Вам также может понравиться

- Accounting Case Study: PC DepotДокумент7 страницAccounting Case Study: PC DepotPutri Saffira YusufОценок пока нет

- 1 Lecture Notes DissolutionДокумент17 страниц1 Lecture Notes DissolutionMaybelle Espenido0% (2)

- 1 - Accounting For Partnership Firms - FundamentalsДокумент12 страниц1 - Accounting For Partnership Firms - FundamentalsAnkit RoyОценок пока нет

- Chapter 8: Admission of Partner: Rohit AgarwalДокумент3 страницыChapter 8: Admission of Partner: Rohit AgarwalbcomОценок пока нет

- 1271 XII Accountancy Study Material Supplementary Material HOTS and VBQ 2014 15 PDFДокумент380 страниц1271 XII Accountancy Study Material Supplementary Material HOTS and VBQ 2014 15 PDFBalaji TkpОценок пока нет

- Tally Model Question PaperДокумент2 страницыTally Model Question PaperMahaveer Choudhary100% (1)

- 4HANA Treasury and Risk ManagementДокумент50 страниц4HANA Treasury and Risk Managementsaigramesh100% (1)

- G1 6.4 Partnership - Amalgamation and Business PurchaseДокумент15 страницG1 6.4 Partnership - Amalgamation and Business Purchasesridhartks100% (2)

- 4 ACCT 2AB P. LiquidationДокумент11 страниц4 ACCT 2AB P. LiquidationMary Angeline Lopez100% (2)

- Accounting For Partnerships: Basic Considerations and FormationДокумент22 страницыAccounting For Partnerships: Basic Considerations and FormationAj CapungganОценок пока нет

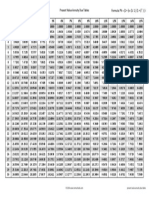

- Present Value Annuity Due TablesДокумент1 страницаPresent Value Annuity Due TablesDecereen Pineda Rodrigueza100% (2)

- ChartChampions LearningModulesДокумент370 страницChartChampions LearningModulesFaizan SawaniОценок пока нет

- Partnership Operations: Accounting Cycle of A PartnershipДокумент13 страницPartnership Operations: Accounting Cycle of A Partnershipred100% (1)

- Problems On Retained EarningsДокумент2 страницыProblems On Retained EarningsDecereen Pineda RodriguezaОценок пока нет

- Practical AccountingДокумент13 страницPractical AccountingDecereen Pineda RodriguezaОценок пока нет

- Unit V PartnershipДокумент11 страницUnit V PartnershipMUDITSAHANIОценок пока нет

- Partnership NotesДокумент10 страницPartnership NotesannabellОценок пока нет

- 2022 9 27 Q Merged - PagenumberДокумент11 страниц2022 9 27 Q Merged - PagenumberMike HKОценок пока нет

- Key Terms and Chapter Summary-3Документ3 страницыKey Terms and Chapter Summary-3AbhiОценок пока нет

- 20 Admission of PartnerДокумент12 страниц20 Admission of PartnerNadeem Manzoor100% (1)

- 23 PartnershiptheoryДокумент10 страниц23 PartnershiptheorySanjeev MiglaniОценок пока нет

- Fundamantal of Partnership PPT As On 21 12 2020Документ50 страницFundamantal of Partnership PPT As On 21 12 2020jeevan varma100% (1)

- Partnership Firms - Part5 Guarantee and Past AdjustmentДокумент15 страницPartnership Firms - Part5 Guarantee and Past AdjustmentDeepti BistОценок пока нет

- Admission of A PartnerДокумент4 страницыAdmission of A PartnerPainОценок пока нет

- 12 AccountancyДокумент4 страницы12 AccountancyAbhishek DhillonОценок пока нет

- AFAR - 1.0 Ul Cpa Review Center R.D.BalocatingДокумент18 страницAFAR - 1.0 Ul Cpa Review Center R.D.Balocatingfghhnnnjml100% (1)

- Key-Terms and Chapter Summary-5Документ3 страницыKey-Terms and Chapter Summary-5Sachin PalОценок пока нет

- 08 Financial Statements For PartnershipsДокумент15 страниц08 Financial Statements For PartnershipsBabamu Kalmoni JaatoОценок пока нет

- Profit & Loss Appropriation Account, Admission, Retirement and Death of A Partner, and Dissolution of A Partnership FirmДокумент10 страницProfit & Loss Appropriation Account, Admission, Retirement and Death of A Partner, and Dissolution of A Partnership Firmd-fbuser-65596417Оценок пока нет

- 3 Partnership AccountsДокумент93 страницы3 Partnership AccountsCA K D Purkayastha100% (1)

- Chapter 17Документ36 страницChapter 17metarereОценок пока нет

- ch2 Slides InstructorДокумент52 страницыch2 Slides Instructorakshitnagpal9119Оценок пока нет

- Ncert Solutions For Class 12 Accountancy 22 May Chapter 3 Reconstruction of A Partnership Firm Admission of A PartnerДокумент86 страницNcert Solutions For Class 12 Accountancy 22 May Chapter 3 Reconstruction of A Partnership Firm Admission of A PartnerHome Grown CreationОценок пока нет

- Chapter 6: Appropriation of Profits: Rohit AgarwalДокумент4 страницыChapter 6: Appropriation of Profits: Rohit AgarwalbcomОценок пока нет

- Accountancy ImpQ CH04 Admission of A Partner 01Документ18 страницAccountancy ImpQ CH04 Admission of A Partner 01praveentyagiОценок пока нет

- Reconstitution of A Partnership Firm-Admission of A PartnerДокумент6 страницReconstitution of A Partnership Firm-Admission of A PartnerKarthik ManikandanОценок пока нет

- Mediocre Non-Profit OrganizationДокумент12 страницMediocre Non-Profit OrganizationveenaОценок пока нет

- Changes in A PartnershipДокумент18 страницChanges in A PartnershipHadi HarizОценок пока нет

- Dissolution of PartnershipДокумент17 страницDissolution of PartnershipJASKARANОценок пока нет

- Chapter 4 Chapter 4 Retirement or Death of A Partner 1599071952606Документ10 страницChapter 4 Chapter 4 Retirement or Death of A Partner 1599071952606gyannibaba2007Оценок пока нет

- 12 Accountancy ImpQ CH05 Retirement and Death of A Partner 01Документ18 страниц12 Accountancy ImpQ CH05 Retirement and Death of A Partner 01praveentyagiОценок пока нет

- Lesson 2 Formation of PartnershipДокумент27 страницLesson 2 Formation of PartnershipheyheyОценок пока нет

- Advance Financial Accounting and Reporting 2 Notes CompressДокумент35 страницAdvance Financial Accounting and Reporting 2 Notes CompressthegreatОценок пока нет

- Partnership Operations P1Документ7 страницPartnership Operations P1Kyut KoОценок пока нет

- Chapter:1 Fundamentals: 1. Fixed and Fluctuating Capital AccountsДокумент98 страницChapter:1 Fundamentals: 1. Fixed and Fluctuating Capital Accountsashit_rasquinha100% (1)

- Must Do Content Accountancy Class XiiДокумент46 страницMust Do Content Accountancy Class XiiHigi SОценок пока нет

- Fundamentals of Accounting 2 Lesson 2 Partnership Formation StudentsДокумент17 страницFundamentals of Accounting 2 Lesson 2 Partnership Formation StudentsFhaye Lea BarroroОценок пока нет

- Accounting For Partnership - UnaДокумент13 страницAccounting For Partnership - UnaJastine Beltran - PerezОценок пока нет

- Accounting For Partnership FormationДокумент25 страницAccounting For Partnership FormationJOANNA ROSE MANALOОценок пока нет

- BODA Mid-TermДокумент2 страницыBODA Mid-TermISLAM KHALED ZSCОценок пока нет

- Amalgamation and Sale of FirmДокумент57 страницAmalgamation and Sale of FirmShrutika singhОценок пока нет

- Post Test. A12Документ5 страницPost Test. A12GICHA FEARL GIPALAОценок пока нет

- Partnership AccountsДокумент26 страницPartnership Accountsoneunique.1unqОценок пока нет

- Chapter 09 - Partnerships - Formation, Operatios, and Changes in Ownership InterestsДокумент53 страницыChapter 09 - Partnerships - Formation, Operatios, and Changes in Ownership Interestsgracerich20Оценок пока нет

- Module 1 - Partnership FormationДокумент25 страницModule 1 - Partnership FormationMaluDyОценок пока нет

- Chapter 15Документ16 страницChapter 15kylicia bestОценок пока нет

- Retiremnet of A Partner - Ashiq MohammedДокумент22 страницыRetiremnet of A Partner - Ashiq MohammedAshiq MohammedОценок пока нет

- SQE - Basic AccoДокумент111 страницSQE - Basic AccoCristinaОценок пока нет

- Partnership Dissolution and Liquidation - 497916619Документ4 страницыPartnership Dissolution and Liquidation - 497916619Carl Yry BitengОценок пока нет

- Handouts PartnershipДокумент9 страницHandouts PartnershipCPAОценок пока нет

- PartnershipДокумент5 страницPartnershipjohnОценок пока нет

- Principles of Accounts: Chapter 26: Goodwill Chapter 27: Admission of Partner/AmalgamationДокумент8 страницPrinciples of Accounts: Chapter 26: Goodwill Chapter 27: Admission of Partner/AmalgamationEphraim PryceОценок пока нет

- Part 1 Partnership BasicДокумент11 страницPart 1 Partnership BasicSagar YadavОценок пока нет

- Accounting For PartnershipsДокумент43 страницыAccounting For PartnershipsAqibОценок пока нет

- Chapter 5 Accounting For Merchandising OperationsДокумент15 страницChapter 5 Accounting For Merchandising OperationsDecereen Pineda RodriguezaОценок пока нет

- Extrinsic and Intrinsic Factors Influencing Employee Motivation: Lessons From AMREF Health Africa in KenyaДокумент12 страницExtrinsic and Intrinsic Factors Influencing Employee Motivation: Lessons From AMREF Health Africa in KenyaDecereen Pineda RodriguezaОценок пока нет

- PPEДокумент3 страницыPPEDecereen Pineda RodriguezaОценок пока нет

- Safe FoodДокумент45 страницSafe FoodDecereen Pineda RodriguezaОценок пока нет

- The Emergence of Consensus: A Primer: ReviewДокумент13 страницThe Emergence of Consensus: A Primer: ReviewDecereen Pineda RodriguezaОценок пока нет

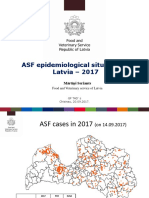

- African Swine Fever: Pesti Porcine Africaine, Peste Porcina Africana, Maladie de MontgomeryДокумент52 страницыAfrican Swine Fever: Pesti Porcine Africaine, Peste Porcina Africana, Maladie de MontgomeryDecereen Pineda Rodrigueza100% (1)

- Sge Asf8 - LatviaДокумент16 страницSge Asf8 - LatviaDecereen Pineda RodriguezaОценок пока нет

- Bersak CMS Thesis FINAL PDFДокумент71 страницаBersak CMS Thesis FINAL PDFDecereen Pineda RodriguezaОценок пока нет

- AdjectivesДокумент10 страницAdjectivesDecereen Pineda RodriguezaОценок пока нет

- Conflict Full TextДокумент392 страницыConflict Full TextAlvin PateresОценок пока нет

- Praktiker ThesisДокумент5 страницPraktiker Thesis1238912Оценок пока нет

- Unit IV Corporate Liquidation PDFДокумент20 страницUnit IV Corporate Liquidation PDFLeslie Mae Vargas ZafeОценок пока нет

- 2021 Problem MojakoeДокумент6 страниц2021 Problem Mojakoedara ibthiaОценок пока нет

- Periyar University: Periyar Palkalai Nagar SALEM - 636011Документ48 страницPeriyar University: Periyar Palkalai Nagar SALEM - 636011sureshkumarОценок пока нет

- Circular No. 38 /2016-Customs: - (1) Notwithstanding Anything Contained in This Act ButДокумент18 страницCircular No. 38 /2016-Customs: - (1) Notwithstanding Anything Contained in This Act ButAnshОценок пока нет

- Om Prakash ResumeДокумент3 страницыOm Prakash Resumeomprakashkarn1Оценок пока нет

- Campos Rueda & Co V Pacific Commercial (44 Phil 916) : Eluao vs. CasteelДокумент7 страницCampos Rueda & Co V Pacific Commercial (44 Phil 916) : Eluao vs. CasteelR-lheneFidelОценок пока нет

- Features of SBI Simply Save CardДокумент2 страницыFeatures of SBI Simply Save CardPradyumna CbОценок пока нет

- Tonka FinalДокумент16 страницTonka Finalআন নাফি100% (1)

- Member Data Record: Philippine Health Insurance CorporationДокумент1 страницаMember Data Record: Philippine Health Insurance CorporationJoseph EsperidaОценок пока нет

- Eco 407Документ4 страницыEco 407LUnweiОценок пока нет

- Vijay Kumar: GuptaДокумент63 страницыVijay Kumar: GuptaContra Value BetsОценок пока нет

- S3 The PTH of A Finaal MoДокумент18 страницS3 The PTH of A Finaal Mosuhasshinde88Оценок пока нет

- Beer, Bourbon, & BBQДокумент3 страницыBeer, Bourbon, & BBQSunlight FoundationОценок пока нет

- 32 1 PDFДокумент402 страницы32 1 PDFThompsonОценок пока нет

- Free Trade and Free ArtДокумент6 страницFree Trade and Free ArtJulian StallabrassОценок пока нет

- Solution Manual For Business Ethics 013142792xДокумент10 страницSolution Manual For Business Ethics 013142792xJamesNewmanjxag100% (38)

- Laporan Keuangan Tahunan HRUM 2021Документ123 страницыLaporan Keuangan Tahunan HRUM 2021Yayu Rahayu100% (1)

- (FINBUS2) (BUS-AC1) Financial Accounting 1 (Nov2013) v5Документ6 страниц(FINBUS2) (BUS-AC1) Financial Accounting 1 (Nov2013) v5mОценок пока нет

- Tata AIA Life Insurance Sampoorna Raksha Supreme TC 110N160V02Документ54 страницыTata AIA Life Insurance Sampoorna Raksha Supreme TC 110N160V02Aman GuptaОценок пока нет

- BEA Associates - Enhanced Equity Index FundДокумент17 страницBEA Associates - Enhanced Equity Index FundKunal MehtaОценок пока нет

- Keenan V Eshleman (Pagcaliwagan)Документ2 страницыKeenan V Eshleman (Pagcaliwagan)AlexandraSoledadОценок пока нет

- Landlord Tenant Frequently Asked Questions CLC 11 1Документ3 страницыLandlord Tenant Frequently Asked Questions CLC 11 1api-477465158Оценок пока нет

- 12.5 - Practice Test SolutionsДокумент15 страниц12.5 - Practice Test SolutionsCamilo ToroОценок пока нет

- Drivers & Dimensions of Market Globalization by Martinson T. YeboahДокумент37 страницDrivers & Dimensions of Market Globalization by Martinson T. YeboahMartinson Tenkorang Yeboah100% (4)