Вам также может понравиться

- Conquering the Seven Faces of Risk: Automated Momentum Strategies that Avoid Bear Markets, Empower Fearless Retirement PlanningОт EverandConquering the Seven Faces of Risk: Automated Momentum Strategies that Avoid Bear Markets, Empower Fearless Retirement PlanningОценок пока нет

- Managing Global Financial and Foreign Exchange Rate RiskОт EverandManaging Global Financial and Foreign Exchange Rate RiskОценок пока нет

- NJ India InvestДокумент43 страницыNJ India Investsachin100% (5)

- Derivatives Market Structure 2020 PRINT.20 2012 PDFДокумент16 страницDerivatives Market Structure 2020 PRINT.20 2012 PDFlaurence34Оценок пока нет

- 3Q18 Industrial Sentiment Survey October 2018Документ19 страниц3Q18 Industrial Sentiment Survey October 2018Mario Di MarcantonioОценок пока нет

- Asia Research - Stakeholder Survey 2021-22 (Final)Документ34 страницыAsia Research - Stakeholder Survey 2021-22 (Final)rikasusanОценок пока нет

- GIIN - 2019 Annual Impact Investor Survey - ExecSumm - WebfileДокумент8 страницGIIN - 2019 Annual Impact Investor Survey - ExecSumm - Webfilemonomono90Оценок пока нет

- Fintech SurveyДокумент22 страницыFintech Surveyali fatehiОценок пока нет

- Money Market Funds Survey ReportДокумент53 страницыMoney Market Funds Survey Reporttalwareswapnil5Оценок пока нет

- 2018 GIIN AnnualSurvey ExecutiveSummary WebfileДокумент8 страниц2018 GIIN AnnualSurvey ExecutiveSummary WebfileLaxОценок пока нет

- ISDA Future of Derivatives SurveyДокумент6 страницISDA Future of Derivatives SurveySimon AltkornОценок пока нет

- A Study On Investors Preferences Towards Various Investment Avenues in Capital Market With Special Reference To DerivativesДокумент10 страницA Study On Investors Preferences Towards Various Investment Avenues in Capital Market With Special Reference To Derivativesmehul_mistry_30% (1)

- UTI Aggressive Hybrid Fund (Formerly UTI Hybrid Equity Fund)Документ28 страницUTI Aggressive Hybrid Fund (Formerly UTI Hybrid Equity Fund)rinkuparekh13Оценок пока нет

- Stress Testing at Major Financial Institutions:: Survey Results and PracticeДокумент46 страницStress Testing at Major Financial Institutions:: Survey Results and Practicebing mirandaОценок пока нет

- July 14 Understanding The CommitmentДокумент3 страницыJuly 14 Understanding The Commitmentmecho satoОценок пока нет

- Research Note India's Hatchback IndustryДокумент11 страницResearch Note India's Hatchback IndustryVilluri BhargavОценок пока нет

- E Tailing Market - Clubfactory GMV - Ajio GMV - Redseer ConsultingДокумент10 страницE Tailing Market - Clubfactory GMV - Ajio GMV - Redseer ConsultingredseerОценок пока нет

- The State of Surveillance Storage 2018 SeagateДокумент14 страницThe State of Surveillance Storage 2018 SeagatePopa CatalinОценок пока нет

- In Consulting Strategy Bfs Consumerbehavior 062016 NoexpДокумент12 страницIn Consulting Strategy Bfs Consumerbehavior 062016 NoexpPhương TrầnОценок пока нет

- JaneStreet Inst ETF Trading Survey 2021Документ16 страницJaneStreet Inst ETF Trading Survey 2021Alan AnggaraОценок пока нет

- Eurex Factsheet - Msci - Index - Dividend - FuturesДокумент2 страницыEurex Factsheet - Msci - Index - Dividend - Futures0840328818zОценок пока нет

- Tink Open Banking Survey 2019Документ62 страницыTink Open Banking Survey 2019Anonymous 3fTQeuhBf100% (1)

- Accenture Investment Banking Survey ResearchДокумент12 страницAccenture Investment Banking Survey Researchjerry zaidiОценок пока нет

- Trust RadiusДокумент64 страницыTrust RadiusAshishОценок пока нет

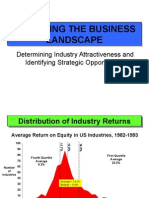

- Analyzing The Business LandscapeДокумент18 страницAnalyzing The Business Landscapedanic13Оценок пока нет

- 2023 WIND Ventures VC Survey On Latin America For Startup GrowthДокумент13 страниц2023 WIND Ventures VC Survey On Latin America For Startup GrowthWIND VenturesОценок пока нет

- Key Findings: Pe Exits: 2018 Annual African Private Equity Data TrackerДокумент1 страницаKey Findings: Pe Exits: 2018 Annual African Private Equity Data TrackerethernalxОценок пока нет

- Hypera Pharma ApresentaçãoДокумент97 страницHypera Pharma ApresentaçãoMilton Gioia NetoОценок пока нет

- Walmart Flipkart Ir PresentationДокумент17 страницWalmart Flipkart Ir PresentationVishal JaiswalОценок пока нет

- Zycus P2P Benchmark Report 2019 PDFДокумент33 страницыZycus P2P Benchmark Report 2019 PDFpradeepvedulaОценок пока нет

- State of PR 2022Документ69 страницState of PR 2022Nofa Haryanto Mch PrawiroОценок пока нет

- BLK 4Q22 Earnings SupplementДокумент15 страницBLK 4Q22 Earnings SupplementSatria MarhaendraОценок пока нет

- 360 ONE Balance Hybrid Fund NFO PresentationДокумент35 страниц360 ONE Balance Hybrid Fund NFO Presentationashish.sanghavi9218Оценок пока нет

- Future Proofing Your BrandДокумент37 страницFuture Proofing Your BrandOzzy López100% (2)

- Skill Up Report 2019Документ44 страницыSkill Up Report 2019v3n4Оценок пока нет

- Impact of Forex On Select It CompaniesДокумент49 страницImpact of Forex On Select It CompaniesvijayОценок пока нет

- Subodh Institute of Management&Career StudiesДокумент14 страницSubodh Institute of Management&Career Studieskaps_er_3Оценок пока нет

- First Round Capital Original Pitch DeckДокумент10 страницFirst Round Capital Original Pitch DeckFirst Round CapitalОценок пока нет

- First Round Capital Original Pitch DeckДокумент10 страницFirst Round Capital Original Pitch DeckJessi Craige ShikmanОценок пока нет

- BAI Business Agility Report 2018Документ22 страницыBAI Business Agility Report 2018Jean Paul Saltos100% (1)

- First Round Capital Slide Deck PDFДокумент10 страницFirst Round Capital Slide Deck PDFEmily StanfordОценок пока нет

- Brochure Columbia Value Investing 11 Sep 19 V9Документ16 страницBrochure Columbia Value Investing 11 Sep 19 V9iwazherОценок пока нет

- Puppet State of Devops Market Segmentation Report - 1Документ23 страницыPuppet State of Devops Market Segmentation Report - 1bhikshuОценок пока нет

- Determining The Optimal Capital Structure: A Practical Contemporary ApproachДокумент16 страницDetermining The Optimal Capital Structure: A Practical Contemporary ApproachAyudya Puti RamadhantyОценок пока нет

- Navigating Car Preferences Across Demographics - FINALДокумент18 страницNavigating Car Preferences Across Demographics - FINALgaya14Оценок пока нет

- Cftcsecac ArchardstudyДокумент3 страницыCftcsecac ArchardstudyMarketsWikiОценок пока нет

- Model 3 Cett ReportДокумент58 страницModel 3 Cett Reporthinduja987Оценок пока нет

- Industry Intelligence - Uber: Ridesharing Services Industry AnalysisДокумент31 страницаIndustry Intelligence - Uber: Ridesharing Services Industry AnalysisRediet TsigeberhanОценок пока нет

- Deloitte NL S&o Global Outsourcing Survey PDFДокумент17 страницDeloitte NL S&o Global Outsourcing Survey PDFRaitei AmanoОценок пока нет

- Coping With COVID-19: Research Education DialogueДокумент13 страницCoping With COVID-19: Research Education DialogueVito NarducciОценок пока нет

- Value Investing (Online) : Making Intelligent Investment DecisionsДокумент16 страницValue Investing (Online) : Making Intelligent Investment DecisionsPepe PerezОценок пока нет

- EA Report IFMR Goa Institute of Management FinGIMДокумент19 страницEA Report IFMR Goa Institute of Management FinGIMHomo SapienОценок пока нет

- 2020 Global Divestiture Survey: Defensive M&A For A Resilient PortfolioДокумент28 страниц2020 Global Divestiture Survey: Defensive M&A For A Resilient PortfoliokumarbipinshahОценок пока нет

- Know Your Behavioural BiasesДокумент44 страницыKnow Your Behavioural BiasesShreeraj ModiОценок пока нет

- Annual Report For The Year Ended December 31 2020Документ132 страницыAnnual Report For The Year Ended December 31 2020MuhammadОценок пока нет

- Under The Able Guidance of Mr. Shreyas Kasa Mr. Satyapal (Territory Manager) (Territory Manager)Документ36 страницUnder The Able Guidance of Mr. Shreyas Kasa Mr. Satyapal (Territory Manager) (Territory Manager)ambrosialnectarОценок пока нет

- Making AI A Killer App For Your Data - A Practical Guide - Sponsored by IBM Watson PresentationДокумент14 страницMaking AI A Killer App For Your Data - A Practical Guide - Sponsored by IBM Watson PresentationjombibiОценок пока нет

- IAPI Webinar-Pwc1Документ24 страницыIAPI Webinar-Pwc1IndriОценок пока нет

- Icici Prudential Asset Allocator Fund PPT - Jan - Investor - 2021Документ17 страницIcici Prudential Asset Allocator Fund PPT - Jan - Investor - 2021hackmeatakashОценок пока нет

- Making Foreign Direct Investment Work for Sub-Saharan AfricaОт EverandMaking Foreign Direct Investment Work for Sub-Saharan AfricaОценок пока нет

- Beyond The Last Blue Mountain - Group - 2Документ6 страницBeyond The Last Blue Mountain - Group - 2Amna NashitОценок пока нет

- Revenue and Gross Profit Operating Expenses: (Except For Per Share Items) Income StatementДокумент16 страницRevenue and Gross Profit Operating Expenses: (Except For Per Share Items) Income StatementAmna NashitОценок пока нет

- Dabur Chyawanprash - BriefДокумент12 страницDabur Chyawanprash - BriefAmna NashitОценок пока нет

- Ankit ResumeДокумент2 страницыAnkit ResumeAmna NashitОценок пока нет

- Egypt Oil and Gas OverviewДокумент5 страницEgypt Oil and Gas OverviewAmna NashitОценок пока нет

- Et - Manac - 2014 SolutionДокумент5 страницEt - Manac - 2014 SolutionAmna NashitОценок пока нет

- ElectivesДокумент21 страницаElectivesAmna NashitОценок пока нет

- GeologyДокумент5 страницGeologyAmna Nashit100% (1)

- Dea Annual Report 2015Документ29 страницDea Annual Report 2015Amna NashitОценок пока нет

- 9M16 Investor UpdateДокумент19 страниц9M16 Investor UpdateAmna NashitОценок пока нет

- Cantu-Chapa, 2009 Ammonites Taraises FMДокумент26 страницCantu-Chapa, 2009 Ammonites Taraises FMAmna NashitОценок пока нет

- Traveling Salesman Problem Theory and ApplicationsДокумент336 страницTraveling Salesman Problem Theory and ApplicationsAmna Nashit100% (1)

- Wind Speed Map IndiaДокумент12 страницWind Speed Map IndiaAn1rudh_Sharma100% (1)

- Invoice GPR PajakДокумент51 страницаInvoice GPR Pajakhandika CHОценок пока нет

- Ref No ECILДокумент1 страницаRef No ECILjude francoОценок пока нет

- Sale 238 26-06-2023Документ2 страницыSale 238 26-06-2023Creeper TechnologiesОценок пока нет

- Payslip Month of December 2022Документ1 страницаPayslip Month of December 2022Amir SohailОценок пока нет

- Demand Letter 2022Документ20 страницDemand Letter 2022Giovanni AlcainОценок пока нет

- Tabel Tugas 1Документ4 страницыTabel Tugas 1Nurul FajriahОценок пока нет

- Indian Rupee: People Also AskДокумент1 страницаIndian Rupee: People Also AskAadish ChopraОценок пока нет

- Aoog Aoq0 FT: Msble S66 0033O6 Customer GST No. 36aexpyo388 Na2Документ3 страницыAoog Aoq0 FT: Msble S66 0033O6 Customer GST No. 36aexpyo388 Na2A.T RamОценок пока нет

- GST InvoiceДокумент6 страницGST InvoiceChamundi MОценок пока нет

- Urban: Pay Date Cac No. Amount Paid Punch DateДокумент1 страницаUrban: Pay Date Cac No. Amount Paid Punch DateMONISH NAYARОценок пока нет

- Axis Bank Rent Diposite DetailsДокумент18 страницAxis Bank Rent Diposite DetailsBANGUR SADANОценок пока нет

- Establishment ListДокумент3 страницыEstablishment ListRiya100% (1)

- Program Kecemerlangan Akademik Sains Komputer Semester 2, Sesi 2018/ 2019Документ2 страницыProgram Kecemerlangan Akademik Sains Komputer Semester 2, Sesi 2018/ 2019mazlinaОценок пока нет

- Bank CodesДокумент2 094 страницыBank CodeskoinsuriОценок пока нет

- Soal UAS Bahasa Inggris Kelas 6 SD Semester 1 (Ganjil) Dan Kunci Jawaban (WWW - Bimbelbrilian.com) - DikonversiДокумент9 страницSoal UAS Bahasa Inggris Kelas 6 SD Semester 1 (Ganjil) Dan Kunci Jawaban (WWW - Bimbelbrilian.com) - DikonversiEKALIAS NOKA SITEPU100% (1)

- List of Currencies of All CountriesДокумент9 страницList of Currencies of All CountriesSilver SurferОценок пока нет

- RRB Postal ChallanДокумент1 страницаRRB Postal Challansudip mukherjeeОценок пока нет

- Bitumenemulsion PriceДокумент1 страницаBitumenemulsion PriceBinay SahooОценок пока нет

- Acp 2015 16 March16Документ2 страницыAcp 2015 16 March16L Sudhakar ReddyОценок пока нет

- SG Price List Dec 2020Документ2 страницыSG Price List Dec 2020Nor Hazwani SharifОценок пока нет

- Other STRBI Table No 20. Bank-Wise and Bank Group-Wise Gross Non-Performing Assets, Gross Advances, and Gross NPA Ratio of Scheduled Commercial BanksДокумент6 страницOther STRBI Table No 20. Bank-Wise and Bank Group-Wise Gross Non-Performing Assets, Gross Advances, and Gross NPA Ratio of Scheduled Commercial BanksPrasad KhandekarОценок пока нет

- S Poddar and Co ProfileДокумент35 страницS Poddar and Co ProfileasassasaaОценок пока нет

- Office Name Office Status Pincode Telephone No. Taluk (The Information Is Sorted District and Taluk Wise)Документ12 страницOffice Name Office Status Pincode Telephone No. Taluk (The Information Is Sorted District and Taluk Wise)Rishi Wadhwani100% (1)

- Tax Invoice / Bill of SupplyДокумент2 страницыTax Invoice / Bill of SupplyKrish JaiswalОценок пока нет

- Bill To Ship To: Signed by Ramesh Natarajan Date: 2023.06.24 13:35:13 IST Location: ChennaiДокумент1 страницаBill To Ship To: Signed by Ramesh Natarajan Date: 2023.06.24 13:35:13 IST Location: ChennaiVivek KhannaОценок пока нет

- Privatization: Name-Alisha Priyadarsini Class-Xii-B (Commerce) Roll No - 01Документ11 страницPrivatization: Name-Alisha Priyadarsini Class-Xii-B (Commerce) Roll No - 01Debahuti JenaОценок пока нет

- Receipt Jan 10Документ14 страницReceipt Jan 10Vivek PatilОценок пока нет

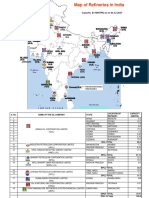

- RefineriesMap PDFДокумент2 страницыRefineriesMap PDFkutikuppalaОценок пока нет

- Embee's Audit Questionnaire (002) VIKASДокумент1 страницаEmbee's Audit Questionnaire (002) VIKASAsep SofyanОценок пока нет

- General Mathematics Performance Task # 2: LEADER: Jercy Constantino MembersДокумент4 страницыGeneral Mathematics Performance Task # 2: LEADER: Jercy Constantino MembersIvan CanosaОценок пока нет