Вам также может понравиться

- Valuations 1: Introduction To Methods of ValuationДокумент17 страницValuations 1: Introduction To Methods of ValuationNormande RyanОценок пока нет

- Foreign Exchange ManagementДокумент21 страницаForeign Exchange ManagementSreekanth GhilliОценок пока нет

- April 2021 Assignment: There Is One (1) Page of Question, Excluding This PageДокумент17 страницApril 2021 Assignment: There Is One (1) Page of Question, Excluding This PageNayodya WorkОценок пока нет

- RTM Company ProfileДокумент10 страницRTM Company ProfileBy StandОценок пока нет

- SM Assignment PDFДокумент21 страницаSM Assignment PDFSiddhant SethiaОценок пока нет

- BreakEvenPointAnalysis and Selling PriceДокумент8 страницBreakEvenPointAnalysis and Selling PriceAnonymous zOo2mbaVAОценок пока нет

- Ch4-Change CommunicationsДокумент18 страницCh4-Change CommunicationsMohammed NafeaОценок пока нет

- Cashflow EnecoДокумент14 страницCashflow EnecoRusli HasanОценок пока нет

- Surface Facilities 2 PDFДокумент54 страницыSurface Facilities 2 PDFBadzlinaKhairunizzahraОценок пока нет

- Waste to Energy in the Age of the Circular Economy: Compendium of Case Studies and Emerging TechnologiesОт EverandWaste to Energy in the Age of the Circular Economy: Compendium of Case Studies and Emerging TechnologiesРейтинг: 5 из 5 звезд5/5 (1)

- Estimasi Budget and Profit + CostДокумент2 страницыEstimasi Budget and Profit + CostD.b. TampubolonОценок пока нет

- 03.OPERATIONAL FMC 5 YrsДокумент17 страниц03.OPERATIONAL FMC 5 YrsJoshwa SimamoraОценок пока нет

- Cash Flow Mining Operation SamarindaДокумент3 страницыCash Flow Mining Operation SamarindaRatmokoAdiNugrohoОценок пока нет

- ANALISIS BAJET PRODUKSI (Hauler DT) IwanДокумент6 страницANALISIS BAJET PRODUKSI (Hauler DT) Iwanagus triyantoОценок пока нет

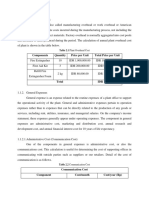

- Components Quantity Price Per Unit Total Price Per Unit: Table 2.1 Plant Overhead CostДокумент4 страницыComponents Quantity Price Per Unit Total Price Per Unit: Table 2.1 Plant Overhead CostFaldy FariskiОценок пока нет

- Profit & Loss Statement February 2022: Jalan Ciwalen 908Документ24 страницыProfit & Loss Statement February 2022: Jalan Ciwalen 90825Salwaa Nabillah RОценок пока нет

- Fixed Cost Assumption Assumption Component Amount Uom RemarksДокумент3 страницыFixed Cost Assumption Assumption Component Amount Uom RemarksQueen AshleyОценок пока нет

- Truck Delivery CostДокумент6 страницTruck Delivery CostSuwardi CatacanaОценок пока нет

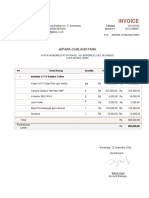

- Contoh Invoice Pemasangan Jasa CCTVДокумент1 страницаContoh Invoice Pemasangan Jasa CCTVFahrur Ahmad50% (2)

- Profit & Loss (Accrual)Документ1 страницаProfit & Loss (Accrual)Bikin OrtubanggaОценок пока нет

- 7.3 Projected Profit Loss: IncomeДокумент10 страниц7.3 Projected Profit Loss: IncomeYusuf RaharjaОценок пока нет

- Profit & Loss (Accrual)Документ1 страницаProfit & Loss (Accrual)WINDA WIDIYANTIОценок пока нет

- Uas Spreadsheet Xakt KunciДокумент9 страницUas Spreadsheet Xakt KunciTiaraAngelОценок пока нет

- Contoh Laba RugiДокумент1 страницаContoh Laba RugiindriОценок пока нет

- Cost Structure Year 2018 2019: (Rp6,540,099,000) (Rp2,701,857,150) (Rp6,540,099,000) (Rp9,241,956,150)Документ3 страницыCost Structure Year 2018 2019: (Rp6,540,099,000) (Rp2,701,857,150) (Rp6,540,099,000) (Rp9,241,956,150)Martin Octavianus AstardiОценок пока нет

- Financial ConexionДокумент2 страницыFinancial ConexionarifОценок пока нет

- Profit & Loss (Accrual)Документ1 страницаProfit & Loss (Accrual)finta febriyantiОценок пока нет

- Profit & Loss (Accrual) - 2Документ1 страницаProfit & Loss (Accrual) - 2Fransiska RikaОценок пока нет

- InvoiceSPG Best Wok 2023Документ60 страницInvoiceSPG Best Wok 2023drieldrewzОценок пока нет

- Actual Cost Project Cost Budget - AMD Tiutali 30092022Документ3 страницыActual Cost Project Cost Budget - AMD Tiutali 30092022Andre DjamhurОценок пока нет

- Cash Forcasting GreenhouseДокумент13 страницCash Forcasting GreenhouseAdam MirzaОценок пока нет

- 02.ANA Profit & Loss (Accrual)Документ1 страница02.ANA Profit & Loss (Accrual)Ana Aulia RizqoОценок пока нет

- Profit & Loss (Accrual) SMK Pgri TurenДокумент1 страницаProfit & Loss (Accrual) SMK Pgri TurenHilma nazilaОценок пока нет

- Deskripsi Biaya Biaya Langsng A) Biaya Penataan Lahan: Biaya Alat Excavator TOTALДокумент13 страницDeskripsi Biaya Biaya Langsng A) Biaya Penataan Lahan: Biaya Alat Excavator TOTALoing mirzaОценок пока нет

- A. Analysis of Preparation of Balance Sheet and Ratio Analysis 1. Supporting Data A. Pro Forma Profit and Loss CompanyДокумент4 страницыA. Analysis of Preparation of Balance Sheet and Ratio Analysis 1. Supporting Data A. Pro Forma Profit and Loss CompanyhamzahОценок пока нет

- Financial Report Sep MasterДокумент13 страницFinancial Report Sep MasterRio RizaldiОценок пока нет

- IC Break Analys MInyak Goreng CurahДокумент40 страницIC Break Analys MInyak Goreng CurahDEPO KELAPA BANG WAHYUОценок пока нет

- Profit & Loss (Accrual) VVVVVVVVДокумент1 страницаProfit & Loss (Accrual) VVVVVVVVniarini12Оценок пока нет

- Profit & Loss (Acrual) RДокумент1 страницаProfit & Loss (Acrual) RRicky PamashaОценок пока нет

- Data Rab PLTMH CileatДокумент10 страницData Rab PLTMH Cileatkesiswaan smkn1legonkulonОценок пока нет

- Profit & Loss (Accrual)Документ1 страницаProfit & Loss (Accrual)Wahyu PrayogoОценок пока нет

- Summary ProjectДокумент1 страницаSummary ProjectDestra M HarisОценок пока нет

- Pengajuan Event KempekДокумент1 страницаPengajuan Event KempekAna Sholeh HataОценок пока нет

- Uas - Myob - 205134022 - Nurul Agni NursyahbaniДокумент5 страницUas - Myob - 205134022 - Nurul Agni NursyahbaniNur LaelahОценок пока нет

- 12 - Shella Endang - Akl 4 - Laba Rugi PDFДокумент1 страница12 - Shella Endang - Akl 4 - Laba Rugi PDFShella EndangОценок пока нет

- Perhitungan Linen VS Dispo CONTOHДокумент4 страницыPerhitungan Linen VS Dispo CONTOHPhil PhilipsОценок пока нет

- SPD Na 40 Pancaran Infinity, 1 Unit, Carry Out VesselДокумент4 страницыSPD Na 40 Pancaran Infinity, 1 Unit, Carry Out VesselArdiansyah SHОценок пока нет

- SPD RH 2023 2unit, Carry Out To WsДокумент4 страницыSPD RH 2023 2unit, Carry Out To WsArdiansyah SHОценок пока нет

- SPD Swadaya Met 42Документ4 страницыSPD Swadaya Met 42Ardiansyah SHОценок пока нет

- SPD VTR 454 Kota Rukun, CARRY OUT TO WSДокумент4 страницыSPD VTR 454 Kota Rukun, CARRY OUT TO WSArdiansyah SHОценок пока нет

- SPD Cat 4 Unit, Carry Out To WSДокумент4 страницыSPD Cat 4 Unit, Carry Out To WSArdiansyah SHОценок пока нет

- Profit & Loss (Accrual) - 1Документ1 страницаProfit & Loss (Accrual) - 1hartatiktatik556Оценок пока нет

- Laporan Keuangan Isi Ulang Air 3Документ6 страницLaporan Keuangan Isi Ulang Air 3Safarah Mulia AnwarОценок пока нет

- Winners' Financial ModelДокумент5 страницWinners' Financial ModelARCHIT KUMARОценок пока нет

- Travel Budget-22312090-Riyan Befi Yudistira-If 22 BДокумент1 страницаTravel Budget-22312090-Riyan Befi Yudistira-If 22 BRiyan Befi yudistiraОценок пока нет

- Cashflow Keripik SingkongДокумент8 страницCashflow Keripik SingkongAnnisa NovrizalОценок пока нет

- Perabotan Rumah Tangga No Item Merk HargaДокумент3 страницыPerabotan Rumah Tangga No Item Merk HargaSaldy AnwarОценок пока нет

- PDF JoinerДокумент6 страницPDF Joinermuthi'ah ulfahОценок пока нет

- Estimation MJДокумент1 страницаEstimation MJprasetyo bbiОценок пока нет

- Asg 4 Chap 2Документ8 страницAsg 4 Chap 2Ajeng FadillahОценок пока нет

- Expense Report: NO Katagori Harga Penawaran Rapp Realisasi BobotДокумент5 страницExpense Report: NO Katagori Harga Penawaran Rapp Realisasi BobotKiki VarelОценок пока нет

- Contoh Cash FlowДокумент9 страницContoh Cash FlowIrma Felicia WidjajaОценок пока нет

- Mobile Legend Build Apk: 1. Project ManagementДокумент5 страницMobile Legend Build Apk: 1. Project ManagementMardiansyah SigitОценок пока нет

- Rab DPP Golkar Plafon & PartisiДокумент5 страницRab DPP Golkar Plafon & PartisijhsudhsdhwuОценок пока нет

- PM Parts List - D6R2XL-TTT BULDOZERДокумент5 страницPM Parts List - D6R2XL-TTT BULDOZERSusti AwanОценок пока нет

- Profit & Loss (Accrual) SuciДокумент1 страницаProfit & Loss (Accrual) Suciniarini12Оценок пока нет

- Business Goals SimulationДокумент12 страницBusiness Goals SimulationArifin MasruriОценок пока нет

- Chapter 7 Ama 8 - DodoДокумент30 страницChapter 7 Ama 8 - DodoBadzlinaKhairunizzahraОценок пока нет

- Kasus 1: 50 % Propana + 50% N-ButanaДокумент2 страницыKasus 1: 50 % Propana + 50% N-ButanaBadzlinaKhairunizzahraОценок пока нет

- Scan Data PreliumДокумент5 страницScan Data PreliumBadzlinaKhairunizzahraОценок пока нет

- Design Constraints of Horizontal SeparatorДокумент2 страницыDesign Constraints of Horizontal SeparatorBadzlinaKhairunizzahraОценок пока нет

- Slug Catcher DLLДокумент28 страницSlug Catcher DLLBadzlinaKhairunizzahraОценок пока нет

- Design Contraints BadzДокумент2 страницыDesign Contraints BadzBadzlinaKhairunizzahraОценок пока нет

- Final Report - BadzДокумент36 страницFinal Report - BadzBadzlinaKhairunizzahraОценок пока нет

- Anti Stain Deodorant: Group 25Документ13 страницAnti Stain Deodorant: Group 25BadzlinaKhairunizzahraОценок пока нет

- Chemical Engineering Department, Faculty of Engineering, Universitas Indonesia, Depok, West Java, IndonesiaДокумент6 страницChemical Engineering Department, Faculty of Engineering, Universitas Indonesia, Depok, West Java, IndonesiaBadzlinaKhairunizzahraОценок пока нет

- Chemical Engineering Department, Faculty of Engineering, Universitas Indonesia, Depok, West Java, IndonesiaДокумент6 страницChemical Engineering Department, Faculty of Engineering, Universitas Indonesia, Depok, West Java, IndonesiaBadzlinaKhairunizzahraОценок пока нет

- Metode DiferentsialДокумент3 страницыMetode DiferentsialBadzlinaKhairunizzahraОценок пока нет

- Bab 3 - Ranya - RevisiДокумент4 страницыBab 3 - Ranya - RevisiBadzlinaKhairunizzahraОценок пока нет

- UopДокумент8 страницUopBadzlinaKhairunizzahraОценок пока нет

- Asma Dan AlergiДокумент7 страницAsma Dan AlergiBadzlinaKhairunizzahraОценок пока нет

- Concept Selection 25Документ42 страницыConcept Selection 25BadzlinaKhairunizzahraОценок пока нет

- Concept Semuaaa IIIДокумент53 страницыConcept Semuaaa IIIBadzlinaKhairunizzahraОценок пока нет

- POLYMATH Results: Multiple Linear RegressionДокумент1 страницаPOLYMATH Results: Multiple Linear RegressionBadzlinaKhairunizzahraОценок пока нет

- POLYMATH Results: Multiple Linear RegressionДокумент1 страницаPOLYMATH Results: Multiple Linear RegressionBadzlinaKhairunizzahraОценок пока нет

- POLYMATH Results: Multiple Linear RegressionДокумент1 страницаPOLYMATH Results: Multiple Linear RegressionBadzlinaKhairunizzahraОценок пока нет

- Analisis Farmasi Dasar - 1 REVДокумент126 страницAnalisis Farmasi Dasar - 1 REVBadzlinaKhairunizzahra100% (1)

- Metode DiferentsialДокумент3 страницыMetode DiferentsialBadzlinaKhairunizzahraОценок пока нет

- Cipro Flax inДокумент4 страницыCipro Flax inBadzlinaKhairunizzahraОценок пока нет

- Concept ScoringДокумент4 страницыConcept ScoringBadzlinaKhairunizzahraОценок пока нет

- Latihan No 1Документ37 страницLatihan No 1BadzlinaKhairunizzahraОценок пока нет

- UasssДокумент9 страницUasssBadzlinaKhairunizzahraОценок пока нет

- LuncheonДокумент1 страницаLuncheonBadzlinaKhairunizzahraОценок пока нет

- Wujud ZatДокумент84 страницыWujud ZatBadzlinaKhairunizzahraОценок пока нет

- LuncheonДокумент1 страницаLuncheonBadzlinaKhairunizzahraОценок пока нет

- Banking in JapanДокумент15 страницBanking in JapanWilliam C JacobОценок пока нет

- Kumar Mangalam Birla Committee - Docxkumar Mangalam Birla CommitteeДокумент3 страницыKumar Mangalam Birla Committee - Docxkumar Mangalam Birla CommitteeVanessa HernandezОценок пока нет

- CTM Macau v6 - May 17Документ4 страницыCTM Macau v6 - May 17gopiv2020Оценок пока нет

- 2 - m1 Sap OverviewДокумент64 страницы2 - m1 Sap OverviewOscar Edgar BarreraОценок пока нет

- ISE Group 4 Business Plan 2022Документ24 страницыISE Group 4 Business Plan 2022Munashe MudaburaОценок пока нет

- Case Study Using ITIL and PRINCE2 Powerpoint Noel ScottДокумент14 страницCase Study Using ITIL and PRINCE2 Powerpoint Noel Scottrillag5Оценок пока нет

- 0450 Y15 SM 1Документ10 страниц0450 Y15 SM 1nouraОценок пока нет

- Five Forces ModelДокумент6 страницFive Forces Modelakankshashahi1986Оценок пока нет

- Life Cycle CostingДокумент34 страницыLife Cycle Costingpednekar30Оценок пока нет

- International Trade TheoryДокумент6 страницInternational Trade TheoryMaxine ConstantinoОценок пока нет

- Performance Evaluation and CompensationДокумент34 страницыPerformance Evaluation and CompensationarunprasadvrОценок пока нет

- Joint Stock CompanyДокумент3 страницыJoint Stock CompanyBhoomi ShekharОценок пока нет

- NoteДокумент4 страницыNotesks0865Оценок пока нет

- MESFIN PROPOSALedДокумент17 страницMESFIN PROPOSALedethnan lОценок пока нет

- Section3 2Документ80 страницSection3 2aОценок пока нет

- Jinnah University For Women: Department: EnglishДокумент4 страницыJinnah University For Women: Department: EnglishHurain ZahidОценок пока нет

- Chapter 7: Net Present Value and Capital BudgetingДокумент6 страницChapter 7: Net Present Value and Capital BudgetingViswanath KapavarapuОценок пока нет

- C4 Strategic ManagementДокумент5 страницC4 Strategic ManagementAdnan ZiaОценок пока нет

- Souq Analysis DocumentДокумент20 страницSouq Analysis DocumentNoha NazifОценок пока нет

- Supply Chain Risk and Disruption Management OutlineДокумент4 страницыSupply Chain Risk and Disruption Management OutlineNgang PerezОценок пока нет

- Symrise AR08Документ156 страницSymrise AR08María Margarita RodríguezОценок пока нет

- AFS - Afghanistan Capital Markets AssessmentДокумент32 страницыAFS - Afghanistan Capital Markets AssessmentShayan0% (1)

- HDFC Bank DDPI - Resident Ver 2 - 17102022Документ4 страницыHDFC Bank DDPI - Resident Ver 2 - 17102022riddhi SalviОценок пока нет

- "Advanced": Business Model Canvas: TemplateДокумент9 страниц"Advanced": Business Model Canvas: TemplateWahid HasimОценок пока нет