Вам также может понравиться

- Subaru Forester ManualsДокумент636 страницSubaru Forester ManualsMarko JakobovicОценок пока нет

- EcR - 1 Leading and Lagging IndicatorsДокумент10 страницEcR - 1 Leading and Lagging IndicatorsMiloš ĐukićОценок пока нет

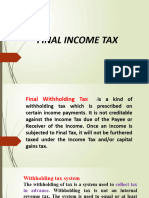

- Final Withholding Tax On Passive IncomeДокумент1 страницаFinal Withholding Tax On Passive IncomeChelsea Anne VidalloОценок пока нет

- REO CPA Review: REO: Income Taxation - Final Withholding Tax TableДокумент2 страницыREO CPA Review: REO: Income Taxation - Final Withholding Tax TableCamille SingianОценок пока нет

- Life Overseas 7 ThesisДокумент20 страницLife Overseas 7 ThesisRene Jr MalangОценок пока нет

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)От EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Рейтинг: 3.5 из 5 звезд3.5/5 (17)

- H04.1 - Final Income Tax TableДокумент2 страницыH04.1 - Final Income Tax Tablenona galidoОценок пока нет

- Quiz EmbryologyДокумент41 страницаQuiz EmbryologyMedShare90% (67)

- Chapter 05 Final Income Taxation1Документ2 страницыChapter 05 Final Income Taxation1raven dayritОценок пока нет

- EX EX EX EX: Regular Income TaxДокумент7 страницEX EX EX EX: Regular Income TaxMary Leigh TenezaОценок пока нет

- BS 5911-120Документ33 страницыBS 5911-120Niranjan GargОценок пока нет

- TRAIN Vs CREATEДокумент6 страницTRAIN Vs CREATEleejongsukОценок пока нет

- ItilДокумент11 страницItilNarendar P100% (2)

- Final Tax LectureДокумент7 страницFinal Tax LectureJefrey Jismen Ballesteros100% (1)

- Stress and FilipinosДокумент28 страницStress and FilipinosDaniel John Arboleda100% (2)

- HVDC BasicДокумент36 страницHVDC BasicAshok KumarОценок пока нет

- Final Tax Lecture PDFДокумент7 страницFinal Tax Lecture PDFMarlo Caluya ManuelОценок пока нет

- Urban Drainage Modelling Guide IUD - 1Документ196 страницUrban Drainage Modelling Guide IUD - 1Helmer Edgardo Monroy GonzálezОценок пока нет

- Regular Business/Corporate Tax: DC RFC NRFCДокумент2 страницыRegular Business/Corporate Tax: DC RFC NRFCGrace Angelie C. Asio-SalihОценок пока нет

- Passive Income Tax Rates for Residents and Non-ResidentsДокумент3 страницыPassive Income Tax Rates for Residents and Non-ResidentsPamela Jean CuyaОценок пока нет

- FT TableДокумент4 страницыFT TableChantie BorlonganОценок пока нет

- Tax Notes Aug 10-11Документ15 страницTax Notes Aug 10-11Reiner NuludОценок пока нет

- RateДокумент3 страницыRatemikamiiОценок пока нет

- Passive Incomefor Both Individual and Corporation Individual CorporationДокумент4 страницыPassive Incomefor Both Individual and Corporation Individual CorporationYrolle Lynart AldeОценок пока нет

- Chapter 05 Final Income Taxation TableДокумент4 страницыChapter 05 Final Income Taxation TablejannyОценок пока нет

- Income RC, NRC & RA Nranetb Interest Income DepositsДокумент3 страницыIncome RC, NRC & RA Nranetb Interest Income DepositsMichael AquinoОценок пока нет

- 8 Passive Income of Individuals LAST TOPIC BEFORE MIDTERMДокумент5 страниц8 Passive Income of Individuals LAST TOPIC BEFORE MIDTERMArgie DeguzmanОценок пока нет

- Source Final Tax: Interest Income or Yield From Local Currency Bank Deposits or Deposit SubstitutesДокумент3 страницыSource Final Tax: Interest Income or Yield From Local Currency Bank Deposits or Deposit SubstitutesJhon Ariel JulatonОценок пока нет

- Tax CH 1 13Документ7 страницTax CH 1 13Charmaine Contillo BasilioОценок пока нет

- Undergrad Review in Income TaxationДокумент17 страницUndergrad Review in Income TaxationJamesОценок пока нет

- AppendicesДокумент8 страницAppendicescrackheads philippinesОценок пока нет

- Income Tax TableДокумент6 страницIncome Tax TableCristle ServentoОценок пока нет

- Income TaxДокумент4 страницыIncome TaxLea Samantha GallardoОценок пока нет

- Tax Table Corporations 2022Документ4 страницыTax Table Corporations 2022Xandredg Sumpt LatogОценок пока нет

- Tax RatesДокумент2 страницыTax RatesSalma GurarОценок пока нет

- Final Taxes RatesДокумент2 страницыFinal Taxes RatesPanda CocoОценок пока нет

- Lesson 4 Final Income Taxation PDFДокумент4 страницыLesson 4 Final Income Taxation PDFErika ApitaОценок пока нет

- Sec. 27 & 28 - Tax On Corporations: Domestic Corporation Resident Foreign Corporation Non Resident Foreign CorporationДокумент13 страницSec. 27 & 28 - Tax On Corporations: Domestic Corporation Resident Foreign Corporation Non Resident Foreign CorporationdencamsОценок пока нет

- Summary of Passive Income and Capital Gains Taxes - MaupoДокумент4 страницыSummary of Passive Income and Capital Gains Taxes - MaupoMae MaupoОценок пока нет

- Citizenship and Taxation StatusДокумент4 страницыCitizenship and Taxation StatusAisah ReemОценок пока нет

- Non-Resident Tax Rates GuideДокумент2 страницыNon-Resident Tax Rates GuideEmy EspirituОценок пока нет

- Equity Oriented Funds (Subject To STT)Документ2 страницыEquity Oriented Funds (Subject To STT)AayushKumarОценок пока нет

- TaxpayerДокумент4 страницыTaxpayerMickaela Jaira AlvarezОценок пока нет

- Taxation: RC NRC RA Nraeb Nraneb SA On Taxable Income On Passive IncomeДокумент1 страницаTaxation: RC NRC RA Nraeb Nraneb SA On Taxable Income On Passive IncomeCyangenОценок пока нет

- FWTX, CWTX and CGTX (Points To Remember and Tax Rates)Документ2 страницыFWTX, CWTX and CGTX (Points To Remember and Tax Rates)Justz LimОценок пока нет

- HO4Passive Income - Revision 1Документ2 страницыHO4Passive Income - Revision 1Christopher SantosОценок пока нет

- Tax RatesДокумент6 страницTax RatesStephany PolinarОценок пока нет

- San Beda College of Law: 2005 C B O Annex B T R CДокумент3 страницыSan Beda College of Law: 2005 C B O Annex B T R CRachel LeachonОценок пока нет

- MF Tax Reckoner 2021 22 Revised01Документ4 страницыMF Tax Reckoner 2021 22 Revised01Alok KeswaniОценок пока нет

- Tax Module-4Документ21 страницаTax Module-4workwithellie1Оценок пока нет

- Tax TablesДокумент3 страницыTax TablesJimbo HotdogОценок пока нет

- Tata MF Tax - Reckoner - 2020 - 21Документ4 страницыTata MF Tax - Reckoner - 2020 - 21saurabhjain8414Оценок пока нет

- Tax Tables Latest Revisions 2022Документ2 страницыTax Tables Latest Revisions 2022Novyh Angelique CabreraОценок пока нет

- Corporate Income Tax RateДокумент3 страницыCorporate Income Tax RateJuliana ChengОценок пока нет

- Monthly Remittance Return of Final Income Taxes Withheld: Kawanihan NG Rentas InternasДокумент2 страницыMonthly Remittance Return of Final Income Taxes Withheld: Kawanihan NG Rentas InternasAlfred BryanОценок пока нет

- Tax Reckoner 2021-22: Snapshot of Tax Rates Specific To Mutual FundsДокумент4 страницыTax Reckoner 2021-22: Snapshot of Tax Rates Specific To Mutual FundsApurva SinghiОценок пока нет

- PASSIVE INCOME Individual With CREATEДокумент2 страницыPASSIVE INCOME Individual With CREATERacelle FlorentinОценок пока нет

- Individuals Corporations RC NRC RA Nraetb Nranetb DC RFC NRFC 1. Interest IncomeДокумент1 страницаIndividuals Corporations RC NRC RA Nraetb Nranetb DC RFC NRFC 1. Interest IncomePaul Winston Mansing Alcala100% (1)

- TAX of PinalizeДокумент19 страницTAX of PinalizeDennis IsananОценок пока нет

- Income Taxation RatesДокумент2 страницыIncome Taxation RatesStephen ChuaОценок пока нет

- Passive income tax rates for individuals and corporationsДокумент1 страницаPassive income tax rates for individuals and corporationsFranz CampuedОценок пока нет

- Tax ReviewerДокумент11 страницTax Reviewerbertochristine10Оценок пока нет

- TAXATION OF CAPITAL GAINS AND PASSIVE INCOMEДокумент12 страницTAXATION OF CAPITAL GAINS AND PASSIVE INCOMELiyana ChuaОценок пока нет

- Philippine Tax Law Changes SummaryДокумент13 страницPhilippine Tax Law Changes SummarykeyelОценок пока нет

- Fit - Tax Table 2Документ4 страницыFit - Tax Table 2zipaganermy15Оценок пока нет

- Individual Income Tax NOTESДокумент1 страницаIndividual Income Tax NOTESNavsОценок пока нет

- Taxation-2 2Документ5 страницTaxation-2 2Yeshua Liebt PhoenixОценок пока нет

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesОт EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesОценок пока нет

- Physical Education Worksheet AssessmentsДокумент3 страницыPhysical Education Worksheet AssessmentsMichaela Janne VegigaОценок пока нет

- Erapol EHP95AДокумент2 страницыErapol EHP95AMohammad Doost MohammadiОценок пока нет

- Kertas Trial English Smka & Sabk K1 Set 2 2021Документ17 страницKertas Trial English Smka & Sabk K1 Set 2 2021Genius UnikОценок пока нет

- Q1 Tle 4 (Ict)Документ34 страницыQ1 Tle 4 (Ict)Jake Role GusiОценок пока нет

- 7 Surprising Cyberbullying StatisticsДокумент4 страницы7 Surprising Cyberbullying StatisticsJuby Ann Enconado100% (1)

- The Impact of StressДокумент3 страницыThe Impact of StressACabalIronedKryptonОценок пока нет

- Characteristics of Uveitis Presenting For The First Time in The Elderly Analysis of 91 Patients in A Tertiary CenterДокумент9 страницCharacteristics of Uveitis Presenting For The First Time in The Elderly Analysis of 91 Patients in A Tertiary CenterFrancescFranquesaОценок пока нет

- Insects, Stings and BitesДокумент5 страницInsects, Stings and BitesHans Alfonso ThioritzОценок пока нет

- Week 6 Blood and Tissue FlagellatesДокумент7 страницWeek 6 Blood and Tissue FlagellatesaemancarpioОценок пока нет

- The Danger of Microwave TechnologyДокумент16 страницThe Danger of Microwave Technologyrey_hadesОценок пока нет

- VIDEO 2 - Thì hiện tại tiếp diễn và hiện tại hoàn thànhДокумент3 страницыVIDEO 2 - Thì hiện tại tiếp diễn và hiện tại hoàn thànhÝ Nguyễn NhưОценок пока нет

- Catherineresume 2Документ3 страницыCatherineresume 2api-302133133Оценок пока нет

- OilДокумент8 страницOilwuacbekirОценок пока нет

- Genetically Engineered MicroorganismsДокумент6 страницGenetically Engineered Microorganismsaishwarya joshiОценок пока нет

- BIRADS Lexicon and Its Histopathological Corroboration in The Diagnosis of Breast LesionsДокумент7 страницBIRADS Lexicon and Its Histopathological Corroboration in The Diagnosis of Breast LesionsInternational Journal of Innovative Science and Research TechnologyОценок пока нет

- Li Ching Wing V Xuan Yi Xiong (2004) 1 HKC 353Документ11 страницLi Ching Wing V Xuan Yi Xiong (2004) 1 HKC 353hОценок пока нет

- Fluid Mechanics Sessional: Dhaka University of Engineering & Technology, GazipurДокумент17 страницFluid Mechanics Sessional: Dhaka University of Engineering & Technology, GazipurMd saydul islamОценок пока нет

- Thee Correlational Study of Possittive Emotionons and Coping Strategies For Academic Stress Among CASS Studentts - updaTEDДокумент23 страницыThee Correlational Study of Possittive Emotionons and Coping Strategies For Academic Stress Among CASS Studentts - updaTEDJuliet AcelОценок пока нет

- Very Easy Toeic Units 7 - 12 (Q1)Документ39 страницVery Easy Toeic Units 7 - 12 (Q1)Minh KhaiОценок пока нет

- Philippines implements external quality assessment for clinical labsДокумент2 страницыPhilippines implements external quality assessment for clinical labsKimberly PeranteОценок пока нет

- Perforamance Based AssessmentДокумент2 страницыPerforamance Based AssessmentJocelyn Acog Bisas MestizoОценок пока нет