Вам также может понравиться

- Business Tax DeductionsДокумент4 страницыBusiness Tax DeductionsGab VillahermosaОценок пока нет

- A BEGINNER'S GUIDE TO SELLING ON AMAZON.INДокумент17 страницA BEGINNER'S GUIDE TO SELLING ON AMAZON.INSanthoshini BhaskaranОценок пока нет

- Basic Hints For GSTДокумент42 страницыBasic Hints For GSTReeni SamuelОценок пока нет

- The Easy Guide To: The Goods and Services or Harmonized Sales Tax (GST/HST)Документ10 страницThe Easy Guide To: The Goods and Services or Harmonized Sales Tax (GST/HST)hellkatОценок пока нет

- Input Tax CreditДокумент8 страницInput Tax CreditPranjal AgrawalОценок пока нет

- GST Accounting Entries in Tally - Sales and PurchasesДокумент39 страницGST Accounting Entries in Tally - Sales and PurchasesNeelu100% (1)

- Goods and Services Tax (GST) KnowledgeДокумент8 страницGoods and Services Tax (GST) KnowledgeJaspreetSinghОценок пока нет

- India GST For Beginners - Jayaram HiregangeДокумент224 страницыIndia GST For Beginners - Jayaram Hiregangesatya1947Оценок пока нет

- GST Accounting Entries in TallyДокумент16 страницGST Accounting Entries in TallyRevathi naiduОценок пока нет

- Loan Agreement DetailsДокумент2 страницыLoan Agreement DetailsJameson Uy100% (1)

- Husband Filing Divorce PetitionДокумент2 страницыHusband Filing Divorce PetitionRaj KumarОценок пока нет

- Delpher Trades Corp. v. IAC ruling on alter ego statusДокумент2 страницыDelpher Trades Corp. v. IAC ruling on alter ego statusBingoheartОценок пока нет

- TAX Setup in FusionДокумент109 страницTAX Setup in FusionObulareddy BiyyamОценок пока нет

- Noncircumvention AgreementДокумент4 страницыNoncircumvention AgreementahelabbasОценок пока нет

- Apelanio vs. ArcanysДокумент2 страницыApelanio vs. ArcanysEmir Mendoza100% (3)

- Case Title - in Re - Resolution Dated August 14, 2013 of The Court of Appeals in CДокумент2 страницыCase Title - in Re - Resolution Dated August 14, 2013 of The Court of Appeals in Cnichols greenОценок пока нет

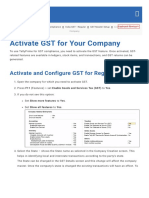

- Activating GST For Your CompanyДокумент158 страницActivating GST For Your CompanyTapas GhoshОценок пока нет

- gstДокумент48 страницgstlusifer kpОценок пока нет

- Department of Commerce Islamia University BahawalpurДокумент1 страницаDepartment of Commerce Islamia University Bahawalpursammar_iubОценок пока нет

- GST BasicsДокумент11 страницGST Basicssowjanya kandukuriОценок пока нет

- India-Gst-Activate-Gst-For-Your-Company-Tally (Sscstudy - Com) - 2Документ6 страницIndia-Gst-Activate-Gst-For-Your-Company-Tally (Sscstudy - Com) - 2Deepak MalusareОценок пока нет

- Compulsory Registration: RequirementДокумент4 страницыCompulsory Registration: RequirementNur Iszyani PoadОценок пока нет

- Research Paper On Service Tax in IndiaДокумент6 страницResearch Paper On Service Tax in Indiaoqphebaod100% (1)

- GST Tax Code ReferenceДокумент7 страницGST Tax Code ReferenceJohn BrittoОценок пока нет

- Summer Training Report on GST and Accounting ServicesДокумент48 страницSummer Training Report on GST and Accounting ServicesRishabh DevОценок пока нет

- TAX CODES AND THEIR USES IN MYOBДокумент4 страницыTAX CODES AND THEIR USES IN MYOBZarina VillagenОценок пока нет

- GST Sales Invoice Creation FormatДокумент10 страницGST Sales Invoice Creation Formatjaffer shadikОценок пока нет

- GST Good Sex Tonight: Input CreditДокумент23 страницыGST Good Sex Tonight: Input CreditaltmashОценок пока нет

- Excise Duty: and Distribution (SD), and Posts Them in Financial Accounting (FI)Документ6 страницExcise Duty: and Distribution (SD), and Posts Them in Financial Accounting (FI)Tuhin DuttaОценок пока нет

- Ir546 2022Документ20 страницIr546 2022KayОценок пока нет

- Ir 1022Документ2 страницыIr 1022jjruttiОценок пока нет

- Taxation IiДокумент60 страницTaxation IiAnkush GuptaОценок пока нет

- Exam Practice ReviewДокумент9 страницExam Practice ReviewSafi NurulОценок пока нет

- Goods and Services Tax (GST)Документ42 страницыGoods and Services Tax (GST)Aditi BagadeОценок пока нет

- VAT vs GST: Key Differences Between Value Added Tax and Goods and Services TaxДокумент7 страницVAT vs GST: Key Differences Between Value Added Tax and Goods and Services TaxArundhuti RoyОценок пока нет

- Sell+on+Amazon Beginner's Guide E BookДокумент17 страницSell+on+Amazon Beginner's Guide E Bookkri satОценок пока нет

- A BEGINNER'S GUIDE TO SELLING ON AMAZON.INДокумент17 страницA BEGINNER'S GUIDE TO SELLING ON AMAZON.INVenkat GopuОценок пока нет

- Sell+on+Amazon Beginner's Guide E BookДокумент17 страницSell+on+Amazon Beginner's Guide E Bookkamal vithlaniОценок пока нет

- GST Vs VATДокумент4 страницыGST Vs VATahil XO1BDОценок пока нет

- Thesis On Goods and Service TaxДокумент5 страницThesis On Goods and Service TaxRobin Beregovska100% (1)

- Guide to Assets and Depreciation 2014Документ16 страницGuide to Assets and Depreciation 2014Muhedin HussenОценок пока нет

- Input Tax Credit BasicsДокумент16 страницInput Tax Credit BasicsPreeti SapkalОценок пока нет

- CHAPTER 8 Business Activity Statements and Instalment Activity StatementsДокумент25 страницCHAPTER 8 Business Activity Statements and Instalment Activity StatementsCJОценок пока нет

- Chapter 1: Introduction To GST 1.1 Basics of GST 1.1.1 What Is GST?Документ13 страницChapter 1: Introduction To GST 1.1 Basics of GST 1.1.1 What Is GST?Ashutosh papelОценок пока нет

- Understanding and Using Quick Books Tax CodesДокумент6 страницUnderstanding and Using Quick Books Tax CodesColin GoudieОценок пока нет

- Guidance Note On Book-KeepingДокумент15 страницGuidance Note On Book-Keeping201CO021 JESSY SAINICA.WОценок пока нет

- Lead Your Firm To Success in The GST SystemДокумент16 страницLead Your Firm To Success in The GST SystemTrinetra AgarwalОценок пока нет

- Input Tax CreditДокумент5 страницInput Tax CreditSowmya GuptaОценок пока нет

- Solutions For GST Question BankДокумент55 страницSolutions For GST Question BankVarun VardhanОценок пока нет

- GST in India: A Comprehensive Guide BookДокумент77 страницGST in India: A Comprehensive Guide Bookgaurav dhallОценок пока нет

- 1) How Income Tax Works in India?: GST Is One of The Biggest Indirect Tax Reforms in The CountryДокумент21 страница1) How Income Tax Works in India?: GST Is One of The Biggest Indirect Tax Reforms in The Countryaher unnatiОценок пока нет

- DIT - Input Tax CreditДокумент10 страницDIT - Input Tax CreditDev ChhatbarОценок пока нет

- About Goods and Services Tax (GST) for Amazon Business - Amazon Customer ServiceДокумент2 страницыAbout Goods and Services Tax (GST) for Amazon Business - Amazon Customer Servicejoystocks777Оценок пока нет

- Suraj Sir 1Документ8 страницSuraj Sir 1Avinash YadavОценок пока нет

- GST For Layman A Book For Non Tax Professionals Read GST Like AДокумент89 страницGST For Layman A Book For Non Tax Professionals Read GST Like Adeys01inОценок пока нет

- Goods and Service TaxДокумент12 страницGoods and Service Taxshourima mishraОценок пока нет

- GT Singapore GST Reverse Charge January 2020 1571421370Документ2 страницыGT Singapore GST Reverse Charge January 2020 1571421370JORGESHSSОценок пока нет

- Untitled DocumentДокумент8 страницUntitled DocumentKr Ish NaОценок пока нет

- GST Definition, Types, Registration Process Bajaj Finance 2Документ1 страницаGST Definition, Types, Registration Process Bajaj Finance 2Raman PalОценок пока нет

- The First Level of Differentiation Will Come in Depending On Whether The Industry Deals With Manufacturing, Distributing and Retailing or Is Providing A ServiceДокумент13 страницThe First Level of Differentiation Will Come in Depending On Whether The Industry Deals With Manufacturing, Distributing and Retailing or Is Providing A ServiceMansi jainОценок пока нет

- 012 Terms and phrases you must know under GST- Part IДокумент3 страницы012 Terms and phrases you must know under GST- Part I0amrevkapeed0Оценок пока нет

- E-Book On GST by CA. (DR.) G. S. Grewal - 2020Документ58 страницE-Book On GST by CA. (DR.) G. S. Grewal - 2020Aarav DhingraОценок пока нет

- Who Should Register For GST?Документ9 страницWho Should Register For GST?Gitu SinghОценок пока нет

- Deductions GuideДокумент16 страницDeductions GuidehellkatОценок пока нет

- Taxation ScriptДокумент3 страницыTaxation ScriptReeni SamuelОценок пока нет

- Concepcion V CA GR 123450, August 31, 2005Документ2 страницыConcepcion V CA GR 123450, August 31, 2005Elvis Jagger Abdul JabharОценок пока нет

- Interim Order - Goldmine Agro LimitedДокумент15 страницInterim Order - Goldmine Agro LimitedShyam SunderОценок пока нет

- February 1, 2017 G.R. No. 188146 Pilipinas Shell Petroleum Corporation, Petitioner Royal Ferry Services, Inc., Respondent Decision Leonen, J.Документ13 страницFebruary 1, 2017 G.R. No. 188146 Pilipinas Shell Petroleum Corporation, Petitioner Royal Ferry Services, Inc., Respondent Decision Leonen, J.Graile Dela CruzОценок пока нет

- USArmy InternmentResettlementДокумент326 страницUSArmy InternmentResettlementCharlesОценок пока нет

- Week 14 NegoДокумент13 страницWeek 14 NegoyassercarlomanОценок пока нет

- Complaint Against MEPCO Zahir PirДокумент3 страницыComplaint Against MEPCO Zahir PirarhijaziОценок пока нет

- 2SR Transpo ReyesДокумент5 страниц2SR Transpo ReyesRikka ReyesОценок пока нет

- Tilaknagar DRHP PDFДокумент221 страницаTilaknagar DRHP PDFsusegaadОценок пока нет

- Mactan ChiongbianДокумент3 страницыMactan ChiongbianJohn Dexter FuentesОценок пока нет

- The Enemy at The Gates: International Borders, Migration and Human RightsДокумент18 страницThe Enemy at The Gates: International Borders, Migration and Human RightsTatia LomtadzeОценок пока нет

- VakalatnamaДокумент1 страницаVakalatnamaAadil KhanОценок пока нет

- Pp. 7 CrimДокумент143 страницыPp. 7 CrimgleeОценок пока нет

- In Re CulanagДокумент8 страницIn Re CulanagGerry DayananОценок пока нет

- Differences between arbitration and mediationДокумент11 страницDifferences between arbitration and mediationRollyn Dee De Marco PiocosОценок пока нет

- CHAPTER - 4 (Working of Institution)Документ2 страницыCHAPTER - 4 (Working of Institution)Kunal BalyanОценок пока нет

- 190-1 Settlement Agreement and ReleaseДокумент57 страниц190-1 Settlement Agreement and ReleaseFair Punishment ProjectОценок пока нет

- Contract Law - The Performance of An Existing Duty Amounts To Valid Consideration To Enable Enforcement of A PromiseДокумент2 страницыContract Law - The Performance of An Existing Duty Amounts To Valid Consideration To Enable Enforcement of A PromiseSultan MughalОценок пока нет

- Bautista vs. UnangstДокумент21 страницаBautista vs. UnangstKim BarriosОценок пока нет

- Life During Martial LawДокумент8 страницLife During Martial LawLou GatocОценок пока нет

- Dayabhai Chaganbhai Thakkar V State of Gujarat AIR 1964 SC 1563Документ26 страницDayabhai Chaganbhai Thakkar V State of Gujarat AIR 1964 SC 1563Arihant RoyОценок пока нет

- Powell Conditions of ReleaseДокумент3 страницыPowell Conditions of ReleasegramabozoОценок пока нет

- TESDA DPA Manual ApprovedДокумент3 страницыTESDA DPA Manual ApprovedBimbo GilleraОценок пока нет

- Certified List of Candidates For Congressional and Local Positions For The May 13, 2013 2013 National, Local and Armm ElectionsДокумент2 страницыCertified List of Candidates For Congressional and Local Positions For The May 13, 2013 2013 National, Local and Armm ElectionsSunStar Philippine NewsОценок пока нет

- The Law of ConfessionДокумент34 страницыThe Law of ConfessionMayank Jain63% (8)