Вам также может понравиться

- Sarfaesi Act PPT-1Документ21 страницаSarfaesi Act PPT-1Vironika Reddy100% (1)

- Final-Sarfaesi Act 2002Документ41 страницаFinal-Sarfaesi Act 2002ninpra50% (2)

- Notes On NBFCДокумент9 страницNotes On NBFCgspkishore7953Оценок пока нет

- School Finance Team TORДокумент2 страницыSchool Finance Team TORGrace Music100% (1)

- Change Management EssayДокумент5 страницChange Management EssayAvinashОценок пока нет

- Non Banking Financial InstitutionsДокумент53 страницыNon Banking Financial InstitutionsVenkat RajuОценок пока нет

- Overview of Sarfaesi Act, 2002Документ8 страницOverview of Sarfaesi Act, 2002Pragati OjhaОценок пока нет

- CP 5 Acceptance of Deposits-UnlockedДокумент38 страницCP 5 Acceptance of Deposits-UnlockedKarthik Imperious100% (1)

- Wealth Management & Asset ManagementДокумент32 страницыWealth Management & Asset ManagementVineetChandakОценок пока нет

- CLTD - Training - Quiz Questions - Module 1 - DoneДокумент32 страницыCLTD - Training - Quiz Questions - Module 1 - DoneTringa0% (1)

- Sarfaesi ACT, 2002: Project Presentstion BY Smit GandhiДокумент16 страницSarfaesi ACT, 2002: Project Presentstion BY Smit GandhismitОценок пока нет

- Business Torts GuideДокумент20 страницBusiness Torts GuideChristina TorresОценок пока нет

- Presentation On NBFCДокумент37 страницPresentation On NBFCNavin Tulsyan100% (3)

- Understanding Chit Funds and NBFCs in IndiaДокумент26 страницUnderstanding Chit Funds and NBFCs in IndiasairishikeshОценок пока нет

- Article On Deposits-Vinod Kothari ConsultantsДокумент9 страницArticle On Deposits-Vinod Kothari ConsultantsNishant JainОценок пока нет

- Chapter 5 Acceptance of Deposits by CompaniesДокумент52 страницыChapter 5 Acceptance of Deposits by CompaniesAbhay SharmaОценок пока нет

- Lesson 3 - Lending IndustryДокумент15 страницLesson 3 - Lending Industryqrrzyz7whgОценок пока нет

- The Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002Документ35 страницThe Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002NeelgaganSaiyanОценок пока нет

- SARFAESI Act - Empowers banks to recover NPAs without court interventionДокумент3 страницыSARFAESI Act - Empowers banks to recover NPAs without court interventionsubhasis123bbsrОценок пока нет

- Chapter 5 - Deposit VfinalДокумент9 страницChapter 5 - Deposit VfinalAryan KapoorОценок пока нет

- (C) NBFC - NotesДокумент30 страниц(C) NBFC - NotesBarkhaОценок пока нет

- Amount Not Considered As DepositsДокумент16 страницAmount Not Considered As Depositsmuthuram2497Оценок пока нет

- CH 3Документ3 страницыCH 3sunilviniОценок пока нет

- Chapter 2 - General ConceptДокумент5 страницChapter 2 - General ConceptShasharu Fei-fei LimОценок пока нет

- Non-Banking Financial Companies (NBFCS) : Project byДокумент25 страницNon-Banking Financial Companies (NBFCS) : Project byBhupen YadavОценок пока нет

- SARFAESI ACT PPTsДокумент109 страницSARFAESI ACT PPTsChandra RajanОценок пока нет

- Sarfaesi ActДокумент13 страницSarfaesi Act..sravana karthik100% (5)

- RBI FAQs NBFCs 10-04-15Документ8 страницRBI FAQs NBFCs 10-04-15jeetОценок пока нет

- 3.2. Law Relating To Commercial Banks-2Документ51 страница3.2. Law Relating To Commercial Banks-2Madan ShresthaОценок пока нет

- Islamic Private Debt Securities (IPDS) RulesДокумент37 страницIslamic Private Debt Securities (IPDS) RulesSara IbrahimОценок пока нет

- SARFAESI Act: Secured creditors' rights for NPA recoveryДокумент9 страницSARFAESI Act: Secured creditors' rights for NPA recoveryDeepak Mangal0% (1)

- DebentureДокумент5 страницDebentureShweta RawatОценок пока нет

- Securitisation Process and Key PartiesДокумент32 страницыSecuritisation Process and Key PartiesAmit SinghОценок пока нет

- NBFC Project - 298647323 PDFДокумент45 страницNBFC Project - 298647323 PDFRupal Rohan DalalОценок пока нет

- Securitisation of Debt (Loan Assets)Документ7 страницSecuritisation of Debt (Loan Assets)Sanskar YadavОценок пока нет

- Chapter 16 SARFESI, 2002Документ58 страницChapter 16 SARFESI, 2002Deepsikha maitiОценок пока нет

- NBFCs: Non-Banking Financial Companies ExplainedДокумент37 страницNBFCs: Non-Banking Financial Companies ExplainedMukul Babbar100% (2)

- Important Points Under The Banning of Unregulated Deposit Schemes Ordinance, 2019Документ6 страницImportant Points Under The Banning of Unregulated Deposit Schemes Ordinance, 2019KARTHIK AОценок пока нет

- Audit of Non Banking Financial Companies: HapterДокумент6 страницAudit of Non Banking Financial Companies: HapterAditya Jayseelan KОценок пока нет

- All About NBFC'SДокумент3 страницыAll About NBFC'SGayatri JoshiОценок пока нет

- Deposit Ordinance BillДокумент4 страницыDeposit Ordinance BillUmesh ChoumalОценок пока нет

- Kenya's banking regulations and licensing rulesДокумент33 страницыKenya's banking regulations and licensing rulesChristine NyangauОценок пока нет

- 5.acceptance of Deposits by CompaniesДокумент39 страниц5.acceptance of Deposits by Companiessamartha umbareОценок пока нет

- Non-Banking Financial CompaniesДокумент18 страницNon-Banking Financial CompaniesBhushan GuptaОценок пока нет

- 39 NBFCДокумент10 страниц39 NBFCDivyam ShahОценок пока нет

- BBI FinalДокумент25 страницBBI FinalVarsha ParabОценок пока нет

- Acceptance of DepositsДокумент19 страницAcceptance of DepositsRam IyerОценок пока нет

- JAIIB Paper 3 Module C Banking Related Laws Download PDFДокумент42 страницыJAIIB Paper 3 Module C Banking Related Laws Download PDFstudy studyОценок пока нет

- Thrift BanksДокумент20 страницThrift BanksIrene Sobiate MorcillaОценок пока нет

- Bnmit College ProjectДокумент21 страницаBnmit College ProjectIMAM JAVOORОценок пока нет

- Presentation On Non Banking Financial CompaniesДокумент17 страницPresentation On Non Banking Financial CompaniesMayurpmОценок пока нет

- NBFCДокумент13 страницNBFCkumarsaorabh131985Оценок пока нет

- NBFCs Explained: What is an NBFC and Key Differences from BanksДокумент49 страницNBFCs Explained: What is an NBFC and Key Differences from BanksMalavika MadhuОценок пока нет

- A Banking Law Presentation On SARFAESI AДокумент23 страницыA Banking Law Presentation On SARFAESI AChandra RajanОценок пока нет

- The Banning of Unregulated Deposit Schemes Act, 2019 - Arrangement of SectionsДокумент23 страницыThe Banning of Unregulated Deposit Schemes Act, 2019 - Arrangement of Sectionsgayatri parkarОценок пока нет

- Venture CapitalДокумент17 страницVenture CapitalVidhyaBalaОценок пока нет

- What Are NBFCsДокумент12 страницWhat Are NBFCsRohan ShirdhankarОценок пока нет

- Unit 16 Banking and Non-Banking Companies - Basic ConceptsДокумент31 страницаUnit 16 Banking and Non-Banking Companies - Basic ConceptsRupa BuswasОценок пока нет

- 5.NBFCs in IndiaДокумент12 страниц5.NBFCs in IndiaDr.R.Umamaheswari MBAОценок пока нет

- Financial Services & Institutions - An IntroductionДокумент11 страницFinancial Services & Institutions - An IntroductionMayank KumarОценок пока нет

- Redemption OF Debentures: After Studying This Unit, You Will Be Able ToДокумент36 страницRedemption OF Debentures: After Studying This Unit, You Will Be Able ToAkansha GuptaОценок пока нет

- May2018 99975Документ41 страницаMay2018 99975naytik jainОценок пока нет

- Project On Banker and CustomersДокумент85 страницProject On Banker and Customersrakesh9006Оценок пока нет

- IIBPS PO DI English - pdf-38 PDFДокумент11 страницIIBPS PO DI English - pdf-38 PDFRahul GaurОценок пока нет

- Republic of Kenya: Kenya Gazette Supplement No. 107 (Acts No.11)Документ26 страницRepublic of Kenya: Kenya Gazette Supplement No. 107 (Acts No.11)Benard OderoОценок пока нет

- Construction and Projects in Indonesia OverviewДокумент31 страницаConstruction and Projects in Indonesia OverviewDaniel LubisОценок пока нет

- Exam Complete Accounting Cycle KAREN JALAДокумент51 страницаExam Complete Accounting Cycle KAREN JALAGlemarie DamalerioОценок пока нет

- Case Study ALSA Contract Negotiation Workshop - Local PartnerДокумент2 страницыCase Study ALSA Contract Negotiation Workshop - Local PartnerAMSОценок пока нет

- 3 Accounting Cycle UDДокумент13 страниц3 Accounting Cycle UDERICK MLINGWAОценок пока нет

- Full FM Module Final Draft 222Документ157 страницFull FM Module Final Draft 222bikilahussenОценок пока нет

- Revision Question Topic 3,4Документ4 страницыRevision Question Topic 3,4Nur Wahida100% (1)

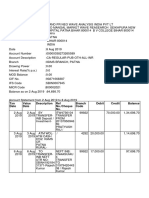

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceДокумент3 страницыTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaОценок пока нет

- English For Business Banking Finance AccountingДокумент66 страницEnglish For Business Banking Finance AccountingnatasyaОценок пока нет

- PRINCIPLES OF APPRAISAL PRACTICE AND CODE OF ETHICSДокумент20 страницPRINCIPLES OF APPRAISAL PRACTICE AND CODE OF ETHICSnaren_3456Оценок пока нет

- Supreme Court rules on banking operations without authorityДокумент45 страницSupreme Court rules on banking operations without authorityJustice PajarilloОценок пока нет

- Unit 21 Private Equity and Venture CapitalДокумент10 страницUnit 21 Private Equity and Venture CapitalHari RajОценок пока нет

- Final Order - Case No 38 of 2014Документ148 страницFinal Order - Case No 38 of 2014sachinoilОценок пока нет

- RA 6713 ReportДокумент6 страницRA 6713 Reportydlaz_tabОценок пока нет

- Lê H NG Linh Tel: 0903 978 552 Faculty of ESP FTUДокумент29 страницLê H NG Linh Tel: 0903 978 552 Faculty of ESP FTUPham Thi Kim OanhОценок пока нет

- Personal Finance Time Value of MoneyДокумент24 страницыPersonal Finance Time Value of MoneyLeo PanesОценок пока нет

- Introduction To AuditingДокумент21 страницаIntroduction To AuditingKul ShresthaОценок пока нет

- The Debtors Are Electroglas, Inc. (EIN 77-0336101) and Electroglas International, Inc. (EIN 77-0345011)Документ20 страницThe Debtors Are Electroglas, Inc. (EIN 77-0336101) and Electroglas International, Inc. (EIN 77-0345011)Chapter 11 DocketsОценок пока нет

- HHHHHДокумент5 страницHHHHHBrajesh PradhanОценок пока нет

- Past ExamДокумент11 страницPast Exammohamed.shaban2533Оценок пока нет

- NOTES Income Taxation Cheat SheetДокумент2 страницыNOTES Income Taxation Cheat SheetMARGARETTE ANGULOОценок пока нет

- Bitong v. CAДокумент36 страницBitong v. CAReemОценок пока нет

- Behavioural Finance Dissertation TopicsДокумент8 страницBehavioural Finance Dissertation TopicsOnlinePaperWritingServiceCanada100% (1)

- Managing Costs and Pricing Strategies for a UniversityДокумент2 страницыManaging Costs and Pricing Strategies for a UniversityAdeirehs Eyemarket BrissettОценок пока нет