Вам также может понравиться

- Internal Control of Fixed Assets: A Controller and Auditor's GuideОт EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideРейтинг: 4 из 5 звезд4/5 (1)

- Consolidation Theories, Push-Down Accounting, and Corporate Joint VenturesДокумент23 страницыConsolidation Theories, Push-Down Accounting, and Corporate Joint Venturesmd salehinОценок пока нет

- Chp11 PDFДокумент23 страницыChp11 PDFYosua SihombingОценок пока нет

- Venture Capital Valuation, + Website: Case Studies and MethodologyОт EverandVenture Capital Valuation, + Website: Case Studies and MethodologyОценок пока нет

- Ch11 Beams12ge SMДокумент28 страницCh11 Beams12ge SMKharisma Pardede33% (3)

- Consolidation Theories, Push-Down Accounting, and Corporate Joint VenturesДокумент28 страницConsolidation Theories, Push-Down Accounting, and Corporate Joint VenturesRiska Azahra NОценок пока нет

- Advanced Accounting Beams 12th Edition Solutions ManualДокумент24 страницыAdvanced Accounting Beams 12th Edition Solutions ManualMariaDaviesqrbg100% (49)

- B. Woods Chapter 11Документ24 страницыB. Woods Chapter 11Esmeraldo Ebenezer SimalangoОценок пока нет

- SMCH 11 BeamsДокумент25 страницSMCH 11 BeamsAtika DaretyОценок пока нет

- Proformaquestionspart 1Документ3 страницыProformaquestionspart 1Kevser BozoğluОценок пока нет

- Chapter 3Документ73 страницыChapter 3Mark Arceo0% (1)

- ValuationДокумент20 страницValuationNirmal ShresthaОценок пока нет

- Online Ass Advance Acc NEWДокумент6 страницOnline Ass Advance Acc NEWRara Rarara30Оценок пока нет

- ACC 113 Module 7 AnswerДокумент4 страницыACC 113 Module 7 AnswerYahlianah Lee100% (2)

- ACC2001 Lecture 10 Interco TransactionsДокумент42 страницыACC2001 Lecture 10 Interco Transactionsmichael krueseiОценок пока нет

- Slide AKT 308 AKL 1Документ92 страницыSlide AKT 308 AKL 1Steve IdnОценок пока нет

- AFA 4e PPT Chap04Документ70 страницAFA 4e PPT Chap04فهد التويجريОценок пока нет

- Chapter 2 Separate and Consolidated FS - Date of AcquisitionДокумент21 страницаChapter 2 Separate and Consolidated FS - Date of AcquisitioneiaОценок пока нет

- Direct Non ControllingДокумент24 страницыDirect Non ControllingJamie ZhangОценок пока нет

- How A Private Equity Deal WorksДокумент2 страницыHow A Private Equity Deal Worksdarthvader79Оценок пока нет

- Acquisition & Mergers ValuationДокумент18 страницAcquisition & Mergers ValuationAqeel HanjraОценок пока нет

- C. Wolken Issued New Common Stock in 2013Документ4 страницыC. Wolken Issued New Common Stock in 2013Talha JavedОценок пока нет

- Indirect and Mutual Holdings: Answers To Questions 1Документ29 страницIndirect and Mutual Holdings: Answers To Questions 1AthayaSekarNovianaОценок пока нет

- Financial Statement Analysis - RatioДокумент7 страницFinancial Statement Analysis - RatioJanelle De TorresОценок пока нет

- Consolidation of Less-than-Wholly-Owned Subsidiaries Acquired at More Than Book ValueДокумент63 страницыConsolidation of Less-than-Wholly-Owned Subsidiaries Acquired at More Than Book ValueSelena SevvinОценок пока нет

- Solution Manual For Advanced Accounting 11th Edition by Beams 3 PDF FreeДокумент14 страницSolution Manual For Advanced Accounting 11th Edition by Beams 3 PDF Freeluxion bot100% (1)

- Chapter 12: Consolidation: Non-Controlling Interest Review QuestionsДокумент35 страницChapter 12: Consolidation: Non-Controlling Interest Review QuestionsLevi LilluОценок пока нет

- Lecture-9 10 Capital-StructureДокумент32 страницыLecture-9 10 Capital-StructuremaxОценок пока нет

- IPPTChap 005Документ71 страницаIPPTChap 005Caroline Elza Brigitha ecaaОценок пока нет

- Capital Structure: Capital Structure Theories - Net Income Net Operating Income Modigliani-Miller Traditional ApproachДокумент50 страницCapital Structure: Capital Structure Theories - Net Income Net Operating Income Modigliani-Miller Traditional Approachthella deva prasadОценок пока нет

- Solution To Self-Study Exercise 1Документ5 страницSolution To Self-Study Exercise 1chanОценок пока нет

- FS Consolidation at The Date of Acquisition v2Документ16 страницFS Consolidation at The Date of Acquisition v2Pagatpat, Apple Grace C.Оценок пока нет

- Capital Structure - 1Документ25 страницCapital Structure - 1bakhtiar2014Оценок пока нет

- BKM 10e Chap014Документ8 страницBKM 10e Chap014jl123123Оценок пока нет

- Impairment of GoodwillДокумент7 страницImpairment of Goodwillalimran177Оценок пока нет

- Fundamentals of Capital StructureДокумент42 страницыFundamentals of Capital StructureSona Singh pgpmx 2017 batch-2Оценок пока нет

- Beams Aa13e SM 01Документ14 страницBeams Aa13e SM 01jiajiaОценок пока нет

- Business Combinations: Answers To Questions 1Документ14 страницBusiness Combinations: Answers To Questions 1MUFC SupporterОценок пока нет

- Risk and Capital Budgeting: © 2009 Cengage Learning/South-WesternДокумент30 страницRisk and Capital Budgeting: © 2009 Cengage Learning/South-WesternSuraj SharmaОценок пока нет

- Corporate AccountingДокумент56 страницCorporate AccountingChandrasekhar ReddypemmakaОценок пока нет

- Jones Corportion SoluationДокумент14 страницJones Corportion SoluationShakilОценок пока нет

- Chapter 4 Consolidated Financial Statements Piecemeal AcquisitionДокумент11 страницChapter 4 Consolidated Financial Statements Piecemeal AcquisitionKE XIN NGОценок пока нет

- Sale/leaseback TransactionsДокумент24 страницыSale/leaseback TransactionsNet Lease100% (2)

- 4 The Firm's Capital Structure and Degree of LeverageДокумент9 страниц4 The Firm's Capital Structure and Degree of LeverageMariel GarraОценок пока нет

- CR Par Value PC $ 1,000 $ 40: 25 SharesДокумент4 страницыCR Par Value PC $ 1,000 $ 40: 25 SharesBought By UsОценок пока нет

- Company Acc B.com Sem Iv...Документ8 страницCompany Acc B.com Sem Iv...Sarah ShelbyОценок пока нет

- Beams AdvAcc11 ChapterДокумент27 страницBeams AdvAcc11 ChapterSt Teresa AvilaОценок пока нет

- Ch7 Problems SolutionДокумент22 страницыCh7 Problems Solutionwong100% (8)

- Dividendtheorypolicy 170303055735 PDFДокумент29 страницDividendtheorypolicy 170303055735 PDFShubham AroraОценок пока нет

- Exercises of Session 11Документ8 страницExercises of Session 11MaiPhương LinhhОценок пока нет

- Dividend Policy1Документ32 страницыDividend Policy1iqbal irfaniОценок пока нет

- Impairment of Goodwill - F7 Financial Reporting - ACCA Qualification - Students - ACCA GlobalДокумент12 страницImpairment of Goodwill - F7 Financial Reporting - ACCA Qualification - Students - ACCA Globalvivsubs18Оценок пока нет

- Chương 3Документ22 страницыChương 3Mai Duong ThiОценок пока нет

- Problem - PROFORMA BALANCE SHEET WITH CHOICE OF FINANCINGДокумент6 страницProblem - PROFORMA BALANCE SHEET WITH CHOICE OF FINANCINGJohn Richard Bonilla100% (4)

- Bank Valuation - FE FIG TryoutДокумент5 страницBank Valuation - FE FIG Tryoutcharlotte.zibautОценок пока нет

- Applied Group Fin Reporting-Changes in Group Structure PDFДокумент25 страницApplied Group Fin Reporting-Changes in Group Structure PDFObey SitholeОценок пока нет

- Financial Planning Working Capital Management Cash ManagementДокумент22 страницыFinancial Planning Working Capital Management Cash ManagementDeniz OnalОценок пока нет

- Solutions Manual Financial Statement AnalysisДокумент14 страницSolutions Manual Financial Statement AnalysisLimОценок пока нет

- Answer Key ABM2Документ6 страницAnswer Key ABM2Elle Alorra RubenfieldОценок пока нет

- Bse, Nse, Ise, Otcei, NSDLДокумент17 страницBse, Nse, Ise, Otcei, NSDLoureducation.in100% (4)

- Protection of Minority Shareholders Rights Under Companies Act 2013Документ13 страницProtection of Minority Shareholders Rights Under Companies Act 2013Amrutha GayathriОценок пока нет

- Manajemen Keuangan - SulisytandariДокумент115 страницManajemen Keuangan - SulisytandariTrianto SatriaОценок пока нет

- Far.118 Sharholders-EquityДокумент8 страницFar.118 Sharholders-EquityMaeОценок пока нет

- Book Value Per ShareДокумент2 страницыBook Value Per ShareGlen Javellana100% (1)

- ISCA Insolvency Update 2017Документ8 страницISCA Insolvency Update 2017terencebctanОценок пока нет

- Fundamentals of Company Law PDFДокумент9 страницFundamentals of Company Law PDFSai Venkatesh RamanujamОценок пока нет

- The Impact of Audit Committee Existence and External Audit On Earnings Management Evidence From PortugalДокумент25 страницThe Impact of Audit Committee Existence and External Audit On Earnings Management Evidence From PortugalasaОценок пока нет

- SHARANNLДокумент2 страницыSHARANNLJade ChengОценок пока нет

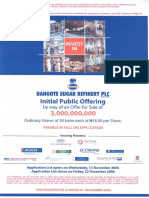

- Dangote Sugar Refinery PLC Prospectus PDFДокумент79 страницDangote Sugar Refinery PLC Prospectus PDFBilly LeeОценок пока нет

- Corporate Books and Records Chapter 11Документ17 страницCorporate Books and Records Chapter 11NingClaudioОценок пока нет

- Clemente V CA DigestДокумент1 страницаClemente V CA DigestMarteCaronoñganОценок пока нет

- Varroc Red Hearing ProspectusДокумент722 страницыVarroc Red Hearing ProspectusankitwithyouОценок пока нет

- Edward J Nell V Pacific Farms - Philippine Legal Guide-HighligtsДокумент4 страницыEdward J Nell V Pacific Farms - Philippine Legal Guide-HighligtsQueenie SabladaОценок пока нет

- 15 - GOCC Governance ActДокумент22 страницы15 - GOCC Governance ActVincent Marius MaglanqueОценок пока нет

- Corporation Accounting - IntroductionДокумент6 страницCorporation Accounting - IntroductionGuadaMichelleGripal100% (3)

- Business Law: COMSATS University of Information Technology, Attock CampusДокумент8 страницBusiness Law: COMSATS University of Information Technology, Attock CampusRabia EmanОценок пока нет

- Phil. Trust Co. Vs RiveraДокумент1 страницаPhil. Trust Co. Vs RiveraRonan Monzon100% (1)

- Myanmar Financial Institutions LawДокумент70 страницMyanmar Financial Institutions LawNelson100% (1)

- DerivativesДокумент111 страницDerivativesMuhammad Moazzam JavaidОценок пока нет

- Instruction Kit For Eform Inc-1 (: Application For Reservation of Name)Документ29 страницInstruction Kit For Eform Inc-1 (: Application For Reservation of Name)srivenramanОценок пока нет

- RTC - 16Документ17 страницRTC - 16api-729618602Оценок пока нет

- Icofr Reference Guide For ManagementДокумент472 страницыIcofr Reference Guide For Managementgladys0% (1)

- Equity Derivatives in IndiaДокумент4 страницыEquity Derivatives in Indiarahul_garg_24Оценок пока нет

- Rules Relating To Compromises, Arrangements, Amalgamations and Capital Reduction NotifiedДокумент8 страницRules Relating To Compromises, Arrangements, Amalgamations and Capital Reduction Notifiedadarsh kumarОценок пока нет

- Usa Batch 1Документ28 страницUsa Batch 1mohanОценок пока нет

- Committees of The IIL BoardДокумент2 страницыCommittees of The IIL BoardNauman ChaudaryОценок пока нет

- AMLCFT Prakas EnglishДокумент24 страницыAMLCFT Prakas EnglishThol LynaОценок пока нет

- Comparison Chart of MOA & AOAДокумент1 страницаComparison Chart of MOA & AOAAsif HameedОценок пока нет

- Currency OptionsДокумент13 страницCurrency OptionsKaren YungОценок пока нет

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)От EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Рейтинг: 4.5 из 5 звезд4.5/5 (13)

- The Millionaire Fastlane: Crack the Code to Wealth and Live Rich for a LifetimeОт EverandThe Millionaire Fastlane: Crack the Code to Wealth and Live Rich for a LifetimeРейтинг: 4.5 из 5 звезд4.5/5 (2)

- Financial Intelligence: How to To Be Smart with Your Money and Your LifeОт EverandFinancial Intelligence: How to To Be Smart with Your Money and Your LifeРейтинг: 4.5 из 5 звезд4.5/5 (540)

- Summary: Trading in the Zone: Trading in the Zone: Master the Market with Confidence, Discipline, and a Winning Attitude by Mark Douglas: Key Takeaways, Summary & AnalysisОт EverandSummary: Trading in the Zone: Trading in the Zone: Master the Market with Confidence, Discipline, and a Winning Attitude by Mark Douglas: Key Takeaways, Summary & AnalysisРейтинг: 5 из 5 звезд5/5 (15)

- Summary of 10x Is Easier than 2x: How World-Class Entrepreneurs Achieve More by Doing Less by Dan Sullivan & Dr. Benjamin Hardy: Key Takeaways, Summary & AnalysisОт EverandSummary of 10x Is Easier than 2x: How World-Class Entrepreneurs Achieve More by Doing Less by Dan Sullivan & Dr. Benjamin Hardy: Key Takeaways, Summary & AnalysisРейтинг: 4.5 из 5 звезд4.5/5 (23)

- Summary: The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel: Key Takeaways, Summary & Analysis IncludedОт EverandSummary: The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel: Key Takeaways, Summary & Analysis IncludedРейтинг: 5 из 5 звезд5/5 (80)

- The Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeОт EverandThe Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeРейтинг: 4.5 из 5 звезд4.5/5 (88)

- Baby Steps Millionaires: How Ordinary People Built Extraordinary Wealth--and How You Can TooОт EverandBaby Steps Millionaires: How Ordinary People Built Extraordinary Wealth--and How You Can TooРейтинг: 5 из 5 звезд5/5 (323)

- Bitter Brew: The Rise and Fall of Anheuser-Busch and America's Kings of BeerОт EverandBitter Brew: The Rise and Fall of Anheuser-Busch and America's Kings of BeerРейтинг: 4 из 5 звезд4/5 (52)

- Broken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterОт EverandBroken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterРейтинг: 5 из 5 звезд5/5 (3)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindОт EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindРейтинг: 5 из 5 звезд5/5 (231)

- Summary of I Will Teach You to Be Rich: No Guilt. No Excuses. Just a 6-Week Program That Works by Ramit SethiОт EverandSummary of I Will Teach You to Be Rich: No Guilt. No Excuses. Just a 6-Week Program That Works by Ramit SethiРейтинг: 4.5 из 5 звезд4.5/5 (23)

- The Holy Grail of Investing: The World's Greatest Investors Reveal Their Ultimate Strategies for Financial FreedomОт EverandThe Holy Grail of Investing: The World's Greatest Investors Reveal Their Ultimate Strategies for Financial FreedomРейтинг: 5 из 5 звезд5/5 (7)

- Summary: The Gap and the Gain: The High Achievers' Guide to Happiness, Confidence, and Success by Dan Sullivan and Dr. Benjamin Hardy: Key Takeaways, Summary & AnalysisОт EverandSummary: The Gap and the Gain: The High Achievers' Guide to Happiness, Confidence, and Success by Dan Sullivan and Dr. Benjamin Hardy: Key Takeaways, Summary & AnalysisРейтинг: 5 из 5 звезд5/5 (4)

- Fluke: Chance, Chaos, and Why Everything We Do MattersОт EverandFluke: Chance, Chaos, and Why Everything We Do MattersРейтинг: 4.5 из 5 звезд4.5/5 (19)

- Rich Bitch: A Simple 12-Step Plan for Getting Your Financial Life Together . . . FinallyОт EverandRich Bitch: A Simple 12-Step Plan for Getting Your Financial Life Together . . . FinallyРейтинг: 4 из 5 звезд4/5 (8)

- Investing for Beginners 2024: How to Achieve Financial Freedom and Grow Your Wealth Through Real Estate, The Stock Market, Cryptocurrency, Index Funds, Rental Property, Options Trading, and More.От EverandInvesting for Beginners 2024: How to Achieve Financial Freedom and Grow Your Wealth Through Real Estate, The Stock Market, Cryptocurrency, Index Funds, Rental Property, Options Trading, and More.Рейтинг: 5 из 5 звезд5/5 (99)

- The Millionaire Fastlane: Crack the Code to Wealth and Live Rich for a LifetimeОт EverandThe Millionaire Fastlane: Crack the Code to Wealth and Live Rich for a LifetimeРейтинг: 4.5 из 5 звезд4.5/5 (58)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassОт EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassОценок пока нет

- Sleep And Grow Rich: Guided Sleep Meditation with Affirmations For Wealth & AbundanceОт EverandSleep And Grow Rich: Guided Sleep Meditation with Affirmations For Wealth & AbundanceРейтинг: 4.5 из 5 звезд4.5/5 (105)

- Psychology of Money: The Essential Guide to Building Your Wealth , Discover All the Important Information And Useful Strategies in the Pursuit of WealthОт EverandPsychology of Money: The Essential Guide to Building Your Wealth , Discover All the Important Information And Useful Strategies in the Pursuit of WealthРейтинг: 4.5 из 5 звезд4.5/5 (68)

- Rich Dad Poor Dad: What the Rich Teach Their Kids About Money That the Poor and Middle Class Do NotОт EverandRich Dad Poor Dad: What the Rich Teach Their Kids About Money That the Poor and Middle Class Do NotОценок пока нет

- The 4 Laws of Financial Prosperity: Get Conrtol of Your Money Now!От EverandThe 4 Laws of Financial Prosperity: Get Conrtol of Your Money Now!Рейтинг: 5 из 5 звезд5/5 (389)

- Rich Dad's Cashflow Quadrant: Guide to Financial FreedomОт EverandRich Dad's Cashflow Quadrant: Guide to Financial FreedomРейтинг: 4.5 из 5 звезд4.5/5 (1385)