Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Solo ParentДокумент1 страницаSolo ParentA Paula Cruz FranciscoОценок пока нет

- Example of JargonsДокумент1 страницаExample of JargonsA Paula Cruz FranciscoОценок пока нет

- Affidavit-of-Loss - MarvinДокумент1 страницаAffidavit-of-Loss - MarvinA Paula Cruz FranciscoОценок пока нет

- Atm AffidavitДокумент2 страницыAtm AffidavitA Paula Cruz FranciscoОценок пока нет

- Borad of TrusteesДокумент1 страницаBorad of TrusteesA Paula Cruz FranciscoОценок пока нет

- Us VS LudeyДокумент2 страницыUs VS LudeyA Paula Cruz FranciscoОценок пока нет

- Human Rights CasesДокумент84 страницыHuman Rights CasesA Paula Cruz FranciscoОценок пока нет

- WillsДокумент11 страницWillsA Paula Cruz FranciscoОценок пока нет

- Case No. 21 Qua Chee Gan Vs Law Union and Rock Insurance CoДокумент2 страницыCase No. 21 Qua Chee Gan Vs Law Union and Rock Insurance CoA Paula Cruz FranciscoОценок пока нет

- MHP Garments Vs C, Puno. C, JДокумент5 страницMHP Garments Vs C, Puno. C, JA Paula Cruz FranciscoОценок пока нет

- E. 20 Duyag vs. InciongДокумент2 страницыE. 20 Duyag vs. InciongA Paula Cruz FranciscoОценок пока нет

- Mindanao Shopping V DuterteДокумент2 страницыMindanao Shopping V DutertefcnrrsОценок пока нет

- No 14 - The Late Lino Gutierrez V Collector of Internal RevenueДокумент2 страницыNo 14 - The Late Lino Gutierrez V Collector of Internal RevenueA Paula Cruz FranciscoОценок пока нет

- Hydro Resources vs. CAДокумент1 страницаHydro Resources vs. CAA Paula Cruz FranciscoОценок пока нет

- Articles of IncorporationДокумент6 страницArticles of IncorporationA Paula Cruz FranciscoОценок пока нет

- Acme Shoes Vs CAДокумент15 страницAcme Shoes Vs CAA Paula Cruz FranciscoОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Cost Engineering YasichalewДокумент220 страницCost Engineering YasichalewYasichalew sefineh0% (1)

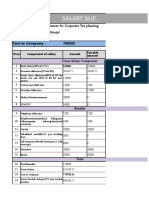

- Salary Slip: Submitted As Part of Assignment For Corporate Tax Planning Student Name: Vaibhav Gunjal Roll No: P81117Документ5 страницSalary Slip: Submitted As Part of Assignment For Corporate Tax Planning Student Name: Vaibhav Gunjal Roll No: P81117D'quorОценок пока нет

- InsurTech & Insurance DistributionДокумент18 страницInsurTech & Insurance DistributionChristian Phan100% (1)

- Independent Contractor Employer Statutory Approaches To Worker ClassificationДокумент17 страницIndependent Contractor Employer Statutory Approaches To Worker ClassificationNational Association of REALTORS®Оценок пока нет

- Cs M.K. PandeyДокумент40 страницCs M.K. PandeySam DanielОценок пока нет

- Drug Supply ManagementДокумент15 страницDrug Supply Managementnasibdin100% (2)

- Metamorphosis of Modern Management - Financial ServicesДокумент12 страницMetamorphosis of Modern Management - Financial ServicesSiva BalajiОценок пока нет

- Enq-2333 - Tender Resume Crpo 125 & 126 Offshore FacilitiesДокумент8 страницEnq-2333 - Tender Resume Crpo 125 & 126 Offshore FacilitiesNIRBHAY TIWARYОценок пока нет

- Icici Lombard Health Care Insurance Claim FormДокумент5 страницIcici Lombard Health Care Insurance Claim FormsperoОценок пока нет

- Car Loan ProposalДокумент6 страницCar Loan ProposalRolly Acuna100% (3)

- FY2024 Proposed BudgetДокумент17 страницFY2024 Proposed BudgetArif EWSОценок пока нет

- MoaДокумент11 страницMoaanon_192297004Оценок пока нет

- Brief Scope of Work:: Greenesol Power Services PVT Ltd.,/Boiler/ENQ/SanghiДокумент8 страницBrief Scope of Work:: Greenesol Power Services PVT Ltd.,/Boiler/ENQ/SanghiJKKОценок пока нет

- Scoot Conditions of Carriage FinalДокумент28 страницScoot Conditions of Carriage FinalRenuga I. KuppusamyОценок пока нет

- Mastering MintДокумент112 страницMastering MintMichelle CrawfordОценок пока нет

- Final Sip KunalДокумент62 страницыFinal Sip KunalVishwas DeveeraОценок пока нет

- Pavilion Rental AgreementДокумент5 страницPavilion Rental AgreementJ. Daniel SpratlinОценок пока нет

- ResumeДокумент4 страницыResumeSumit KumarОценок пока нет

- Adjudicators ContractДокумент3 страницыAdjudicators ContractBRGRОценок пока нет

- AbhinavДокумент3 страницыAbhinavpraveen kumarОценок пока нет

- Tatyana PCM Study Guide PDFДокумент19 страницTatyana PCM Study Guide PDFComfort Pinkney100% (2)

- Song Agreement - Damitha Ayodya - Re Sanda Paya-Theekshana Anuradha - 25052017...Документ2 страницыSong Agreement - Damitha Ayodya - Re Sanda Paya-Theekshana Anuradha - 25052017...Charitha WeerasooriyaОценок пока нет

- Earthwatch Field Grant Budget TemplateДокумент8 страницEarthwatch Field Grant Budget TemplatetoddopoliОценок пока нет

- Proposal Form - Householders Insurance PolicyДокумент4 страницыProposal Form - Householders Insurance PolicyscribdОценок пока нет

- O'gilvie Et Al., Minors v. United StatesДокумент1 страницаO'gilvie Et Al., Minors v. United StatesVel JuneОценок пока нет

- Torts Case Digest Baliwag V CAДокумент1 страницаTorts Case Digest Baliwag V CAKristine Joy TumbagaОценок пока нет

- MERS Electronic Tracking Agreement Whole Loan Template v6Документ16 страницMERS Electronic Tracking Agreement Whole Loan Template v6Tim BryantОценок пока нет

- Agent/ Intermediary Name and Code:BABU RAO CHILAKALAPUDI POS0000064Документ2 страницыAgent/ Intermediary Name and Code:BABU RAO CHILAKALAPUDI POS0000064seshu 2010Оценок пока нет

- Small Business Presentation For HAULДокумент23 страницыSmall Business Presentation For HAULErin McClartyОценок пока нет

- FNA - Product Mapping - Individual - Corporate - Hot Product - June 2020Документ1 страницаFNA - Product Mapping - Individual - Corporate - Hot Product - June 2020Steven CW CheungОценок пока нет