Вам также может понравиться

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeОт Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeРейтинг: 1 из 5 звезд1/5 (1)

- CP 9 Advanced Tax, Tax Deduction at Source and Introduction of Tax Collection at SourceДокумент108 страницCP 9 Advanced Tax, Tax Deduction at Source and Introduction of Tax Collection at Sourcesaravana pandianОценок пока нет

- Allowable Deductions From Gross Income - ReviewerДокумент4 страницыAllowable Deductions From Gross Income - RevieweryzaОценок пока нет

- RR 13-00Документ2 страницыRR 13-00saintkarri100% (2)

- Maybank Annual Report 2011Документ555 страницMaybank Annual Report 2011rizza_jamahariОценок пока нет

- KSB Pumps - Key Officials With ContactsДокумент3 страницыKSB Pumps - Key Officials With ContactsCatherine JovitaОценок пока нет

- VP Director IT Professional Services in Detroit MI Resume Rick PaulДокумент3 страницыVP Director IT Professional Services in Detroit MI Resume Rick PaulRickPaulОценок пока нет

- RR 13-2000Документ4 страницыRR 13-2000doraemoan100% (1)

- Shell International MarketingДокумент37 страницShell International MarketingParin Shah0% (1)

- Tds Amendements Via Finance Bill 2020Документ12 страницTds Amendements Via Finance Bill 2020ABHISHEKОценок пока нет

- June 2020 SP 1Документ7 страницJune 2020 SP 1Avinash ShettyОценок пока нет

- Deduction, Collection & Recovery of TaxesДокумент143 страницыDeduction, Collection & Recovery of TaxesjyotiОценок пока нет

- Nov 2019Документ39 страницNov 2019amitha g.sОценок пока нет

- Part I: Statutory Update: © The Institute of Chartered Accountants of IndiaДокумент4 страницыPart I: Statutory Update: © The Institute of Chartered Accountants of IndiaRamanОценок пока нет

- Delloite CIT (A) PDFДокумент7 страницDelloite CIT (A) PDFshashi vermaОценок пока нет

- Executive Programme (New Syllabus) Supplement FOR Tax LawsДокумент22 страницыExecutive Programme (New Syllabus) Supplement FOR Tax LawsJitendra RavalОценок пока нет

- Executive Programme (New Syllabus) Supplement FOR Tax LawsДокумент22 страницыExecutive Programme (New Syllabus) Supplement FOR Tax LawsShubham SarkarОценок пока нет

- Question and Answers Ques. No.1) Write Notes On: A.) Taxability of Deep Discount Bond - A Recent Move of The Central Board ofДокумент6 страницQuestion and Answers Ques. No.1) Write Notes On: A.) Taxability of Deep Discount Bond - A Recent Move of The Central Board ofAnamika VatsaОценок пока нет

- All About New TDS Section 194R and Section 194S - Taxguru - inДокумент7 страницAll About New TDS Section 194R and Section 194S - Taxguru - inParag Jain DugarОценок пока нет

- Statutory Updates For Nov-21 ExamsДокумент50 страницStatutory Updates For Nov-21 ExamsShodasakshari VidyaОценок пока нет

- Income Tax Amendments For May-2023Документ12 страницIncome Tax Amendments For May-2023Shubham krОценок пока нет

- TDS On Salaries - Income Tax Department, INDIAДокумент112 страницTDS On Salaries - Income Tax Department, INDIAArnav MendirattaОценок пока нет

- Changes in International TaxesДокумент4 страницыChanges in International TaxesManoj GuptaОценок пока нет

- CA CS CMA Final Statutory Updates For Nov Dec 2020Документ43 страницыCA CS CMA Final Statutory Updates For Nov Dec 2020Anu GraphicsОценок пока нет

- PK Budget Briefing EY 2019Документ86 страницPK Budget Briefing EY 2019IkhlasОценок пока нет

- Amity Global Business School, PuneДокумент15 страницAmity Global Business School, PuneChand KalraОценок пока нет

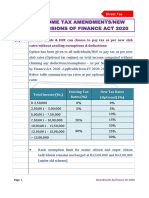

- Income Tax Amendments/New Provisions of Finance Act 2020Документ46 страницIncome Tax Amendments/New Provisions of Finance Act 2020shubhamworkОценок пока нет

- Nigeria - Highlights of Finance Act 2021 - EY - GlobalДокумент16 страницNigeria - Highlights of Finance Act 2021 - EY - GlobalAyodeji BabatundeОценок пока нет

- QUESTION: I Own A Commercial Building Giving Me A Rent of Rs. 4 Lakhs A Month. TheДокумент3 страницыQUESTION: I Own A Commercial Building Giving Me A Rent of Rs. 4 Lakhs A Month. TheCma Saurabh AroraОценок пока нет

- Latest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Документ0 страницLatest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Ketan ThakkarОценок пока нет

- Interim-Dividen-2021-22 - TDS-on-dividend-CommunicationДокумент4 страницыInterim-Dividen-2021-22 - TDS-on-dividend-CommunicationNimesh PatelОценок пока нет

- Finance Act 2024 Tax MeasuresДокумент46 страницFinance Act 2024 Tax Measuresetudiant etudiantsОценок пока нет

- Applicable Tax Deduction at Source Tds 2023Документ4 страницыApplicable Tax Deduction at Source Tds 2023Hemangi PrabhuОценок пока нет

- Budget 2021Документ15 страницBudget 2021RohitKumarDiwakarОценок пока нет

- One Advice For Investors Earning Dividend Income - Unlearn, Then Relearn!Документ6 страницOne Advice For Investors Earning Dividend Income - Unlearn, Then Relearn!Ramasayi Gummadi100% (1)

- Do You Know GST - August 2021Документ11 страницDo You Know GST - August 2021CA Ranjan MehtaОценок пока нет

- Changes in GSTДокумент4 страницыChanges in GSTRanjodh KaurОценок пока нет

- SKA - Sectionwise GST Analysis - Finance Bill 2021Документ24 страницыSKA - Sectionwise GST Analysis - Finance Bill 2021Sandip GoyalОценок пока нет

- Elective Ourse in Commerce ECO-11 Elements of Income TaxДокумент12 страницElective Ourse in Commerce ECO-11 Elements of Income TaxJai GorakhОценок пока нет

- Recent Amendments in TDS Under Income Tax - TVM BR CPE 03.09.2022Документ64 страницыRecent Amendments in TDS Under Income Tax - TVM BR CPE 03.09.2022sushant980Оценок пока нет

- Expenses Under Section 43B (H) - Taxguru - inДокумент4 страницыExpenses Under Section 43B (H) - Taxguru - inanascrrОценок пока нет

- Tax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeДокумент7 страницTax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeJouhara ObeñitaОценок пока нет

- 142 150Документ7 страниц142 150NikkandraОценок пока нет

- Decoding Indian Union BudgetДокумент6 страницDecoding Indian Union BudgetkumarОценок пока нет

- 30851ipcc May Nov14 It Vol1 CP 9.unlockedДокумент43 страницы30851ipcc May Nov14 It Vol1 CP 9.unlockedavesatanas13Оценок пока нет

- Article On Section 194Q and Common Queries TheretoДокумент5 страницArticle On Section 194Q and Common Queries TheretonamanojhaОценок пока нет

- TDS Under Sec 194A EtcДокумент26 страницTDS Under Sec 194A EtcDivyaОценок пока нет

- Tdsincometax (210621)Документ3 страницыTdsincometax (210621)Pallavi SharmaОценок пока нет

- Circular No 18 2022Документ6 страницCircular No 18 2022Manish KumarОценок пока нет

- Recent Amendments Companies Act 2013Документ39 страницRecent Amendments Companies Act 2013warner313Оценок пока нет

- 83 ITR 362 106 ITR 119: EditorДокумент3 страницы83 ITR 362 106 ITR 119: EditorKunwarbir Singh lohatОценок пока нет

- RMC 42-99 17533-1999-Amending - Revenue - Memorandum - Circular - No.Документ3 страницыRMC 42-99 17533-1999-Amending - Revenue - Memorandum - Circular - No.KC AtinonОценок пока нет

- Professional Programme (New Syllabus) Supplement FOR Advanced Tax LawsДокумент4 страницыProfessional Programme (New Syllabus) Supplement FOR Advanced Tax LawsPriyanga TОценок пока нет

- Tds Law and Practice: Under Income Tax Act, 1961Документ84 страницыTds Law and Practice: Under Income Tax Act, 1961Vaibhav ChauhanОценок пока нет

- How To Deal With 206AAДокумент5 страницHow To Deal With 206AAnamanojhaОценок пока нет

- Finance Act 2021 Major HighlightsДокумент6 страницFinance Act 2021 Major HighlightsAyodeji BabatundeОценок пока нет

- The Rigours of TDS - An OverviewДокумент31 страницаThe Rigours of TDS - An OverviewShaleenPatniОценок пока нет

- Using Relevant Examples Discuss The Importance of Board of Governors in An Institution of LearningДокумент10 страницUsing Relevant Examples Discuss The Importance of Board of Governors in An Institution of Learningivanongia2000Оценок пока нет

- India Of: SS, S A o OweveДокумент6 страницIndia Of: SS, S A o OwevevijayОценок пока нет

- ASC Group - Budget 2021 HighlightsДокумент32 страницыASC Group - Budget 2021 Highlightssaurav royОценок пока нет

- Citibank Nigeria Limited v. Lagos State Internal Revenue Service - Composition of Gross Income For Consolidated Relief Allowance - PedaboДокумент3 страницыCitibank Nigeria Limited v. Lagos State Internal Revenue Service - Composition of Gross Income For Consolidated Relief Allowance - PedaboAkinloluwa TokedeОценок пока нет

- 31188sm DTL Finalnew-May-Nov14 Cp28Документ66 страниц31188sm DTL Finalnew-May-Nov14 Cp28gvcОценок пока нет

- Requirements of Facilities Road Transportation For Disabilities MobilityДокумент20 страницRequirements of Facilities Road Transportation For Disabilities MobilityrayhanОценок пока нет

- Case OverviewДокумент3 страницыCase OverviewHeni Oktavianti50% (2)

- Firstmasterclass TB Progress Test 3 A4Документ4 страницыFirstmasterclass TB Progress Test 3 A4Adri ChОценок пока нет

- EcДокумент2 страницыEcArgie FlorendoОценок пока нет

- ROAD TO BASEL III - An International Banking Event - EgyptДокумент4 страницыROAD TO BASEL III - An International Banking Event - Egyptديفولوبرز للإستشارات والتدريبОценок пока нет

- OligopolyДокумент8 страницOligopolyYashsav Gupta100% (1)

- Labeling, Handling and Collection of Healthcare WasteДокумент28 страницLabeling, Handling and Collection of Healthcare WasteKanze AhiuОценок пока нет

- Special Power of AttorneyДокумент2 страницыSpecial Power of AttorneyjustineОценок пока нет

- Midterm 1 Winter 10 Answers Geography 213Документ11 страницMidterm 1 Winter 10 Answers Geography 213Michael HosaneeОценок пока нет

- Sewale Bitew PDFДокумент84 страницыSewale Bitew PDFTILAHUNОценок пока нет

- The Great DepressionДокумент15 страницThe Great DepressionRAahvi RAahnaОценок пока нет

- Características de Los Valores Que Negocian en El Segmento de Warrants, Certificados Y Otros Productos (Sistema de Interconexión Bursátil)Документ100 страницCaracterísticas de Los Valores Que Negocian en El Segmento de Warrants, Certificados Y Otros Productos (Sistema de Interconexión Bursátil)nicolasbaz01Оценок пока нет

- Statement OF Financial Interests: Nadc Form C-1Документ4 страницыStatement OF Financial Interests: Nadc Form C-1nebraskawatchdogОценок пока нет

- Annual Report 2017Документ158 страницAnnual Report 2017speedenquiryОценок пока нет

- Tax Invoice: Bhagyalaxmi Plastics (23-24) 30/2023-24 3-May-23Документ1 страницаTax Invoice: Bhagyalaxmi Plastics (23-24) 30/2023-24 3-May-23Avinash TiwariОценок пока нет

- Country Report MyanmarДокумент34 страницыCountry Report MyanmarAchit zaw tun myatОценок пока нет

- DCPD Editorial Ebook Till Sep 29, 19Документ181 страницаDCPD Editorial Ebook Till Sep 29, 19segnumutraОценок пока нет

- Boq 3Документ2 страницыBoq 3China AlemayehouОценок пока нет

- An Appraisal of Nigeria's Micro Small and Medium Enterprises MSMES Growth Challenges and Prospects.Документ15 страницAn Appraisal of Nigeria's Micro Small and Medium Enterprises MSMES Growth Challenges and Prospects.playcharles89Оценок пока нет

- Cost Analysis PaperДокумент6 страницCost Analysis PaperJeff MercerОценок пока нет

- Rs. 20 Lakh Crore Haryana Realestate ScamДокумент53 страницыRs. 20 Lakh Crore Haryana Realestate ScamSrini KalyanaramanОценок пока нет

- Green Et Al 2003.phil Fisheries in Crisis PDFДокумент89 страницGreen Et Al 2003.phil Fisheries in Crisis PDFMabelGaviolaVallenaОценок пока нет

- SWOT of Indian Banking SectorДокумент10 страницSWOT of Indian Banking SectorRashi AroraОценок пока нет

- PNB Overseas Directory PDFДокумент7 страницPNB Overseas Directory PDFReah Liza Padaoan SalvinoОценок пока нет

- Ignou - Challan (PNB)Документ1 страницаIgnou - Challan (PNB)GirdharОценок пока нет

- SLA Lead Goal CalculatorДокумент20 страницSLA Lead Goal CalculatorRejoy RadhakrishnanОценок пока нет