Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- EMCEE ScriptДокумент3 страницыEMCEE ScriptSunshine Garson84% (31)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Due DiligenceДокумент7 страницDue Diligenceanand guptaОценок пока нет

- RB Group Case StudyДокумент1 страницаRB Group Case Studyanand gupta100% (1)

- CAMELS Ratios MethodologyДокумент4 страницыCAMELS Ratios Methodologyanand guptaОценок пока нет

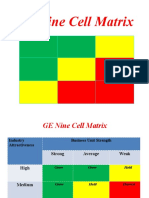

- GE MatrixДокумент13 страницGE Matrixanand guptaОценок пока нет

- GE MatrixДокумент13 страницGE Matrixanand guptaОценок пока нет

- Child LaborДокумент15 страницChild Laboranand guptaОценок пока нет

- AOLДокумент3 страницыAOLanand guptaОценок пока нет

- Internship Report On "Audit Procedures of A Chartered Accountant Firm"Документ2 страницыInternship Report On "Audit Procedures of A Chartered Accountant Firm"anand guptaОценок пока нет

- A Functional Project Done In: Analysis On Performance of Wipro and Infosys"Документ29 страницA Functional Project Done In: Analysis On Performance of Wipro and Infosys"anand guptaОценок пока нет

- Promotional Strategy of Dmart Influencing Consumer Buying BehaviourДокумент15 страницPromotional Strategy of Dmart Influencing Consumer Buying Behaviouranand guptaОценок пока нет

- A Summer Internship Project (SIP) Done in Asset Villa Financial AdvisorДокумент33 страницыA Summer Internship Project (SIP) Done in Asset Villa Financial Advisoranand guptaОценок пока нет

- Chapter 1: Introduction of The Project 1.1conceptДокумент37 страницChapter 1: Introduction of The Project 1.1conceptanand guptaОценок пока нет

- General Terms Conditions For Sales Purchases LPG and Chemical TankersДокумент34 страницыGeneral Terms Conditions For Sales Purchases LPG and Chemical TankersSally AhmedОценок пока нет

- Marking SchemeДокумент57 страницMarking SchemeBurhanОценок пока нет

- Lipura Ts Module5EappДокумент7 страницLipura Ts Module5EappGeniza Fatima LipuraОценок пока нет

- Integrative Assessment OutputДокумент2 страницыIntegrative Assessment OutputRonnie TambalОценок пока нет

- History and Culture of The Indian People, Volume 10, Bran Renaissance, Part 2 - R. C. Majumdar, General Editor PDFДокумент1 124 страницыHistory and Culture of The Indian People, Volume 10, Bran Renaissance, Part 2 - R. C. Majumdar, General Editor PDFOmkar sinhaОценок пока нет

- Pre-Qualification Document - Addendum 04Документ4 страницыPre-Qualification Document - Addendum 04REHAZОценок пока нет

- Fillomena, Harrold T.: ObjectiveДокумент3 страницыFillomena, Harrold T.: ObjectiveHarrold FillomenaОценок пока нет

- Literature ReviewДокумент11 страницLiterature ReviewGaurav Badlani71% (7)

- NPS Completed ProjectДокумент53 страницыNPS Completed ProjectAkshitha KulalОценок пока нет

- Sharmeen Obaid ChinoyДокумент5 страницSharmeen Obaid ChinoyFarhan AliОценок пока нет

- Glossary of Important Islamic Terms-For CourseДокумент6 страницGlossary of Important Islamic Terms-For CourseibrahimОценок пока нет

- Service Letter SL2019-672/CHSO: PMI Sensor Calibration RequirementsДокумент3 страницыService Letter SL2019-672/CHSO: PMI Sensor Calibration RequirementsSriram SridharОценок пока нет

- Susan Rose's Legal Threat To Myself and The Save Ardmore CoalitionДокумент2 страницыSusan Rose's Legal Threat To Myself and The Save Ardmore CoalitionDouglas MuthОценок пока нет

- Web Development AgreementДокумент3 страницыWeb Development AgreementRocketLawyer100% (2)

- Contemporary World Reflection PaperДокумент8 страницContemporary World Reflection PaperNyna Claire GangeОценок пока нет

- Eicher HR PoliciesДокумент23 страницыEicher HR PoliciesNakul100% (2)

- Albanian DialectsДокумент5 страницAlbanian DialectsMetaleiroОценок пока нет

- Analysis of Business EnvironmentДокумент6 страницAnalysis of Business EnvironmentLapi Boy MicsОценок пока нет

- Savage Worlds - Space 1889 - London Bridge Has Fallen Down PDFДокумент29 страницSavage Worlds - Space 1889 - London Bridge Has Fallen Down PDFPablo Franco100% (6)

- GR - 211015 - 2016 Cepalco Vs Cepalco UnionДокумент14 страницGR - 211015 - 2016 Cepalco Vs Cepalco UnionHenteLAWcoОценок пока нет

- Essentials of Economics 3Rd Edition Brue Solutions Manual Full Chapter PDFДокумент30 страницEssentials of Economics 3Rd Edition Brue Solutions Manual Full Chapter PDFsilas.wisbey801100% (11)

- NIST SP 800-53ar5-1Документ5 страницNIST SP 800-53ar5-1Guillermo Valdès100% (1)

- 2016 GMC Individuals Round 1 ResultsДокумент2 страницы2016 GMC Individuals Round 1 Resultsjmjr30Оценок пока нет

- WFP AF Project Proposal The Gambia REV 04sept20 CleanДокумент184 страницыWFP AF Project Proposal The Gambia REV 04sept20 CleanMahima DixitОценок пока нет

- API1 2019 Broken Object Level AuthorizationДокумент7 страницAPI1 2019 Broken Object Level AuthorizationShamsher KhanОценок пока нет

- 1-Introduction - Defender (ISFJ) Personality - 16personalitiesДокумент6 страниц1-Introduction - Defender (ISFJ) Personality - 16personalitiesTiamat Nurvin100% (1)

- Republic Act No. 9775 (#1)Документ6 страницRepublic Act No. 9775 (#1)Marc Jalen ReladorОценок пока нет

- C1 Level ExamДокумент2 страницыC1 Level ExamEZ English WorkshopОценок пока нет