Вам также может понравиться

- Options Trading Strategies - Complete Guide To Getting Started and Making Money With Stock OptionsДокумент74 страницыOptions Trading Strategies - Complete Guide To Getting Started and Making Money With Stock OptionsshreekilambiОценок пока нет

- Equity Based CompensationДокумент20 страницEquity Based Compensationhimanshi100% (1)

- Exporting Services: A Developing Country PerspectiveОт EverandExporting Services: A Developing Country PerspectiveРейтинг: 5 из 5 звезд5/5 (2)

- Financials of Fleet Power Inc. 2020 - V2Документ53 страницыFinancials of Fleet Power Inc. 2020 - V2john markОценок пока нет

- Complete Guide To Container Freight DerivativesДокумент81 страницаComplete Guide To Container Freight Derivativesmaersk01Оценок пока нет

- Compund Financial Instrument - ProblemsДокумент3 страницыCompund Financial Instrument - ProblemsLouiseОценок пока нет

- Introduction To Real OptionsДокумент80 страницIntroduction To Real OptionsTito Feliciano100% (1)

- file ôn trắc nghiệm cuối kì 8 .vi.enДокумент38 страницfile ôn trắc nghiệm cuối kì 8 .vi.en2-Nguyễn Thị Lan Anh100% (2)

- Investments 8th Canadian Edition by Bodie Kane Marcus Perrakis Ryan Solution Manual DownloadДокумент8 страницInvestments 8th Canadian Edition by Bodie Kane Marcus Perrakis Ryan Solution Manual Downloadrausgolzaler100% (1)

- The Iron Condor Trading Guide: by Craig SeversonДокумент33 страницыThe Iron Condor Trading Guide: by Craig SeversonSekhar Muppuri50% (2)

- Using Economic Indicators to Improve Investment AnalysisОт EverandUsing Economic Indicators to Improve Investment AnalysisРейтинг: 3.5 из 5 звезд3.5/5 (1)

- AP.2808 - Audit of Equity MAY 2020: Auditing Problems Ocampo/Cabarles/Soliman/OcampoДокумент5 страницAP.2808 - Audit of Equity MAY 2020: Auditing Problems Ocampo/Cabarles/Soliman/OcampoMay Grethel Joy PeranteОценок пока нет

- Shareholder S Equity ReviewerДокумент20 страницShareholder S Equity ReviewerKarlovy DalinОценок пока нет

- SIP Report OldДокумент27 страницSIP Report OldAbhishek rajОценок пока нет

- Chap 60Документ3 страницыChap 60Vijay ManeОценок пока нет

- Private Equity InvestmentДокумент12 страницPrivate Equity InvestmentRishipal ChauhanОценок пока нет

- Mutual Fund Portfolio Insight Report: Mohit GuptaДокумент7 страницMutual Fund Portfolio Insight Report: Mohit GuptaMohit GuptaОценок пока нет

- Real Estate: Presented By: Mukesh Singh SauravДокумент13 страницReal Estate: Presented By: Mukesh Singh SauravSaurabh SagarОценок пока нет

- SRPM Economy Analysis - Group-7Документ58 страницSRPM Economy Analysis - Group-7hiitsds12bОценок пока нет

- NNNNN NNNNNNNNN NNNNNNNNNДокумент70 страницNNNNN NNNNNNNNN NNNNNNNNNSheheryar KhanОценок пока нет

- Real Estate: Nishant Kumar PGDM 09 JimlДокумент13 страницReal Estate: Nishant Kumar PGDM 09 Jimlpankaj09128Оценок пока нет

- Japonia & TurciaДокумент8 страницJaponia & Turciabiancaftw90Оценок пока нет

- MD & Ceo CFO CRO CIO: Note For Investment Operation CommitteeДокумент4 страницыMD & Ceo CFO CRO CIO: Note For Investment Operation CommitteeAyushi somaniОценок пока нет

- IREF V 6 Pager Brochure - X UnitsДокумент6 страницIREF V 6 Pager Brochure - X UnitsPushpa DeviОценок пока нет

- 'KQHK NhikoyhДокумент12 страниц'KQHK NhikoyhGiri BabaОценок пока нет

- IREF V 6 Pager Brochure - Regular UnitsДокумент6 страницIREF V 6 Pager Brochure - Regular UnitsPushpa DeviОценок пока нет

- Chap 62Документ2 страницыChap 62api-19641717Оценок пока нет

- BD FinanceДокумент5 страницBD Financesibgat ullahОценок пока нет

- India: Asia-Pacific'S Next Mutual Funds Giant: Markets and Securities Services - 1Документ10 страницIndia: Asia-Pacific'S Next Mutual Funds Giant: Markets and Securities Services - 1EdifyОценок пока нет

- Aug-2010-Citi Indonesia ConferenceДокумент67 страницAug-2010-Citi Indonesia ConferenceFatchul WachidОценок пока нет

- Nitori Analyst ReportДокумент7 страницNitori Analyst ReportAhmad HaikalОценок пока нет

- The Philippine Stock Exchange, Inc.: February 26, 2021Документ212 страницThe Philippine Stock Exchange, Inc.: February 26, 2021Algen Lyn MendozaОценок пока нет

- DDW 20201105 PDFДокумент1 страницаDDW 20201105 PDFVimal SharmaОценок пока нет

- Monthly Bulletin July 2023 EnglishДокумент13 страницMonthly Bulletin July 2023 EnglishNirmal MenonОценок пока нет

- Government Domestic Borrowing: Monthly Report OnДокумент8 страницGovernment Domestic Borrowing: Monthly Report Onrashedul islamОценок пока нет

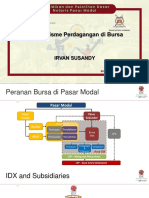

- Materi Mekanisme Perdagangan LMKA Nov 2020 - BPK IrvanДокумент29 страницMateri Mekanisme Perdagangan LMKA Nov 2020 - BPK IrvannurlisaОценок пока нет

- Debt 3Документ16 страницDebt 3mohsin.usafzai932Оценок пока нет

- January 21, 2022: Press ReleaseДокумент2 страницыJanuary 21, 2022: Press ReleaseAayush GuptaОценок пока нет

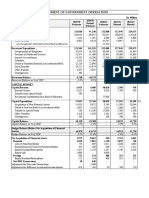

- Statement of Government Operations: O/w Exceptional Contribution From Bank of Mauritius 33,000Документ2 страницыStatement of Government Operations: O/w Exceptional Contribution From Bank of Mauritius 33,000Yashas SridatОценок пока нет

- India Grid Q3FY18 - Result Update - Axis Direct - 22012018 - 22!01!2018 - 14Документ5 страницIndia Grid Q3FY18 - Result Update - Axis Direct - 22012018 - 22!01!2018 - 14saransh saranshОценок пока нет

- Portfolio Management: Assortment of Investments Options To Enhance Portfolio ValueДокумент24 страницыPortfolio Management: Assortment of Investments Options To Enhance Portfolio Valuechintan shahОценок пока нет

- PT Nusantara Infrastructure TBK: Draft 1 (For Discussion)Документ6 страницPT Nusantara Infrastructure TBK: Draft 1 (For Discussion)Cindy CinintyaОценок пока нет

- Iiww 031210Документ4 страницыIiww 0312109913004606Оценок пока нет

- 0315富邦年報 - 英文.indd 1 2021/5/17 下午 02:54:09Документ32 страницы0315富邦年報 - 英文.indd 1 2021/5/17 下午 02:54:09YudyChenОценок пока нет

- DEL L&T Infrastructure BondДокумент3 страницыDEL L&T Infrastructure Bondpoly899Оценок пока нет

- Indian Mutual Fund IndustryДокумент25 страницIndian Mutual Fund Industryravijha_1984Оценок пока нет

- 5e7d86f900475 2019 BPI Audited FS CompressedДокумент125 страниц5e7d86f900475 2019 BPI Audited FS CompressedHannah Brynne UrreraОценок пока нет

- Current State of Japanese Business in IndiaДокумент13 страницCurrent State of Japanese Business in IndiaPayal KathiawadiОценок пока нет

- Wipro Limited: Investor PresentationДокумент22 страницыWipro Limited: Investor PresentationKaveri PandeyОценок пока нет

- IapmДокумент6 страницIapmvishalsingh9669Оценок пока нет

- Wipro Limited: Investor PresentationДокумент22 страницыWipro Limited: Investor Presentationashokdb2kОценок пока нет

- Indian Stock MarketsДокумент13 страницIndian Stock Marketsmr.avdheshsharmaОценок пока нет

- List of Content: FINANCIAL STATEMENT - Asat30September2010 (Unaudited)Документ17 страницList of Content: FINANCIAL STATEMENT - Asat30September2010 (Unaudited)Aziz MuhammadОценок пока нет

- Infra Bonds FAQs PDFДокумент3 страницыInfra Bonds FAQs PDFAnshuman SharmaОценок пока нет

- Debt Bulletin-Govt. of The PunjabДокумент4 страницыDebt Bulletin-Govt. of The PunjabSaqib JoyiaОценок пока нет

- Investor Presentation FY13 v1Документ16 страницInvestor Presentation FY13 v1Shakti ShuklaОценок пока нет

- Indonesia: The Delta Variant and Lagging Vaccination Have Set Back The RecoveryДокумент4 страницыIndonesia: The Delta Variant and Lagging Vaccination Have Set Back The RecoveryTopan ArdiansyahОценок пока нет

- Data SheetДокумент3 страницыData SheetAmey SawantОценок пока нет

- Saad - IFДокумент5 страницSaad - IFRidwan KabirОценок пока нет

- Ptmail m1219 Ss Two Stock Special Report PDFДокумент18 страницPtmail m1219 Ss Two Stock Special Report PDFAaron MartinОценок пока нет

- BS Delhi English 22-10-2022Документ26 страницBS Delhi English 22-10-2022Relaxing MusicОценок пока нет

- Zee Entertainment SELL (Recommendation Downgrade) 20240122Документ13 страницZee Entertainment SELL (Recommendation Downgrade) 20240122Rohan KhannaОценок пока нет

- Role of FII in INDIAN Capital Market: Presented By: Sanketh Shetty HarishДокумент35 страницRole of FII in INDIAN Capital Market: Presented By: Sanketh Shetty HarishHarish ShettyОценок пока нет

- Strategic Financial Analysis of Diversified and Undiversified CompanyДокумент15 страницStrategic Financial Analysis of Diversified and Undiversified CompanyarunprakaashОценок пока нет

- Analyst PPT De9 PDFДокумент65 страницAnalyst PPT De9 PDFAmit GagraniОценок пока нет

- INDIA@2030 Presentation - M.D. PaiДокумент33 страницыINDIA@2030 Presentation - M.D. Paimannugupta123Оценок пока нет

- Credit Risk - JPM Case Study IIM KДокумент8 страницCredit Risk - JPM Case Study IIM KSourabh Agrawal 23Оценок пока нет

- Globalising Cost of Capital Cap Budgeting Case - Akash LodhaДокумент78 страницGlobalising Cost of Capital Cap Budgeting Case - Akash LodhaKushal AdaniОценок пока нет

- Wipro Investor PPT q4 Fy 2022Документ22 страницыWipro Investor PPT q4 Fy 2022sri KarthikeyanОценок пока нет

- Ystematic Nvestment Lan UTI: An Early & Regular Investment Today, Leads To Prosperous TomorrowДокумент26 страницYstematic Nvestment Lan UTI: An Early & Regular Investment Today, Leads To Prosperous Tomorrown_akash3977Оценок пока нет

- BCG CaseДокумент2 страницыBCG Caseorigami87Оценок пока нет

- Market Internal WeeklyДокумент15 страницMarket Internal WeeklyDavid YANGОценок пока нет

- Kahema - Investor Protection in Kenya An Exposition Into The Legal Regime andДокумент89 страницKahema - Investor Protection in Kenya An Exposition Into The Legal Regime andSAMUEL KIMANIОценок пока нет

- Presentation On Functions of Future ContractДокумент10 страницPresentation On Functions of Future ContractSusweta SarkarОценок пока нет

- I.L.L. Research Paper by Thy and MariyaДокумент9 страницI.L.L. Research Paper by Thy and MariyaPrem ChopraОценок пока нет

- Ticker: CTM AU Cash 3Q20: US$27m Project: Jaguar Market Cap: A$200m Price: A$0.615/sh Country: BrazilДокумент5 страницTicker: CTM AU Cash 3Q20: US$27m Project: Jaguar Market Cap: A$200m Price: A$0.615/sh Country: BraziltomОценок пока нет

- Chapter 5 - Currency Derivatives - Currency Forward and FuturesДокумент73 страницыChapter 5 - Currency Derivatives - Currency Forward and Futuresธชพร พรหมสีดาОценок пока нет

- Maya Meidias P - 01017190005 - Chapter 22Документ5 страницMaya Meidias P - 01017190005 - Chapter 22Kinas AnugrahaningОценок пока нет

- Coupon 21.4% P.A. 3 Months EUR Barrier at 80%: Single Barrier Reverse Convertible On DEUTSCHE BANK AG-REGISTEREDДокумент1 страницаCoupon 21.4% P.A. 3 Months EUR Barrier at 80%: Single Barrier Reverse Convertible On DEUTSCHE BANK AG-REGISTEREDapi-25890856Оценок пока нет

- Forwards and Futures: Futures Exchanges in China, India, and Ethiopia, and E-Choupal in Village IndiaДокумент26 страницForwards and Futures: Futures Exchanges in China, India, and Ethiopia, and E-Choupal in Village IndiaMuhammad AliОценок пока нет

- Requirements:: Intermediate Accounting 3Документ7 страницRequirements:: Intermediate Accounting 3happy240823Оценок пока нет

- Islamic Derivatives 2Документ19 страницIslamic Derivatives 2syedtahaaliОценок пока нет

- Introduction To DerivativesДокумент35 страницIntroduction To DerivativesNukaraju_marojuОценок пока нет

- On January 1 2017 Frederiksen Inc S Stockholders Equity Category AppearedДокумент1 страницаOn January 1 2017 Frederiksen Inc S Stockholders Equity Category AppearedMiroslav GegoskiОценок пока нет

- Chapter 10 Futures Arbitrate Strategies Test BankДокумент6 страницChapter 10 Futures Arbitrate Strategies Test BankJocelyn TanОценок пока нет

- SOA Exam FM SyllabusДокумент6 страницSOA Exam FM Syllabuscrackjak4129Оценок пока нет

- Paper: 08, International Business Operations: ManagementДокумент14 страницPaper: 08, International Business Operations: ManagementMonika SainiОценок пока нет

- Mutual FundДокумент13 страницMutual FundYeshwanth KumarОценок пока нет

- Annex 25 Using T2S For Transaction Management PDFДокумент46 страницAnnex 25 Using T2S For Transaction Management PDFteriyaadienОценок пока нет