Вам также может понравиться

- Petition for Certiorari – Patent Case 01-438 - Federal Rule of Civil Procedure 52(a)От EverandPetition for Certiorari – Patent Case 01-438 - Federal Rule of Civil Procedure 52(a)Оценок пока нет

- A.M. No. 11-7-10-SCДокумент7 страницA.M. No. 11-7-10-SCEvangelical Mission College CommunityОценок пока нет

- RE COA Opinion 678 SCRA 1 (2012)Документ5 страницRE COA Opinion 678 SCRA 1 (2012)John OrdanezaОценок пока нет

- Per Curiam:: Custom SearchДокумент7 страницPer Curiam:: Custom SearchKim Laurente-AlibОценок пока нет

- Re Coa Opinion Am No. 11-7-10-ScДокумент6 страницRe Coa Opinion Am No. 11-7-10-ScAl FrederickОценок пока нет

- Proton Pilipinas Corporation v. Banque, G.R. No. 151242, June 15, 2005Документ8 страницProton Pilipinas Corporation v. Banque, G.R. No. 151242, June 15, 2005jessa abellonОценок пока нет

- Payment Due: DC: 10 July 2020Документ2 страницыPayment Due: DC: 10 July 2020angel santosОценок пока нет

- 1.0 PM Toyota Camry Price ListДокумент1 страница1.0 PM Toyota Camry Price Listdarren.ryan1988Оценок пока нет

- 1.0 PM (IPte) Toyota Corolla Price ListДокумент1 страница1.0 PM (IPte) Toyota Corolla Price ListEasy FurnishingОценок пока нет

- Policy RiteshДокумент2 страницыPolicy Riteshsmbcards50% (2)

- Fortitch Compre 2Документ7 страницFortitch Compre 2uas.jlagroupОценок пока нет

- Putrajaya OT 30%Документ7 страницPutrajaya OT 30%lokman hakimОценок пока нет

- IAS 38 HomeworkДокумент6 страницIAS 38 HomeworkSheilaОценок пока нет

- CIT v. Tata Iron & Steel Co. Ltd.Документ3 страницыCIT v. Tata Iron & Steel Co. Ltd.Saksham ShrivastavОценок пока нет

- Objection Deadline: June 2, 2009 4:00 P.M. Hearing Date: June 25, 2009 2:00 P.MДокумент3 страницыObjection Deadline: June 2, 2009 4:00 P.M. Hearing Date: June 25, 2009 2:00 P.MChapter 11 DocketsОценок пока нет

- Standard Insurance: Philippine British Assurance Co. IncДокумент4 страницыStandard Insurance: Philippine British Assurance Co. IncVince Felipe OlivarОценок пока нет

- AP07DR1510 EstДокумент2 страницыAP07DR1510 EstSåí Kûmã RОценок пока нет

- 1.0 PM (CC) Toyota Hiace Price List May 2022Документ1 страница1.0 PM (CC) Toyota Hiace Price List May 2022saarizal samsudinОценок пока нет

- 202253-2016-Autozentrum Alabang Inc. v. Spouses Bernardo20231212-11-294k3vДокумент10 страниц202253-2016-Autozentrum Alabang Inc. v. Spouses Bernardo20231212-11-294k3vCalista GarciaОценок пока нет

- GUILLERMO T. PILI JR.-SI-PCV-500579648 - RN-500218633 - Schedule PDFДокумент7 страницGUILLERMO T. PILI JR.-SI-PCV-500579648 - RN-500218633 - Schedule PDFPearl JoyОценок пока нет

- Cta 2D CV 07989 D 2013aug08 Ass PDFДокумент43 страницыCta 2D CV 07989 D 2013aug08 Ass PDFhgcisoОценок пока нет

- Proforma Invoice: Used Farm Tractors 1 7000.00 1 3700.00 1 5900.00Документ2 страницыProforma Invoice: Used Farm Tractors 1 7000.00 1 3700.00 1 5900.00Anerol CondoriОценок пока нет

- Qty Price Total PriceДокумент1 страницаQty Price Total PriceDump GandaraОценок пока нет

- CP Decision - Violations of RA9184Документ7 страницCP Decision - Violations of RA9184Abby ReyesОценок пока нет

- 9 ACCRA Investments Vs CA GR No. 96322 PDFДокумент9 страниц9 ACCRA Investments Vs CA GR No. 96322 PDFJeanne CalalinОценок пока нет

- Premium Calculation Worksheet For PrivatecarДокумент2 страницыPremium Calculation Worksheet For Privatecarप्रितम उत्तम लोखंडेОценок пока нет

- Benguet Corp. v. CIRДокумент7 страницBenguet Corp. v. CIRMika Aurelio100% (1)

- 202253-2016-Autozentrum Alabang Inc. v. Spouses Bernardo20170704-911-609ony PDFДокумент9 страниц202253-2016-Autozentrum Alabang Inc. v. Spouses Bernardo20170704-911-609ony PDFJNCОценок пока нет

- 05-01-19 Kristy Ann B. de VeraДокумент1 страница05-01-19 Kristy Ann B. de VeraFernando CabreraОценок пока нет

- Hyundai-Pricelist-2023 New With DP DJДокумент1 страницаHyundai-Pricelist-2023 New With DP DJDaniel Jhon GradoОценок пока нет

- ESTANISLAO v. CHINA BANKING CORPORATIONДокумент1 страницаESTANISLAO v. CHINA BANKING CORPORATIONJenina Clarisse B. PascuaОценок пока нет

- In Re:) : Debtors.)Документ24 страницыIn Re:) : Debtors.)Chapter 11 DocketsОценок пока нет

- Capital CostДокумент2 страницыCapital CostRajibDebОценок пока нет

- DTC Proforma Invoice (6) .PDF 6794Документ1 страницаDTC Proforma Invoice (6) .PDF 6794AshokОценок пока нет

- Service Estimate: CustomerДокумент2 страницыService Estimate: CustomerazharОценок пока нет

- Yap vs. COAДокумент5 страницYap vs. COATrishia TanОценок пока нет

- 1433 EstimateДокумент2 страницы1433 Estimatesnss.fmОценок пока нет

- United India Insurance Company Limited: WWW - Uiic.co - inДокумент2 страницыUnited India Insurance Company Limited: WWW - Uiic.co - inpmukundaОценок пока нет

- Price List For Peninsular Malaysia Effective From 15: UMW Toyota Motor SDN BHD (60576-K) June 2020Документ1 страницаPrice List For Peninsular Malaysia Effective From 15: UMW Toyota Motor SDN BHD (60576-K) June 2020Noryuhanis NasirОценок пока нет

- Quotation Sheet FormatДокумент2 страницыQuotation Sheet FormatpaobaguioОценок пока нет

- 3005 53561895 01 000Документ1 страница3005 53561895 01 000santoshganjure@bluebottle.comОценок пока нет

- Adobe Scan 12-Apr-2024Документ1 страницаAdobe Scan 12-Apr-2024furquan10010Оценок пока нет

- 1.0 PM IPte Toyota Corolla Cross Price ListДокумент1 страница1.0 PM IPte Toyota Corolla Cross Price ListAlexander LeeОценок пока нет

- United India Insurance Company Limited: This Document Is Digitally SignedДокумент2 страницыUnited India Insurance Company Limited: This Document Is Digitally SignedArjun Singh AОценок пока нет

- Penalties and Surcharges Incurred Due To Late Registration of Motor VehiclesДокумент4 страницыPenalties and Surcharges Incurred Due To Late Registration of Motor VehiclesDino De LeonОценок пока нет

- 4858 - ReportДокумент5 страниц4858 - ReportSanjay KumarОценок пока нет

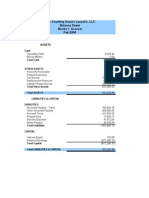

- Usa Courtney Downs Leaseco, LLC Balance Sheet Books Accrual Feb 2008Документ58 страницUsa Courtney Downs Leaseco, LLC Balance Sheet Books Accrual Feb 2008MarcyОценок пока нет

- 5.0 SWK (IPte) Corolla Cross Price ListДокумент1 страница5.0 SWK (IPte) Corolla Cross Price Listafieyz219Оценок пока нет

- CLM - Loa - Report - 2023-01-05T162055.948Документ3 страницыCLM - Loa - Report - 2023-01-05T162055.948Jaiden AlanaОценок пока нет

- 1.0 PM (IPte) Corolla Cross Price List PDFДокумент1 страница1.0 PM (IPte) Corolla Cross Price List PDFHaru BiruОценок пока нет

- Island Curtain 65-11023Документ1 страницаIsland Curtain 65-11023Gianni MicchiaОценок пока нет

- Bsa Prof 02: Preliminary Examination: Long Problem: 02Документ3 страницыBsa Prof 02: Preliminary Examination: Long Problem: 02Jalaine SalazarОценок пока нет

- Ruksar ZabiДокумент2 страницыRuksar ZabiMAA DURGA TVSОценок пока нет

- Smart Communications v. Astorga G.R. No. 148132Документ7 страницSmart Communications v. Astorga G.R. No. 148132shannonОценок пока нет

- Objection Deadline: 1017110 at 4:00 PM Hearing Date: To Be Scheduled Only NecessaryДокумент46 страницObjection Deadline: 1017110 at 4:00 PM Hearing Date: To Be Scheduled Only NecessaryChapter 11 DocketsОценок пока нет

- Federal Register / Vol. 64, No. 158 / Tuesday, August 17, 1999 / Rules and RegulationsДокумент6 страницFederal Register / Vol. 64, No. 158 / Tuesday, August 17, 1999 / Rules and RegulationsP MillerОценок пока нет

- 1.0 PM IPte Toyota Corolla Cross Price ListДокумент1 страница1.0 PM IPte Toyota Corolla Cross Price Listlynnda hamidОценок пока нет

- Cir Vs SM Prime HoldingsДокумент20 страницCir Vs SM Prime HoldingsMitch Arcones-GabineteОценок пока нет

- Case - Matter of BuschДокумент2 страницыCase - Matter of BuschSocОценок пока нет

- United MuslimДокумент10 страницUnited MuslimSocОценок пока нет

- Case - Dixie Coal MiningДокумент1 страницаCase - Dixie Coal MiningSocОценок пока нет

- Company Law of The People's Republic of China (2018 Revision)Документ50 страницCompany Law of The People's Republic of China (2018 Revision)Zulaine GuerraОценок пока нет

- Case - Arnold V PhillipsДокумент7 страницCase - Arnold V PhillipsSocОценок пока нет

- Division (GR No. 145368, Apr 12, 2002) Salvador H. Laurel V. Aniano A. DesiertoДокумент24 страницыDivision (GR No. 145368, Apr 12, 2002) Salvador H. Laurel V. Aniano A. DesiertoSocОценок пока нет

- PioneerДокумент14 страницPioneerSocОценок пока нет

- JosephДокумент4 страницыJosephSocОценок пока нет

- Case - Dixie Coal MiningДокумент1 страницаCase - Dixie Coal MiningSocОценок пока нет

- (GR No. L-24069, Jun 28, 1968) La Fuerza V. Ca: DecisionДокумент6 страниц(GR No. L-24069, Jun 28, 1968) La Fuerza V. Ca: DecisionSocОценок пока нет

- (GR No. L-24069, Jun 28, 1968) La Fuerza V. Ca: DecisionДокумент6 страниц(GR No. L-24069, Jun 28, 1968) La Fuerza V. Ca: DecisionSocОценок пока нет

- Cabugao v. People Summary: Dr. Ynzon Was Convicted of The Crime of Reckless Imprudence Resulting To Homicide. While The Case WasДокумент2 страницыCabugao v. People Summary: Dr. Ynzon Was Convicted of The Crime of Reckless Imprudence Resulting To Homicide. While The Case WasSocОценок пока нет

- Case - Arnold V PhillipsДокумент7 страницCase - Arnold V PhillipsSocОценок пока нет

- Republic V GonzalesДокумент2 страницыRepublic V GonzalesSocОценок пока нет

- RR No 12-2018Документ20 страницRR No 12-2018june Alvarez100% (1)

- EDCA Publishing V SantosДокумент3 страницыEDCA Publishing V SantosSocОценок пока нет

- DulayДокумент9 страницDulaySocОценок пока нет

- DulayДокумент9 страницDulaySocОценок пока нет

- PioneerДокумент14 страницPioneerSocОценок пока нет

- Republic of The Philippines V Acoje Mining FactsДокумент2 страницыRepublic of The Philippines V Acoje Mining FactsSocОценок пока нет

- LimbonaДокумент12 страницLimbonaSocОценок пока нет

- Second Division G.R. NO. 156294, November 29, 2006: Supreme Court of The PhilippinesДокумент7 страницSecond Division G.R. NO. 156294, November 29, 2006: Supreme Court of The PhilippinesSocОценок пока нет

- Menciano V San JoseДокумент9 страницMenciano V San JoseSocОценок пока нет

- Division (GR No. 111091, Aug 21, 1995) Engineer Claro J. Preclaro V. SandiganbayanДокумент19 страницDivision (GR No. 111091, Aug 21, 1995) Engineer Claro J. Preclaro V. SandiganbayanSocОценок пока нет

- Ca 146Документ1 страницаCa 146SocОценок пока нет

- Suan Ay Vs GalangДокумент3 страницыSuan Ay Vs GalangSocОценок пока нет

- Philippine FruitsДокумент8 страницPhilippine FruitsSocОценок пока нет

- A.M. No 02-11-12Документ3 страницыA.M. No 02-11-12SocОценок пока нет

- D - o - 40 I 15Документ8 страницD - o - 40 I 15SocОценок пока нет

- The Recent History of The Aromanians From Romania - Alexandru GicaДокумент32 страницыThe Recent History of The Aromanians From Romania - Alexandru Gicavaler_crushuveanlu100% (2)

- Ideal President Miriam SantiagoДокумент1 страницаIdeal President Miriam SantiagoMa Monica M. MuncadaОценок пока нет

- PV Checklist QuestionsДокумент1 страницаPV Checklist QuestionsSaTya PrakashОценок пока нет

- Introductory Lecture Foreign PolicyДокумент2 страницыIntroductory Lecture Foreign PolicyMazhar HussainОценок пока нет

- Art and History of Paris and Versailles (Art Ebook)Документ212 страницArt and History of Paris and Versailles (Art Ebook)x01001932100% (4)

- LandmarkДокумент5 страницLandmarkapi-3716851Оценок пока нет

- Mask Maker, Mask Maker: The Black Gay Subject in 1970S Popular CultureДокумент30 страницMask Maker, Mask Maker: The Black Gay Subject in 1970S Popular CultureRajan PandaОценок пока нет

- Role of Youth in Nation BuildingДокумент11 страницRole of Youth in Nation BuildingAnthony Robert XОценок пока нет

- Phil HistoryДокумент2 страницыPhil HistoryShena DionaldoОценок пока нет

- Entman and HerbstДокумент4 страницыEntman and HerbstBarbi GuibertОценок пока нет

- American Colonization in PhilippinesДокумент4 страницыAmerican Colonization in Philippinesarrowsin votigeorОценок пока нет

- Diniyat Level 8Документ170 страницDiniyat Level 8Jordan GinsbergОценок пока нет

- 3 Branches of The Government AssignmentДокумент3 страницы3 Branches of The Government AssignmentAlni Dorothy Alfa EmphasisОценок пока нет

- Kaine Military Spouse Provisions in FY19 NDAAДокумент2 страницыKaine Military Spouse Provisions in FY19 NDAAU.S. Senator Tim KaineОценок пока нет

- The School of The Archdiocese of Capiz Roxas City Capiz Worksheet in MC 1 Semester A.Y. 2020-2021Документ5 страницThe School of The Archdiocese of Capiz Roxas City Capiz Worksheet in MC 1 Semester A.Y. 2020-2021Janine May FabalesОценок пока нет

- Gmef Organizational Assessment Questionnaire-: Enabling MechanismsДокумент15 страницGmef Organizational Assessment Questionnaire-: Enabling Mechanismseva roslindaОценок пока нет

- LLC II EnglishДокумент2 страницыLLC II EnglishKapil KumarОценок пока нет

- Global Consumer CultureДокумент16 страницGlobal Consumer Cultureschole60100% (1)

- Complaint To NHRC Tibetian Students-1Документ4 страницыComplaint To NHRC Tibetian Students-1Kaustubh Das DehlviОценок пока нет

- Wwii Essay Topics0Документ3 страницыWwii Essay Topics0Jessica ZhaoОценок пока нет

- Lonzanida vs. Comelec, G.R. No. 135150, July 28, 1999Документ9 страницLonzanida vs. Comelec, G.R. No. 135150, July 28, 1999ArnelValdezОценок пока нет

- Mahatma Gandhi and Nonviolent ResistanceДокумент4 страницыMahatma Gandhi and Nonviolent ResistanceGrapes als Priya100% (1)

- Character Profiles Rear WindowДокумент2 страницыCharacter Profiles Rear WindowoskarОценок пока нет

- Society For American ArchaeologyДокумент21 страницаSociety For American ArchaeologyHawi CastanedaОценок пока нет

- 1) 15.1.2013 (Nat Ong's Conflicted Copy 2013-05-10)Документ4 страницы1) 15.1.2013 (Nat Ong's Conflicted Copy 2013-05-10)Cherie KohОценок пока нет

- O Socrealizmu (Jugoslovenski Spomenici)Документ5 страницO Socrealizmu (Jugoslovenski Spomenici)Re Born100% (2)

- Tourism Brochure ManilaДокумент3 страницыTourism Brochure ManilaKeeva TienzoОценок пока нет

- More Than A WallДокумент99 страницMore Than A WallLatino RebelsОценок пока нет

- (Middle East Today) Asma Afsaruddin (Eds.) - Islam, The State, and Political Authority - Medieval Issues and Modern Concerns (2011, Palgrave Macmillan US) PDFДокумент259 страниц(Middle East Today) Asma Afsaruddin (Eds.) - Islam, The State, and Political Authority - Medieval Issues and Modern Concerns (2011, Palgrave Macmillan US) PDFJoky Satria100% (1)

- Deoband MovementДокумент1 страницаDeoband MovementAffan AliОценок пока нет