Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Oral and Textual Traditions of Veda - Tamil Nadu Region: GotraДокумент10 страницOral and Textual Traditions of Veda - Tamil Nadu Region: GotraSergeyОценок пока нет

- Spots of Wilderness. 'Nature' in The Hindu Temples of KeralaДокумент33 страницыSpots of Wilderness. 'Nature' in The Hindu Temples of KeralaSergeyОценок пока нет

- Ritual Rivalry in KeralaДокумент16 страницRitual Rivalry in KeralaSergeyОценок пока нет

- Algebraic GamesДокумент25 страницAlgebraic GamesSergeyОценок пока нет

- A Sanskrit Manuscript of The Sarvabuddha PDFДокумент2 страницыA Sanskrit Manuscript of The Sarvabuddha PDFSergeyОценок пока нет

- 340515a0 PDFДокумент1 страница340515a0 PDFSergeyОценок пока нет

- J Jmacro 2019 103167Документ52 страницыJ Jmacro 2019 103167SergeyОценок пока нет

- T S W D H S: J E ' A - S P C: Shai A. Alleson-GerbergДокумент24 страницыT S W D H S: J E ' A - S P C: Shai A. Alleson-GerbergSergeyОценок пока нет

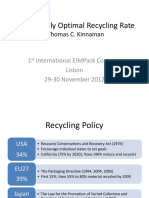

- 0.2 KinnamanДокумент38 страниц0.2 KinnamanSergeyОценок пока нет

- 522-Article Text-1004-1-10-20180408Документ7 страниц522-Article Text-1004-1-10-20180408SergeyОценок пока нет

- Padoux 2001 RGnoliДокумент4 страницыPadoux 2001 RGnoliSergeyОценок пока нет

- Xtable GalleryДокумент29 страницXtable GallerySergeyОценок пока нет

- Computationally Intelligent Agents in Economics and Finance: EditorialДокумент16 страницComputationally Intelligent Agents in Economics and Finance: EditorialSergeyОценок пока нет

- Toward Understanding Some Paradoxes in Capital Theory: Leland Yeager University of VirginiaДокумент34 страницыToward Understanding Some Paradoxes in Capital Theory: Leland Yeager University of VirginiaSergeyОценок пока нет

- Christian Elements in Early Frankist Doc PDFДокумент31 страницаChristian Elements in Early Frankist Doc PDFSergeyОценок пока нет

- Toh563 - 84000 Upholding The Great Secret MantraДокумент30 страницToh563 - 84000 Upholding The Great Secret MantraSergeyОценок пока нет

- Toh558 - 84000 Destroyer of The Great Trichiliocosm PDFДокумент101 страницаToh558 - 84000 Destroyer of The Great Trichiliocosm PDFSergey100% (1)

- In Search of The Marginal Entrepreneur BenchmarkinДокумент22 страницыIn Search of The Marginal Entrepreneur BenchmarkinSergeyОценок пока нет

- Toh558 - 84000 Destroyer of The Great TrichiliocosmДокумент101 страницаToh558 - 84000 Destroyer of The Great TrichiliocosmSergeyОценок пока нет

- Toh384 - 84000 The Glorious King of Tantras That Resolves All SecretsДокумент58 страницToh384 - 84000 The Glorious King of Tantras That Resolves All SecretsSergey100% (1)

- Military LogisticsДокумент20 страницMilitary LogisticsSergeyОценок пока нет

- Shu-Heng ChenДокумент22 страницыShu-Heng ChenSergeyОценок пока нет

- Toh544 - 84000 The Tantra of Siddhaikavira PDFДокумент61 страницаToh544 - 84000 The Tantra of Siddhaikavira PDFSergeyОценок пока нет

- Toh425 - 84000 The Maha Maya TantraДокумент40 страницToh425 - 84000 The Maha Maya TantraSergeyОценок пока нет

- The Practice Manual of Noble Tārā KurukullāДокумент131 страницаThe Practice Manual of Noble Tārā Kurukullāawacs12100% (4)

- Koppl - Against RA MethodologyДокумент13 страницKoppl - Against RA MethodologySergeyОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Active Critical ReadingДокумент22 страницыActive Critical ReadingYonn Me Me KyawОценок пока нет

- Reaserch ProstitutionДокумент221 страницаReaserch ProstitutionAron ChuaОценок пока нет

- Modules 1-8 Answer To Guides QuestionsДокумент15 страницModules 1-8 Answer To Guides QuestionsBlackblight •Оценок пока нет

- Case2-Forbidden CItyДокумент10 страницCase2-Forbidden CItyqzbtbq7y6dОценок пока нет

- Odysseus JourneyДокумент8 страницOdysseus JourneyDrey MartinezОценок пока нет

- He Hard Truth - If You Do Not Become A BRAND Then: Examples Oprah WinfreyДокумент11 страницHe Hard Truth - If You Do Not Become A BRAND Then: Examples Oprah WinfreyAbd.Khaliq RahimОценок пока нет

- Sibayan, Patrick Jorge - Weekly Accomplishment (July 8-14, 2019)Документ2 страницыSibayan, Patrick Jorge - Weekly Accomplishment (July 8-14, 2019)Patrick Jorge SibayanОценок пока нет

- Engineering Management Past, Present, and FutureДокумент4 страницыEngineering Management Past, Present, and Futuremonty4president100% (1)

- Invoice: Page 1 of 2Документ2 страницыInvoice: Page 1 of 2Gergo JuhaszОценок пока нет

- Abhiraj's Data Comm - I ProjectДокумент15 страницAbhiraj's Data Comm - I Projectabhirajsingh.bscllbОценок пока нет

- Randy Rowles: HAI's 2021-22 Chairman Keeps Moving ForwardДокумент76 страницRandy Rowles: HAI's 2021-22 Chairman Keeps Moving Forwardnestorin111Оценок пока нет

- Ikea ReportДокумент48 страницIkea ReportPulkit Puri100% (3)

- Region 12Документ75 страницRegion 12Jezreel DucsaОценок пока нет

- Nurlilis (Tgs. Bhs - Inggris. Chapter 4)Документ5 страницNurlilis (Tgs. Bhs - Inggris. Chapter 4)Latifa Hanafi100% (1)

- Pankaj YadavSEPT - 2022Документ1 страницаPankaj YadavSEPT - 2022dhirajutekar990Оценок пока нет

- Simao Toko Reincarnated Black JesusДокумент25 страницSimao Toko Reincarnated Black JesusMartin konoОценок пока нет

- The Boy Behind The CurtainДокумент6 страницThe Boy Behind The CurtainpewomokiОценок пока нет

- Pup LawДокумент144 страницыPup LawSheena ValenzuelaОценок пока нет

- Music Tradition of Kamrup-KamakhyaДокумент15 страницMusic Tradition of Kamrup-KamakhyaDilip ChangkakotyОценок пока нет

- Sample TosДокумент7 страницSample TosJenelin EneroОценок пока нет

- Hospital List (Noida & GZB)Документ3 страницыHospital List (Noida & GZB)prince.bhatiОценок пока нет

- P.S. Deodhar - Cinasthana Today - Viewing China From India-Tata McGraw Hill Education (2014)Документ372 страницыP.S. Deodhar - Cinasthana Today - Viewing China From India-Tata McGraw Hill Education (2014)MANEESH JADHAVОценок пока нет

- Cebu BRT Feasibility StudyДокумент35 страницCebu BRT Feasibility StudyCebuDailyNews100% (3)

- Eliza Valdez Bernudez Bautista, A035 383 901 (BIA May 22, 2013)Документ13 страницEliza Valdez Bernudez Bautista, A035 383 901 (BIA May 22, 2013)Immigrant & Refugee Appellate Center, LLCОценок пока нет

- 304 1 ET V1 S1 - File1Документ10 страниц304 1 ET V1 S1 - File1Frances Gallano Guzman AplanОценок пока нет

- Calendar of ActivitiesДокумент2 страницыCalendar of ActivitiesAJB Art and Perception100% (3)

- On Islamic Branding Brands As Good DeedsДокумент17 страницOn Islamic Branding Brands As Good Deedstried meОценок пока нет

- PS2082 VleДокумент82 страницыPS2082 Vlebillymambo0% (1)

- Mercado v. Nambi FLORESДокумент2 страницыMercado v. Nambi FLORESCarlos JamesОценок пока нет

- EDUC - 115 D - Fall2018 - Kathryn GauthierДокумент7 страницEDUC - 115 D - Fall2018 - Kathryn Gauthierdocs4me_nowОценок пока нет