Вам также может понравиться

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeОт EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeОценок пока нет

- IA2 Finals ReviewerДокумент6 страницIA2 Finals ReviewerJoana MarieОценок пока нет

- CFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)От EverandCFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)Рейтинг: 5 из 5 звезд5/5 (1)

- Management Advisory Services - Final RoundДокумент14 страницManagement Advisory Services - Final RoundRyan Christian M. CoralОценок пока нет

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)От EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Рейтинг: 4.5 из 5 звезд4.5/5 (5)

- Practical Accounting 2 - RMYCДокумент10 страницPractical Accounting 2 - RMYCZadharie Abby Gail BurataОценок пока нет

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsОт EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsОценок пока нет

- MA CUP PracticeДокумент9 страницMA CUP PracticeFlor Danielle Querubin100% (1)

- Pamantasan NG Cabuyao: Katapatan Subd., Banay Banay, City of CabuyaoДокумент5 страницPamantasan NG Cabuyao: Katapatan Subd., Banay Banay, City of CabuyaoLyca SorianoОценок пока нет

- Quiz 1 Inventory and InvestmentsДокумент7 страницQuiz 1 Inventory and InvestmentsMark Lawrence YusiОценок пока нет

- L 1Документ5 страницL 1Elizabeth Espinosa ManilagОценок пока нет

- Poem PoemДокумент5 страницPoem PoemElizabeth Espinosa ManilagОценок пока нет

- 1617 2ndS 3rde JonaldBДокумент11 страниц1617 2ndS 3rde JonaldBAlyssa Andrea SabinoОценок пока нет

- Jam QaДокумент7 страницJam QaVinluan JeromeОценок пока нет

- Qualifying Exam Reviewer Basic Accounting StudentДокумент10 страницQualifying Exam Reviewer Basic Accounting StudentAngelica PostreОценок пока нет

- Solutions Intangible Assets PDFДокумент16 страницSolutions Intangible Assets PDFSittie Ainna A. UnteОценок пока нет

- Special TransactionsДокумент5 страницSpecial TransactionsJehannahBarat100% (1)

- Ba 13 Final Departmental ExamДокумент9 страницBa 13 Final Departmental ExamKristine Joy Peñaredondo BazarОценок пока нет

- Usc Part 2020 (Far) - RetakeДокумент25 страницUsc Part 2020 (Far) - RetakeVince AbabonОценок пока нет

- Qualifying Exam Reviewer 2017 - Basic AccountingДокумент10 страницQualifying Exam Reviewer 2017 - Basic AccountingAdrian Francis95% (20)

- ACCO 20033 FAR 1 Departmental MidtermsДокумент5 страницACCO 20033 FAR 1 Departmental MidtermsNana LeeОценок пока нет

- Business Combination and Consolidated FS 2020 PDFДокумент22 страницыBusiness Combination and Consolidated FS 2020 PDFAPO 0005100% (1)

- Rmyc Cup 1 Addtl QuestionsДокумент15 страницRmyc Cup 1 Addtl QuestionsJasper Andrew AdjaraniОценок пока нет

- Review of Accounting Cycle Review of Accounting CycleДокумент4 страницыReview of Accounting Cycle Review of Accounting CycleJerome BaluseroОценок пока нет

- 102 Quiz 1 She 2020Документ6 страниц102 Quiz 1 She 2020Eunice MartinezОценок пока нет

- PDF Intermediate Accounting Volume 3 ValixДокумент4 страницыPDF Intermediate Accounting Volume 3 ValixJosh Cruz CosОценок пока нет

- Prac 2Документ10 страницPrac 2Fery AnnОценок пока нет

- Bfjpia Cup 3 - Practical Accounting 2 Easy: Page 1 of 10Документ10 страницBfjpia Cup 3 - Practical Accounting 2 Easy: Page 1 of 10Arah OpalecОценок пока нет

- No. of Rooms Ave, Monthly Rent Per Room Annual Rent Per RoomДокумент7 страницNo. of Rooms Ave, Monthly Rent Per Room Annual Rent Per RoomKimberlyОценок пока нет

- Intermediate Accounting Volume 3 ValixДокумент4 страницыIntermediate Accounting Volume 3 ValixVyonne Ariane EdiongОценок пока нет

- Cup 3 AFAR 1Документ9 страницCup 3 AFAR 1Elaine Joyce GarciaОценок пока нет

- Financial Statement AnalysisДокумент26 страницFinancial Statement AnalysisJade Gomez100% (2)

- Junior Philippine Institute of AccountantsДокумент18 страницJunior Philippine Institute of AccountantsBlessy Zedlav LacbainОценок пока нет

- Manila MAY 5, 2022 Preweek Material: Management Advisory ServicesДокумент25 страницManila MAY 5, 2022 Preweek Material: Management Advisory ServicesJoris YapОценок пока нет

- Work Cap QuizДокумент8 страницWork Cap QuizLieza Jane AngelitudОценок пока нет

- MGT Adv Serv 09.2019Документ11 страницMGT Adv Serv 09.2019Weddie Mae VillarizaОценок пока нет

- Auditing Theory and Problems (Qualifying Round) : Answer: DДокумент15 страницAuditing Theory and Problems (Qualifying Round) : Answer: DJohn Paulo SamonteОценок пока нет

- Quiz Conso FSДокумент3 страницыQuiz Conso FSMark Joshua SalongaОценок пока нет

- BBДокумент3 страницыBBJoshua WacanganОценок пока нет

- Answer Key POD Cup Jr. Final RoundДокумент6 страницAnswer Key POD Cup Jr. Final RoundRitsОценок пока нет

- National Federation of Junior Philippine Institute of Accountants Financial AccountingДокумент8 страницNational Federation of Junior Philippine Institute of Accountants Financial AccountingWeaFernandezОценок пока нет

- RESA 1st PBДокумент9 страницRESA 1st PBRay Mond0% (1)

- AFAR TestbankДокумент56 страницAFAR TestbankDrama SubsОценок пока нет

- Pre Board P1 Dec 2020Документ26 страницPre Board P1 Dec 2020k.balaga.513134Оценок пока нет

- FAR Qualifying Examination ReviewerДокумент5 страницFAR Qualifying Examination Reviewertutorjaime05Оценок пока нет

- BFJPIA Cup Level 4 P2Документ9 страницBFJPIA Cup Level 4 P2Blessy Zedlav LacbainОценок пока нет

- Advance AccountingДокумент5 страницAdvance AccountingChristopher PriceОценок пока нет

- AFARДокумент9 страницAFARRed Christian PalustreОценок пока нет

- Assignment Business CombinationДокумент2 страницыAssignment Business CombinationZarah H. LeongОценок пока нет

- Semi-Finals Financial Accounting and ReportingДокумент23 страницыSemi-Finals Financial Accounting and Reportingjoyce KimОценок пока нет

- FS Analysis Ans KeyДокумент5 страницFS Analysis Ans KeyTeofel John Alvizo PantaleonОценок пока нет

- Examination About Investment 12Документ4 страницыExamination About Investment 12BLACKPINKLisaRoseJisooJennieОценок пока нет

- Problem SolvingДокумент23 страницыProblem SolvingFery AnnОценок пока нет

- AC15 Quiz 1 Solution ManualДокумент8 страницAC15 Quiz 1 Solution ManualKristine Esplana ToraldeОценок пока нет

- Financial Asset ClassifiedДокумент6 страницFinancial Asset ClassifiedQueenie ValleОценок пока нет

- Quiz 1Документ6 страницQuiz 1Jonathan VidarОценок пока нет

- Bfjpia Cup 2 - Practical Accounting 1 Easy: Page 1 of 10Документ10 страницBfjpia Cup 2 - Practical Accounting 1 Easy: Page 1 of 10kristelle0marisseОценок пока нет

- Exercises - Capital Gains TaxДокумент12 страницExercises - Capital Gains TaxElla Marie Lopez80% (5)

- RESA - AFAR Preweek Lecture 2Документ15 страницRESA - AFAR Preweek Lecture 2MellaniОценок пока нет

- Practical Accounting TwoДокумент25 страницPractical Accounting TwoJoseph SalidoОценок пока нет

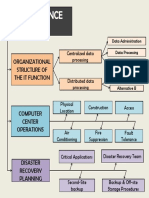

- Organizational Structure of The It Function: Centralized Data ProcessingДокумент1 страницаOrganizational Structure of The It Function: Centralized Data ProcessingRyan Christian M. CoralОценок пока нет

- Theoretical FrameworkДокумент1 страницаTheoretical FrameworkRyan Christian M. CoralОценок пока нет

- Management Advisory Services-Elimination RoundДокумент18 страницManagement Advisory Services-Elimination RoundRyan Christian M. Coral0% (1)

- Auditing Theory MCQs by Salosagcol With AnswersДокумент31 страницаAuditing Theory MCQs by Salosagcol With AnswersYeovil Pansacala79% (62)

- Audit Plan GuideДокумент4 страницыAudit Plan GuideRyan Christian M. CoralОценок пока нет

- AcadsДокумент4 страницыAcadsRyan Christian M. CoralОценок пока нет

- FinMan PDFДокумент7 страницFinMan PDFPrincess Engreso100% (1)

- Contents of A Good Research Proposal v1.0Документ2 страницыContents of A Good Research Proposal v1.0Bright Williams BoakyeОценок пока нет

- Management Advisory Services-Elimination RoundДокумент18 страницManagement Advisory Services-Elimination RoundRyan Christian M. Coral0% (1)

- 12 x10 Financial Statement AnalysisДокумент22 страницы12 x10 Financial Statement AnalysisRaffi Tamayo92% (25)

- 19 x12 ABC B Activity-Based Cost SystemДокумент15 страниц19 x12 ABC B Activity-Based Cost SystemJericho Pedragosa67% (6)

- Natalie WrightДокумент1 страницаNatalie Wrightapi-545483813Оценок пока нет

- Chap 16Документ29 страницChap 16Dyan IRОценок пока нет

- International Economics 16th Edition Thomas Pugel Test BankДокумент24 страницыInternational Economics 16th Edition Thomas Pugel Test Bankkhucly5cst100% (25)

- A Handbook On Private Equity FundingДокумент109 страницA Handbook On Private Equity FundingLakshmi811Оценок пока нет

- Busy Association BeckyДокумент11 страницBusy Association BeckySamuel L EОценок пока нет

- BBFS CorporateДокумент5 страницBBFS Corporatehasan_siddiqui_15Оценок пока нет

- o F Fortis HospitalДокумент15 страницo F Fortis HospitalPrakriti Sinha0% (1)

- ICGIM'2022 ProceedingsДокумент306 страницICGIM'2022 ProceedingsGuru Kandhan100% (1)

- Earlier This Month, Your Company, A Running Equipment Designer and ManufacturerДокумент2 страницыEarlier This Month, Your Company, A Running Equipment Designer and Manufacturermayank goyalОценок пока нет

- Hidden ChampionsДокумент20 страницHidden ChampionsAna-Maria Nastasa100% (1)

- Triana Saleh CVДокумент4 страницыTriana Saleh CVtriana saIehОценок пока нет

- Cost Behavior-Analysis and UseДокумент74 страницыCost Behavior-Analysis and UseGraciously ElleОценок пока нет

- Nature of TQMДокумент11 страницNature of TQMChristine SalazarОценок пока нет

- 7 Step Guide - ERP TransformationДокумент11 страниц7 Step Guide - ERP TransformationPaul Vintimilla CarrascoОценок пока нет

- Sap Modules Overview PDFДокумент32 страницыSap Modules Overview PDFRamonaIrofteОценок пока нет

- Anurag ShuklaДокумент23 страницыAnurag Shukladeepkamal_jaiswalОценок пока нет

- NewStudioNPVS Brochure 220726 EN FINALДокумент2 страницыNewStudioNPVS Brochure 220726 EN FINALmining engineerОценок пока нет

- Ms8-Set C Midterm - With AnswersДокумент5 страницMs8-Set C Midterm - With AnswersOscar Bocayes Jr.Оценок пока нет

- C6-Intercompany Inventory Transactions PDFДокумент43 страницыC6-Intercompany Inventory Transactions PDFVico JulendiОценок пока нет

- Venture DevelopmentДокумент21 страницаVenture DevelopmentRahul singhОценок пока нет

- 4QUIZДокумент3 страницы4QUIZMarilyn Nelmida TamayoОценок пока нет

- WorkdayДокумент22 страницыWorkdaysunnydeol4580% (5)

- Assets Current AssetsДокумент2 страницыAssets Current AssetsRIAN MAE DOROMPILIОценок пока нет

- KRU Affiliation Fee ChallanДокумент1 страницаKRU Affiliation Fee ChallansuryanetsОценок пока нет

- White Paper Start Ups EcosystemsДокумент9 страницWhite Paper Start Ups EcosystemsAndy PermanaОценок пока нет

- CMC Global - Offer Letter - Mr. Nguyen Huu Phuoc - 170122Документ1 страницаCMC Global - Offer Letter - Mr. Nguyen Huu Phuoc - 170122kamusuyurikunОценок пока нет

- Cloud Security Knowledge (CCSK) Foundation H8P75S: Audience Course ObjectivesДокумент3 страницыCloud Security Knowledge (CCSK) Foundation H8P75S: Audience Course ObjectivesGaaliОценок пока нет

- BW ExtractorsДокумент50 страницBW ExtractorsnagredyОценок пока нет

- Management Accountant Sep 2020Документ124 страницыManagement Accountant Sep 2020ABC 123Оценок пока нет

- Tourism Destination MarketingДокумент37 страницTourism Destination MarketingAvatar YuwonoОценок пока нет

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)От EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Рейтинг: 4.5 из 5 звезд4.5/5 (5)

- Finance Basics (HBR 20-Minute Manager Series)От EverandFinance Basics (HBR 20-Minute Manager Series)Рейтинг: 4.5 из 5 звезд4.5/5 (32)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindОт EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindРейтинг: 5 из 5 звезд5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)От EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Рейтинг: 4.5 из 5 звезд4.5/5 (13)

- Getting to Yes: How to Negotiate Agreement Without Giving InОт EverandGetting to Yes: How to Negotiate Agreement Without Giving InРейтинг: 4 из 5 звезд4/5 (652)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantОт EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantРейтинг: 4.5 из 5 звезд4.5/5 (146)

- Ledger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceОт EverandLedger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceОценок пока нет

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsОт EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsРейтинг: 5 из 5 звезд5/5 (1)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyОт EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyРейтинг: 4.5 из 5 звезд4.5/5 (37)

- The Credit Formula: The Guide To Building and Rebuilding Lendable CreditОт EverandThe Credit Formula: The Guide To Building and Rebuilding Lendable CreditРейтинг: 5 из 5 звезд5/5 (1)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?От EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Рейтинг: 5 из 5 звезд5/5 (1)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyОт EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyРейтинг: 5 из 5 звезд5/5 (1)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)От EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Рейтинг: 4 из 5 звезд4/5 (33)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!От EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Рейтинг: 4.5 из 5 звезд4.5/5 (14)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeОт EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeРейтинг: 4 из 5 звезд4/5 (21)

- Warren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageОт EverandWarren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageРейтинг: 4.5 из 5 звезд4.5/5 (109)

- I'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)От EverandI'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)Рейтинг: 4.5 из 5 звезд4.5/5 (24)

- Accounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)От EverandAccounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)Рейтинг: 4.5 из 5 звезд4.5/5 (5)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetОт EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetОценок пока нет

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelОт Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelОценок пока нет

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineОт EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineОценок пока нет

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesОт EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesОценок пока нет

- Contract Negotiation Handbook: Getting the Most Out of Commercial DealsОт EverandContract Negotiation Handbook: Getting the Most Out of Commercial DealsРейтинг: 4.5 из 5 звезд4.5/5 (2)