Вам также может понравиться

- Fraud Risk MДокумент11 страницFraud Risk MEka Septariana PuspaОценок пока нет

- Risk & Controls ToolkitДокумент15 страницRisk & Controls Toolkitvivekan_kumar90% (10)

- Sox GC Ac SpreadsheetcompressedДокумент92 страницыSox GC Ac SpreadsheetcompressedSaugat BoseОценок пока нет

- Control Testing Vs Substantive by CPA MADHAV BHANDARIДокумент59 страницControl Testing Vs Substantive by CPA MADHAV BHANDARIMacmilan Trevor JamuОценок пока нет

- The Audit Risk ModelДокумент3 страницыThe Audit Risk ModelShane LimОценок пока нет

- 2015 SOx Guidance FINAL PDFДокумент35 страниц2015 SOx Guidance FINAL PDFMiruna RaduОценок пока нет

- Entity Control Risk MatrixДокумент5 страницEntity Control Risk Matrixdonmarquez100% (1)

- 2023 Annual Plan Risk ManagementДокумент60 страниц2023 Annual Plan Risk ManagementCatherineОценок пока нет

- Segregation of Duties ReviewДокумент4 страницыSegregation of Duties ReviewManishОценок пока нет

- Audit Risk Assessment Best PracticeДокумент10 страницAudit Risk Assessment Best PracticeEmily MauricioОценок пока нет

- Working Papers - Top Tips PDFДокумент3 страницыWorking Papers - Top Tips PDFYus Ceballos100% (1)

- Internal Controls 101Документ25 страницInternal Controls 101Arcee Orcullo100% (1)

- Risk Rating The Audit UniverseДокумент10 страницRisk Rating The Audit UniverseTahir IqbalОценок пока нет

- Auditing Theory and Practice NotesДокумент187 страницAuditing Theory and Practice NotesMoyo Clifford100% (1)

- Developing A Risk Based Internal Audit PlanДокумент43 страницыDeveloping A Risk Based Internal Audit PlanOSAMA ABUSKAR100% (1)

- Internal Financial Controls WIRC 24062017Документ141 страницаInternal Financial Controls WIRC 24062017Ayush KishanОценок пока нет

- Understanding Internal Financial ControlsДокумент27 страницUnderstanding Internal Financial ControlsCODOMAIN100% (4)

- Control Risk MatrixДокумент7 страницControl Risk Matrixmuhammad andri lowe100% (1)

- I General: Internal Audit ChecklistДокумент33 страницыI General: Internal Audit ChecklistHimanshu GaurОценок пока нет

- Controls in Ordering & PurchasingДокумент32 страницыControls in Ordering & PurchasingGrazel CalubОценок пока нет

- Impact and Likelihood ScalesДокумент3 страницыImpact and Likelihood ScalesRhea SimoneОценок пока нет

- Anti-Money Laundering and Combating The Financing of TerrorismДокумент124 страницыAnti-Money Laundering and Combating The Financing of TerrorismLaurette M. BackerОценок пока нет

- Risk Control MatrixДокумент18 страницRisk Control MatrixRemi AboОценок пока нет

- PURCHASE-TO-PAYMENT PROCESS ASSESSMENT REVIEWДокумент36 страницPURCHASE-TO-PAYMENT PROCESS ASSESSMENT REVIEWviswaja100% (1)

- ITGC Guidance 2Документ15 страницITGC Guidance 2wggonzaga0% (1)

- Risk Control Matrix Template: Name ObjectiveДокумент3 страницыRisk Control Matrix Template: Name ObjectiveKyaw HtutОценок пока нет

- Entity-Level Risk Assessment WorksheetsДокумент26 страницEntity-Level Risk Assessment WorksheetsChinh Lê ĐìnhОценок пока нет

- Internal Control ConceptsДокумент14 страницInternal Control Conceptsmaleenda100% (1)

- 155289907A-133 Compliance Internal Control ToolДокумент43 страницы155289907A-133 Compliance Internal Control ToolrajsalgyanОценок пока нет

- ISA Audit Guide 2010-01Документ243 страницыISA Audit Guide 2010-01Victor JacintoОценок пока нет

- Record-to-Report Risk Control MatrixДокумент30 страницRecord-to-Report Risk Control MatrixAswath SОценок пока нет

- IT audit checklist reviews controlsДокумент11 страницIT audit checklist reviews controlsមនុស្សដែលខកចិត្ត ជាងគេលើលោក100% (1)

- Information Technology General Controls LeafletДокумент2 страницыInformation Technology General Controls LeafletgamallofОценок пока нет

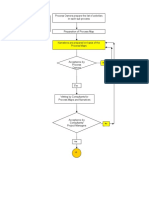

- Fund TransfersДокумент32 страницыFund TransfersvangieОценок пока нет

- SOX Activity FlowchartДокумент3 страницыSOX Activity Flowchartnarasi64100% (1)

- Internal Audit Training SyllabusДокумент2 страницыInternal Audit Training SyllabusIndra Permana SuhermanОценок пока нет

- Rbi A ManualДокумент344 страницыRbi A ManualAlexandru VasileОценок пока нет

- IIIB RICE Digital Audit ProgramsFromAuditNetДокумент100 страницIIIB RICE Digital Audit ProgramsFromAuditNetspicychaitu0% (1)

- At.01 Fundamentals of Assurance and Non Assurance EngagementsДокумент3 страницыAt.01 Fundamentals of Assurance and Non Assurance EngagementsAngelica Sanchez de VeraОценок пока нет

- IT Risk and Control FrameworkДокумент25 страницIT Risk and Control FrameworkAdityaNugrahaОценок пока нет

- Risk ControlДокумент7 страницRisk ControlDinesh AravindhОценок пока нет

- Chapter 4: Revenue CycleДокумент12 страницChapter 4: Revenue CycleCyrene CruzОценок пока нет

- CPF Annual Report 2020Документ22 страницыCPF Annual Report 2020AlioОценок пока нет

- Segregation of Duties Framework OverviewДокумент2 страницыSegregation of Duties Framework OverviewChinh Lê ĐìnhОценок пока нет

- SOX OverviewДокумент29 страницSOX Overviewnarasi64100% (2)

- Draft RCM - ExpensesДокумент9 страницDraft RCM - ExpensesAbhishek Agrawal100% (1)

- 2018 Internal Audit CharterДокумент4 страницы2018 Internal Audit CharterAlezNg100% (1)

- Purchasing Payables ControlДокумент9 страницPurchasing Payables ControljenjenheartsdanОценок пока нет

- Handbook - On - Professional - Opportunities in Internal AuditДокумент278 страницHandbook - On - Professional - Opportunities in Internal Auditahmed raoufОценок пока нет

- True & FalseДокумент13 страницTrue & FalseYasir Ali Gillani100% (2)

- Steam AppidДокумент38 страницSteam AppidMikey Chua67% (3)

- Internal Controls Guidance - Audit and Compliance ServicesДокумент15 страницInternal Controls Guidance - Audit and Compliance Servicestunlinoo.067433Оценок пока нет

- Risk Register FormatДокумент24 страницыRisk Register FormatShyam_Nair_9667Оценок пока нет

- It Audit Risk MatrixДокумент16 страницIt Audit Risk MatrixChinh Lê ĐìnhОценок пока нет

- Taxation Risk Control MatrixДокумент2 страницыTaxation Risk Control MatrixMitchell ShermanОценок пока нет

- Audit Universe and Risk Assessment ToolДокумент10 страницAudit Universe and Risk Assessment ToolAsis KoiralaОценок пока нет

- Uwex Internal Controls Plan 20102Документ89 страницUwex Internal Controls Plan 20102Deasy Nursyafira SariОценок пока нет

- Test of Controls For Some Major ActivitiesДокумент22 страницыTest of Controls For Some Major ActivitiesMohsin RazaОценок пока нет

- Business Risk Assessment - ERM ProcessДокумент26 страницBusiness Risk Assessment - ERM ProcesscarwadevilisbackОценок пока нет

- Financial Controls Closing ProcessДокумент16 страницFinancial Controls Closing Processvikrant durejaОценок пока нет

- E7 - TreasuryRCM TemplateДокумент30 страницE7 - TreasuryRCM Templatenazriya nasarОценок пока нет

- Sarbanes-Oxley (SOX) Project Approach MemoДокумент8 страницSarbanes-Oxley (SOX) Project Approach MemoManna MahadiОценок пока нет

- Interim IT SOX 2018 Preliminary FindingДокумент2 страницыInterim IT SOX 2018 Preliminary FindingT. LyОценок пока нет

- RiskMgt PolicyДокумент10 страницRiskMgt PolicyNeoОценок пока нет

- Information and Communication Audit Work ProgramДокумент4 страницыInformation and Communication Audit Work ProgramLawrence MaretlwaОценок пока нет

- Prevention of SpoilageДокумент1 страницаPrevention of SpoilagePlanco RosanaОценок пока нет

- Inventory Observation MemoДокумент5 страницInventory Observation MemoPlanco RosanaОценок пока нет

- Inventory Observation MemoДокумент5 страницInventory Observation MemoPlanco RosanaОценок пока нет

- Atsilab Form Meeting NoticeДокумент1 страницаAtsilab Form Meeting NoticeAneez AbdulJaleelОценок пока нет

- Inventory Control SpoilageДокумент63 страницыInventory Control SpoilagePlanco RosanaОценок пока нет

- Atsilab Form Meeting NoticeДокумент1 страницаAtsilab Form Meeting NoticeAneez AbdulJaleelОценок пока нет

- GuidelinesДокумент1 страницаGuidelinesPlanco RosanaОценок пока нет

- GuidelinesДокумент1 страницаGuidelinesPlanco RosanaОценок пока нет

- DistributionДокумент2 страницыDistributionPlanco RosanaОценок пока нет

- Sales and Receipts CycleДокумент52 страницыSales and Receipts Cyclejossiah13Оценок пока нет

- GuidelinesДокумент1 страницаGuidelinesPlanco RosanaОценок пока нет

- Audiying TheoryДокумент2 страницыAudiying TheoryPlanco RosanaОценок пока нет

- Audit Report Cash SalesДокумент30 страницAudit Report Cash SalesPlanco RosanaОценок пока нет

- Auditing Theory Key Concepts ExplainedДокумент12 страницAuditing Theory Key Concepts ExplainedKevin Ryan EscobarОценок пока нет

- Finacle Command - TM For Transaction Maintainance Part - I - Finacle Commands - Finacle Wiki, Finacle Tutorial & Finacle Training For BankersДокумент4 страницыFinacle Command - TM For Transaction Maintainance Part - I - Finacle Commands - Finacle Wiki, Finacle Tutorial & Finacle Training For BankersShubham PathakОценок пока нет

- Ankit Gautam ResumeДокумент3 страницыAnkit Gautam ResumeK.d. GargОценок пока нет

- Internal Halal Auditing Documents and MaДокумент20 страницInternal Halal Auditing Documents and Maquality wyzeОценок пока нет

- PTB Annual Report 2020Документ74 страницыPTB Annual Report 2020lurjnoaОценок пока нет

- Exact Globe UserGuide On FinancialsДокумент188 страницExact Globe UserGuide On Financialsaluaman100% (9)

- Illustrative Problem Worksheet AДокумент6 страницIllustrative Problem Worksheet AJoy SantosОценок пока нет

- Auditing-Unit 3-VouchingДокумент12 страницAuditing-Unit 3-VouchingAnitha RОценок пока нет

- CEO CFO COO Vice President in Canada Resume Kenneth TanДокумент3 страницыCEO CFO COO Vice President in Canada Resume Kenneth TanKennethTan2Оценок пока нет

- Red Book & Internal Auditing: Presented By: Maxene M. Bardwell, CPA, CIA, CFE, CISA, CIGA, CITP, CrmaДокумент78 страницRed Book & Internal Auditing: Presented By: Maxene M. Bardwell, CPA, CIA, CFE, CISA, CIGA, CITP, CrmaАндрей МиксоновОценок пока нет

- Advanced M AДокумент276 страницAdvanced M ADark PrincessОценок пока нет

- Sofi XP - Daftar IsiДокумент4 страницыSofi XP - Daftar IsiRobin GohОценок пока нет

- Accounting Changes in The Public Sector in EstoniaДокумент10 страницAccounting Changes in The Public Sector in EstoniaMohammad AlfianОценок пока нет

- Tax Deductions GuideДокумент14 страницTax Deductions GuideJEPZ LEDUNAОценок пока нет

- Intacc 1Документ17 страницIntacc 1Xyza Faye RegaladoОценок пока нет

- Presentation of COGS COST PratikshaДокумент16 страницPresentation of COGS COST PratikshasonalliОценок пока нет

- NSDL IAR New FormatДокумент20 страницNSDL IAR New FormatMansoor Ahmed Siddiqui0% (1)

- Fuje 1990Документ5 страницFuje 1990ibrahimОценок пока нет

- Portfolio Management Association of Canada: Reference Guide To Policies and Procedures For Portfolio ManagersДокумент20 страницPortfolio Management Association of Canada: Reference Guide To Policies and Procedures For Portfolio ManagersShaibyaОценок пока нет

- Corrective Action Report (Car) : Safety & Quality DirectorateДокумент26 страницCorrective Action Report (Car) : Safety & Quality DirectorateNAI HmamiОценок пока нет

- Steven Lim & Associates ProfileДокумент6 страницSteven Lim & Associates ProfileReika KuaОценок пока нет

- Assessment - FNSACC606Документ25 страницAssessment - FNSACC606tunhaОценок пока нет

- RSHBBA207171022215134Документ25 страницRSHBBA207171022215134Suraj MishraОценок пока нет

- Ca Inter NotesДокумент5 страницCa Inter NotesAjay RajputОценок пока нет