Вам также может понравиться

- Government Securities Market Development The Indonesia CaseДокумент31 страницаGovernment Securities Market Development The Indonesia CaseADBI EventsОценок пока нет

- Bank Licensing Requirements in the PhilippinesДокумент27 страницBank Licensing Requirements in the PhilippinesDu Baladad Andrew MichaelОценок пока нет

- SEBI Draft Regulations Investment AdvisorsДокумент51 страницаSEBI Draft Regulations Investment AdvisorspbdkpkОценок пока нет

- Introduction To Financial ManagementДокумент19 страницIntroduction To Financial ManagementSaurabh AgrawalОценок пока нет

- Financial ManagementДокумент886 страницFinancial ManagementKRISHNA PRASAD SAMUDRALAОценок пока нет

- Master in Business Finance Structured FinanceДокумент38 страницMaster in Business Finance Structured Financepraloy66Оценок пока нет

- A Presentation On Commercial BanksДокумент9 страницA Presentation On Commercial BanksAhel Patrick VitsuОценок пока нет

- Audit of Banks - July 8, 2022Документ29 страницAudit of Banks - July 8, 2022Bea Garcia100% (1)

- Ares Pathfinder Core Fund Presentation To The City of Phoenix January 2024 Redacted vFINALДокумент26 страницAres Pathfinder Core Fund Presentation To The City of Phoenix January 2024 Redacted vFINALgeorgi.korovskiОценок пока нет

- Vietnam: Increasing Access To Credit Through Collateral (Secured Transactions) ReformДокумент62 страницыVietnam: Increasing Access To Credit Through Collateral (Secured Transactions) ReformIFC Access to Finance and Financial MarketsОценок пока нет

- Finance Lesson 1Документ5 страницFinance Lesson 1JM BalanoОценок пока нет

- Bai Muajjal Bai Salam and Istisna inДокумент18 страницBai Muajjal Bai Salam and Istisna inFariaFaryОценок пока нет

- Institutional and Legal Frameworks For Public Debt ManagementДокумент22 страницыInstitutional and Legal Frameworks For Public Debt ManagementAsian Development Bank - Event DocumentsОценок пока нет

- Bipartite 1 FINO AGREEMENTДокумент20 страницBipartite 1 FINO AGREEMENTSaanvi Singh100% (1)

- Shashank Rao CV - Canada FormatДокумент2 страницыShashank Rao CV - Canada FormatShashank RaoОценок пока нет

- Msme Advances: Canara Bank Officers' Association Promotion Study Material - 2018Документ67 страницMsme Advances: Canara Bank Officers' Association Promotion Study Material - 2018Majhar HussainОценок пока нет

- 7 Investment PolicyДокумент87 страниц7 Investment PolicyShaurya Singh100% (1)

- Cvccreditpartnerseuropeanopportunitiesjul 16Документ48 страницCvccreditpartnerseuropeanopportunitiesjul 16Mus ChrifiОценок пока нет

- GANASEVA0MODEL Enabling Rural BankingДокумент20 страницGANASEVA0MODEL Enabling Rural BankingAnjali AryaОценок пока нет

- Deleveraging Investing Optimizing Capital StructurДокумент42 страницыDeleveraging Investing Optimizing Capital StructurDanaero SethОценок пока нет

- Alternatives in Todays Capital MarketsДокумент16 страницAlternatives in Todays Capital MarketsjoanОценок пока нет

- World Gold Analyst - Zimbabwe Special Report September 2010Документ100 страницWorld Gold Analyst - Zimbabwe Special Report September 2010dshornikovОценок пока нет

- Web Analytics, Web Mining, and Social AnalyticsДокумент53 страницыWeb Analytics, Web Mining, and Social AnalyticsAsmita NagpalОценок пока нет

- Taxguru - In-Checklist For Statutory Audit of Bank Branch Audit An OverviewДокумент8 страницTaxguru - In-Checklist For Statutory Audit of Bank Branch Audit An OverviewBhavani GirineniОценок пока нет

- Hamden Audit FY20Документ131 страницаHamden Audit FY20Helen BennettОценок пока нет

- 10 Years AnniversaryДокумент88 страниц10 Years AnniversarykaryssmakyОценок пока нет

- Week 2 Week 3 - Acc For Deposits and InvestmentsДокумент28 страницWeek 2 Week 3 - Acc For Deposits and InvestmentsimieОценок пока нет

- Service Request Form - Axis BankДокумент2 страницыService Request Form - Axis BankRishab GoelОценок пока нет

- NabkisanДокумент24 страницыNabkisanDnyaneshwar Dattatraya PhadatareОценок пока нет

- Pillar#1B-1: Classification of Financial Intermediaries: Bank & NBFCДокумент27 страницPillar#1B-1: Classification of Financial Intermediaries: Bank & NBFCPRATIK PRAKASHОценок пока нет

- Key Risk Management Issues (5) Liquidity Risk Basel ProposalsДокумент63 страницыKey Risk Management Issues (5) Liquidity Risk Basel ProposalsNGUYEN HUU THUОценок пока нет

- Functions and Roles of the Financial SystemДокумент33 страницыFunctions and Roles of the Financial SystemtanzirkhanОценок пока нет

- Cambodia Census Result 98Документ305 страницCambodia Census Result 98Kouhei NyamukОценок пока нет

- BOG Notice No. BG GOV SEC 2021 13 Requirement To Paticipate in The Credit Reporting SystemДокумент2 страницыBOG Notice No. BG GOV SEC 2021 13 Requirement To Paticipate in The Credit Reporting SystemFuaad DodooОценок пока нет

- Merchant Banking in Indian Financial SystemДокумент91 страницаMerchant Banking in Indian Financial SystemVENKATESAN R-2020Оценок пока нет

- Investing in Mutual Funds: Types, Expenses, and PerformanceДокумент12 страницInvesting in Mutual Funds: Types, Expenses, and PerformanceDave ThreeTearsОценок пока нет

- Pssbooklet PDFДокумент142 страницыPssbooklet PDFForkLogОценок пока нет

- Term LoanДокумент39 страницTerm Loanashok_gupta077Оценок пока нет

- Pule MFMP Quotation 16 UДокумент3 страницыPule MFMP Quotation 16 UPuleОценок пока нет

- FEMA REGULATION OF FOREIGN EXCHANGEДокумент31 страницаFEMA REGULATION OF FOREIGN EXCHANGEManpreet Kaur SekhonОценок пока нет

- 2023 L1 FixedIncomeДокумент117 страниц2023 L1 FixedIncomezirabamuzale sowediОценок пока нет

- Kim - Sbi Equity Hybrid FundДокумент24 страницыKim - Sbi Equity Hybrid FundbbaalluuОценок пока нет

- 166-2020 Roi PDFДокумент47 страниц166-2020 Roi PDFANJAN SINGH 3AОценок пока нет

- Export-Import Docs: Step-by-Step GuideДокумент91 страницаExport-Import Docs: Step-by-Step GuideadhinayakgoharОценок пока нет

- Introduction and Users Guide Module 1Документ23 страницыIntroduction and Users Guide Module 1Holy BankОценок пока нет

- ALM Project ReportДокумент18 страницALM Project ReportAISHWARYA CHAUHANОценок пока нет

- Wealth Management Group 8: Name Roll NoДокумент16 страницWealth Management Group 8: Name Roll NoAdii AdityaОценок пока нет

- Morgan Stanley: Ka Him NG Kevin Yu Eric Long Ming ChuДокумент116 страницMorgan Stanley: Ka Him NG Kevin Yu Eric Long Ming ChuvaibhavОценок пока нет

- Offer DocumentДокумент14 страницOffer DocumentsidhanthaОценок пока нет

- Mergers SPAC ELearnДокумент3 страницыMergers SPAC ELearnOwen ChanОценок пока нет

- Icici NPSДокумент30 страницIcici NPSRamanathan KathiresanОценок пока нет

- Tutorial 9 Q & AДокумент2 страницыTutorial 9 Q & Achunlun87Оценок пока нет

- DAIBB Lending - 2 - 0Документ8 страницDAIBB Lending - 2 - 0ashraf294Оценок пока нет

- Fin656 U1Документ73 страницыFin656 U1Elora madhusmita BeheraОценок пока нет

- The Optimal Capital Structure: Balancing the Costs and Benefits of DebtДокумент127 страницThe Optimal Capital Structure: Balancing the Costs and Benefits of DebtMailyn Castro-VillaОценок пока нет

- A Study On The Growth in Assets and Composition of Mutual Funds Assets in IndiaДокумент47 страницA Study On The Growth in Assets and Composition of Mutual Funds Assets in Indiavinayjain221Оценок пока нет

- DR Chipika Financial Inclusion Forum Presentation - 19 Feb 2019Документ59 страницDR Chipika Financial Inclusion Forum Presentation - 19 Feb 2019TinasheОценок пока нет

- Wcms 437194Документ12 страницWcms 437194Akshaya K C PSGRKCWОценок пока нет

- BIFSIR Documentation (Small 15.12.16) PDFДокумент15 страницBIFSIR Documentation (Small 15.12.16) PDFaimeinstaОценок пока нет

- Director FamilirisationДокумент16 страницDirector FamilirisationSriramОценок пока нет

- Colliers Manila Full Report Q4 2020 v1Документ16 страницColliers Manila Full Report Q4 2020 v1Ronnie EncarnacionОценок пока нет

- Urban Sprawl and Land Use Characteristics in The Urban Fringe of Metro Manila PhilippinesДокумент8 страницUrban Sprawl and Land Use Characteristics in The Urban Fringe of Metro Manila PhilippinesElaine SamaniegoОценок пока нет

- Urban Growth in Metro ManilaДокумент4 страницыUrban Growth in Metro ManilaRonnie EncarnacionОценок пока нет

- Urban Sprawl and Land Use Characteristics in The Urban Fringe of Metro Manila PhilippinesДокумент8 страницUrban Sprawl and Land Use Characteristics in The Urban Fringe of Metro Manila PhilippinesElaine SamaniegoОценок пока нет

- Urban Growth in Metro ManilaДокумент4 страницыUrban Growth in Metro ManilaRonnie EncarnacionОценок пока нет

- Issues and Directions on Integrated Public Transport in Metro ManilaДокумент16 страницIssues and Directions on Integrated Public Transport in Metro ManilaRonnie EncarnacionОценок пока нет

- Issues and Directions on Integrated Public Transport in Metro ManilaДокумент16 страницIssues and Directions on Integrated Public Transport in Metro ManilaRonnie EncarnacionОценок пока нет

- Trading RulesДокумент48 страницTrading RulesRonnie EncarnacionОценок пока нет

- Financial Inclusion Initiatives 2017: Bangko Sentral NG PilipinasДокумент26 страницFinancial Inclusion Initiatives 2017: Bangko Sentral NG PilipinasRonnie EncarnacionОценок пока нет

- OBLICON-2nd Exam - 1245 (Dation) and 1252 (Application)Документ2 страницыOBLICON-2nd Exam - 1245 (Dation) and 1252 (Application)Karen Joy MasapolОценок пока нет

- Corporate Financial Management Practice Exam QuestionsДокумент10 страницCorporate Financial Management Practice Exam QuestionsAston CheeОценок пока нет

- Writing Inequalities From Word ProblemsДокумент28 страницWriting Inequalities From Word Problemsapi-379755793Оценок пока нет

- Case Dismissals For Lack of Standing To ForecloseДокумент28 страницCase Dismissals For Lack of Standing To Foreclosejacque zidane100% (1)

- Summary Economics of Money Banking and Financial Markets Frederic S Mishkin PDFДокумент143 страницыSummary Economics of Money Banking and Financial Markets Frederic S Mishkin PDFJohn StephensОценок пока нет

- ICICI Bank Ltd. Versus Official Liquidator of APS StarДокумент17 страницICICI Bank Ltd. Versus Official Liquidator of APS StarAman Kumar YadavОценок пока нет

- 29 9 13 Accounts SumsДокумент11 страниц29 9 13 Accounts SumssahilgeraОценок пока нет

- Invitation for Bids Nepal Water ProjectДокумент3 страницыInvitation for Bids Nepal Water Projectshrinath2kОценок пока нет

- CS Excutive Programme Module II (New Course) Appendix Final June 2010Документ15 страницCS Excutive Programme Module II (New Course) Appendix Final June 2010Vaneet KumarОценок пока нет

- Arceo, Jr. Vs People of The PHДокумент2 страницыArceo, Jr. Vs People of The PHToni CalsadoОценок пока нет

- A Study On Analysis of Financial Statements of Polyhydron Pvt. LTDДокумент107 страницA Study On Analysis of Financial Statements of Polyhydron Pvt. LTDkunal hajareОценок пока нет

- Example Credit Application FormДокумент1 страницаExample Credit Application FormPrime PropsОценок пока нет

- Photography Session ContractДокумент5 страницPhotography Session Contractapi-24913181367% (3)

- Maharashtra Act No. XLV of 1963Документ20 страницMaharashtra Act No. XLV of 1963BalrajОценок пока нет

- BMV L20 3EF LiverpoolДокумент6 страницBMV L20 3EF LiverpoolOctav CobzareanuОценок пока нет

- Chronology of Data Breaches - Privacy Rights Clearinghouse - June 4, 2014Документ558 страницChronology of Data Breaches - Privacy Rights Clearinghouse - June 4, 2014St. Louis Public RadioОценок пока нет

- Winding Up - 2017Документ44 страницыWinding Up - 2017Lim Yew TongОценок пока нет

- Pimco Corp. Opp Fund (Pty)Документ46 страницPimco Corp. Opp Fund (Pty)ArvinLedesmaChiongОценок пока нет

- Black ScholesДокумент57 страницBlack ScholesAshish DixitОценок пока нет

- BD Price ListДокумент1 страницаBD Price Listherodataherculis2172100% (1)

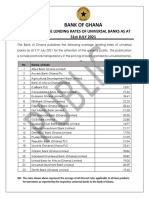

- Average Lending Rates As at July 2021Документ1 страницаAverage Lending Rates As at July 2021Fuaad DodooОценок пока нет

- Mnitest Chapter 18Документ2 страницыMnitest Chapter 18An DoОценок пока нет

- Intracompany Accounting SetupДокумент9 страницIntracompany Accounting SetupcanjiatpОценок пока нет

- Bank Guarantees and Trade FinanceДокумент14 страницBank Guarantees and Trade Finance1221Оценок пока нет

- Fears and Lobbying in Colli..Документ9 страницFears and Lobbying in Colli..spudgun56Оценок пока нет

- cd8cd552db28943f022096d821b9a279 (1)Документ12 страницcd8cd552db28943f022096d821b9a279 (1)Azri LunduОценок пока нет

- G.R. No. 85733 February 23, 1990 Land Dispute Case Between Original Owners and Successive BuyersДокумент5 страницG.R. No. 85733 February 23, 1990 Land Dispute Case Between Original Owners and Successive BuyersJay-ar TeodoroОценок пока нет

- Playing The REITs GameДокумент2 страницыPlaying The REITs Gameonlylf28311Оценок пока нет

- RIZAL COMMERCIAL BANKING CORPORATION, UY CHUN BING AND ELI D. LAO, Petitioners, vs. COURT OF APPEALS and GOYU & SONS, INC.Документ16 страницRIZAL COMMERCIAL BANKING CORPORATION, UY CHUN BING AND ELI D. LAO, Petitioners, vs. COURT OF APPEALS and GOYU & SONS, INC.ceilo coboОценок пока нет

- 4th SemДокумент6 страниц4th SemSijo JacobОценок пока нет