Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- 30 LLRRRRK L-: Lt.'l'iong Lntcrest DiscountДокумент1 страница30 LLRRRRK L-: Lt.'l'iong Lntcrest DiscountJimuel Sanchez CayabasОценок пока нет

- 13 Chieng V Sps SantosДокумент2 страницы13 Chieng V Sps SantosArtemisTzyОценок пока нет

- TDS - TCSДокумент55 страницTDS - TCSBeing HumaneОценок пока нет

- Taxation of Fringe Benefits: (Art 212, Labor Code)Документ7 страницTaxation of Fringe Benefits: (Art 212, Labor Code)Lyca VОценок пока нет

- Renters Policy PDFДокумент18 страницRenters Policy PDFMumy MoraОценок пока нет

- Terms and Conditions: Æ ON Credit Service (M) BerhadДокумент19 страницTerms and Conditions: Æ ON Credit Service (M) BerhadKhazwan AriffОценок пока нет

- Neraca Dan Laba Rugi (Blank Form)Документ2 страницыNeraca Dan Laba Rugi (Blank Form)Ugi Dwiki PОценок пока нет

- Chapters 20, 22 & 24Документ59 страницChapters 20, 22 & 24Manidipa BoseОценок пока нет

- Tax Invoice: Shabab Anwer Shabab AnwerДокумент1 страницаTax Invoice: Shabab Anwer Shabab AnwerSkill India0% (1)

- Formulas #1: Future Value of A Single Cash FlowДокумент4 страницыFormulas #1: Future Value of A Single Cash FlowVikram Sathish AsokanОценок пока нет

- United States Court of Appeals, First CircuitДокумент10 страницUnited States Court of Appeals, First CircuitScribd Government DocsОценок пока нет

- Plaintiff-Appellant vs. vs. Respondents-Appellees Solicitor General Meer, Meer & MeerДокумент7 страницPlaintiff-Appellant vs. vs. Respondents-Appellees Solicitor General Meer, Meer & MeerVMОценок пока нет

- Producers Bank of The Philippines v. Excelsa Industries, Inc.Документ11 страницProducers Bank of The Philippines v. Excelsa Industries, Inc.MonicaSumanga0% (1)

- The Importance of Working Capital ManagementДокумент2 страницыThe Importance of Working Capital ManagementparthОценок пока нет

- 3Документ2 страницы3Glaiza OtazaОценок пока нет

- Sanction Letter MitaBrickДокумент15 страницSanction Letter MitaBricktarique2009Оценок пока нет

- Bin GeneratorДокумент3 страницыBin GeneratorShashank GuptaОценок пока нет

- Income Tax AustraliaДокумент9 страницIncome Tax AustraliaAbdul HadiОценок пока нет

- Case Study On Gainesboro Machine Tools CorporationДокумент13 страницCase Study On Gainesboro Machine Tools Corporationemehmehmeh86% (7)

- Accounting Cycle ProblemДокумент13 страницAccounting Cycle Problemapi-300305341Оценок пока нет

- Week3. CHAPTER 34 - SHARE-BASED PAYMENTS PART 1Документ17 страницWeek3. CHAPTER 34 - SHARE-BASED PAYMENTS PART 1Loi KkimakimОценок пока нет

- Investor Protection Measures by Sebi: Dr. KVSN Jawahar Babu S. Damodahr NaiduДокумент9 страницInvestor Protection Measures by Sebi: Dr. KVSN Jawahar Babu S. Damodahr NaiduaswinecebeОценок пока нет

- In Ejectment CasesДокумент7 страницIn Ejectment CasesJaniceОценок пока нет

- DCF Application - Asian PaintsДокумент6 страницDCF Application - Asian PaintsKashish PopliОценок пока нет

- Start Up Costs CalculatorДокумент5 страницStart Up Costs CalculatorMainul HossainОценок пока нет

- Lifting of The Corporate VeilДокумент7 страницLifting of The Corporate VeilAmit Grover100% (1)

- Bhavna Patil (NBFC)Документ55 страницBhavna Patil (NBFC)BHAVNA PATIL100% (3)

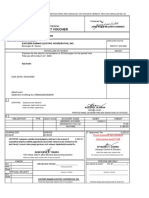

- Disbursement Voucher: Republic of The PhilippinesДокумент1 страницаDisbursement Voucher: Republic of The PhilippinesJepernick EspaderoОценок пока нет

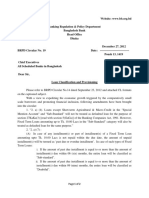

- BRPD Circular No. 19 (2012)Документ2 страницыBRPD Circular No. 19 (2012)Mohaiminul Islam ShuvraОценок пока нет

- Engineering Economy II PDFДокумент2 страницыEngineering Economy II PDFrenzon272Оценок пока нет