Академический Документы

Профессиональный Документы

Культура Документы

Merger and Acquisition

Загружено:

Mashood Rehman Khan NiaziАвторское право

Доступные форматы

Поделиться этим документом

Поделиться или встроить документ

Этот документ был вам полезен?

Это неприемлемый материал?

Пожаловаться на этот документАвторское право:

Доступные форматы

Merger and Acquisition

Загружено:

Mashood Rehman Khan NiaziАвторское право:

Доступные форматы

Journal of Management http://jom.sagepub.

com/

Taking Stock of What We Know About Mergers and Acquisitions: A Review and

Research Agenda

Jerayr Haleblian, Cynthia E. Devers, Gerry McNamara, Mason A. Carpenter and Robert B.

Davison

Journal of Management 2009 35: 469 originally published online 23 February 2009

DOI: 10.1177/0149206308330554

The online version of this article can be found at:

http://jom.sagepub.com/content/35/3/469

Published by:

http://www.sagepublications.com

On behalf of:

Southern Management Association

Additional services and information for Journal of Management can be found at:

Email Alerts: http://jom.sagepub.com/cgi/alerts

Subscriptions: http://jom.sagepub.com/subscriptions

Reprints: http://www.sagepub.com/journalsReprints.nav

Permissions: http://www.sagepub.com/journalsPermissions.nav

Citations: http://jom.sagepub.com/content/35/3/469.refs.html

>> Version of Record - Jun 5, 2009

OnlineFirst Version of Record - Feb 23, 2009

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

What is This?

Taking Stock of What We Know

About Mergers and Acquisitions:

A Review and Research Agenda†

Jerayr Haleblian*

Anderson Graduate School of Management, University of California, Riverside

Cynthia E. Devers

Wisconsin School of Business, University of Wisconsin–Madison

Gerry McNamara

Broad Graduate School of Management, Michigan State University, East Lansing

Mason A. Carpenter

Wisconsin School of Business, University of Wisconsin–Madison

Robert B. Davison

Broad Graduate School of Management, Michigan State University, East Lansing

Scholars from multiple fields have shown increasing interest in the causes and consequences of

mergers and acquisitions (M&A). Although this proliferation of research has the potential to

significantly improve our understanding of M&A activity, absent is the necessary step of con-

solidating and integrating extant knowledge. Accordingly, this article develops a framework to

organize and review recent empirical findings, principally from management, economics, and

finance in which interest in acquisition behavior is high but also from other areas that have tan-

gentially explored acquisition activity such as accounting and sociology. This article identifies

patterns and theoretical gaps and provides recommendations for future research aimed at devel-

oping a more integrated M&A research agenda for management scientists.

Keywords: acquisitions; mergers; mergers and acquisitions

†We would like to thank Manuel Becerra for his insightful comments, which significantly improved our manuscript.

This article was accepted under the editorship of Russell Cropanzano.

*Corresponding author: Tel.: 951-827-3608.

E-mail address: john.haleblian@ucr.edu

Journal of Management, Vol. 35 No. 3, June 2009 469-502

DOI: 10.1177/0149206308330554

© 2009 Southern Management Association. All rights reserved.

469

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

470 Journal of Management / June 2009

Global investment in mergers and acquisitions (hereafter referred to simply as acquisitions)

has reached unprecedented levels in recent years (Barkema & Schijven, 2008a). Paralleling this

practical importance, in both monetary and strategic terms, acquisition activity has increasingly

become a focus of study in several academic fields. Although this interest has generated con-

siderable acquisition-related knowledge, the range of findings from these diverse areas lacks

theoretical integration, which constrains scholars’ abilities to synthesize notable contributions

from each discipline. For instance, initial research, concentrated mostly in the finance literature,

paved the way for scholarly work in the acquisition literature. These scholars looked with great

interest at whether acquisitions added value to the firm, by focusing largely on assessing the

relationship between acquisition activity and firm performance through changes in shareholder

value (Carper, 1990). This period also witnessed the advent of event study methodology (Brown

& Warner, 1980, 1985), designed to aid researchers in assessing market expectations of future

cash flows related to discrete events, such as acquisition announcements.

Typical findings from these early studies suggested that acquisitions did not enhance

acquiring firm value, as measured by either short-term (Asquith, 1983; Dodd, 1980; Jarrell

& Poulsen, 1989; Malatesta, 1983) or long-term performance measures (Agrawal, Jaffe, &

Mandelker, 1992; Asquith, 1983; Loderer & Martin, 1992). More specifically, acquisitions

were often found to erode acquiring firm value (Chatterjee, 1992; D. K. Datta, Pinches, &

Narayanan, 1992; King, Dalton, Daily, & Covin, 2004; Moeller, Schlingemann, & Stulz,

2003; Seth, Song, & Pettit, 2002) and produce highly volatile market returns (Langetieg,

Haugen, & Wichern, 1980; Pablo, Sitkin, & Jemison, 1996).

Although much of the early empirical attention centered on the performance of bidding

firms, some finance researchers also assessed the returns accrued by target firms. Perhaps

not surprising, given that acquirers generally pay premiums to acquire targets, results

showed that target shareholders generally fared well, often experiencing significant positive

returns (Asquith & Kim, 1982; D. K. Datta et al., 1992; Hansen & Lott, 1996; Malatesta,

1983). In addition to target performance, scholars also examined the effects of acquisitions

on combined bidder and target returns (Bradley, Desai, & Kim, 1988; Bruner, 1988; Carow,

Heron, & Saxton, 2004; Healy, Palepu, & Ruback, 1992; Wright, Kroll, Lado, & van Ness,

2002). Whereas these studies generally showed that acquisitions produce positive combined

returns, importantly, decomposition of these joint outcomes revealed that targets accounted

for the majority of those gains, with acquiring firms contributing neutral or negative returns

(i.e., Bradley et al., 1988; Houston, James, & Ryngaert, 2001; Leeth & Borg, 2000).

In light of these performance consequences for acquirers, more recent finance and strategic

management work focused on antecedents of acquisitions, as scholars sought to uncover why

firms acquired. Perhaps encouraged by the increasing popularity of acquisitions, this research

gained traction in recent decades. Although scholars have uncovered a number of antecedents

that appear to trigger acquisition activity, much of this research has occurred in isolated pock-

ets, leaving a unified theoretical view of why firms acquire markedly absent from this litera-

ture. Further research has focused on identifying both potential moderators of acquisition

performance and other acquisition-related outcomes. Although this work confirms that, on

average, acquiring firms do not benefit from acquisitions, it importantly reveals conditions and

situations under which acquisitions do benefit acquirers. Nevertheless, like the work cited ear-

lier, these rich insights have yet to be effectively integrated into the vast acquisition literature.

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

Haleblian et al. / Mergers and Acquisitions 471

Given the practical and theoretical importance of acquisitions, it is surprising that no

comprehensive reviews of acquisition research have been published in the past decade.1 As

a result, few unifying theoretical threads capable of knitting together the unique, discipli-

nary-based perspectives on acquisitions have emerged, leaving an understanding of the

acquisition process punctuated by critical gaps. In this review, we begin to address these

gaps by developing a comprehensive theoretical framework that organizes the acquisition lit-

erature. In turn, we use our framework to review extant research within and across multiple

disciplines. Building on this review, we then highlight the theoretical and empirical gaps that

continue to plague the acquisition literature and outline several future research suggestions

for advancing the state of acquisition research.

We followed five steps to manage the scope of our review and ensure consistent coverage

of relevant studies in our sample. First, we focused on quantitative acquisition research in

the accounting, economics, finance, management, and sociology literatures from 1992 to

present. Second, given the considerable size of the acquisition literature and space limita-

tions, we restricted our sample to articles published in leading journals in each of these

areas.2 Within the constraints of the first two sampling steps, our third step consisted of a

search of titles and abstracts of the target journals on the keywords merger, merge, acquisi-

tion, acquire, and mergers and acquisitions (M&A). We made the decision to focus our

search on a limited range of keywords directly related to the topic of the review, as expand-

ing outside of this list to include related words, such as diversification, yielded an over-

whelming number of articles, almost all of which were not relevant to the topic of the review.

Even with the narrow focus of our keyword search, our initial search identified 864 articles.

Fourth, we independently reviewed subsets of these articles for relevance and fit, reading the

text and verifying their empirical nature. Many articles were eliminated as being clearly off

topic (e.g., “information acquisition,” “knowledge acquisition”); discrepancies in opinions

about inclusion or exclusion were resolved through discussion. This fourth step reduced the

set to 310 articles. In the fifth and final step, we further reviewed each study to confirm rel-

evance and eliminated studies in which acquisitions were not the central focus. This resulted

in a sample of 167 empirical articles.

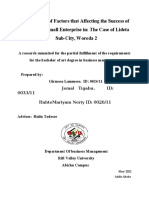

To get a sense of how interest in the topic of acquisitions has evolved, we plotted the

number of studies published in the period examined by academic discipline.3 (See Figure 1.)

This plot shows, not surprisingly, that the management and finance fields have generated the

bulk of published acquisition research since 1992. It also shows that although research inter-

est in acquisitions in the management field remained fairly constant throughout the period

examined, interest in acquisitions increased in finance in recent years. This reinforces our

belief that a multidisciplinary review of the field is beneficial because it fosters cross-disci-

plinary learning, allowing the management field to incorporate knowledge from recent

finance work on acquisitions into our own research.

We then moved from the search for articles to the coding and categorizing of the articles. In

this step, we coded the primary variables and key findings. Drawing from this coding, we

developed a model in which to frame and interpret the research on acquisitions and to ease the

presentation of the body of work on this topic. This comprehensive theoretical framework cat-

egorizes recent acquisition research into three broad areas: (a) antecedents, the factors that lead

firms to undertake acquisitions; (b) moderators, internal and external factors that moderate

acquisition performance; and (c) other acquisition outcomes (summarized in Figure 2). Next,

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

472 Journal of Management / June 2009

Figure 1

The Trends in Research on Mergers and Acquisitions

Number of Articles by Discipline

30

25

20

15

10

92-93 94-95 96-97 98-99 00-01 02-03 04-05 06-07

Management Finance Accounting

Economics Sociology

we present our full review of this literature, using this framework to discuss the current state

of knowledge regarding acquisitions.

Antecedents: Why Do firms Acquire?

A primary line of research across many of the sampled articles centers on why firms

acquire. Although scholars have proposed a number of acquisition antecedents, they fall

broadly into four categories: value creation, managerial self-interest (value destruction),

environmental factors, and firm characteristics.

Value Creation

Market power. Market power may be considered an attempt to appropriate more

value from customers. The finance literature was first to explore the market power

hypothesis—the idea that having fewer firms in an industry increases firm-level pricing

power—by examining rival firms’ stock price reactions to horizontal mergers. Although

this early research found no support for market power as an acquisition antecedent

(Eckbo, 1983; Stillman, 1983), some economists criticized this work by arguing that the

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

Haleblian et al. / Mergers and Acquisitions 473

Figure 2

Mergers and Acquisitions Literature Overview

MODERATORS

Deal Characteristics

• Payment type

• Deal type

Managerial Effects

• Ownership

• Compensation

• Managerial

experience

• Cognition/

Personality

Firm Characteristics

ANTECEDENTS • Performance

• Size

Value Creation

• Acquirer

• Market power experience

• Efficiency

• Resource Environmental Factors

redeployment • Waves

• Market discipline • Regulations

Managerial Self-Interest

(Value Destruction)

• Compensation OUTCOMES

• Hubris

Performance Outcomes

• Target defense

Other Outcomes

tactics ACQUISITION

BEHAVIOR • Premiums

Environmental Factors

• Turnover

• Environmental • Customers/

uncertainty Bondholders

• Regulation

• Imitation

• Resource

dependence

• Networks ties

Firm Characteristics

• Acquisition

experience

• Firm strategy

and position

rivals studied were large, multiproduct firms that derived only a small fraction of their

revenues from the affected market and that the sample periods examined were subsequent

to highly restrictive antitrust legislation. Using the same methodological approach, on a

period preceding both those antitrust laws and the rise of highly diversified firms (early

1900s), Prager (1992) found that railroad industry rivals’ stock prices increased the week

acquisitions were announced, suggesting support for the market power hypothesis.

Similarly, an analysis of 1980s airline mergers showed that prices on routes serviced by

merging firms increased relative to those of a matched sample unaffected by the merger (Kim

& Singal, 1993). Thus, some limited evidence supports market power as an acquisition motive.

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

474 Journal of Management / June 2009

Efficiency. To reduce the cost side of value creation, economists have also assessed

whether acquisitions are motivated by the desire to increase efficiency. Suggestive of

efficiency motives, Banerjee and Eckard (1998) found that the market bid up horizontal merg-

ers during the first great merger wave (early 1900s). Additional support came from more

recent samples documenting improvements in long-term plant productivity (McGuckin &

Nguyen, 1995) and public accounting service delivery (Banker, Chang, & Cunningham,

2003). Nevertheless, all evidence is not so straightforward. For example, in a multiperiod

study, Klein (2001) found a diversification “discount” for late period (1970 to 1974) con-

glomerates; however, contrary to prior work implying inefficiency in 1960s conglomeration

(e.g., P. Berger & Ofek, 1995; Jensen & Ruback, 1983; Kaplan & Weisbach, 1992), Klein

reported a premium for late-1960s acquisitions, supporting the efficiency motive for unrelated

acquisitions during early yet not later periods.

Resource redeployment. Scholars have argued that managers view horizontal acquisitions

as a means of facilitating redeployment of assets and competency transfers to generate

economies of scope. Consistent with this argument, Capron, Dussauge, and Mitchell

(1998) found that horizontal acquisitions often led to significant resource realignment

between acquirers and targets. In addition, King, Slotegraaf, and Kesner (2008) showed

that acquirer abnormal returns were associated with the degree of acquirer and target firm

resource complementarity. In a similar vein, Karim and Mitchell (2000) reported that

acquirers exhibited greater changes in their resource sets than nonacquirers. Specifically,

acquirers deepened resource sets by both adding to existing areas of strength and extend-

ing resources into new areas. Notably, acquirers extended their resources to include recent

entries to the industry, suggesting that managers may use acquisitions as a means of inno-

vation. Extending this work, Uhlenbruck, Hitt, and Semadeni (2006) drew on resource-

based and organizational learning perspectives to demonstrate that offline firms used

acquisitions to acquire scarce resources held by Internet firms, which in turn led to posi-

tive acquirer returns. More recently, Puranam and Srikanth (2007) demonstrated that

acquiring firms leveraged the innovation-oriented resources of target firms either by inte-

grating those resources into the acquiring firm or by leveraging the innovative capabilities

of the firm as an independent unit. The results above are consistent with research demon-

strating that the market position and resources of firms involved in acquisitions influence

future product market performance (Lubatkin, Schulze, Mainkar, & Cotterill, 2001).

Market discipline. Additional research from finance suggests that acquisitions may be

value enhancing when they are used to discipline ineffective managers. Agency theorists, in

particular, contend that acquisitions can help protect shareholders from poor management

(Jensen, 1986; Jensen & Ruback, 1983). Consistent with this notion, research has found that

CEOs of acquired firms are often dismissed after an acquisition has been completed

(Agrawal & Walkling, 1994; Martin & McConnell, 1991). Moreover, studies have shown

that relative to other managers, target firm managers who were overcompensated prior to

takeovers received reduced compensation after acquisition completion (Agrawal &

Walkling, 1994). Agrawal and Walkling (1994) argued that this reflected the full playing out

of the market for corporate control, with firms managed by ineffective and overcompensated

top managers being the target of takeovers made with the intention of corporate turnaround.

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

Haleblian et al. / Mergers and Acquisitions 475

An implied assumption within the market discipline hypothesis is that firms with poor

corporate governance have low market values and are taken over by higher valued bidders

(i.e., high buys low). However, Rhodes-Kropf and Robinson (2008) showed that rather than

high-asset-value firms buying low-asset-value firms, firms with similar asset valuation tend

to purchase one another (i.e., like buys like). Hence, although a firm may want to merge with

a stronger firm, in such a case, they would likely have reduced bargaining power. Thus, evi-

dence has accrued for complementarity asset quality as a driver of acquisition activity in

which firms with similar quality seek each other out as high market-to-book acquirers will

acquire high market-to-book targets and weaker acquirers will buy weaker targets.

Consistent with this logic, Wang and Zajac (2007) found that resource similarity between

firms increases the likelihood of an acquisition over an alliance.

Managerial Self-Interest (Value Destruction)

It is interesting that although much work assumes that acquisitions are made to maxi-

mize shareholder value (e.g., market power, efficiency, asset redeployment, market disci-

pline), a substantial amount of studies make the opposing assumption—that acquisitions

destroy shareholder value as managers attempt to maximize their own self-interest.

Compensation. A number of finance and management scholars have demonstrated important

links between upper echelon compensation and ownership and acquisitive behavior. For

example, research has shown that industries with higher CEO compensation generally exhibit

greater acquisition activity (Agrawal & Walkling, 1994) and, further, that acquiring CEO

(Sanders, 2001) and director (Deutsch, Keil, & Laamanen, 2007) stock option grants are posi-

tively associated with such activity. Agency theory holds that compensation contracts should be

designed to reduce managerial opportunism and align managers’ and shareholders’ interests.

However, a growing body of recent evidence suggests that managers’ desire for increased com-

pensation elicits strong, self-interested motivations to acquire. This is consistent with evidence

demonstrating that acquiring CEOs’ postacquisition compensation generally increases, irre-

spective of acquisition performance through liberal postacquisition equity-based pay grants

(Harford & Li, 2007), bonuses (Grinstein & Hribar, 2004), and other compensation (Bliss &

Rosen, 2001) that offset potential decreases of acquiring CEOs’ wealth. Additionally, managing

larger firms generally also increases CEO discretion and power, which can further entrench

managers and reduce their employment risk (e.g., Gomez-Mejia & Wiseman, 1997; Haleblian

& Finkelstein, 1993; Hambrick & Finkelstein, 1987). This research suggests that, in general,

acquisitions may appear overly attractive for CEOs. However, vigilant governance may attenu-

ate this effect, as Kroll, Wright, Toombs, and Leavell (1997) found that acquisitions led to higher

size-based CEO compensation in manager-controlled firms, yet in owner-controlled firms,

acquiring CEOs’ compensation was more closely tied to shareholder returns.

Managerial hubris. In addition to compensation, other work has shown that manager-

ial confidence and ego gratification may also increase acquisition behavior. Finance

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

476 Journal of Management / June 2009

scholars were the first to propose CEO hubris—exaggerated self-confidence—as an

acquisition motive (Roll, 1986). In line with this argument, management research has

empirically demonstrated that CEO hubris increased acquisition premiums, which in turn

decreased acquisition performance (Hayward & Hambrick, 1997). In a closely related

article, Malmendier and Tate (2008) found that overconfident CEOs overestimate their

ability to generate returns and as a result overpay for target companies and undertake

value-destroying mergers. Moreover, this effect was found to be particularly pronounced

for firms that have access to internal financing.

Target defense tactics. Arguably, target defense tactics are created to enhance managerial

self-interest at the expense of shareholder wealth. Hence, finance scholars have shown inter-

est in the implications of defense tactics on acquisition likelihood. For example, Ambrose

and Megginson (1992) found that blank check preferred stock authorizations tended to

decrease target acquisition likelihood. Similar findings in initial public offering (IPO)

research revealed that when IPO managers deployed defenses, such defenses were negatively

related to subsequent acquisition likelihood (Field & Karpoff, 2002). However, in contrast,

Bates and Lemmon (2003) found that rather than serving to deter bidding, target payable

fees (termination fee provisions in which the target has agreed to pay a fee to the acquirer in

the event the merger agreement is terminated) led to higher deal completion rates and greater

takeover premiums, suggesting that defense tactics do not have homogeneous effects.

Additional work is consistent with the notion of managerial self-interest from the perspec-

tive of targets. Cai and Vijh (2007) showed that target CEOs with greater levels of illiquid

(not yet vested) stock were more likely to become acquired. More specifically, the restricted

stock of target CEOs becomes vested after an exchange of control, allowing them to sell their

stock, which increases the value of their holdings, and incents them to sell the firm.

Overall, it is interesting to note that although self-interested behavior sometimes leads to

acquisition activity, ineffective governance that may follow self-interested activity may lead

to market discipline-based acquisition activity. Perhaps this is one reason we see so much

acquisition activity—acquisitions are made for multiple reasons: value-enhancing and value-

destroying ones.

Environmental Factors

Environmental uncertainty and regulation. Strategic management scholars have

focused attention on whether the fit between environment and firm strategy motivates

acquisition behavior. Some of this work has shown that environmental uncertainty affects

whether firms select to acquire or opt for other cooperative means. This research has shown

that although environmental uncertainty increased the likelihood of collaboration over acqui-

sition (Folta, 1998), it also increased the likelihood of acquisition over licensing agreement

(Schilling & Steensma, 2002). Additional work has investigated how environmental factors

influence corporate portfolio restructuring generally and acquisition likelihood specifically.

Bergh and Lawless (1998) showed that highly diversified firms were more likely to pursue

acquisitions in decreasing environmental uncertainty, whereas the opposite occurred in less

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

Haleblian et al. / Mergers and Acquisitions 477

diversified firms; Thornton (2001), however, demonstrated that the failure to shift firm strat-

egy with environmental changes increased acquisition likelihood.

Examining environmental factors from a different perspective, finance scholars have

demonstrated that external governance structures also influence acquisition likelihood. More

specifically, this work examined the influence of regulatory actions on acquisition behavior.

Results of this work found that antitrust laws did not appear to impede acquisition activity

(Matsusaka, 1996) and, furthermore, that countries with higher accounting standards and

stronger shareholder protection had a greater amount of acquisition activity than their counter-

parts (Rossi & Volpin, 2004). More recent work suggests that impending regulation of sin

industries (e.g., tobacco, alcohol, gaming) may have motivated firms to engage in domestic

expansion through diversifying acquisitions as a means of garnering the political clout to influ-

ence policies aimed at mitigating the costs of such regulation (Beneish, Jansen, Lewis, &

Stuart, 2008).

Imitation and resource dependence. Sociologists have also shown interest in why firms

acquire. Extending interorganizational imitation theory to explore interindustry mergers,

Stearns and Allan (1996) found that fringe actors initiated innovations that enabled them to

execute mergers and, as these actors became increasingly successful, others, in turn, imitated

their innovations. Drawing on resource dependence theory, to assess the likelihood of

becoming a target, Palmer, Zhou, Barber, and Soysal (1995) showed that although the capac-

ity to constrain firms in other industries gave corporations in the 1960s conglomerate wave

little incentive to seek friendly acquisition partners, it also made them targets of predators

from other nonlinked industries.

Pioneering resource dependency work in the management literature, Pfeffer (1972) showed

that firms managed resource dependencies by absorbing needed resources through mergers.

This basic finding was subsequently replicated, although the use of more powerful analytical

methods generated results that suggested the strength of this relationship was weaker than orig-

inally found (Finkelstein, 1997). Additional research conducted by Casciaro and Piskorski

(2005) extended Pfeffer’s contributions by showing that although mutual dependence between

two firms was a key driver of acquisition behavior in interindustry acquisitions, power imbal-

ances between these same two firms acted as an obstacle to their combination.

Network ties. Building on network ties research, originally developed by Granovetter

(1973) and other sociologists, management scholars have shown the importance of net-

work ties as a driver of acquisition behavior. For example, Haunschild (1993) found that

managers imitated the acquisition activities of firms to which they were tied through

interlocking directorships. Subsequent work demonstrated that the number of current

acquisitions made by firms was positively related to the number of acquisitions com-

pleted by interlock partners (Haunschild & Beckman, 1998). Similarly, Westphal, Seidel,

and Stewart (2001) found that changes in the acquisition activity of “tied-to” firms had

significant positive effects on changes in focal firm acquisition activity. This research

identifies managers’ desires to achieve peer isomorphism as an important antecedent of

acquisitions.

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

478 Journal of Management / June 2009

Firm Characteristics

Acquisition experience. The management literature has been interested in the influ-

ence of experience as an acquisition motivator. Acquisitions are an excellent context to

study organization learning, in that acquisitions are strategically significant, discrete

events. Furthermore, because they often occur multiple times in a firm’s history, scholars

have the opportunity to assess whether performance improvements occurred across

acquisition events. An excellent comprehensive review of the influence of experience in

the context of acquisitions has recently been published in Journal of Management

(Barkema & Schijven, 2008a). Thus, we limit our scope in this section to provide a cursory

overview.

In general, research on acquisition experience has shown recent experience to be pos-

itively related to subsequent acquisition likelihood (Haleblian, Kim, & Rajagopalan,

2006), particularly when this experience is rewarded (i.e., strong acquisition perfor-

mance). However, other work has shown that acquisition experience of a particular type

(e.g., horizontal, vertical, product extension) can increase the likelihood of subsequent

acquisitions of the same type (Amburgey & Miner, 1992) and, correspondingly, decrease

the likelihood of acquisition of any different types (Yang & Hyland, 2006). Related work

suggests that experiential processes encourage repetitive behavior. Specifically, Baum,

Li, and Usher (2000) found that firms acquired other firms that were geographically and

organizationally similar to their own most recent prior acquisitions. Moreover, they fur-

ther proposed that in addition to firms’ own experience, vicarious learning also appeared

to influence acquisition behavior, as they found that firms imitated the location choices

of other visible and comparable firms’ recent acquisitions (Baum et al., 2000). It is inter-

esting that the experience effect appears to generalize beyond acquisitions, as

Vanhaverbeke, Duysters, and Noorderhaven (2002) found that prior alliance experience

increased the likelihood of one partner acquiring the other, highlighting the influence of

experience, in general, on acquisition behavior.

Firm strategy and position. Although work in this area is recent and limited, it suggests

that firms’ strategic positions and intentions may have strong influences on acquisition

behavior. In the context of international strategy, evidence has shown that companies fol-

lowing a global strategy have higher proportions of greenfield subsidiaries than multido-

mestics, whereas companies following a multidomestic strategy exhibit higher proportions

of acquisitions (Harzing, 2002). Furthermore, in an entrepreneurial firm context, Graebner

and Eisenhardt (2004) found that targets facing “difficult strategic hurdles” such as a chief

executive search or an impending funding round were more likely to be acquired than those

that were not facing such hurdles.

Overall, then, a multitude of factors from different disciplines have been offered as to

why firms acquire. However, a nagging basic question within this area still remains:

Which of these antecedents has the most influence on acquisition behavior and under what

conditions?

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

Haleblian et al. / Mergers and Acquisitions 479

Moderators of the Acquisition–Performance Relationship

Given that acquiring firms generally do not benefit from making acquisitions, scholars

have increasingly concerned themselves with developing a better understanding of the spe-

cific situations that allow the minority of acquirers to create value. Results of this work have

uncovered multiple conditions that moderate the acquisition–performance relationship,

which we organize based on four levels of analysis: deal characteristics, managerial effects,

firm characteristics, and environmental factors.

Deal Characteristics

Payment type. Beginning with the deal itself, a common argument asserts that managers

finance acquisitions with cash when they perceive their firms are undervalued and with stock

when they perceive their firms are overvalued (King et al., 2004), suggesting that the market

should perceive stock-financed deals as a signal of bidder overvaluation (Loughran & Vijh,

1997). Taking a somewhat different view, Hayward (2003) argued that powerful banks with

specialized expertise are quick to use this expertise and, thus, direct clients to complex solu-

tions, such as stock-financed deals. In support, he reported that using investment banks to

advise stock-financed acquisitions harmed acquirer performance.

Regardless of the motivations behind financing choice, several studies have shown that

cash-financed deals are more beneficial, or at least less detrimental, to bidding firms’ share-

holders (e.g., Carow et al., 2004; Huang & Walkling, 1987; Loughran & Vijh, 1997; Travlos,

1987). However, this evidence is not as straightforward as some might suggest. For example,

although Healy et al. (1992) reported no effect of payment method on bidder accounting per-

formance, other studies found mixed results. Specifically, Heron and Lie (2002) found no

material differences in operating performance between cash and stock deals, yet they reported

lower announcement and postacquisition market returns for stock acquisitions than for cash

acquisitions. Furthermore, in a sample of serial acquirers, Fuller, Netter, and Stegemoller

(2002) found that regardless of payment method, public acquisitions resulted in insignificant

bidder returns for cash or combination deals and significantly negative returns for stock deals.

However, it is interesting that private and subsidiary acquisitions increased bidder perfor-

mance, regardless of method of payment, but those returns were greater when stock financ-

ing was used. Similarly, in a comparison of acquisitions of Canadian firms by domestic and

foreign bidders, contrary to many studies of U.S. acquisitions, Eckbo and Thorburn (2000)

found that returns were highest for domestic bidders who financed acquisitions with stock.

Examining payment method from a different perspective, Bharadwaj and Shivdasani (2003)

found that acquisitions entirely financed by banks resulted in high positive announcement

returns, suggesting that bank debt served as a signal of certification and monitoring for bidding

firms. Louis (2005) also found an effect for monitoring by demonstrating that bidders audited

by non–Big 4 accounting firms experienced higher abnormal announcement returns that those

audited by Big 4 firms. This effect was greater for private firms and when auditors appeared to

have served in an advisory capacity. Faccio, McConnell, and Stolin (2006) added additional

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

480 Journal of Management / June 2009

support for the private firm effect by reporting higher acquirer abnormal announcement returns

for private versus public targets that held over time and across Western European countries.

Explaining the private firm effect, Hansen and Lott (1996), citing a similar argument made by

Easterbrook and Fischel (1982), proposed that when bidding firm shareholders also hold tar-

get shares, they are indifferent to how acquisition gains arise (from the bidder or the target).

Therefore, bidding firm returns should be higher when acquiring private firms, where cross-

ownership (bidder and target ownership) is expected to be low or nonexistent. Bae, Kang, and

Kim (2002) offered support for the cross-ownership effect by demonstrating that although bid-

ding Korean chaebol firms’ minority shareholders suffered acquisition announcement losses,

controlling shareholders gained from such announcements through increases in the values of

other member firms (a tunneling effect).

Deal type. In general, research on deal types has suggested that tender offers outperform

mergers (e.g., Agrawal et al., 1992), particularly in cash-financed deals (Loughran & Vijh,

1997). However, in a more in-depth examination of the tender offer/merger distinction, Rau

and Vermaelen (1998) reported that the negative performance of mergers owed primarily to

low book-to-market “glamour” bidders whose postacquisition performance was significantly

lower than that of other glamour bidders and value bidders. They concluded that the man-

agers of low book-to-market firms might make poorer acquisition decisions than managers

of other firms, suggesting the importance of prior performance on acquisition returns.

Managerial Effects

Ownership and compensation. Following the agency-theoretic perspective that executive

equity and compensation influence interest alignment, finance and management scholars

have examined the influence of various ownership and compensation schemes on the

acquisition–performance relationship. For example, Hubbard and Palia (1995) found a

curvilinear relationship between managerial ownership and acquirer announcement returns.

Specifically, returns were highest at moderate levels of ownership. The authors argued that

under moderate levels of ownership, managers’ interests were more aligned with those of

shareholders, which resulted in lower bid premiums. However, they suggested that at low and

high levels of ownership, managers’ interests were misaligned with shareholders’, and thus,

they overpaid for acquisitions, which negatively affected announcement returns. Similarly,

Wright et al. (2002) found a nonlinear relationship between ownership and acquisition

announcement returns, such that under moderate levels of CEO ownership, combined bidder

and target announcement returns were positive; however, CEO stock options exhibited a

positive, linear influence on these returns. S. Datta, Iskandar-Datta, and Raman (2001)

reported a positive relationship between the Black-Scholes values of previous-year stock

option grants on subsequent-year bidder announcement returns. In addition, high levels of

previous-year options grants led to lower acquisition premiums and to the propensity to

acquire higher growth targets that increased firm risk.

Nevertheless, the results of other studies challenged these results. For example, Loderer

and Martin (1997) used a simultaneous equations framework to examine whether managers’

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

Haleblian et al. / Mergers and Acquisitions 481

stock ownership led to acquisition performance or acquisition performance led to increased

ownership. Results showed that acquisition announcement returns were positively associated

with higher stock holdings; however, stock ownership was not related to acquisition perfor-

mance, suggesting that performance begets ownership rather than vice versa. Consistent with

our earlier discussion in which acquisitions allow bidding firms’ managers to gain at the

expense of shareholders, Grinstein and Hribar (2004) found that CEOs with higher power

over their boards received larger acquisition bonuses; however, such bonuses did not trans-

late into increased stock returns. They also revealed that although more powerful CEOs

made larger acquisitions than lower power peers, the market responded more negatively to

these acquisition announcements.

In general, research examining the effects of equity holdings and incentive pay on acqui-

sition behavior and performance has returned mixed results. However, recent management

and finance research has suggested a troubling view of the role of equity-based rewards in

managerial decision making, as findings suggest that managers may engage in opportunistic

behaviors to achieve personal gain (Devers, Cannella, Reilly, & Yoder, 2007).

Managerial experience and cognition/personality. The characteristics of managers have also

been shown to exhibit important influences on acquisition decisions and acquisition perfor-

mance. For example, the market appears to value the expertise and knowledge held by key tar-

get executives, as their postacquisition departures have been shown to negatively affect both

acquisition performance (Cannella & Hambrick, 1993; Krishnan, Miller, & Judge, 1997) and

bidding firms’ satisfaction with acquisition decisions (Saxton & Dollinger, 2004). Furthermore,

research suggests that cognitive influences figure importantly into acquisition performance.

Specifically, perceptions of task, cultural, and political characteristics (Pablo, 1994), and CEOs’

perceptions of invulnerability (hubris; Hayward & Hambrick, 1997) affect managers’ acquisi-

tion judgments and acquisition performance. Other research has shown that top managers’ per-

ceptions of cultural differences between bidders and targets have negatively affected both bidder

announcement returns (Chatterjee, Lubatkin, Schweiger, & Weber, 1992) and managers’ per-

ceptions of postmerger performance (Very, Lubatkin, Calori, & Veiga, 1997). This desire for fit

is consistent with research showing that strategic similarity (Ramaswamy, 1997) and alliance

experience between bidders and targets (Porrini, 2004) enhanced synergy realization during

integration and, in turn, positively influenced long-term postacquisition accounting returns.

Firm Characteristics

Historical performance. Scholars have paid particular attention to the role of historical

operating performance in acquisition events. For example, Heron and Lie (2002) showed that

acquirers experienced strong operating performance both before and after acquisitions and,

furthermore, that postacquisition performance increased when bidders with higher market-

to-book ratios acquired targets with low market-to-book ratios. Using another performance

measure, Lang, Stulz, and Walkling (1989) reported that high Tobin’s Q bidders gained more

than low Tobin’s Q bidders and, additionally, low Tobin’s Q targets benefited more from

takeovers than high Tobin’s Q targets. Similarly, Servaes (1991) found that bidders’ abnormal

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

482 Journal of Management / June 2009

returns were also higher when their Tobin’s Q ratios were higher and increased further with

decreases in targets’ Tobin’s Q ratios. In a test of Jensen’s (1986) free cash flow hypothesis

(managers endowed with free cash flow will invest it in negative net present value projects

rather than pay it out to shareholders), Lang, Stulz, and Walkling (1991) found that bidder

announcement returns were negatively related to cash flow for low Tobin’s Q bidders but not

related to cash flow for high Tobin’s Q bidders. Similar to Rau and Vermaelen (1998), the

authors concluded that firms with agency problems (low Tobin’s Q ratios) appeared to invest

in negative net present value projects, including acquisitions. In a somewhat related vein,

Bruner (1988) found that the combination of slack-rich (cash and unused debt capacity) bid-

ders and slack-poor targets created positive combined bidder-target announcement returns,

again implying the importance of prior performance for acquisition returns.

Not surprisingly, taken together, this evidence suggests that acquisition performance

increases when high-performing firms pair with low-performing targets. This perhaps results

because low-performing targets offer upside restructuring value, which has been shown to

offer the greatest opportunity for value creation in takeovers (Chatterjee, 1992) and bank

mergers (Houston et al., 2001). Although this suggests some benefit in picking the low-

hanging fruit, Agrawal and Jaffe (2003) found little evidence to support the common con-

tention that all takeover targets’ preacquisition operating and stock returns were poor. Thus,

although the takeover market is often viewed as a disciplinary mechanism, acquisitions are

undertaken for a variety of reasons. Furthermore, although acquiring low-performing firms

may offer value, research by Clark and Ofek (1994) suggests this relationship may have

boundary conditions, as they found that bidders were generally unable to successfully

restructure severely distressed firms and, as a result, acquiring deeply troubled targets

decreased acquirers’ long-term accounting and market returns. Thus, there appear to be

diminishing returns for poor target performance; hence, picking the lowest hanging fruit

may not be the wisest path to wealth creation.

Firm size. Scholars have also argued that firm size affects the performance of acquisitions.

In support, some studies have found that large mergers produced positive postacquisition

accounting performance, which the authors attributed to increased asset productivity (Healy

et al., 1992) and enhanced customer attraction, employee productivity, and asset growth

(Cornett & Tehranian, 1992). Conversely, however, S. B. Moeller, Schlingemann, and Stulz

(2004) found that small acquisitions by small acquirers resulted in positive announcement

gains, whereas large acquisitions by large acquirers resulted in significant announcement

losses. Findings indicated that large firms not only offered larger acquisition premiums than

smaller firms, but they were also more likely to complete an offer, suggesting that manager-

ial hubris played more of a role in the acquisition decisions of large firms than of small firms.

In a related vein, Fuller et al. (2002) partitioned the returns to acquirers on the relative size of

the target as compared to the bidder and found that for public targets, as the relative size of

the target increased, returns became more positive for cash offers, more negative for stock

offers, and changed little for combination offers. They also found, however, that for private

acquisitions, as the relative size of the target increased, returns accrued by stock-financing

bidders were greater than those accrued by cash-financing bidders. Whereas firm size appears

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

Haleblian et al. / Mergers and Acquisitions 483

to influence acquisition returns in important ways, the mixed results inherent in this work

illustrate that an understanding of how this effect manifests is underdeveloped. Thus, the role

of firm size in acquisition performance remains a fertile area for acquisition research.

Acquirer experience. Acquisition scholars have also examined the role of acquirers’ expe-

rience on acquisition performance. Although it seems intuitive that acquisition experience

should positively affect the performance of subsequent acquisitions, the results of these stud-

ies are mixed, suggesting moderating influences. Haleblian and Finkelstein (1999) found

that the relationship between acquisition experience and acquisition performance was U-

shaped, not positively linear. The authors concluded that these results are owed to the notion

that inexperienced acquirers inappropriately applied experience garnered from first acquisi-

tions to following dissimilar acquisitions, whereas highly experienced acquirers were able to

avoid these missteps. Discussing the moderating influence of task heterogeneity on organi-

zational learning, Zollo and Winter (2002) offer support for this conclusion, arguing that

high heterogeneity in organizational tasks such as acquisition decisions increases the likeli-

hood of erroneous generalizations because of an overreliance on tacit knowledge accumula-

tion. They hypothesized that when the heterogeneity of task experiences is high, as is often

the situation facing infrequent and inexperienced acquirers, firms employing explicit knowl-

edge articulation and codification mechanisms, as opposed to those relying on tacit knowl-

edge accumulation, will reap additional learning benefits resulting in more effective decision

making. In support of this hypothesis, Zollo and Singh (2004) found that prior acquisition

experience alone did not positively influence acquisition performance, whereas knowledge

codification of experience did. More recently, in a study of the most active U.S. acquirers in

the 1990s, Laamanen and Keil (2008) found that although both high rate of acquisitions and

high variability of the rate were negatively related to performance, the relationship was

weakened through the moderating effects of an acquirer’s size, the scope of its acquisition

program, and acquisition experience.

Examining the role that transfer effects played in multiple acquisitions, Finkelstein and

Haleblian (2002) found that (a) bidder-to-target similarity increased announcement returns, a

finding indicative of a positive transfer effect, and (b) firms’ first acquisitions outperformed

their second acquisitions, particularly when those acquisitions were made in dissimilar indus-

tries, a finding indicative of a negative transfer effect. These results suggest that although rou-

tines and practices transfer from prior to new situations, positive transfer is dependent on

similarity. Hayward (2002) found that acquisition experience increased acquisition perfor-

mance when targets were not markedly similar to or dissimilar from previous acquisitions.

Collectively, this evidence suggests that although similarity is important, at higher levels, it

may exhibit diminishing returns for learning. Finally, although much of the experience and

learning literature focuses on learning by doing, Delong and Deyoung (2007) showed large

commercial banks learned not by engaging directly in repeated acquisitions, but indirectly by

observing other banks’ acquisition-related successes and failures. Therefore, in addition to

experiential learning and codification of knowledge, vicarious learning may be beneficial to

managers’ acquisition decisions.

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

484 Journal of Management / June 2009

Environmental Factors

Waves. Several scholars have proposed that temporal and episodic effects influence market

responses to acquisitions. Following this logic, some scholars have examined the performance

consequences of acquirers across different acquisition waves. For example, Banerjee and

Eckard (1998) found that acquisitions in the first great merger wave period resulted in signifi-

cant value creation for bidders and targets, as firms pursued greater efficiency. Analyzing a

later wave (1920s), however, Leeth and Borg (2000) reported that although targets gained from

being acquired, bidding firms neither gained nor lost. Conversely, Matsusaka (1993) found

that during the 1960s merger wave, acquiring firms accrued negative returns from related

acquisitions but received positive returns from diversifying acquisitions, particularly if target

managers were retained. Reexamining this wave, Hubbard and Palia (1999) found that the

greatest returns for diversifying acquisitions resulted when financially unconstrained bidders

acquired financially constrained targets, suggesting that investors viewed internal capital mar-

kets as more efficient than external capital markets. Although these results are fairly mixed,

they suggest that the strategic focus of acquisitions influences acquiring firm returns.

Although the work cited above focused on single waves, some researchers have examined

the consequences of moving between or within wave periods. For example, examining mul-

tiple waves, Matsusaka (1993) uncovered interesting changes in investor sentiment toward

diversification over time. Specifically, he noted that diversifying acquisitions resulted in pos-

itive bidder returns from 1968 to1974, neutral returns from 1975 to 1979, and negative

returns from 1980 to 1987. Although the reasons behind this sentiment shift are unclear, he

suggested that it may owe to first-mover effects, regulation such as the Williams Act of 1968

(Malatesta & Thompson, 1993), and exogenous shocks or changes in fads and fashions

regarding acquisitions. In a more recent study, S. B. Moeller et al. (2004) demonstrated that

although, in aggregate, acquiring firms’ shareholders experienced greater losses during the

1998-2001 wave than during the 1980s wave, more recent losses resulted from a few

extremely large loss deals, suggesting the importance of controlling for outliers.

Still other scholars have examined the effects of acquiring at different stages within acquisi-

tion waves. For example, Carow et al. (2004) found moving early in acquisition waves resulted

in higher combined target-bidder abnormal returns. However, they further reported that early

moving bidders accrued positive returns only when they possessed superior information, paid

with cash, and expanded in related industries during widespread expansion periods. In a more

fine-grained analysis of the performance consequences of acquiring at different wave stages,

McNamara, Haleblian, and Dykes (2008) revealed that, on average, firms that acquired early

within an industry acquisition wave achieved positive returns, whereas the market punished

later acquirers. Although these results underscored the importance of ordering, interestingly,

their data also revealed that although returns werse positive for early acquirers and negative for

later acquires, returns began to improve for firms acquiring at the farthest point of the wave.

They concluded that the worst returns might have resulted from acquirers’ falling prey to band-

wagon imitation, whereas acquirers at the far end of waves may have benefited from learning

by observing and reduced bandwagon pressures. Finally, acquiring during low-equity market

cycles has been shown to generate higher announcement returns than during high-equity

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

Haleblian et al. / Mergers and Acquisitions 485

market cycles, suggesting that managers are less likely to overpay for acquisitions when equity

market cycles are low (Pangarkar & Lie, 2004).

Regulations. Scholars have also shown that regulatory events can influence the attrac-

tiveness of acquiring (e.g., Tax Reform Act of 1986) and shift the bidder–target power rela-

tionship (e.g., Williams Act of 1968). Specifically, evidence has suggested that regulatory

reforms have been detrimental to bidder returns (Asquith, Bruner, & Mullins, 1983;

Malatesta & Thompson, 1993; Schipper & Thompson, 1983) yet beneficial to target returns

(Bradley et al., 1988). Similarly, recent strategic risk-taking research has found that regula-

tory changes resulting from the implementation of the Sarbanes-Oxley Act (SOX) have

influenced CEOs’ strategic decisions (Devers, McNamara, Wiseman, & Arrfelt, 2008).

Although we found no studies directly examining how recent regulatory changes influenced

acquisition performance, the work cited above suggests that future research considers SOX

and other forthcoming regulatory changes.

As with work on antecedents, although many moderating variables have been offered that

improve acquisition performance, it is currently unclear which of these moderators have the

greatest impact on improving shareholder value. Moreover, given that scholars have been able

to isolate some conditions in which acquirers generate value, it remains puzzling as to why

acquisitions on average still perform poorly. It may be that scholarly insights are not transfer-

ring to practitioners, they are impractical or unfeasible to execute, or although they produce

“statistical significance” that justifies publication in academic journals, they do not generate

sufficient increased shareholder value to justify implementation. Regardless of the reason, it is

clear that developing a deeper understanding of these moderating influences is necessary.

Other Acquisition Outcomes

In addition to acquisition performance, a smaller number of studies have examined other

consequences associated with acquisitions. There is an implicit assumption, as well as some

empirical evidence, that lower acquisition premiums lead to better acquisition performance

(Hayward & Hambrick, 1997). Although a likely mediating variable, acquisition premiums

have also been studied without mention of their relationship to other measures of perfor-

mance and thus are often considered a relevant dependent variable on their own. Aside from

premiums, the most commonly examined nonperformance outcomes are turnover and cus-

tomer and bondholder consequences.

Acquisition premium. In general, an acquisition premium is measured by the difference

between the purchase price of the target firm’s stock, paid by the acquiring firm, and the

target’s pre-acquisition stock price, divided by the target’s pre-acquisition stock price.

Whereas finance studies have focused on target influences on premium price, management

studies have concentrated more on the acquirers and their motivations to acquire. The

finance literature has examined target tactics aimed at influencing acquisition premiums

and/or the likelihood of being acquired. The 1980s saw an increase in corporate anti-

takeover methods, as many firms adopted shareholder rights plans (poison pills). Evidence

showed in the broad market that although poison pills were associated with higher

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

486 Journal of Management / June 2009

takeover premiums, they did not decrease acquisition activity (Comment & Schwert,

1995). However, in the specific context of IPO firms, although the presence of takeover

defenses had no effect on takeover premiums, they were negatively related to subsequent

acquisition likelihood (Field & Karpoff, 2002), which is consistent with the idea that man-

agers take steps at the time of the IPO to ensure the continuation of their personal benefits

of control, as takeover defenses help firms remain independent after IPO. Another tactic

targets have used to their advantage is a termination fee. Research has shown that such

clauses result in both higher success rates and higher premiums, suggesting that target

managers use such fees to encourage bidder participation by ensuring that the bidder is

compensated for the revelation of valuable private information released during merger

negotiations (Officer, 2003).

Other finance scholars have proposed that target managers with high levels of ownership

will resist takeovers unless they feel fully compensated for their loss of control. Following

this logic, acquisition premiums should be increasing with managerial ownership levels as

entrenched managers negotiate more vigorously (Song & Walkling, 1993). Supporting the

resistance argument, Song and Walkling (1993) found that eventual targets exhibited lower

levels of managerial ownership than industry peers and random nontargets. Furthermore,

returns to target firm shareholders increased with managerial ownership in contested but suc-

cessful acquisitions, indicating that managerial ownership can be beneficial to target share-

holders when it encourages bid resistance that leads to deal negotiation but not when such

resistance leads to deal termination. More recent research on bid negotiation has supported

the resistance argument (see Bruner, 1999; Burch, 2001; Holl & Kyriazis, 1997).

The finance literature has also focused on the influence of target shareholder control on pre-

miums. Findings have shown that targets highly controlled by shareholders also achieve higher

premiums. This result suggests that when target shareholders are weak and a target CEO is

strong, one way to entice target CEOs’ approval at a reduced price is for bidders to offer the

CEO a position in the merged firm. However, strong target shareholders appear to intervene in

such transactions and raise premiums (T. Moeller, 2005). Relatedly, the results of additional

studies have shown that targets with short-term institutional shareholders are more likely to

receive an acquisition bid and receive lower premiums. This finding suggests that firms held

by short-term investors hold weaker bargaining positions in acquisitions, which allows man-

agers to proceed with value-reducing acquisitions (Gaspar, Massa, & Matos, 2005).

In contrast to the majority of work in finance focusing on targets, one lone study examined

the influence of national investor protection on premiums. Consistent with the notion that

investor protection can create more active markets for acquisitions, findings showed that

investor protection (quality accounting standards, quality law enforcement, and shareholder

rights) resulted in higher premiums (Rossi & Volpin, 2004). Although this works suggests that

macrolevel factors including national culture may exhibit important influences on premiums,

and perhaps other aspects of acquisitions more generally (Stahl & Voigt, 2008), the area is

underdeveloped and thus presents a fruitful opportunity for future research.

It is interesting that management scholars have focused more on bidders than targets,

specifically their motivations to acquire. Consistent with this notion, indicators of CEO

hubris were highly associated with the size of premiums paid (Hayward & Hambrick, 1997).

As discussed earlier, network ties have been shown to influence premiums such that the

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

Haleblian et al. / Mergers and Acquisitions 487

premiums paid by acquirers were related to premiums previously paid by board interlock

partners (Haunschild, 1994). Furthermore, firms tied to other firms with heterogeneous prior

premium experience tended to pay less for acquisitions than those tied to partners with more

homogeneous experience (Beckman & Haunschild, 2002). More recently, Laamanen (2007)

showed that premiums might be higher when target firms’ resources were intangible and that

such intangibles-related premiums did not cause negative abnormal returns. Using acquisi-

tions as a context to study such resource diffusion and learning processes, all three of these

studies suggest the importance of interorganizational knowledge transfer for acquisition pre-

miums, thus pointing to acquisitions as a fertile area for the study of organizational learning.

Turnover. The finance field has drawn primarily on agency theory views to understand the

relationship between acquisitions and governance, and although some management scholars

have likewise employed this perspective, others have studied the governance and leadership

consequences of acquisitions through much more of a resource-based lens. Focusing more on

firm-level, strategic consequences, the management literature has not regarded acquisition-

driven top management turnover as a logical and productive consequence. Instead, building

on Cannella and Hambrick’s (1993) argument that top management team turnover reflects a

loss of firm and industry knowledge, the management literature has viewed top management

turnover as an unintended loss of human resources valuable to the firm. Haveman (1995)

found acquisitions in the financial services industry resulted in increased exit by top managers

in the acquiring firm, especially more senior executives, resulting in a top management team

with reduced average tenure. A number of management studies have found that target firms

experience a higher than normal turnover of top managers (Krug & Hegarty, 1997; Walsh,

1988, 1989). Additional research has indicated that top management turnover in target firms

is moderated by key aspects of acquisitions. Specifically, target firm turnover is higher when

the acquiring firm is foreign (Krug & Hegarty, 1997), when managers perceive significant cul-

tural differences between the acquiring and the target firm (Lubatkin, Schweiger, & Weber,

1999), and when managers view the merger announcement negatively or expect the merger to

have negative long-term professional consequences (Krug & Hegarty, 2001).

There is some evidence as well from the finance literature regarding the consequences of

acquisitions for board members; for instance, Harford (2003) showed that board members of

target firms typically lose their board positions and are often unable to replace them by mov-

ing to other boards. This suggests that there are tangible and reputational costs for board

members of target firms, highlighting a potential misalignment of interests between target

firm shareholders and their representatives, the board of directors.

In addition to executive turnover, scholars have also examined acquisition-related

employee turnover. For example, Fried, Tiegs, Naughton, and Ashforth (1996) found that sur-

viving middle managers’ perceptions of change in job control and postacquisition employee

termination fairness had important implications for subsequent commitment to work and

intentions to leave. Consistent with synergy and market for corporate control arguments,

O’Shaughnessy and Flanagan (1998) found that layoffs were more likely when acquisitions

combined related firms and when target firms were less efficient relative to industry peers. In

a more fine-grained analysis, Iverson and Pullman (2000) distinguished between the drivers

of voluntary versus involuntary turnover after acquisitions. Using a hospital industry sample,

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

488 Journal of Management / June 2009

they found that younger and white-collar workers were more likely to voluntarily leave after

an acquisition, whereas employees who were older, were blue-collar, and felt they received

less support from their coworkers were more likely to be laid off after an acquisition.

Combined, this work indicates that acquisitions often have negative implications for employees

but that certain classes of employees disproportionately perceive these consequences.

Customer and bondholder outcomes. The finance literature has also focused on the effect

of acquisitions on customers and bondholders. For example, A. N. Berger, Saunders, Scalise,

and Udell (1998) examined changes in lending to small business customers after bank acqui-

sitions. They found evidence that acquisitions led to reduced lending by acquiring banks but

that this reduction in lending was filled by increased lending by competing banks. They con-

cluded that acquisitions did not appear to have negative effects on this category of customers.

Looking more directly at acquisition effects on particular borrowers, Karceski, Ongena, and

Smith (2005) found that, in reaction to bank acquisition announcements, borrowers of target

banks experienced negative stock returns whereas borrowers of the acquiring bank experi-

enced positive stock returns. They concluded that the market reaction is negative for target

bank borrowers, as these borrowers often switch banks after acquisitions and often incur sig-

nificant switching costs when doing so. Thus, the research suggests that acquisitions, at least

in the banking market, have limited, if any, negative consequences for customers in an aggre-

gate sense, but particular customers of target firms often suffer economic harm.

Finance scholars have also examined the effect of acquisitions on the bondholders of

acquiring and target firms, finding somewhat inconsistent results. In a general sample

of acquisitions, Billet, King, and Mauer (2004) found that the returns to bondholders of

acquiring firms were negative in response to acquisition announcements but that the returns

for target firm bondholders were positive—particularly when target firms’ bonds were

below investment grade. In a more focused sample of acquisitions in the banking industry,

Penas and Unal (2004) found positive returns to both acquiring and target firm bondhold-

ers. Although these findings provide some support that acquisitions reduce risk to bond-

holders, primary beneficiaries appear to be target bondholders.

After our review of the research of nonfinancial performance outcomes, we come to two

conclusions. First, acquisition premiums are underused in acquisitions research. More specifi-

cally, under the assumptions that acquiring firms attempt to pay the lowest premium possible

while concurrently deterring competing offers (Asquith, 1983; Bradley et al., 1988; Malatesta

& Thompson, 1993) and that the majority of the value of a target is reflected in its stock price

(Haunschild, 1994), we argue that acquisition premiums offer an effective proxy for managers’

strategic intentions, in that high premiums indicate both managers’ motivations to acquire and

their confidence in their abilities to extract value from the acquisition. Second, we surmise that

the effect of acquisitions on stakeholders other than shareholders (i.e., employees, customers,

rivals) has not been sufficiently examined, and thus, this area is ripe for future work.

Future Research Directions

Collectively, the management, finance, economics, sociology, and accounting literatures

have employed a rich and diverse set of methodologies to examine acquisition phenomena.

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

Haleblian et al. / Mergers and Acquisitions 489

Although this work has uncovered numerous notable findings, few attempts to synthesize

these insights across fields have emerged. Therefore, we turn attention to several opportuni-

ties for scholars to advance the understanding of acquisitions. Our suggestions for future

research are not intended to be exhaustive, but rather, they represent our perceptions of the

most impactful directions management scholars can pursue.

Antecedents

Although scholars have identified many acquisition antecedents, it remains unclear which

antecedents are primary, secondary, or tertiary triggers or how these factors may jointly oper-

ate on acquisition behavior. It is interesting that even the most basic questions remain unan-

swered: For example, are acquisitions driven more by a genuine profit motive (market power,

efficiency, asset redeployment, market discipline) or by managerial self-interest (hubris,

empire building to justify increased compensation)? We realize that empirical research is

reductionist by design, so we are not surprised that many individual factors that drive acqui-

sition behavior have been isolated. However, because multiple drivers have already been

determined, we suggest that, at this stage, the field might benefit from developing a deeper

understanding of the relative importance of, and contingency conditions associated with,

those established drivers.

We also see value in more fully examining the influence of governance mechanisms on

acquisition behavior. As noted earlier, executive compensation is but one facet of corporate

governance. A simplifying assumption underlying the agency theory perspective is that

shareholders hold homogenous profit maximization interests. Also assumed is that large

shareholders fulfill external monitoring roles and, furthermore may initiate takeovers or

other activist measures, to discipline ineffective management (Shleifer & Vishny, 1997).

Nevertheless, evidence shows that large shareholders often seek opportunistic interests and

can have heterogeneous interests and objectives, which may or may not align with the goals

of other shareholders (Claessens, Djankov, Fan, & Lang, 2002; La Porta, Lopez-De-Silanes,

Shleifer, & Vishny, 2000; Shleifer & Vishny, 1997). Furthermore, in the United States, recent

years have witnessed the emergence of powerful and active minority shareholders, such as

rapidly growing hedge funds or activist investors, who often seek to pressure managers into

transactions (e.g., acquisitions or divestitures) that hold benefit for them yet, arguably, are

not always in the best interests of the broader shareholder base (Anabtawi, 2006).

Paralleling these issues are those related to choices between the antecedents of IPOs and

acquisitions as value creation vehicles. We have noted the burgeoning literature on acquisitions,

and there is similar growth in attention to the antecedents of IPOs. And although executives and

other stakeholders like investment firms increasingly make tradeoffs between taking a business

public and finding a strategic buyer and sometimes “tee up” a future acquisition by taking a firm

or business unit public, rarely do we see these topics linked in academic studies (Reuer & Shen,

2003). As noted earlier in our review, recent work (Field & Karpoff, 2002) suggests that there

is a relationship between what IPO managers do following an offering and subsequent acquisi-

tion, but beyond this very general understanding, we know little about how tradeoffs between

IPO and acquisition as value creation vehicles are managed or staged.

Downloaded from jom.sagepub.com at RYERSON UNIV on December 2, 2014

490 Journal of Management / June 2009

Collectively, these factors give rise to this question: How are changing trends in corporate gov-

ernance regulation, shareholder demographics, and shareholder activism—labeled the move

toward “shareholder democracy” (Anabtawi & Stout, 2008)—affecting decisions around when

and if to acquire? Scholars have only begun to examine how the governance structures of

acquiring firms influence whether managers enrich shareholders or themselves by growing the

firm through acquisitions (Kroll et al., 1997). For instance, Kroll, Walters, and Wright (2008)

found that vigilant boards rich in relevant experience were associated with superior acquisition

outcomes. Thus, we encourage research that more fully examines the role of ownership and