek Talukder DiproangelОценок пока нет

- Chapter 1: IntroductionДокумент20 страницChapter 1: IntroductionangelОценок пока нет

- 2011017004.gulam Haidar SiddiqueДокумент24 страницы2011017004.gulam Haidar SiddiqueangelОценок пока нет

- Chapter 4: AppendixДокумент5 страницChapter 4: AppendixangelОценок пока нет

- Leading University: On Problem and Prospectus of Tailoring Shop in Sylhet''Документ4 страницыLeading University: On Problem and Prospectus of Tailoring Shop in Sylhet''angelОценок пока нет

- Simple Progressive Simple Progressive: Active Voice Passive VoiceДокумент2 страницыSimple Progressive Simple Progressive: Active Voice Passive VoiceangelОценок пока нет

- Group 3 Vikings - MBA 4th-BДокумент24 страницыGroup 3 Vikings - MBA 4th-BangelОценок пока нет

- Leading University, Sylhet: Student ID Student Name Mid-TermДокумент2 страницыLeading University, Sylhet: Student ID Student Name Mid-TermangelОценок пока нет

- Group 3 VikingsДокумент30 страницGroup 3 VikingsangelОценок пока нет

- Marketing Innovation During The Corona PandemicДокумент4 страницыMarketing Innovation During The Corona PandemicangelОценок пока нет

- Student ID and Name List by TopicДокумент2 страницыStudent ID and Name List by TopicangelОценок пока нет

- List of PrepositionsДокумент5 страницList of PrepositionsangelОценок пока нет

- Your 5 Strengths and Weaknesses with ExplanationsДокумент3 страницыYour 5 Strengths and Weaknesses with ExplanationsangelОценок пока нет

- Identify The Distinctive Characteristics/Behaviors of Quality Leaders/LeadershipДокумент2 страницыIdentify The Distinctive Characteristics/Behaviors of Quality Leaders/LeadershipangelОценок пока нет

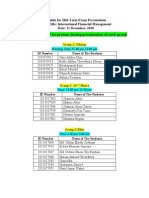

- MBA/EMBA Semester Final Exam Groups & ScheduleДокумент2 страницыMBA/EMBA Semester Final Exam Groups & ScheduleangelОценок пока нет

- Chamika's Style: Hairstylist: Braids, Twist, Cornrows, Those Type of Hair StylesДокумент30 страницChamika's Style: Hairstylist: Braids, Twist, Cornrows, Those Type of Hair StylesUmarОценок пока нет

- Financial AidДокумент1 страницаFinancial Aidshb100% (1)

- Engineering EconomyДокумент23 страницыEngineering EconomyFaten Nabilla Nordin100% (1)

- BASO Presentation PDFДокумент25 страницBASO Presentation PDFGEOEXPLOREMINPERU MINERÍA Y GEOLOGIAОценок пока нет

- Credit Rating AgenciesДокумент40 страницCredit Rating AgenciesSmriti DurehaОценок пока нет

- 15968615919016284WДокумент2 страницы15968615919016284WSourya MitraОценок пока нет

- BPI's Opposition to Sarabia Manor's Rehabilitation PlanДокумент2 страницыBPI's Opposition to Sarabia Manor's Rehabilitation PlanJean Mary AutoОценок пока нет

- FAR NotesДокумент11 страницFAR NotesJhem Montoya OlendanОценок пока нет

- Atlas Honda - Balance SheetДокумент1 страницаAtlas Honda - Balance SheetMail MergeОценок пока нет

- Mrunal Economy Handouts PCB8 2023-24Документ901 страницаMrunal Economy Handouts PCB8 2023-24Adharsh Surendhiran100% (3)

- ch03 - Free Cash Flow ValuationДокумент66 страницch03 - Free Cash Flow Valuationmahnoor javaidОценок пока нет

- Small Business Loan Application Form For Individual - Sole - BDOДокумент2 страницыSmall Business Loan Application Form For Individual - Sole - BDOjunco111222Оценок пока нет

- Impact of The Tax System On The Financial Activity of Business EntitiesДокумент6 страницImpact of The Tax System On The Financial Activity of Business EntitiesOpen Access JournalОценок пока нет

- ანგარიშგება PDFДокумент39 страницანგარიშგება PDFSandro ChanturidzeОценок пока нет

- Medical Reimbursemen APPLICATION SETДокумент5 страницMedical Reimbursemen APPLICATION SETLeelakrishna GvОценок пока нет

- Cir Vs Metro Star SuperamaДокумент2 страницыCir Vs Metro Star SuperamaDonna TreceñeОценок пока нет

- CMA Case Study Blades PTY LTDДокумент6 страницCMA Case Study Blades PTY LTDMuhamad ArdiansyahОценок пока нет

- KOMALДокумент50 страницKOMALanand kumarОценок пока нет

- Project Report On "Role of Banks in International Trade": Page - 1Документ50 страницProject Report On "Role of Banks in International Trade": Page - 1Adarsh Rasal100% (1)

- CV - Divya GoyalДокумент1 страницаCV - Divya GoyalGarima JainОценок пока нет

- Fin 580 WK 2 Paper - Team CДокумент5 страницFin 580 WK 2 Paper - Team Cchad salcidoОценок пока нет

- Tugas P2-1A Dan P2-2A Peng - AkuntansiДокумент5 страницTugas P2-1A Dan P2-2A Peng - AkuntansiAlche MistОценок пока нет

- Solution Manual For Designing and Managing The Supply Chain 3rd Edition by David Simchi LeviДокумент5 страницSolution Manual For Designing and Managing The Supply Chain 3rd Edition by David Simchi LeviRamswaroop Khichar100% (1)

- Annual Report 2019Документ228 страницAnnual Report 2019Rohit PatelОценок пока нет

- Central Surety and Lnsurance Company, Inc. vs. UbayДокумент5 страницCentral Surety and Lnsurance Company, Inc. vs. UbayMarianne RegaladoОценок пока нет

- Part-1-General - and - Financial - Awareness Set - 1Документ4 страницыPart-1-General - and - Financial - Awareness Set - 1Anto KevinОценок пока нет

- Alagappa University DDE BBM First Year Financial Accounting Exam - Paper2Документ5 страницAlagappa University DDE BBM First Year Financial Accounting Exam - Paper2mansoorbariОценок пока нет

- Vajiram & Ravi Civil Services Exam Details for Sept 2022-23Документ3 страницыVajiram & Ravi Civil Services Exam Details for Sept 2022-23Appu MansaОценок пока нет

- Blank - Nota SiasatanДокумент41 страницаBlank - Nota SiasatanprinceofkedahОценок пока нет